Here are my Top 10 links from around the Internet at 10 to 12 pm, brought to you in association with New Zealand Mint for your reading pleasure.

I welcome your additions and comments below, or please send suggestions for Thursday's Top 10 at 10 via email to bernard.hickey@interest.co.nz.

I'll pop any surplus suggestions I get into the comment stream.

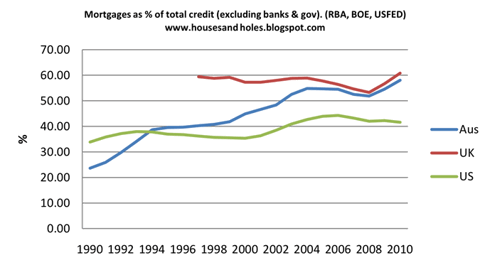

1. The Aussie housing and banking debate - Australian investment banker Leith van Onselen has again stirred up the debate about the Australian housing market and the exposure of Australia's banks again.

The banks deny there's a bubble and say stress tests show their balance sheets could handle a fall anyway.

But van Onselen says the banks are exposed to a liquidity shock. This isn't a surprising claim.

Many worry that the Australian banks borrow heavily offshore and they're vulnerable to a freeze on financial markets. Our own central bank has been working hard to wean the banks off this hot foreign funding.

But it's worth reading a reminder about this risk. HT Hugh via email.

The chart is a cracker. There are plenty more in Leith's detailed post, which I reckon is a must read.

offshore borrowings by depository corporations has exploded over the past 20 years, from around $50 billion in 1988 to nearly $700 billion currently. Currently, depository corporations have around $300 billion of short-term foreign borrowings maturing within 12 months, in addition to another $380 billion of longer-term foreign borrowings outstanding. Other things equal, this $300 billion of short-term foreign borrowings must be refinanced within 12 months just to maintain the current level of credit within the Australian economy (let alone increase it).

2. 'Did he really mean it?' - World Bank President Robert Zoellick's comments about some sort of gold basis for a new global currency system have caused a real stir. Was he really calling for a return to a gold standard? Possibly not, but he's up to something. Alan Bollard was particularly sceptical today, referring back to way a gold standard contributed to the Depression.

Here's Ryan Avent at The Economist trying to make some sense of it.

It seems like he's trying to work toward a solution to the problem of the dollar's international reserve status. As nearly everyone agrees, other currencies need to play a larger role in international reserves, but it's not necessarily easy to understand how this might take place. There are advantages to being the issuer of a reserve currency—interest rates are kept lower than normal, for instance.

But such status also tends to mean a relatively dear currency, not to mention international anger at attempts to allow the currency to weaken (which, in addition to generating a trade advantage reduces the value of foreign reserve holdings). And so countries' are a bit wary about achieving reserve status. This has led to calls for expansion of the SDR ("special drawing right"), a quasi-currency doled out by the IMF. But an effective global currency requires an effective global central bank, and there isn't one backing the SDR. So maybe that's the gap in the international monetary system that Mr Zoellick is seeking to fill with gold. But gold just isn't a magic bullet.

A real gold standard would likely be deflationary and would bring with it all the problems of any system of fixed exchange rates—stresses on reserves and loss of monetary independence among them. Broad fixed exchange rate regimes don't look that hot right now, given the significant struggles within the euro zone and the imbalances that have been generated within the dollar zone thanks to China's peg.

Gold makes for a lousy medium of exchange, and as I mentioned above, its expectation signalling properties aren't perfect or unique. The world will simply have to fumble its way forward on the reserve currency issue, perhaps focusing first on the development of regional reserve currencies.

3. 'Clueless and hopeless' - German finance minister Wolfgang Schäuble has become famous as a high profile official criticising the Fed's QE II.

“They have already pumped endless amounts of money into the economy with extremely high budget deficits, and with a monetary policy which has already pumped in lots of money. The results have been hopeless.” "[Our] successes are not the result of some sort of currency manipulation … The American growth model on the other hand is in a deep crisis. The US lived on borrowed money for too long, inflating its financial sector unnecessarily.”

Felix Salmon at Reuters thinks the G20 meeting this weekend will be fractious.

All of this is a recipe for fractiousness at the G20 meeting this week in Seoul. The unity we saw at the London summit in 2009 is a distant memory: no one, now, can even agree on what internationally coordinated action should look like, let alone actually get their respective parliaments to implement it. Which in turn means that G20 national economic policies are increasingly likely to work against each other than constructively with each other. It might well take another full-blown crisis before Germany and the U.S. are on the same page again.

4. What happens when you turn off the tap? - Bloomberg reports on what happens when a central bank pulls back from supporting a troubled credit market, just in case the European Central Bank, the Bank of Japan and the US Federal Reserve are wondering what might happen next.

Since the Swedish Riksbank became the world’s first central bank to end emergency loans just over a month ago, short-term interest rates have soared to the highest levels since January. The withdrawal of 300 billion kronor ($46 billion) of crisis loans has also sparked a selloff in the country’s mortgage debt market, which is twice the size of its government bond market.

The difference between mortgage rates and swaps last month rose to the widest since March, as Sweden’s covered-debt market slumped. The tensions in Sweden, which boasts the European Union’s smallest budget deficit, come as President Jean-Claude Trichet signals he’s undeterred in withdrawing the emergency measures the ECB introduced to fight the financial crisis.

The risk for Trichet is that too speedy an exit will switch off the flow of credit to cash-strapped banks in Ireland, Greece and Portugal, worsening a crisis across the euro region’s periphery. “The Swedish exit has proved that financial systems still are extremely vulnerable and that confidence is not that great,” said Andreas Halldahl, who helps manage about $15 billion in fixed-income assets at Storebrand Kapitalforvaltning AS in Stockholm.

“The implications for Europe could be severe if the ECB doesn’t handle things delicately.”

5. The other side of the debate - Martin Wolf at FT.com has written a piece defending the Fed's money printing. Here's his thinking.

It is hardly a surprise that Wolfgang Schäuble, finance minister of Germany, thinks differently. He describes the US growth model as in "deep crisis", adding that "it's not right when the Americans accuse China of manipulating exchange rates and then push the dollar exchange rate lower by opening up the flood gates".

Presumably, he believes that, in a proper world, the US would be forced to follow the deflationary route imposed upon Greece and Ireland, instead. This is not going to happen. Nor should it. Boiled down, the criticisms of the Fed come down to two: its policies are leading to hyperinflation; and they are "beggar my neighbour", in consequence, if not intention.

The first of these criticisms is not just wrong, but weird. The essence of the contemporary monetary system is creation of money, out of nothing, by private banks' often foolish lending.

Why is such privatisation of a public function right and proper, but action by the central bank, to meet pressing public need, a road to catastrophe? When banks will not lend and the broad money supply is barely growing, that is just what it should be doing

6. Even the World Bank is saying it now... - Bloomberg reports the World Bank is saying Asian countries may need capital controls to control the inflation bubbles being exported by America through its latest bout of Quantitative Easing.

Any curbs should be “targeted,” temporary and tailored to address specific problems, Sri Mulyani Indrawati, a World Bank managing director, said in an interview. This could include countries tying up funds for as long as a year to help limit hot-money, she said.

“Certain assets will become, potentially, bubbles,” Sri Mulyani said in Kuala Lumpur late yesterday. “The quantitative easing will create a lot of liquidity flooding to the East Asia Pacific region, because it is the most dynamic and attractive with a higher return on investment.”

Real-estate prices are a concern in China, Australia and parts of Southeast Asia, she said. Japan, Thailand and Malaysia have seen their currencies surge more than 10 percent against the dollar this year, while some of the region’s stock markets have jumped more than 50 percent, Sri Mulyani said. Sri Lanka’s benchmark stock index is up more than 90 percent this year, while the measures for Thailand and Indonesia have exceeded 40 percent, according to Bloomberg data.

7. ANZ joins CBA...sort of - Ralph Norris now has company as one of the least popular men in Australia. After raising CBA's floating mortgage rate by 20 basis points more than the RBA's official rate, Norris has been joined (sort of) by ANZ. The SMH reports the Mike Smith-led Aussie bank has lifted its floating rate by 14 basis points more than the RBA's hike, but it has also cut its exit fees.

In a move perhaps aimed at soothing that anger, the ANZ also announced today that it would scrap its mortgage exit fees. The change comes as the Australian Securities and Investments Commission is expected to hand down recommendations later today on exit fees – widely considered an obstacle for mortgage competition.

“Raising lending rates is never an easy decision and while we have taken a commercial decision to increase variable interest rates, we've also recognised that we need to take the lead in doing more to give customers' choice and to help them manage their finances in this uncertain interest rate environment,” said ANZ chief executive officer Australia Philip Chronican.

8. SanLu's toxic fallout - The Daily Telegraph reports that one of the parents of a Chinese child poisioned in the SanLu Melamine scandal has been jailed for "creating a disturbance" when warning other parents about the toxic effects of the milk.

HT Andrew via email.

A man whose five year-old son was poisoned during China's toxic milk crisis has been jailed for two-and-a-half years after he set up a website to warn other parents about the disease. Zhao Lianhai, a 38-year-old former employee of China's Food Quality and Safety authority, created the site in 2009 after more than 300,000 Chinese toddlers were poisoned, and at least six killed, by milk that was laced with melamine, an industrial chemical that made the milk appear more wholesome.

Mr Zhao told The Daily Telegraph that he was determined to spread information about melamine-poisoning so that parents in the Chinese countryside, who lived far away from hospitals, would be spurred to seek treatment for their children. However, as more and more parents began to call for justice and compensation, and Mr Zhao began to press their case publicly, he came to the attention of the Chinese authorities.

Last November, he was arrested by the police and then charged in March with "creating a disturbance". His lawyer, Li Fangping, said the evidence for the charge had been that Mr Zhao had given a media interview on a public pavement, held a dinner in a restaurant for a dozen parents of other victims, and that he had held up a small sign in protest outside a trial of milk company executives responsible for the poisoning.

9. Now they want gold too - China's demand for gold is helping push prices up, Reuters reports.

China, the world's largest consumer of base metals and the second biggest user of oil, is on gold bugs' radar screens, with any hint that Beijing may want to boost its gold holdings rippling through international markets, sending bullion higher. So far China's central bank has shied away from the international market and has instead been building reserves from its domestic mining industry, the largest in the world.

But that may change after the People's Bank of China said in August it would let its banks export and import more gold in a program to drive the development of the country's market in the precious metal. By opening up the market, the PBOC may be able to draw tonnes of gold into China, which it could then pick up on the domestic market, without disrupting market equilibrium too much.

10. Totally irrelevant video - Jon Stewart looks at Barack Obama's trip to Asia.

| The Daily Show With Jon Stewart | Mon - Thurs 11p / 10c | |||

| Let's Go Anywhere - Lonely President's Guide to Getting Out of the Country | ||||

|

||||

12 Comments

Here's the WSJ on the problems in Ireland. A sample of the rotten detail at the core of an insolvent state.

HT Tristan via email

http://online.wsj.com/article/SB100014240527487045064045755923603344570…

In early 2010, Mr. McDonagh's team got a rude surprise upon diving into the books.

"We opened it up and said, 'Oh, my God,"' Mr. McDonagh said in an interview. "What they are telling us is not the reality."

The banks had said they had loaned 77% of the value of a property, on average. The other 23%, put up by the borrower, would cushion a default.

The NAMA teams found that banks often piled on "equity releases" that amounted to lending out 100% of the value, and left them fully responsible in a default.

Worse, much of the collateral was shaky. Several times, a developer pledged future profits on other ventures. Many loans were riddled with flawed documentation, leaving banks without solid legal rights to the property they had believed was backing up the loans.

cheers

Bernard

It may still be Wednesday here in the Phils , but youse guys has crossed the dateline into Thursday !

Yer can't con me with your journalistic tricks , Bernard , I was employed at Fairfax too .

Hey , you that old thing about women screaming and falling to pieces when they spot a mouse in the house ; well it works when they're butt naked and there's a hefty great frog in the shower , too ................ Shit that was funny !

[ the Hero gently released the culprit into the jungle , unharmed , ribbit ribbit ]

Now are you sure you released the right one back into the jungle Gummy...!

By the light of dawn I do believe that you're correct Wolly , she does look greener and slimier than usual ................. ooooooooooooops !

President Aquino must've been listening to Chicken-Little Hickey , 'cos the Philippines announced an introduction of currency controls .............. the insanity spreads .

There is no " Currency War " ! ............. It is a mere fiscal figment of furtive financial journalists' fecund thinking .

Interesting and alarming...comments from Bollard on the other article BH posted.

"The RBNZ said in the report that a further weakening in the recovery had the potential to generate further loan losses in the banking system.

“House sales have stalled for the past six months and there are signs of prices falling again. Were this to be accompanied by renewed weakness in the labour market, some mortgage borrowers would find themselves in a position of financial stress,” it said.

“Furthermore, the banking sector remains heavily exposed to developments in the agricultural sector. Strong increases in commodity prices over the past year have boosted the cash flow position of many farms,” it said.

“Nevertheless, agricultural land values have been falling and farm sales volumes are very low. Any material drop in commodity prices could expose relatively indebted farms in the sector to significant stress.”

"Any material drop"........think about that.......you have to start seeing mortgage debt in the same way you would a redback spider in your pocket.

Thanks for all the extra time you would have needed to put into into yesterdays news. Been a follower of your views even when you were with Fairfax. Very helpful

Zillow - US house price declines accelerating, on course to equal length of decline seen during Great Depression:

http://www.zillow.com/blog/research/2010/11/09/it%E2%80%99s-going-to-be…

As fast as Bernanke is creating money, it is simultaneously being destroyed in the threshing machine which is the declining US housing market.

By the way wasnt there some smart Alec on here a few months back posting about how his company was picking up loads of cheap US property (West coast I recall) 'at the bottom' and how they were going to make a killing as the market recovered?

Knife. Falling. Never. Catch.

i just got back from a trip to vancouver and seattle. house prices in vancouver still seemed pretty high, and things were reasonably buoyant. tv was still riddled with property shows

the 'states was a different story. every shop was discounting heavily. retailers i spoke to said it was slow and that people were starting to understand that things were going to change in a big way but they weren't sure how. lots of closing down sales. not so much in the way of property shows on telly

A couple from me:

Al Gore’s Climate Exchange Utterly Fails… Media Ignores It All

http://neuralnetwriter.cylo42.com/node/3839

Al Gore’s much ballyhooed Chicago Climate Exchange (CCX) has recently announced that it will no longer be engaging in carbon trading, an activity that was the sole purpose that it was created. This is an utter failure of purpose in global warming hysteria yet the Old Media is almost completely silent on this colossal failure.

Why has the media remained utterly quite on this abject failure after unleashing on the public an avalanche of stories that touted the creation of the CCX back in 2000 — and since for that matter?

=========

Re Robert Zoelick on Gold, there seems to be much ignorance and misinformation.It's most likely IMO he's talking about something like "Freegold". This has been much discussed on my website, and the main proponent is FOFOA who bases his articles/views on the writing of Another & FOA.

The idea in its simplest form is:

1. Gold is allowed to float freely.

2. It serves as a store of value in parallel to the currencies that act as medium of exchange.

The store of value function of gold then acts as a limiter on the excesses of the medium of exchange.

This is NOT a gold standard.

For more details:

What is "Freegold"? Is it a free oz of gold in every cornflakes packet, or is it a liberated gold market, free of constraints?

http://neuralnetwriter.cylo42.com/node/3052

Hi Steve,

I must be slow today, as I can't understand your thing about FreeGold.

You said it means two things:

1. Gold is allowed to float freely.

2. It serves as a store of value in parallel to the currencies that act as medium of exchange.

Well, gold IS free floating against all (free floating) currencies and indeed against all commodities.

In addition, it already IS a store of value - just ask any gold bug, but also witness the reserves held by central banks.

Clearly there is something more here than I am appreicating?

Thanks,

Alan.

Hi Alan,

I'll try and answer your question, although my time is very limited right now and it's a complicated subject.

Gold is not free at the moment:

1. There is real physical gold, and there is paper gold. The paper gold exceeds the real physical gold, and greatly affects (to the downside) the "price". The paper gold increases the apparent supply.

2. Gold reserves are not "priced" at current rates by most central banks. Europe is one notable exception, where the gold reserve value reflects the current "price".

As such gold has not served as well as it should have as a store of value.

The reasons are easy to see, the bankers prefer their fraudulent paper (freaudulaet because the paper currencies derive from gold receipts which they then started creating in excess of the gold they held, which was the original fraud). Governments prefer the paper notes because it enables them to spend the inflated currency first and tax less, enabling them to spend more while hiding some of their taxing with inflation and the resulting rising prices.

The reason they have a lower price rise target of 2 to 3%/year is because that enabled them to stealth tax via inflation without people realising.

Thus gold is the enemy of the bankers and the goverments.

That's the best I can do in a short time.

Bernard claims to have an "algorithm" for preventing naughty words. I think you actually have a simple word checking module. Let's see who is right :)

SLUT - this shouldn't get through

S L U T - I bet this does

S-L-U-T - And I bet this one does also.

Then of course there are the more tricky ones:

Some

Lucky

Uncle

Terry

LOL

====

Disappointed, it appears SLUT isn't even a naughty word :( :( :(

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.