By Sheryl Sutherland*

It’s crucial to understand the trade-off between risk and return. Higher risk is associated with higher return, lower risk with lower return. Historically market-linked funds have provided the highest long-term returns, but have also shown the highest losses over short-term periods. At the other extreme, cash management funds are among the safest when it comes to stability, but they have provided the lowest long-term returns. Some important risks to consider include the following.

• Market risk – the prices of shares or government stock can move up and down dramatically. This can be eased, but not eliminated, by investing in more than one asset class.

• Interest rate risk – government stock and some fixed interest securities can rise or fall because of changes in interest rates. When interest rates rise, government stock prices fall; conversely, when interest rates fall, government stock prices rise. This risk can be minimised by holding shorter-term fixed interest securities.

• Income risk – as interest rates change so can the income provided by fixed interest securities.

• Inflation risk – rising prices due to inflation can erode the value of investments. Over long periods share market investments have beaten inflation by a larger margin than fixed interest investments.

• Currency risk – fluctuations in the value of foreign currencies can hurt or help the performance of investments.

• Manager risk – investment managers can make poor decisions that reduce the value of your investment – diversification between fund managers will reduce this risk.

To read the first part of Sheryl's series on getting started click here.

To read the second part of Shery's series on goal setting, click here.

There is no way to eliminate these risks entirely but there are ways to reduce the overall risk of your portfolio. Two of the simplest are holding a balanced portfolio with some investments in each asset class, and aligning your investments with your various financial goals. Money needed in the near future should be kept in cash management or fixed interest funds. Money that will not be needed until later may be invested more aggressively, say in share market or commodity linked funds.

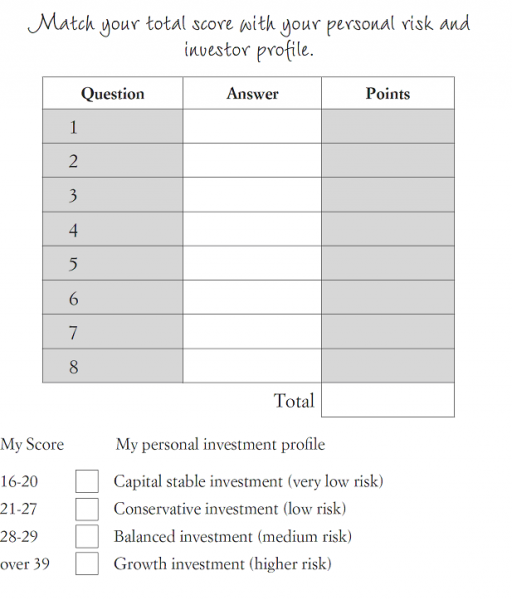

Read the eight questions below and tick the statement that best resembles you, selecting only one option. You will use your answers to these questions to determine your investment profile in Step 4, below.

Your financial ability to handle risk:

1 The following percentage of my income is spent on debts, eg credit cards, car repayments, rent or mortgage payments:

a) More than 33 per cent;

b) Between 10 per cent and 33 per cent;

c) Less than 10 per cent.

2 If there was an emergency, I would have savings available to pay:

a) Less than 2 months of living expenses;

b) 2 to 4 months of living expenses;

c) 5 months or more of living expenses.

3 Losing my job or facing a large financial burden in the next year is:

a) Somewhat likely;

b) Not very likely;

c) Not at all likely.

4 I will change to another investment if:

a) There is a drop in the value of my investment;

b) The value drops by 20 per cent in a given year;

c) It doesn’t bother me if my investment drops in value. I might even buy more since prices are lower.

5 I currently invest most of my money in:

a) On-call savings account or term deposits. They don’t pay a lot of interest, but I know my money is secure.

b) Blue chip shares, rental property, managed funds such as unit trusts that are pretty reliable, or high quality corporate bonds.

c) Predominantly small company shares or aggressively managed funds. Even though I could lose money, I like to invest in opportunities that could bring a very high return.

6 The following statement best describes my investment objectives:

a) I prefer to put my money in a secure account, one where my money is absolutely safe, even if this means I earn a lower rate.

b) I prefer investments that show steady growth, but I want to beat inflation so I’m willing to assume some risk.

c) I prefer a more aggressive mix of investments, some with moderate growth, but mostly those with higher risk and the chance for the highest returns.

7 What type of return would you expect from your investment?

a) Regular income;

b) Both income and capital growth;

c) Mainly capital growth.

Finding your investment time horizon

Consider what your primary investment objective is:

Retirement planning.

Estate planning.

Education funding.

Funding a holiday.

Buying a new home.

Other ____________________________

8 Based on your investment time horizon, how soon will it be before you expect to need your money?

a) 1 to 4 years;

b) 5 to 10 years;

c) More than 10 years.

Your investment profile

To determine your investment profile, write the letter corresponding to your answers in the box below next to the appropriate question number. Then enter the score for that answer in the box on the right, where a = 2, b = 4 and c = 6.

Risk Management

As Robbie Burns said, ‘The best laid plans of mice and women gang aft agley’, which in English means we need to plan for the unexpected. There is no point in creating a plan that could be derailed by an event such as a major illness – a serious illness means your financial security could be threatened. Disability income insurance is essential, as is superannuation. Life insurance is also important if you have dependents who may be financially compromised on your death. Complete the following exercises to help you make a decision on your insurance needs.

Risk Management Checklist

Life Insurance

To provide a cash sum on my death or the death of my partner

Mortgage repayment insurance

To provide mortgage repayment protection.

Income protection

To provide a monthly income in the event of disablement through illness or injury.

Major trauma

To provide a cash sum on diagnosis of a defined critical illness, e.g. stroke, cancer, kidney failure, heart attack, blindness.

Total and permanent disablement

To provide health insurance benefits.

Health insurance*

To provide health insurance benefits.

Life Cover Calculation

How much Life Cover is needed? This provides an indication of how much cover may be required to provide security for a family.

Assets Liabilities

Life insurance _________ Mortgage _________

Bank account _________ Hire purchase _________

Savings _________ Credit cards __________

Shares _________ Other debt __________

Unit trusts _________

Superannuation _________

Other investments _________

Investment property _________

Total: _________ Total: _________

(Assets do not include the family home as this is needed for family dwelling)

Amount of weekly income required by surviving partner: _________

(Can be reduced from current income by amount of mortgage repayments)

Amount needed for Education Fund: _________

Multiply the weekly income by 52 to provide a sum to allow family to live for one year until investments produce annual income: _________

Lump sum needed to provide ongoing income. _________

How much is needed to provide annual income at current conservative interest rates, say 7 per cent. (Annual Income / 7*100) _________

Calculation to establish amount of Life Assurance required

Liabilities: _________

Education Fund: _________

One year of income: _________

Lump sum to provide ongoing income: _________

Financial Needs, Total: _________

Less Assets: _________

Total Additional Cover Required: _________

This calculation is obviously dependent on each individual’s requirements. When you take out life insurance in a partnership, it is important to cross-assign the policies, by this I mean that your partner owns the policy over your life and you own your partner’s policy. On your death the proceeds are then paid directly to the policy owner on probate rather than being paid into your estate. It is difficult enough to cope with the death of a loved one, without coping with money worries as well.

*I find some clients prefer to use investments rather than pay premiums for health insurance thus creating the large sums needed for medical care. Their argument is that the insurance premiumswill build a nest egg that will cover the health care costs. As with all insurances, compare cost with values received. Don’t be scared to use an adviser.

Sheryl Sutherland is director of The Financial Strategies Group and co-author of Smart Money, and author of Girls Just Want to Have Funds and Money, Money, Money, Ain't it Funny.

2 Comments

Reading your very professional advices – I think I have to be careful – it seems I'm all wrong - in slowly catching the “Winter Gold Bug” of 2012.

Gold - back up US$ 2’000.- p/oz soon.

Stability and choice - "THE NZ GOLD DOLLAR"

Recommended for Bernard and team and other experts: Listen to Dr. Bruno Bandulet – could be an interesting concept for New Zealand.

http://www.youtube.com/watch?v=GXC44l942bE

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.