ANZ’s former chief economist, Cameron Bagrie, is wary of the Reserve Bank’s (RBNZ) bank capital proposals turning it into a punching bag.

He maintains the RBNZ is copping too much flak for the dairy farming industry’s woes - many of which have nothing to do with the RBNZ consulting on requiring banks to hold more capital.

Bagrie accepts that if implemented, the RBNZ’s proposals will come at a cost. Yet he’s concerned some of the lobbying against the proposals have conflated what could happen with what’s already happening.

Federated Farmers’ economics and commerce spokesperson Andrew Hoggard last month, for example, told interrst.co.nz: "It is certainly concerning that banks seem to be acting prematurely on what are proposals for consultation.”

Dairy dilemmas external to potential bank capital changes

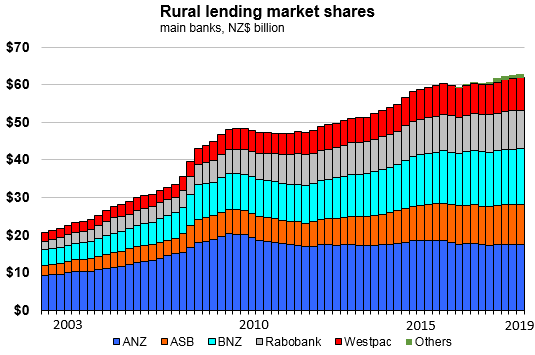

Bagrie, who now runs a consultancy called Bagrie Economics, stressed to interest.co.nz the fact that banks are already restricting their lending. The dairy sector’s been particularly vulnerable to their changes of appetite because it’s highly leveraged.

Indeed, the RBNZ in its latest Financial Stability Report said that 35% of dairy sector debt was to “highly indebted farms”, defined as farms with more than $35 of debt per kilogram of milk solids produced annually.

Bagrie was concerned the sector is trying to pay down $41 billion of debt at the same time Fonterra’s deleveraging. He said the sector’s net equity position is falling, with dairy land prices on the decline.

Fonterra, in a statement made to the NZX last week on its soft share price, warned: “While the share price does not impact the Co-op’s balance sheet or our ability to operate and pay our bills, it does impact our farmers’ balance sheets.”

If farmers have weaker balance sheets, the value of what dairy loans are secured against falls.

“I do not like some of the signals that I’m seeing at the moment in regard to Fonterra’s share price,” Bagrie said, also noting Fonterra is losing market share.

He said about a third of dairy farmers weren’t making money even with the pay-out being in excess of $6 per kilogram of milk solids.

He didn’t believe milk production would increase over the next decade. What’s more, he said uncertainty over government policy and environmental standards was translating into uncertainty over costs.

“There’s a whole array of complicating issues across the sector… It’s a bit of a perfect storm.”

Bagrie said the sector was being “repriced”, having been “mispriced for risk for a long time”.

“And now I think a few chickens are coming home to roost.”

What adding bank capital changes to the landscape could do

Asked how much more aggressive be believed this “repricing” would be if the RBNZ implemented its bank capital proposals, Bagrie said it was difficult to say at this stage.

“Is there going to be a cost for holding more capital? Yes. Some interest rates will be higher than would otherwise be the case.

“Can we come up with some hard and fast numbers? No. We’re in proposal stage.

“It concerns me how some of the conversations are starting to be shaped…

“There just seems to be this attitude across the financial services sector that borrowers are going to wear all the costs. If borrowers wear all the costs, that tells me there is something fundamentally wrong with the competitive landscape across the banking sector in New Zealand.”

Bagrie said the return on equities of banks operating in New Zealand were “right up there” by international standards and could come down a bit.

“The banks are still going to make a pretty hefty return on their equity. We want banks to be profitable, but I do not agree with getting out there and just saying this is going to be the impact and there are going to be big numbers.”

Bagrie, went further on TVNZ's Q + A programme to say that he believed banks were “scaremongering”.

'Next asset price correction could be a belter'

Bagrie said a bit of "tinkering" was required to the RBNZ's proposal to require banks to hold an additional $20 billion over a minimum of five years.

Yet he said the RBNZ was “in the right area in the spirit of what it's trying to do" and it still had to be a "big number".

Bagrie stressed how the 2008 Global Financial Crisis, which happened at a time the RBNZ had more monetary policy ammunition than it does now, showed how vulnerable New Zealand's banking system was.

"The GFC exposed a fundamental weakness of the NZ economy which is insufficient savings to fund our investment/borrowing needs," he said.

"Banks remained profitable but a lack of access to foreign capital as credit markets froze made life very difficult for the banking system.

"Aggressive interest rate cuts helped stabilise the NZ and global economy which stopped asset prices falling too far and threatening the banking sector.

"Banks are still very reliant on foreign capital markets to fund a domestic savings shortfall and this remains a point of vulnerability for the banking system in NZ.

"A key issue now is what happens if we experience another GFC? Global interest rates are already incredibly low and fiscal firepower across the G7 is low. China has heavy corporate debt levels.

"The next asset price correction could be a belter."

12 Comments

"He said about a third of dairy farmers weren’t making money even with the pay-out being in excess of $6 per kilogram of milk solids"

Not over leveraged courtesy of bank lending by chance?

"The next asset price correction could be a belter."

Understatement.

A realignment to real income and return on investment principles would mean a vast majority are insolvent

And then the deflationary spiral begins

The article is significant in that it ties together the main cross-winds affecting one of our major export earners:

- High debt, being repaid albeit at a time of low interest rates

- Uncertainty over environmental legislation (RMA, N and P loadings, Zero Carbon, vehicle feebates, Regional Council tightening)

- Market uncertainty as to prices, against a static volume of production

- Assets price (of FSF shares, dairy land) uncertainty and hence lender reluctance to roll over borrowing against lower collateral

- Structural and management issues, writ large, for the main cooperative (Fonterra) and at least one lesser one (Westland)

If the Dairy Golden Goose is cooked, Tourism is increasingly the next in line (too much carbon and too many loopies). So Pop goes a majority of export earnings, if these cross-winds turn into raging head-winds. Which, as we have seen with the Oil and Gas debacle, could easily turn on a Captain's Call....

"Banks are still very reliant on foreign capital markets to fund a domestic savings shortfall and this remains a point of vulnerability for the banking system in NZ.

Utter nonsense.

Rebuttal:

I-4 We need to save in order to fund investments that are the precondition of economic growth and development. If domestic savings are insufficient, we need to borrow from abroad or attract foreign investment.

The fourth pillar of the central bankers’ narrative has been the claim that nations that would like to develop and grow the economy need to accumulate scarce savings first, in order to fund the necessary investments. To attract these scarce savings, interest rates are needed, linking into claim 1. Moreover, since many developing countries were seen to have insufficient savings, the central banking narrative maintained that they needed to borrow the necessary funds from abroad. Thus it was fortuitous – if not serendipitous – that at the very moment when the developing countries had been educated into understanding their need of foreign borrowing, it just so happened that foreign bankers stood ready to engage in this selfless task. This need to borrow from foreign bankers has been the basis for postwar IMF and World Bank policies that drove home this point with developing countries over the past decades – if, that is – and this is a major caveat – they were in possession of attractive assets, such as raw materials and resources that are needed by industrialised countries. (Notice that countries without attractive assets never got into debt, because nobody would lend to them in the first place; likewise it was always a little curious that the global financiers at JP Morgan and other big global banks, the world’s experts in the latest derivative instruments, genuinely believed that developing countries like Ghana or Sudan were in fact much better at managing foreign exchange risk than the top teams at JP Morgan – for why else would the global bankers insist on lending to the eveloping countries in foreign currency, leaving any hedging to their exposed customers?).

II-4. We do not need to save or borrow from abroad in order to expand investment and growth

A basic argument by economists has been that we first need to accumulate scarce savings in order to fund investments and hence enjoy economic growth – or alternatively borrow those savings from abroad by taking a loan from the international banking community. But this argument is based on the erroneous belief that banks are merely financial intermediaries that require savings first in order to be able to lend money out. In reality, increased domestic investment requires neither savings nor borrowing from abroad. Domestic banks can fund domestic investment without prior savings becoming available.

Once we realize this, the power of the bankers crumbles. It has been their ploy to pretend that they were issuing what is a very scarce and precious resource – savings or money. For if it was not scarce, why should we be prepared to pay the bankers for this service (in the form of interest)? Governments could just create their own money, without having to pay interest on the national debt (which by now in a number of countries takes up the majority of national annual budgets – usually well hidden from the eyes of the public, by publishing only the fiscal budgets that are considered “discretionary spending” – pretending that interest payments are non-negotiable and compulsory). Or in the words of Leo Tolstoy (paraphrased): The reason why economists single out ‘labour’ and ‘capital’ in their ‘production function’ is, firstly, because they want to charge for ‘capital’ (interest), justifying it as being equivalent to the wages that workers get, and secondly, because nobody has figured out how to charge for the sun light, the air and other necessary factors of production. And they can only charge for ‘capital’, because economics has been designed to create the myth of its scarcity.

That money is not in fact a scarce resource, but a tool that can and should be employed by governments as benefits communities and nations is also true for developing economies and emerging markets: the “Third World Debt Crisis” was unnecessary, since for most purposes the affected countries did not need to borrow money from the foreign bankers in order to grow their economies. Worse, the foreign money from the foreign currency-denominated loans given to developing countries never even reached the borrowing economy’s borders. This is because it is one of the rules in international banking that pound sterling bank money stays with UK-authorised banks, euros stay in eurozone economy banks and US dollars remain with US banks. A so-called “US dollar deposit” in the UK is in actual fact a deposit with a US bank that is crediting the account of its UK respondent bank with this amount. Thus when a developing country borrowed from the international banks, they invariably lent dollars, pounds, euros or other currencies of industrialised countries, because the foreign bankers can only create foreign money (and they do create it out of nothing). The cruel joke on developing countries is now that those foreign dollars or euros that they borrowed will always stay abroad, in their respective foreign banking systems.

It is of course possible to sell the foreign currency and purchase domestic currency with it – but that only results in domestic bank credit creation, something that can be undertaken without getting indebted to foreign bankers in foreign currency in the first place – while it is the borrowers who are made to shoulder the large foreign currency risk. As the currencies of developing countries invariably fall over time against those of industrialised countries, they quickly get stuck in a foreign debt trap, unable to service or repay the foreign debt which is spiraling out of control in domestic currency terms. That is when the foreign vultures move in and demand ‘debt for equity swaps’, handing over valuable domestic assets, land, mines, mineral resources or mining rights, from poor countries to the rich foreign bankers, who had in any case simply created the money out of nothing. The developing country debt is in fact a form of predatory lending to ensure that the former colonies remain, in economic terms, in the hands of their former masters – if they have attractive assets, that is. Most of all, the round-trip via foreign banks is wholly unnecessary, if the borrowing nations want domestic currency: that is only created by their own banking system.

Thus it is becoming apparent that the central banking narrative of scarce money and scarce savings has been a hoax. This has become particularly obvious since central banks have opened all taps and created trillions of dollars and euros and handed them over to the big banks and large-scale financial speculators – under the pretense that this is ‘necessary’ or would somehow benefit society at large. (Their definition of this activity as ‘quantitative easing’ is also designed to mislead: the original thrust of quantitative easing is an expansion in credit creation for the real economy, not mainly for the financial markets – see my writings on this in Japan in the mid to late 1990s, or Voutsinas and Werner, 2011; Lyonnet and Werner, 2012; Werner, 2013).

which all ties into the Petrodollar ... Ultimately its not money you need to develop your economy. Its Oil.

and you must buy in US$ ... which holds demand for US$ up whatever deficit the big boys are running ...

so they print, while you pay in real resources ... (the real resources/output are the local "savings"that must be generated)

"Banks are still very reliant on foreign capital markets to fund a domestic savings shortfall and this remains a point of vulnerability for the banking system in NZ. >

I remember highlighting this some time ago and David Chaston quickly pointed out to me that mortgage lending in NZ was on the whole funded internally by domestic deposits.

Nonetheless, the RBNZ had this to say:

Banks’ offshore funding is typically issued in foreign currency. The banking system currently has around $100 billion of foreign-denominated debt liabilities, primarily in US dollars and euros. Banks use derivatives to hedge their foreign exchange (FX) risks. Around 95 percent of their offshore FX borrowing is hedged, with most of the remainder ‘naturally’hedged with foreign currency assets. FX risk is largely eliminated by these hedges, but risks can emerge in some circumstances (see box A). Link- page 14 (20 of 48) PDF

Beside the point that debt liabilities are hedged. Do you really believe that banks would be so free and easy with lending if their funding was wholly derived from domestic liabilities (deposits)? It's fair to say that the Aussie banks have been on a gravy train because of offshore funding. Now also consider the extent to which Aussie banks are also important for superannuation. Do you think this is a good thing if shareholder returns fall substantially in the current environment?

Do you really believe that banks would be so free and easy with lending if their funding was wholly derived from domestic liabilities (deposits)?

Why not? It's simple and approved under law:

https://www.sciencedirect.com/science/article/pii/S1057521914001434

https://vimeopro.com/bankofengland/research/video/332687750

Furthermore, regulatory capital requirements are asset dependent.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.