*This is the third article in a series on Visa, Mastercard, banks and New Zealand's retail payments systems. Parts one and two can be found here and here. Note the research for this article was done in February and early March, prior to the battle against COVID-19 superseding everything else.

By Gareth Vaughan

It's a complicated business this interchange.

To recap: An interchange fee is a fee charged by the financial institution on one side of a payment transaction to the financial institution on the other side of the transaction. A typical card transaction involves four parties the cardholder, the cardholder's financial institution (the issuer), the merchant and the merchant's financial institution (the acquirer). For most card transactions, the interchange fee is paid by the acquirer to the issuer.

Visa and Mastercard point out interchange doesn't generate revenue for them. However it underpins and grows their networks, meaning more transactions for them to clip the ticket on. And critics argue it drives up costs for merchants and ultimately consumers too with Retail NZ, the retailers' lobby group, describing "a wealth transfer from New Zealanders to foreign-owned banks and credit card companies."

Typical bank guidance for merchants, such as Westpac New Zealand's, features long lists of varying prices for different categories as demonstrated below.

Interchange is typically the biggest part of a broader fee known as the merchant service fee (MSF). Each bank sets its own interchange rates within a cap set by Visa and Mastercard. The MSF is set by banks. Through these fees a percentage of each sale is paid to the merchant's bank for the processing of the merchant's monthly transactions.

"Your MSF will be different depending on things like what type of business you have, how many transactions you process, and what card types you accept," Westpac explains.

The variable interchange fees set by Visa and Mastercard depend on the nature of the transaction, card type, merchant industry and processing environment for the transaction, according to Westpac.

"For example, a contactless card transaction may have a different fee to a chip and PIN transaction. The interchange fee can be calculated as a percentage of the transaction value, or set as a fixed dollar amount...Interchange makes up the bulk of the Merchant Service Fee."

Did I say this was complicated?

Westpac also details acquiring fees. These include a scheme fee, which is described as the fee charged by Visa, Mastercard and Union Pay for the provision of the card payment services. The switch fee, which is charged by the payment network or electronic commerce gateway to process a transaction, for example Paymark, Verifone or Payment Express. And there's Westpac's fee, or the fee the acquiring bank charges for the provision of card payment services. Westpac says this can include merchant support, fraud prevention and authorisations.

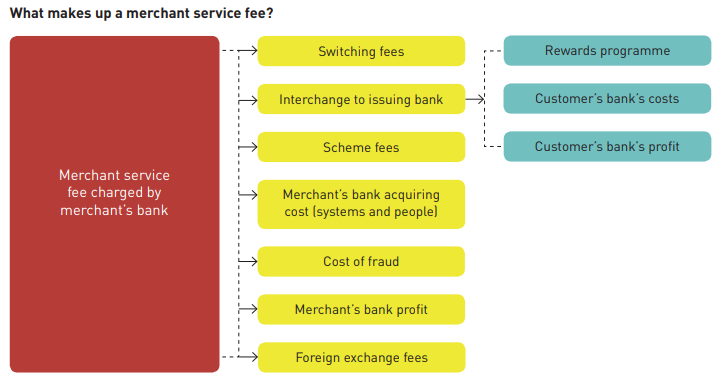

According to Retail NZ, a merchant's bank pays the majority of the MSF to the card issuer of the retailer's customers, and a smaller amount to other suppliers to cover processing and operational costs.

The diagram below comes from Retail NZ.

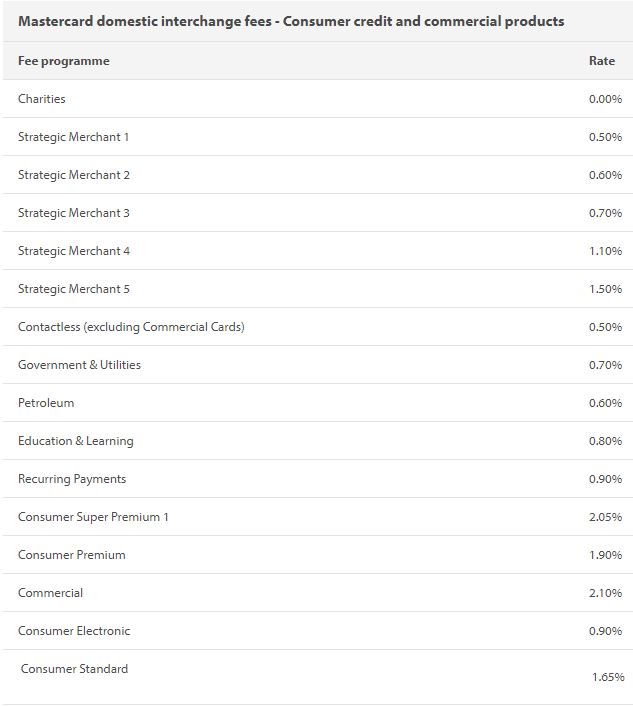

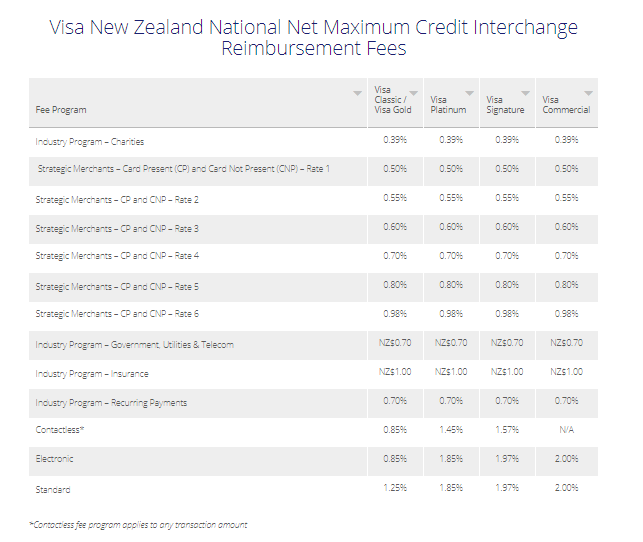

Visa and Mastercard also have lengthy lists of pricing details for credit and debit interchange on their websites, as the Visa example below shows. These tables show the Visa maximum interchange reimbursement fees applicable to NZ domestic transactions processed through Visa’s national net settlement service. Mastercard also explains who qualifies for each category albeit some descriptions are vague. For example, those qualifying for the "strategic merchants 1" category are merchants and or merchant groups, as advised by Mastercard from time to time, that meet agreed performance requirements.

One hundred page price lists

It's also a complicated business for banks. A senor NZ banking figure, who didn't want to be named, told interest.co.nz Visa and Mastercard have 100 page price lists. Staff at their bank waded through this to try and ascertain what they'd be paying, having been told it would be an average of about 20 basis points per transaction. It turned out it was but no one at the credit card scheme their bank was working with could explain how you arrived at this, the senior banking figure told interest.co.nz.

In its ongoing review of retail payments regulation, detailed in Part 2 of this series, the Reserve Bank of Australia (RBA) also outlines the complexity around scheme fees.

"The Bank understands that the international schemes have schedules of hundreds, if not thousands, of individual fees but these are not published. The fee schedules are usually a combination of global and domestic fees. Listed fee schedules may be subject to bank-specific rebates or discounts to encourage card issuance and exclusivity arrangements," the RBA said.

"The Bank has previously considered issues relating to greater transparency of scheme fees...It may be time to revisit the issue of scheme fee transparency as part of this review."

(Note the RBA review of retail payments regulation discussed in part two of this series has been put on hold due to "the current extraordinary circumstances associated with the impact of COVID-19." The RBA now expects the review to be completed in 2021 rather than 2020).

Part two also detailed an issues paper entitled 'Retail payment systems in New Zealand' issued by the Ministry of Business, Innovation & Employment (MBIE) in 2016. In this MBIE said market dynamics suggested there was cause for concern in both the credit and debit card markets. The National Party's then-Commerce and Consumer Affairs Minister Paul Goldsmith said the Government was "prepared to consider regulatory options" if competition failed to moderate retail payments costs.

In a 2017 Cabinet paper Goldsmith's successor, Jacqui Dean, said she was concerned the declining use of EFTPOS - fee free for merchants - may limit choice and place further pressure on prices.

"Between January 2014 and June 2017 the value of transactions made with EFTPOS cards declined from around 44% to 32% of card transactions. there has been a corresponding increase in contactless (tap and go) debit transactions (by value) over this period from about 1% to 9%, as well as increases in credit and debit card usage," Dean said.

"As EFTPOS declines, it becomes more likely that merchants wishing to receive electronic payments, and not discourage customers, will have limited choice but to accept card scheme products, Visa and Mastercard, at the going price. Over time this may further increase costs to the economy and pressure on the prices of goods and services," Dean added.

The 2016 MBIE report raised similar concerns.

"We estimate that fees to merchants on scheme debit transactions could rise by $216 million per year if contactless usage increases to 60% of debit payments...This could result in the interchange dynamics we currently see in the credit card market driving inefficiency and large scale cross-subsidisation in the debit market as well," MBIE said.

Additionally MBIE pointed out "systemically higher costs" on smaller merchants for the processing of retail transactions, with interchange charged for small merchants in some cases two and a half times rates for the biggest merchants such as supermarkets. In part two we reported that MBIE says credit and debit interchange fees have decreased by between 8% and 14% since 2016.

Faafoi encourages banks and merchants to explore alternatives to credit card payments

So what does Minister of Commerce and Consumer Affairs Kris Faafoi have to say? Note that in 2018 Faafoi said: "We and I have chosen not to go down the route that Australia and European Union has done in respect of regulating interchange fees. However that remains an open option and very much on the table, particularly if we see fees rise again." Faafoi also called for "an ongoing commitment from banks and Visa and Mastercard to increase the transparency of costs associated with retail payments, and continuing work to educate merchants," adding he wanted "to see low cost debit options remain to ensure that merchants do have a choice about what forms of payment they accept."

Earlier this month Faafoi told interest.co.nz he is "continuing to keep a close eye on interchange fees. While average weighted interchange fees have tracked down over the last three years, if we start seeing increases I won’t rule out taking action including regulation."

"It’s important that new payment methods continue to develop, as this will lead to greater competition and lower payment fees passed onto consumers. While I don’t have a strong view on particular technologies that might be developed in this space, I expect they might involve mobile and internet-based payments that bypass the card schemes. The development of open banking also benefits consumers by giving them control and choice over their data. So I continue to encourage banks and merchants to explore alternatives to credit card payments and take up the open payment standards that Payments NZ is developing," said Faafoi.

In December Faafoi made it clear open banking isn't progressing as fast as the Government would like. Open banking should give customers greater access to and control over their own banking data, and requires banks to give competing third parties access to their systems. The threat of legislating for open banking remains.

"In my letter to API [application programming interface] providers in December last year, I expressed my concern at the slow pace of progress on industry-led open banking initiatives and outlined my expectations for providers to prioritise this work. I am treating these concerns seriously and will continue to consider the appropriate role for government in this space," Faafoi added.

Retail NZ, Consumer NZ advocate regulation

Retail NZ issued a report in 2015 that helped spark MBIE's probe of retail payment fees. Retail NZ pointed out NZ payment systems were unregulated and argued there was little transparency around fee levels. Retail NZ cited a report it commissioned by economic consultancy Covec that estimated the hidden cost of payment systems to shoppers in 2015 was about $380 million. This was forecast to rise to as high as $711 million by 2025, meaning an estimated total cost of $3.1 billion over 10 years.

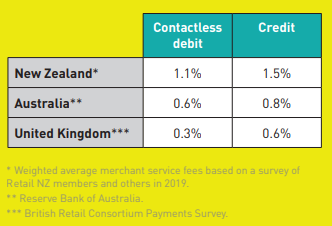

Retail NZ's latest payments survey, for 2019, puts weighted average MSFs for contactless debit and credit card transactions at 1.1% and 1.5%, respectively. In comparison Australia's were 0.6% and 0.8%, and the United Kingdom's 0.3% and 0.6%. (See table below). Retail NZ says the NZ credit card MSF is down from 1.7% in 2016, while the debit card MSF is up from 1.0%.

CEO Greg Harford said essentially Retail NZ's position hasn't changed over the past few years. Its 2015 report said; "It is likely that direct regulation will ultimately prove to be the most appropriate way of regulating payments systems."

"There needs to be more oversight of merchant fees charged by the banks. Interchange is a component of merchant fees, and is likely the largest component, but it is only one of the components. Interchange is the rate the banks pay each other to settle a transaction, while the merchant service fee is what the retailer pays its bank. Historically, in at least some cases, there would appear to have been a significant mismatch between interchange and the merchant fees actually paid by the merchant," Harford told interest.co.nz.

"Retail NZ welcomed changes made last year by Visa and Mastercard to maximum interchange rates. However, we don’t have up to date information on what that has actually meant for merchant fees. We are currently undertaking some research on this."

The table below comes from Retail NZ's latest payments survey.

Retail NZ points out that NZ is unique in having a domestic EFTPOS network that's "essentially fee-free" for merchants.

"This means that merchants face a particular cost challenge as customers migrate away from traditional EFTPOS and towards contactless debit, either with a card, Apple Pay or Android Pay," said Retail NZ.

"The New Zealand payments landscape is continuing to evolve. Over the past 24 months, we have seen a significant uptake of 'buy now, pay later' schemes. These are proving to be popular with consumers, but come at a high price for retailers, often more than three times the cost of a credit card transaction."

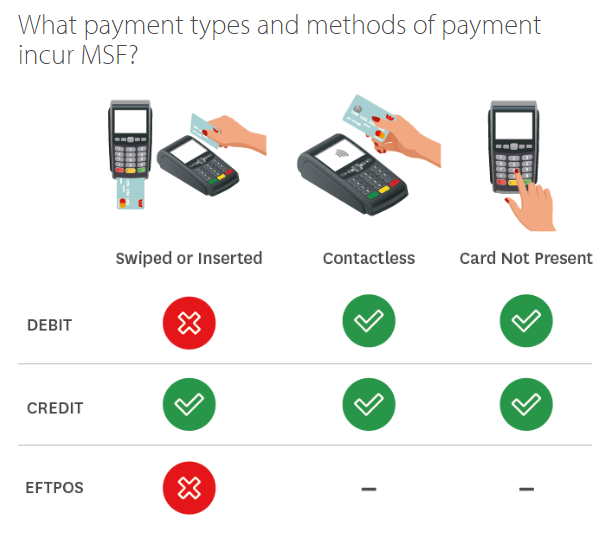

The diagram below comes from Westpac.

Last year Harford told interest.co.nz that buy now, pay later schemes have proven effective at generating sales but come at a "very hefty price" for the merchant.

"Our understanding is most merchants are paying north of 5% for buy now, pay later transactions, which is substantially more than credit card transactions, around 1.5% on average, or contactless debit transactions, around 1.1% on average. Note, credit and contactless debit rates are substantially higher [in NZ] than in Australia, the UK or Europe," Harford said. "Buy now, pay later schemes are very popular with customers, especially the younger millennials who need credit but who seem less likely to have a credit card."

In part one of this series we detailed how Visa and Mastercard work in partnership with threats to their businesses, including the buy now pay later service providers.

Consumer NZ head of research Jessica Wilson said the group's submission on MBIE's issues paper also supported regulation. The submission argued that high interchange fees allow banks and card schemes to incentivise consumers to use high-cost credit and debit cards.

"The use of these cards generates revenue for banks and schemes but increases the cost of doing business for merchants and results in higher prices for consumers."

"Credit card providers have argued that interchange regulation would require them to scale-back reward programmes or increase card fees to pay for rewards. We don’t consider these are valid reasons to keep interchange unregulated. Rewards schemes, which interchange fees help fund, don’t offer good value for most consumers. Their value is also often difficult for individual shoppers to assess due to the complicated calculations required to convert spend into actual rewards," Consumer NZ said.

'A fine-tuning exercise of identifying the right balance in the market'

So what do Visa and Mastercard say?

Visa says interchange is a tool used to bring balance to the payments ecosystem for all parties being card issuers, acquirers, merchants and cardholders. A Visa NZ spokesman also points interest.co.nz to a submission the company made to the Australian Productivity Commission in 2018. Remember from part two in this series that the Productivity Commission recommended banning interchange.

According to Visa's submission, in the name of its Australia, New Zealand and South Pacific group country manager Julian Potter, a ban would eliminate a key mechanism for developing electronic payments and ensuring balance across a wide range of participants in the payments system.

"Interchange serves as a key source of payments system funding, which enables financial institutions to connect to merchants and cardholders all around the globe. Networks like Visa create the ideal balance of incentives for cardholders and merchants to maximise transactions across sectors. Interchange ensures that issuers, acquirers, and merchants invest in the payment system in a manner that benefits all participants. By balancing the economics and value among all participants, interchange also encourages more merchants to accept Visa," Potter said.

"Interchange is a strategic tool to balance the two-sides of the payments market; that is the interest from consumers, businesses, and governments in using electronic payments provided by issuers and the merchants’ interest in accepting those payments via acquirers. For Visa, setting the right level and structure of interchange is not a mathematical formula or a cost-based exercise only, but a fine-tuning exercise of identifying the right balance in the market. Setting interchange too high or too low could affect one or the other side of the market. This may cause lower investments in acceptance or lower investment in issuance."

"Visa also has made its products more attractive to participants in its payments system by creating incentives via reduced interchange rates to encourage marketplace behaviours, including the adoption of technologies that reduce fraud, such as electronic authorisation of transactions in the 1980s, the PCI DSS 4 standard used to protect cardholder information and most recently, the secure EMV chip technologies. Visa similarly provides reduced interchange rates on transactions that are submitted with accurate data elements, processed in a timely manner, and (on commercial products) come with enhanced data, all of which improves the timeliness and accuracy of data in the Visa system to the benefit of all participants," said Potter.

"Finally, interchange also provides some of the economic means for banks to invest in security and payments solutions that benefit the economy as a whole, which necessitates adequate revenue and consistency across the globe for issuers to support their card programs."

Mastercard hasn't responded to interest.co.nz's requests for comment. However, in its submission on MBIE's issues paper Mastercard said there was no incentive for it to set interchange at rates that would negatively impact business acceptance or negatively impact card issuance. Interchange, it said, facilitates the secure and efficient functioning of the payment system.

"While Mastercard does not directly earn revenue from interchange, we do benefit when interchange is set at the right level through higher transaction volumes. The right interchange level is one that: Recognises the value delivered to merchants when they accept cards, and compensates issuing banks fairly for the costs involved in providing businesses and governments who accept cards with the value they receive," Mastercard said.

"Interchange covers the cost of fraud protection, so cardholders are protected in the rare event of a fraudulent transaction. For example, in the event of a stolen card, Mastercard cardholders are protected from fraud or unauthorised transactions under Mastercard’s zero liability policy. Investment in EMV chip technology has also enhanced the anti-fraud capability of cards, making them almost impossible to counterfeit and adding an extra layer of protection not possible with magnetic stripe cards."

Interchange also pays for the interest free days on credit cards, which nearly three in four New Zealanders rely on to pay off their credit card bills, Mastercard said. Businesses, or merchants, benefit through guaranteed payment, cost efficiency and increased sales, Mastercard argued. And from a government perspective it said using electronic payments rather than cash reduces the shadow economy and tax avoidance.

Mastercard claims in Australia RBA regulation of interchange means cardholders pay about $480 million more in additional fees each year, while Australian banks have reduced their customer rewards programmes.

"Mastercard strongly recommends the existing payments framework be retained. It has yielded positive outcomes for not only consumers and businesses, but for New Zealand’s broader economic objectives of productivity and innovation. More specifically, current arrangements for interchange rates provide an array of critical services that benefit all payments system participants," Mastercard said.

'Credit cardholders were made unambiguously worse off'

As noted in part two of this series bank lobby group the New Zealand Bankers' Association (NZBA) doesn't think retail payments regulation is needed in NZ. The 2016 MBIE issues paper said market dynamics suggested there was cause for concern in both the credit and debit card markets.

A report by Axiom Economics commissioned by NZBA told MBIE that if the level of credit card interchange fees was regulated in NZ, resulting in a reduction in those rates, this would decrease the revenues earned by bank card issuers.

"Those issuers would be expected to respond by either increasing the fees payable by credit cardholders and/or reducing the value of benefits received from the use of credit cards. This was certainly the outcome when the Reserve Bank of Australia regulated the level of credit card interchange fees in Australia in the early 2000s: credit cardholders were made unambiguously worse off," Axiom argued.

"What is also interesting is the form that those fee increases took in Australia. Specifically, they manifested primarily in the form of higher annual fixed fees, i.e., fees that were independent of transaction volume... fixed fees have virtually no effect on the ‘marginal price’ for different payment mechanisms. Once a cardholder has paid that annual fee, she is no more likely to use an EFTPOS card than her credit card when paying for an item, since that cost is ‘sunk’ and forgotten."

NZBA itself told MBIE unintended consequences of regulation could include risks that regulating interchange wouldn't lead to price reductions being passed on to consumers, additional costs, and the potential to inhibit innovation. NZBA pledged a commitment from acquirers (banks) to offer transparent merchant pricing options across the market, including:

a. Acquiring institutions will provide key acquiring related information to merchants, including information on cancellation and renewal of terms and conditions.

b. This information will be disclosed in a way that is clear and simple.

c. Acquirers will make information about interchange rates set by schemes available to customers. In particular merchant statements will separately identify fees for debit and credit.

d. Acquirers will disclose their fees, fee structures and the costs to individual merchants in a clear and accessible form, and, subject to notification by the schemes, provide a reasonable minimum period of notice (to be determined) of changes to fees and/or fee structures.

What the banks say

So what do the banks themselves say, are they doing the things NZBA said they would do? Interest.co.nz asked the big five.

ANZ NZ, the country's biggest bank, provided a detailed response.

"ANZ NZ’s average Merchant Service Fee (MSF) rate for contactless debit across all our customers, from mass market through to large retailers (as at Jan-2020), was below 60 basis points. This is comparable with the Australian market. It’s important to remember there is no MSF in NZ for EFTPOS whereas in Australia the average cost per transaction is $AU0.16. Around 50% of all ANZ NZ’s transactions processed are EFTPOS. You’ve also seen ANZ is waiving the fee for contactless debit transactions until 30 June to help eligible small business customers prevent the spread of coronavirus," an ANZ NZ spokeswoman said.

In terms of the NZBA pledges on behalf of acquiring banks ANZ NZ provides merchants with the following documents which outline all key acquiring related information, including information relating to cancellation and renewals; ANZ letter of offer, ANZ merchant business solutions terms and conditions, and ANZ merchant business solutions merchant operating guide.

"ANZ removed all early termination penalty fees in 2017 and is currently also removing contract terms for all retail/mass market customers. ANZ FastPay, our micro merchant solution, has no contract term which means that customers can exit at any time without penalty."

In terms of disclosing information in a clear and simple manner, the ANZ NZ spokeswoman said key information is sent in hard copy to each merchant during the "onboarding" process. This information can also be found on ANZ’s website here and here. Interchange rates are listed on ANZ’s website for Visa, Mastercard and UnionPay with interchange rates for all categories, showing debit and credit interchange rates separately. ANZ NZ said it also provides separate debit and credit pricing for all its merchants.

"ANZ was the first New Zealand acquirer to launch contactless debit in 2011, as part of the Rugby World Cup, and has provided merchants with separate debit and credit pricing since the solution launched. As well as separate debit and credit pricing, ANZ provides a range of pricing options to support businesses with their payment needs including: Interchange plus, fixed rates and matrix."

The bank spokeswoman said interchange plus provides a direct pass through of the interchange costs that the card issuers charge the acquiring bank for each transaction, plus a total margin to cover scheme fees paid to the card scheme provider being Visa or Mastercard, network fees paid to the network provider e.g. Paymark or EFTPOS NZ, float costs being the cost of settling funds to customers before ANZ NZ receives the funds from card issuers, and the ANZ acquirer margin.

Fixed rates are calculated based on the merchant’s average transaction value, card mix and origin of card being domestic versus international, the ANZ NZ spokeswoman said. The bank provides a range of options under this structure, including separate rates for domestic versus international or; separate rates for Visa versus Mastercard or; one rate applied to all credit transactions and a separate debit rate, capped at 0.95% for ANZ settled customers, is always applied to all contactless debit transactions, the spokeswoman said.

Meanwhile with matrix the fee varies each month depending on the transaction levels processed for that month.

"The merchant service fee is a percentage of the total dollar value of the credit card and international debit card transactions processed during each month. The percentage applied is determined by sales volume and the average monthly ticket size of transactions processed," the ANZ NZ spokeswoman said.

"ANZ terms and conditions state that changes to merchant pricing or fee structures can be made by providing at least 14 days’ notice in writing. In practice, ANZ generally provides customers with more notice. ANZ proactively communicates scheme interchange changes to interchange plus priced merchants."

A spokeswoman for ASB said the bank has made a number of changes to how it provides merchants with key information since 2017. This includes information provided during the application process, as well as providing ongoing updates to terms and conditions.

"The merchant application forms the legal agreement which includes full disclosure of fees and pricing. This is acknowledged by the customer with the returned signed form. Our sales team uses the application form to scope and understand the customer’s needs and requirements. Pricing and fees are always discussed prior to the application form being sent to the customer for acknowledgment," the ASB spokeswoman said.

Merchants can choose from three ASB pricing options; Fixed pricing that is the same rate for all transactions, interchange plus – where the merchant pays the scheme interchange rate for each transaction plus an agreed ASB margin, and semi bundled where the transactions are grouped in seven different bundles based on the transaction type and similar interchange rates.

"For example some of our groups are compiled as super premium cards/commercial, premium cards/commercial, credit contactless cards, debit contactless cards, international cards, standard credit cards, standard debit cards," the ASB spokeswoman said.

"We regularly review our pricing options to ensure they are in line with the market, and that we are providing the best value for our merchants. For pricing changes, we provide one month notice to our merchants. We also have our merchant operating guide on our website, which outlines general information and contains helpdesk contact details. We also post notices on our website around any changes to terms and conditions."

A spokesman for BNZ said the bank provides full information on terms and conditions including cancellation information.

"We have simplified our terms and conditions and we’re continuing to do more work here to make things simpler and clearer for customers," the BNZ spokesman said.

Information about interchange rates set by schemes is provided by BNZ "in various levels of details depending on the agreement we have with the merchant."

"BNZ has changed our statements to reflect the guidance of the MBIE review and provides a number of pricing options to suit our customers’ needs. We updated our merchant statements in late 2018 to provide more transaction details. For customers using our interchange plus services, the statements provide full product type breakdown, transaction numbers, transaction value, interchange rate, and margin (which is also detailed in our agreement). We also split these out by international and domestic."

"For customers on our standard offering, their invoice provides a summary of value and transaction numbers by product, international, and domestic," the BNZ spokesman said.

"BNZ believes providing more information to our merchant customers is important, and this is an area of ongoing focus for us. We are continually developing our systems and capabilities to support more development here and we are looking forward to being able to deliver the next improvements we have in the pipeline."

"We ensure that a minimum notice period of up to 60 days is adhered to for any changes. Amongst those changes was the reduction of premium interchange and premium contactless interchange that BNZ passed on to merchants in full at the time of the scheme changes," the BNZ spokesman said.

A spokeswoman for Kiwibank said since the bank started providing merchant facilities in August 2013 it has used the interchange plus pricing methodology as its default pricing for merchant service fees, believing this provides customers with the most transparency.

"Aside from the information made available on our, and the card schemes’, websites, our agreements and monthly statements give our customers a very granular pricing breakdown on the fees. I’m not able to provide you more information on our fee disclosures as this is commercially sensitive," the Kiwibank spokeswoman said.

A spokesman for Westpac NZ said the bank offers three merchant pricing options.

These are blended rate, which is a fixed percentage payable on all credit and contactless debit transactions covering interchange, scheme fees, switching fees, other associated costs and Westpac's fee. Unbundled rate which is the actual interchange payable on each transaction plus a fixed percentage on all credit and contactless debit transactions. The fixed percentage covers scheme fees, switching fees, other associated costs and Westpac's fee. And a fully unbundled rate which includes the actual interchange, scheme fees, switching fees and associated costs payable on each transaction plus a fixed Westpac fee.

The Westpac NZ spokesman notes information on domestic interchange rates is published on the bank’s website.

"We have made improvements to Westpac's external website, including enhanced information, to provide clarity around the different costs and fee structures of merchant pricing. In addition, our internal website has been updated with information to help our relationship managers and customer-facing teams better serve our customers," the Westpac NZ spokesman said.

"A significant piece of work is under way to separate our debit and credit merchant service fees for customers on a blended rate. This is due to be in market later this year. Any customer on an unbundled or fully unbundled rate already has the actual interchange, by card type and/or payment method, charged and displayed on their statement. Westpac may change the merchant service fee rate and/or methodology from time to time by providing written notice to the merchant. Customers are typically given at least two weeks notice.”

In its 2019 retail payments survey Retail NZ noted that some banks had moved to ‘unbundle’ their merchant customers - meaning different rate structures for credit and contactless debit transactions.

"This is an area to watch over the next 12 months. If other banks follow suit, unbundling is likely to reduce the overall merchant service fee for contactless debit payments in particular. Our survey shows that merchants with an unbundled rate for contactless debit pay, on a weighted-average basis, 0.1% less than those on a bundled rate," Retail NZ said.

Commerce Commission hasn't looked at the issue for 7 years

The Commerce Commission is tasked with enforcing the Commerce Act to promote competition in markets for the long-term benefit of consumers. In 2006 the Commission went to the High Court alleging fixing interchange fees, charged by credit card companies and paid by retailers as part of the fees they pay to banks, was anti-competitive. The fee was up to 1.8% of each credit card transaction, the Commission said, noting retailers weren't allowed to charge customers extra to use credit cards so had to recover the fees by increasing prices, regardless of whether customers pay by credit, cash or EFTPOS.

The Commission said it had received numerous complaints from the retail sector about the setting of credit card merchant service fees and associated rules imposed by the credit card schemes. Interchange fees represented 80% of merchant service fees, inflating merchants’ costs leading to higher prices for consumers.

Among those alleged to be involved in anti-competitive arrangements were Visa, Mastercard, ANZ, ASB, BNZ, Westpac, TSB, Kiwibank and HSBC. Ultimately the case was settled in 2009. Visa and Mastercard agreed bank credit card issuers could individually set the interchange rates applying to transactions using their credit cards, subject to maximum rates determined by Visa and Mastercard which would be publicly available. Additionally merchants were no longer prevented from applying surcharges to payments made by credit cards or by specific types of credit cards, with surcharges to be disclosed to cardholders at the time of sale and bear a reasonable relationship to the merchant's costs of accepting Visa and Mastercard products.

In 2013 the Commission issued a report evaluating the 2009 interchange and credit card settlements. This was after the consumer watchdog had been collecting data from the parties involved to ensure compliance with the settlement agreements, and undertaking a broader evaluation of the settlement agreements to see if they had succeeded in promoting competition.

"From the aggregate data collected by the Commission, we estimate that merchants paid over $70 million less in interchange fees between 2010 and 2013 compared to what they would have paid had fees stayed at 2009 levels over that time period. We are therefore satisfied the settlements contributed to significant savings for merchants, although we are unable to establish the extent to which these savings have been passed on to consumers," the Commission said.

"We note that overseas jurisdictions have specifically regulated interchange fees, or taken steps towards such regulation. For instance, in 2003 the Reserve Bank of Australia mandated that interchange fees be set on a cost-based benchmark, which has resulted in significantly lower interchange fees. In 2010, the US Federal Reserve was given the authority to cap interchange fees for debit cards, which the Federal Reserve has now implemented. More recently, in 2013 the European Commission announced a proposal to regulate interchange fees on credit and debit card transactions," the Commission added.

Interest.co.nz sought the Commission's views on where credit card merchant service fees and associated rules are at today. Are they reasonable? Do any rules need changing? Should interchange fees be regulated in NZ as they are in dozens of other countries? And are the interests of consumers being served?

"We have not conducted another report into merchant service fees since the 2013 study and are unable to answer questions about whether fees are currently reasonable or excessive, or not. Further questions about regulation of fees are policy questions and not appropriate for the Commission to answer," a Commission spokesman said.

To be continued...

You can find parts one and two in this series by clicking on the links below.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

5 Comments

This long and complex article - perhaps unintentionally - echoes the complex pricing structures of MSF themselves, which are overlaid with bundling, discounting, waivers, inducements and penalties.

The crux of the Gubmint thinking seems to be summed up in Faafoi's frustration that there's slow progress: 'It’s important that new payment methods continue to develop, as this will lead to greater competition and lower payment fees passed onto consumers.'

But this typically naive view stems from a failure to appreciate three aspects of banking software and hardware:

- It is apart from Defence and Secret Squirrel agencies, easily the most difficult software and hardware environment on the planet. Everything has to adhere to extremely conservative standards, pass stringent user testing, survive simulated attacks, hacks and penetrations, and allow an easy upgrade path for all existing devices, cards, comms protocols to whatever succeeds them.

- So none of this is cheap, fast or simple. It is extremely expensive, needs to achieve a critical mass of merchant and bank acceptance to have any hope of recovering those costs, and survive the overviews of everything from international standard-setters, central banks, auditors and of course Govenments/regulators.

- The combination of expense, the risk that even modest initiatives will be turned down after a development cycle, and the sheer elapsed time implicit in all of the above, means that literally years have to be expended assembling the many, many ducks into tidy rows. By which time, and inevitably, the world has turned, and new features are needed, so some of the existing iteration is rendered obsolete, and another cycle starts.

So it is small wonder that Faafoi is frustrated with the glacial speed of 'open banking' and other nice-to-haves. But it's just not feasible to unleash a bunch of script kiddies on the sector and expect a result by lunchtime.....

What about the 3-5% that retailers are willing to pay for buy now pay later and instalment providers? They whinge about a modest fee that actually helps grease the wheels of consumer's money moving around easily, but they'll pay through the nose for something that's getting heaps of kids into untold debts - untold because it's got no regulation at all!!!

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.