*This is the Fourth article in a series on Visa, Mastercard, banks and New Zealand's retail payments systems. Parts one, two and three can be found here, here and here.

By Gareth Vaughan

COVID-19 is hitting the economy like a meteorite with the Government and Reserve Bank throwing cash around like confetti in a desperate attempt to keep businesses alive and people in work. The unfortunate inevitability is there will be many casualties. Shutting the economy down for at least four weeks, to fight a highly contagious, dangerous and unpredictable virus, will do that.

The impact will be immense and will continue to be felt for years. So longer-term, could EFTPOS, the highly successful electronics payments system that launched in 1989, be among the COVID-19 casualties?

Initially that may sound unlikely. In part three of this series we heard from ANZ New Zealand, the country's biggest bank, that by dollar value about half of all its transactions processed are EFTPOS ones.

But EFTPOS has been under attack by banks and the Visa and Mastercard "card schemes" for years. And ironically the major banks' waiving of fees on contactless debit card transactions for business customers during the coronavirus crisis, and in some cases merchant service fees too, could spell bad news for EFTPOS. That's even though this is a welcome saving for businesses. For retailers, for example, card acceptance fees are typically the third highest cost of doing business after wages and rent. The move is, of course, good for public health as well because when making contactless payments customers don't need to touch payments terminals.

However, the theory is that with banks giving contactless transactions away for free, many merchants who normally don't offer them to customers because of the cost will embrace contactless payments. This means more and more consumers will get used to the ease and convenience of making contactless payments instead of paying via EFTPOS, which involves inserting their cards into payments terminals, and utilising mag-stripe technology.

The $80 limit on contactless payments may also be lifted during the COVID-19 pandemic so more transactions are contactless. In Australia the limit has already been increased to A$200 from A$100.

An executive with high level experience in the payments sector who spoke to interest.co.nz on condition of anonymity, worries that all this could ultimately be the death of EFTPOS. Especially if the fee waiving goes on beyond the initial three to six months proposed by bank card issuers.

"Coronavirus is almost disastrous in the sense of the demise of EFTPOS," the executive says. "With more and more [payments] terminals being activated [for contactless payments] people will develop the habit...[And] the banks essentially don't see a future [in EFTPOS] because it doesn't drive any revenue for them."

As we saw in part three weighted average merchant service fees come in at 1.1% for contactless debit transactions, and 1.5% for credit transactions, according to Retail NZ. In contrast EFTPOS transactions are free for merchants.

Why does it matter? In a 2016 issues paper the Ministry of Business, Innovation & Employment said market dynamics suggested there was cause for concern in both the credit and debit card markets. In a 2017 Cabinet paper National Party Commerce and Consumer Affairs Minister Jacqui Dean said she was concerned the declining use of EFTPOS may limit choice and increase costs to the economy.

"Between January 2014 and June 2017 the value of transactions made with EFTPOS cards declined from around 44% to 32% of card transactions. there has been a corresponding increase in contactless (tap and go) debit transactions (by value) over this period from about 1% to 9%, as well as increases in credit and debit card usage," Dean said.

"As EFTPOS declines, it becomes more likely that merchants wishing to receive electronic payments, and not discourage customers, will have limited choice but to accept card scheme products, Visa and Mastercard, at the going price. Over time this may further increase costs to the economy and pressure on the prices of goods and services," Dean added.

And as we reported in part three, current Commerce and Consumer Affairs Minister Kris Faafoi isn't ruling out taking action including potentially regulating interchange fees, which we'll recap later.

What about Online EFTPOS?

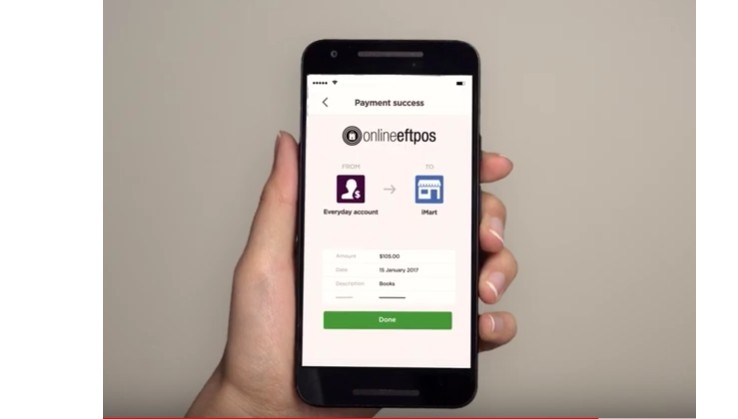

Paymark, which connects to about 100,000 EFTPOS terminals across NZ, on Tuesday took the opportunity to spruik Online EFTPOS, a service it launched in 2016. Initially launched with ASB, Westpac, The Co-operative and Heartland Bank now also support it. Paymark points out that, in the age of COVID-19, Online EFTPOS removes the need for shoppers to interact with anything except their own phones.

“There’s no need to use credit cards, customers can buy products using their own money direct from their own bank accounts. That’s great if you don’t have a credit card or if you want to pay from your home, and just drop in and pick up the product.” says Paymark CEO Maxine Elliott.

"Customers can shop in-store and when making their purchase the retailer can use their own websites to conclude the transaction via Online EFTPOS. The customer approves the purchase through their own banks’ mobile apps and the transaction is completed with the minimum of contact," adds Elliott.

Paymark says more than 200 merchants use Online EFTPOS, a drop in the ocean considering the tens of thousands of merchants in NZ. The company says merchants who aren’t already set up to use Online EFTPOS can do so with no set-up cost. Merchants do pay $14.00 plus GST per EFTPOS machine per month. And Online EFTPOS comes with a percentage transaction fee charge of about 1% of the sale.

In contrast to Online EFTPOS, when celebrating traditional EFTPOS' 30th anniversary last year, Paymark boasted of having more than 85,000 merchants using the Paymark network every month, with a total of 170,000 terminals processing more than 1.6 billion EFTPOS transactions a year.

Asked why so few retailers use Online EFTPOS, Retail NZ CEO Greg Harford says the service is relatively new, and has previously been seen primarily as a mechanism to support online sales, which is "a pretty crowded marketplace."

"I’m not aware that the service has been substantially used in-store in the past," says Harford, adding before the lockdown there were about 27,000 retailers, both online and bricks and mortar, in NZ operating from around 35,000 sites.

The executive with high level experience in the payments sector argues Online EFTPOS is a great example of a contactless payments technology that can compete with the bank, Visa and Mastercard juggernaut. What's thwarting its growth, he says, is the banks won't embrace it because doing so would cannibalise their own revenue.

"The banks do enough to look as though they're innovating but they don't want to do too much that threatens all the money they make out of debit and credit card payments."

The executive argues that if banks opened up Online EFTPOS and made it available to everyone, the hundreds of millions of dollars in annual revenue they generate through merchant service fees and interchange "would disappear overnight." That's because merchants could use iPads or similar devises, and consumers their smartphones, to make payments. There wouldn't be a need for payments terminals and the interchange model would collapse.

"The tech is there. [But] banks are the incumbent. When they innovate it cannibalises their existing revenue so you see no innovation," the executive says.

"Online EFTPOS, when you've got one or two banks [enabling it], a merchant still needs to have the existing [payments] terminal, and they still need to have a merchant service agreement with each of the banks, because half their customer base might be on the banks that don't have online EFTPOS."

What about interchange for EFTPOS?

Another move Paymark could try to make EFTPOS sustainable is establishing its own system to clip the ticket on transactions. For example, charging merchants 0.6% on each EFTPOS transaction. By doing so Paymark could potentially create its own interchange model, like Visa and Mastercard's, passing revenue through to bank card issuers.

A source with knowledge in this area suggested to interest.co.nz Paymark doing this would involve "pretty simple pricing change work," three to four months of software development and testing, and cost about $250,000.

Across the Tasman, eftpos Payments Australia Ltd runs its own interchange regime. The company describes itself as a mutual style corporation not motivated by profit that promotes choice and competition in the Australia market, where there are 50 million eftpos-enabled cards.

An interchange fee is a fee charged by the financial institution on one side of a payment transaction to the financial institution on the other side of the transaction. A typical card transaction involves four parties the cardholder, the cardholder's financial institution (the issuer), the merchant and the merchant's financial institution (the acquirer). For most card transactions, the interchange fee is paid by the acquirer to the issuer.

Visa and Mastercard point out interchange doesn't generate revenue for them. However it underpins and grows their networks, meaning more transactions for them to clip the ticket on. Interchange is typically the biggest part of a broader fee known as the merchant service fee. Each bank sets its own interchange rates within a cap set by Visa and Mastercard. The merchant service fee is set by banks.

Paymark was sold by ANZ NZ, ASB, BNZ and Westpac NZ to French payment terminals and digital payment services provider Ingenico Group for $190 million in 2018, with the deal completed in early 2019 once Commerce Commission and Overseas Investment Office approval was obtained. Ingenico is itself now being bought by French rival Worldline in a €7.8 billion deal. With Paymark's bank owners having officially commenced a strategic review of their ownership in February 2016, the company is enduring a long period of unsettled ownership.

Even if Paymark wanted to launch an interchange model to incentivise banks to promote EFTPOS, could it? The executive with high level experience in the payments sector suggests when the banks sold Paymark they may have made it a condition of the sale that Paymark never charges for EFTPOS transactions. A spokesman for Paymark says there are "some constraints with our pricing due to our agreements with the banks, [but] Paymark is actively reviewing how it will price for the future of payments."

"We, however, have no plans to charge a percentage fee for EFTPOS to merchants at this point," the Paymark spokesman says.

Australia's dual-network debit cards & least-cost routing

In part two of this series we detailed how NZ's regulatory oversight of retail payments is behind where Australia was at in 2001. We've looked at the example of our neighbour because that's where the parents of our big four banks call home and somewhere else Visa and Mastercard are strong.

Another area of interest in Australia is the use of dual-network debit cards, or DNDCs. According to the Reserve Bank of Australia (RBA), about 90% of debit cards issued in Australia are DNDCs. These allow a domestic point-of-sale payment to be processed via either Australian eftpos or one of the other debit schemes such as Mastercard or Visa. However, online and foreign transactions are only done via the international schemes such as Visa and Mastercard.

In an issues paper released in December as it launched a review of retail payments regulation, the RBA explains how the DNDC system works.

"When a cardholder inserts their DNDC into a terminal to make a payment, they are asked to select the debit card scheme to process the transaction (for example, by pressing CHQ or SAV for eftpos and CR for Debit Mastercard or Visa Debit). By contrast, if the cardholder makes a contactless (‘tap-and-go’) payment, the default is for the transaction to be automatically routed to the network which has been programmed as the default network by the issuing financial institution," the RBA says.

"From a merchant’s perspective, the cost of accepting a debit card payment can vary depending on which of the three networks processes the transaction. For most merchants, payments via eftpos can be significantly cheaper for them to accept than payments via the international schemes."

In 2018 the Australian Productivity Commission recommended the Payments System Board, which has responsibility for determining the RBA's payments system policy, should; "Set a regulatory standard that gives merchants the ability to choose the default network to route transactions for dual-network cards. As the technology is readily available, this reform should be in force by 1 January 2019 at the latest."

"Merchants choose which payment methods to accept given the costs and benefits they face. Currently, contactless transactions using dual network cards (such as ‘tap and go’ facility at point of sale) are mainly processed through the generally higher-cost Visa or Mastercard networks by default, rather than through eftpos," the Productivity Commission said.

Australia now has what's known as a least-cost routing (LCR) system in place. Through this merchants can choose to route contactless transactions via whichever of the two networks on the card costs them less to accept. The RBA suggests this can help merchants reduce their payment costs, and also increases competitive pressure between the debit schemes, with greater incentives for them to lower their fees.

ANZ & 'merchant choice routing'

The Aussie parents of NZ's four major banks launched LCR functionality between March and July last year.

In a submission to the RBA the ANZ Banking Group, parent of ANZ NZ, says it has made merchant choice routing (MCR/LCR) available to nearly all its merchant customers, and is providing them with information about MCR's availability and potential benefits.

"ANZ commenced offering MCR in April 2019 and has made it available to approximately 96% of our merchant customers...As at December 2019, around 5% of merchant customers that have MCR available to them have enabled the service," the ANZ Group says.

The introduction of LCR/MCR is not, however, proving a silver bullet to reduce merchant service fees. In its issues paper the RBA points out some of the major banks only offer LCR for merchants, typically bigger ones, that are on interchange-plus pricing contracts. It also says none of the major banks has implemented LCR ‘in the background’ as a way to offer improved pricing for smaller and medium-sized merchants on ‘simple merchant plans’.

Furthermore the RBA sees key differences in the LCR capabilities offered by different card acquirers (banks), with some not yet offering a version that maximises merchant savings by enabling routing based on transaction size and payment network. Additionally, for some acquirers, LCR is not yet available on all the payment terminals they support.

"As LCR functionality has been gradually rolled out, schemes have responded with lower interchange rates for merchants that might be considering adopting LCR . However, there are several factors which may be limiting the overall downward pressure on merchant payment costs. First, lower interchange rates for some debit card transactions have been accompanied by increases in rates on other types of cards and/or transactions, in some cases for segments of the market where LCR is not an option," the RBA says.

"Second, the Bank [RBA] has continued to hear concerns that merchants may lose access to favourable strategic rates on credit transactions if they adopt LCR for debit transactions. Third, there appears to have been only limited competitive response in the form of lower scheme fees, which also affect payment costs to merchants and where the international schemes appear to remain more expensive than eftpos."

A warning from the RBA

The RBA says if incentives offered by Visa and Mastercard to bank card issuers were to lead to the issuance of single network international scheme cards, LCR would no longer be feasible on these cards, and the decline in the market share of eftpos seen over the last decade would probably continue. This would probably see an increase in payment costs to merchants.

"In such an environment where single-network debit cards were becoming the main type of card issued, the Bank [RBA] would likely need to assess the impact on competition and efficiency in the debit card system," the RBA says.

One possible policy response to any upward pressure on payment costs would be a reconsideration of the level of the interchange benchmark for debit cards, the RBA says. Currently in Australia there's a cap on debit card and prepaid card interchange fees to a weighted average of 8 cents per transaction, with a ceiling on individual interchange rates of 15 cents or 0.20% if specified in percentage terms. In NZ interchange is unregulated, as detailed in parts two and three of this series.

"An alternative could be to set separate interchange fee benchmarks for single-network cards and DNDCs. Issuers might be incentivised to issue DNDCs if the interchange cap for transactions on DNDCs with full functionality to enable LCR were higher than for single-network card transactions. Another possibility might be regulatory actions to facilitate the entry of new schemes that could compete more aggressively to be the low-cost scheme on DNDCs. This might include consideration of the effect of the current long-term exclusivity arrangements between issuers and international schemes, which may hinder the entrance of competitor schemes," the RBA says.

"Another policy option might be explicit regulatory action regarding the issuance of DNDCs. For example, the approach taken in the ‘Durbin amendment’ in the United States obliges all issuers with over US$10 billion in assets to have two unaffiliated networks on a debit card, to enable merchant choice of routing."

The RBA argues that such an approach would support LCR, and could help maintain downward pressure on interchange and scheme fees.

"To be effective, however, it might have to be supported by regulation covering online and mobile payments (e.g. where card credentials are tokenised) that ensured that both networks remained accessible to merchants as the industry shifts away from physical cards to digital credentials."

Visa & Mastercard's retort

In their submissions Visa and Mastercard are not thrilled at the RBA's regulatory stick waving. (Visa and Mastercard's business model was detailed in part one of this series).

Mastercard says the already high level of competition in the Australian payments market suggests further regulatory intervention should only occur in areas not exposed to market forces. It also maintains regulatory and policy interventions are having the unintended consequence of reducing competition and potentially increasing risk in the system. It says the current framework used to signal the price of electronic payments, including LCR for DNDCs, fails to achieve its intended purpose of improving transparency and competition in the debit card market, suggesting pricing practices are impeding consumers’ ability to choose.

"DNDCs duplicate functionality for consumers across two payments networks, creating cost and complexity for issuers and acquirers for the short-term benefit of merchants," argues Mastercard.

For its part Visa says should the RBA decide to mandate LCR/MCR, 'it will adversely impact Australian consumers’ right to choose their payment service, and it could limit their ability to benefit from contactless payments. Alternatively, allowing issuance of single-network debit cards would better enable consumer choice and facilitate network-based innovation and competition."

Another point Visa makes is that mandating routing could limit innovation and further inhibit consumer choice because consumers and banks would not benefit from Visa’s innovations, including enhanced security, if transactions were routed on another platform.

"A bank’s ability to choose a single network supports cost efficiencies, particularly for smaller financial institutions, rather than being required to maintain the infrastructure and rule requirements of multiple networks," says Visa.

eftpos Payments Australia, not surprisingly, has a different perspective.

"There can be no argument that the introduction of LCR in Australia has enhanced competition in the debit market, putting downward pressure on the costs of payments for the benefit of consumers and merchants," its submission to the RBA says.

eftpos Payments Australia calls for "significant additional steps" to remove obstacles to merchant adoption of LCR and achieve the regulatory intent of providing merchants with the information necessary to make an informed choice to control their costs.

"Had it been supported by clear regulation, LCR could have been more successful in gaining higher priority to overcome the market conditions, such as competing business priorities for acquirers, that have impacted delivery of LCR."

"Instead, the impact of LCR has been limited because only a small percentage of merchants (and DNDC debit transactions) currently enjoy the benefits of LCR. Pricing complexity and cross subsidisation, the lack of availability of LCR functionality on some terminals and opaque pricing plans have limited growth to date. These issues appear to be more pronounced for small merchants who have no market power. These small merchants are currently bearing the lion’s share of the costs," eftpos Payments Australia says.

It also suggests the RBA could regulate to require dual network functionality, including eftpos, on all debit payment methods issued in Australia across all form factors and channels for the lifecycle of a debit product.

New and evolving technology; Banks in charge

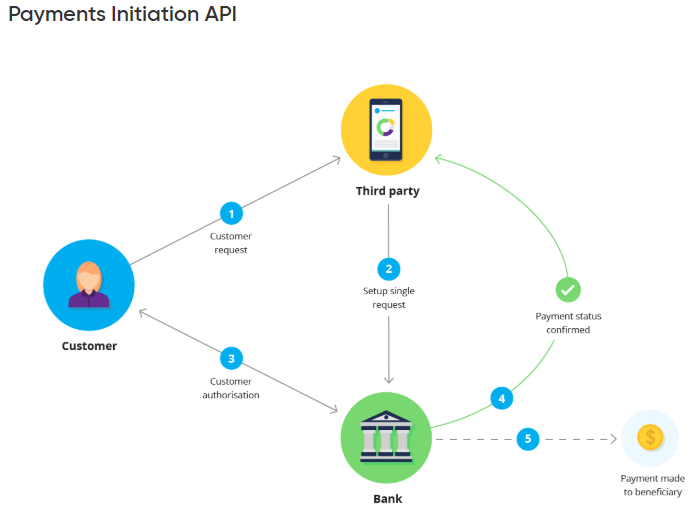

In part three of this series we heard from Commerce and Consumer Affairs Minister Kris Faafoi. Among other things Faafoi expressed concern at the slow pace of progress on industry-led open banking initiatives, saying he will "continue to consider the appropriate role for government in this space."

The idea behind open banking is that it gives customers greater access to and control over their own banking data, and requires banks to give competing third parties access to their systems. This could lead to a wide range of payment service providers accessing and securely switching transactions between banks in real time. Consumers could be able to do all this via a mobile device or from the likes of a smartwatch, with no cards or debit networks needed.

In NZ the development of open banking APIs, or application programming interfaces, is being overseen by Payments NZ, which is owned by eight banks. Between them ANZ NZ, Westpac NZ, BNZ and ASB own more than 88% of Payments NZ, comparable to the four's share of NZ banking system assets. The smaller shareholders are Kiwibank, TSB, HSBC and Citibank. Thus the country's oligopoly banks are the owners of the company tasked with opening their networks to competitors.

It has been suggested to interest.co.nz that Payments NZ has been focusing on APIs for desktop and laptop computers rather than smartphones. Keeping open banking away from phones would limit consumers' ability to conduct daily transactions through it, thus helping protect banks' debit and credit card revenue.

A spokeswoman for Payments NZ says the Payments Initiation API standard can support both browser based and mobile app based payments instructions.

"Via the API Centre, work on the next iteration of the standard, which further enhances mobile app based customer payment interactions, is underway," the Payments NZ spokeswoman says.

What about real-time payments?

Real-time payments could also enhance competition. If a consumer could make a payment to a merchant via a smartphone using say bluetooth technology, there'd be no need for payments terminals nor interchange.

So where are real-time payments at in NZ? A Reserve Bank spokesman acknowledges there's currently no NZ real-time 365-day payments system. However he notes Payments NZ has a number of strategic initiatives underway.

"One of which is SBI365 that is aimed at developing a recommendation which sets out the proposed next steps for industry consideration," the Reserve Bank spokesman says.

As for Payments NZ, the spokeswoman says it has a payments direction programme that "works with industry to understand the evolving future of payments."

"Part of this work includes exploring opportunities to speed up the end-to-end payments experience for account to account transactions, which includes real time payments. You can find out some more information via this link."

Of its SBI365 work stream Payments NZ says SBI refers to settlement before interchange, a SWIFT-based payment settlement and interchange system used by its banks. The work stream doesn't appear to have been moving very quickly.

"The industry working group have been developing a recommendation about a possible move to 365-day service availability. In early 2018 they finalised a draft report recommending steps which could be taken to extend availability across the system. This report is being refined from a technical perspective and will be socialised with industry stakeholders over the coming months," Payments NZ's website says.

"Following that socialisation we expect to be in a position to share the improvements the industry expects to make and provide a timeframe."

'You never want to eat your own lunch if you can eat someone else's'

The executive with high level experience in the payments sector argues the technology exists to enable greater competition with banks, Visa and Mastercard. As well as real time payments, online EFTPOS and open banking APIs, the executive cites Vend's web-based point of sale system.

The problem from a competitive perspective for consumers and merchants is the incumbent banks are in the driver's seat and don't want to take action that will cannibalise their own rivers of gold.

"The tech's all there. [But] you never want to eat your own lunch if you can eat someone else's. A bank isn't going to issue an EFTPOS card if it can issue a contactless paywave debit card that drives revenue to it...Banks are a business and they'll choose the product that gives them the higher revenue unless they're forced by regulation to open up."

To be continued...

Also see:

In the first part of a series on NZ's retail payment systems, Gareth Vaughan details the scale of key players Visa & Mastercard, looks at how & why they pay a miniscule amount of tax & how interchange works

In the second part of a series on NZ's retail payment systems, Gareth Vaughan looks at how New Zealand's regulatory oversight of retail payments is behind where Australia was at in 2001

In the third part of a series on NZ's retail payment systems, Gareth Vaughan looks at the complications of interchange & merchant service fees and finds a government minister still waving a regulatory stick

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

12 Comments

Lets take them away and revert back to cash right ? Why does those damn theater companies build movie theaters and then take cash off me when I use them ? why does .............................. ever business is designed to take money off you, but if don't like or value it, don't use it

The key sentence in this complex article is this:

the incumbent banks are in the driver's seat and don't want to take action that will cannibalise their own rivers of gold.

Plus, and I've made this point before, flowing money around the Interwebs via Open API's etc is superficially appealing. But it needs to be absolutely proof, and to prove that it is so via white-hat hack attempts, against any and every possible theft, interception, fraud, or other mischief.

The thing about banking software is that it has to interact with big iron at both bank's ends, cross dangerous connections, and be initiated from devices that, like the many varieties of Android, have to be assumed to be malware and hack-prone. That's a very tall and expensive order......

So it's no wonder that banks, having disincentives to do something along these lines, can simply sit on their hands and wait for much less well-resourced parties to flounder their way through this maze.

It doesn't help that large payment providers, like Visa, have waived large cash incentives in front to banks to lock our rivals providers or that banks have been so gullible as not to fully appreciate the value in what they are selling. They are giving up a goldmine tomorrow for shiny gold coin today, what an incredible destruction of shareholder value.

Talking about shares value, the further delay.. axing the idea.. will be inevitable because of Covids prevent people movement/hence their capital, could be temporary set back for sure.

But they'll glad for those further time reprieve as .. get more time to enjoy the sweet nectar of NZ flowers.

NZ banks cartel, liked the delayed approach, 'time is $'.. as you can see across the ditch it's rife with new technology adaptation, yet also accompanying by their ethics (or lack of it/just call it slip up). Couple months back ANZ announced to customer about abolishing their credit card fee, after years of milking it, fee reductions.

Like the rest of technology deployment, adaptation, but sadly lack of competition/regulatory measures.. it will come to NZ eventually, and like other things (eg. cancer drugs) it will always be 'slow approach'.. as the cream so yum, better share it with couple line of beurocrats... to make it seamless BAU - Shuush Gareth ;-)

@Gareth Vaughan , just a question ................have read about oil refineries shutting down production overseas

from next week due to fall in demand , whats the position at Marsden Refinery , any idea ?

Edited ............. I have found an article from 2 weeks ago saying they would reduce refining , store oil on the ships or in tanks until refining became viable again, but that demurrage was an issue

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.