By Janine Starks

Here's a question I received from on pension transfers from the U.K. and when to make the cross over from sterling to Kiwi:

I recently transferred my pension from the UK, via Brittania Financial Services. It has been sitting in pound sterling in an offshore BNZ account for the past 6 months. I've been waiting for the value of NZ dollar to drop before converting (I have to convert the total sum at one time) but am now becoming concerned that it's actually going to continue to rise. I was made redundant 6 months ago and so was intending to use half the money to pay off my mortgage (as I’m allowed access to 49%). Do you think the NZ dollar will continue to rise over the next 6-12 months?

It’s a famous rugby saying, ‘a game of two halves’, but the phrase applies rather nicely to the Kiwi-sterling cross rate. In the grand scheme of things, not a lot of trade goes on between here and the UK, so flows between the countries have no effect on the cross rate. To pick its direction means you have to study the two separate halves:

1. Where is the NZD/USD going? From current levels of 0.79-80 are we headed up or down?

2. Where is the GBP/USD going? From levels of 1.66 will it fall or rise against the US?

3. You then need to divide 1 by 2 to get the cross: 0.48-0.49, or if you do the calculation in reverse you currently get about NZ$2.10 for every pound you exchange.

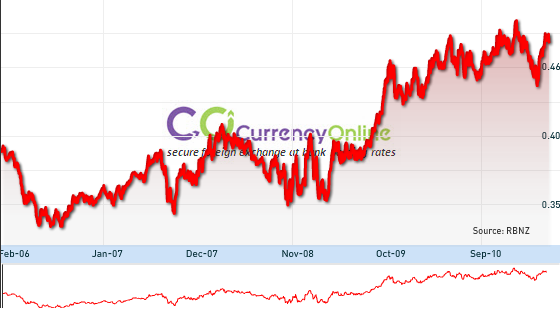

When you look at the NZD/GBP chart below, you’d think it was easy to pick the trend in the last 5 years – up, up and up again. To think five years ago you could get a rate like 0.33 ($3.03 for every pound) and now we are at 0.48 ($2.10 for every pound). On a pension fund of £100,000, it makes a difference of almost $95,000 in your bank account. It’s painful to think about it, because it’s a 30% loss in value.

While the over-riding trend in the five year period looks blindingly obvious, a closer look at the chart shows times when people have made good gains by waiting. For example the significant drop from January 2008 to 2009 is one such period.

Clairvoyancy no cure

Even if you rub your crystal ball and get the direction of both currencies correct over a chosen time frame, you can still muck up the direction of the cross rate. The last 12 months is a good example of this. Both the Kiwi and the pound have risen in value against the USD. The movement in the Kiwi has been quite staggering from 0.65 to 80cents.

| Email questions starkadvice@gmail.com, subject line: Financial Agony Aunt. Anonymity is guaranteed. |

With the pound, there has been an impressive move from 1.42 to 1.67. But twelve months ago, even if a currency trader believed both currencies would appreciate, very few would’ve had a strong view on the cross. Quite often, when both currencies go the same way, nothing happens to the cross – it just range trades.

Twelve months ago, you needed to know which currency would appreciate more and that’s a hard call to get right. The only time it becomes easier, is when the Kiwi goes through one of its big cyclical swings.

It spends years grinding up, then drops out of thin air and that usually makes the cross rate plunge. Some people may say we’re at one of those times now, with the Kiwi getting into the territory of historical highs. But it’s naive to just look at charts and say it must come down, when there have been massive economic changes (like the printing of money in the US) which justify a major shift.

I can honestly say the NZD/GBP is one of the most frustrating crosses to predict.

I spent my early years on a trading floor, telling exporters and importers when to hedge and what direction various currencies would go.

If I’m candid, I used to send up silent prayers each morning that no one would ask about the Kiwi-Pound. You’ll never find a currency trader who will give a decent 6 to 12 month view. They get really shifty in their seats if you want any more than a month out.

With every view comes a wall of caveats about the risks of unexpected economic news and important indicators. I used to traipse over to the trading desk as a 25 year old, to ask if they could reveal their older and wiser secrets, but they had no more idea than me on the pound cross. It was worth it to watch them squirm though.

I would love to give you a view on where the rate will be in 6-12 months, but I’m not close enough to those markets anymore. And I think from what I’ve told you, you’ll realise that a view given by any expert, gets more and more unreliable when you go out as far as 12 months. However, you could ring the international services area of your bank and ask what forecasts their traders are making. They also have the proper legal mandate to give advice.

A change in optics

What I’d like to suggest is that you need to change your perspective on the problem.

Britannia has only offered this GBP cash account in the last year.

In the past the money was simply changed into NZD when the pension transfer took place. They’ve added this service because the currency was moving against clients and getting more volatile, so there was demand for a bit of flexibility to allow for timing the market.

While that’s a good thing, the downside is that you instantly have to start thinking like an FX trader as you only get one shot at changing the money into NZD.

It’s a very difficult situation to manage because pension transfers can take 6 months to go through, so the rate could be vastly different from when you instructed the transfer. On top of that, you now have the opportunity to dilly dally and try and pick an optimal point, without being able to put any hedging strategy in place because the trade is being done by the Trustee of the super-scheme and not you personally.

Options

In normal circumstances it’s sensible to move the money in tranches to get an average over a period of weeks or months, or you would take out an ‘option’.

This is a contract where you pay a percentage fee to the bank, to lock in a rate at a future date, but you don’t have to go ahead with it if it’s more attractive to take the spot rate on the day. Any profits simply get netted out against the spot market and added to your bank account.

If you had the money to pay for the FX-option, you would need to take any net gains and add them to your super-fund. It’s pretty complicated for the average person to manage. Due to the lack of control you have had, it would be easier to tackle things from a different angle:

1. Ask yourself what you can afford to do? If the rate went to 0.55 ($1.81) would it seriously impact your retirement? I don’t know how close to retirement you are, but the less time you have the higher the impact will be. If it would, you are probably running a risk you can’t afford to run.

2. How serious is your mortgage / redundancy situation. If you are not managing to make mortgage payments, there is only so long you can hold on. It would be unwise to put your home at risk, if the situation is serious.

3. If you think you have time on your side and can withstand the stress of the currency going higher, you could look at making a decision to hold out. Currencies are notoriously volatile and there are usually opportunities to wait for a dip. The key is not to be greedy and set an achievable target, close to current levels.

4. At the moment your money is earning no return. The BNZ account held by Britannia pays no interest, so there is the opportunity cost of time out of the market. If you decide you want to keep waiting, set a time-frame, otherwise you’ll wait and wait and keep taking risks. Do not kid yourself that sitting doing nothing is low risk.

5. Don’t beat yourself up over it. Everyone is forced to get on with their life and deal with the exchange rate at the time. Don’t look back and concern yourself with rates from the past. You are where you are, so base the decision on what is affordable from today’s levels. Very few people are ever happy with the rate they get on the day they transfer money, because it’s human nature to expect tomorrow would have been better.

Tax bites and minimum mandatory waiting times

You have said you plan on withdrawing 49% of your fund in order to make a mortgage repayment. Before you do, I just need to question if you have been away from the UK for five full UK tax years (5 April to 6 April; the first part year after your arrival doesn’t count).

If you haven’t been away for five years, there is a rather nasty sting in the tail when you withdraw money.

While Britannia may well give you the cash, because you can claim hardship from a redundancy and the need for debt repayment, they are forced to advise the Revenue in the UK of an ‘unauthorised withdrawal’ and hand over your details.

They will give you the full 49% but you run the risk that at a later date, you become liable for the tax on this withdrawal. It’s an eye-watering 55% penalty, so you run the risk of having more than half the money clawed back. If you have been away longer than five years, the withdrawal can be made penalty free.

Rest assured, Britannia will make you well aware of the risks before they give you the cash.

NZD against the GBP over 5 year period to 26 April 2011

Range during last 12 months: 0.4439 to 0.5035

Here's a dynamic chart showing the NZD against the USD. Scroll back to see historical data.

No chart with that title exists.

NZD against the USD over 5 year period to 26 April 2011

Range during last 12 months: 0.6561 to 0.8074

GBP against the USD over 5 year period to 26 April 2011

Range during last 12 months: 1.4227 to 1.6705

Janine Starks is Co-Managing Director of Liontamer Investments. Opinions in this column represent her personal views and are not made on behalf of Liontamer. These opinions are general in nature and are not a recommendation, opinion or guidance to any individuals in relation to acquiring or disposing of a financial product. Readers should not rely on these opinions and should always seek specific independent financial advice appropriate to their own individual circumstances.

2 Comments

I echo the broad advice here. You can never know whether the exchange rate is going to get better or worse and getting the timing right is doubly hard when you have little or no influence over the timing of the UK transfer.

The main point that investors must ask themselves is whether the money is more useful in New Zealand - and do you need it right now? Sometimes I see people really pushing to transfer from the Civil Service or Police or National Health Service schemes that have superb, guaranteed defined benefits and public-purse funded inflation-proofing built in.

As a general rule, with these schemes, the transfer value increases as you get older and accumulate more benefits in the UK scheme. So by leaving it where it is, the transfer value will increase over time, thereby gving your fund some growth.

In some cases, the best advice is to wait until you get nearer to retirement age. The transfer value will be larger and the exchange rate may have improved somewhat by then. Sometimes a pension surplus develops and is distributed to members, even if you left active service some years earlier. As long as you are still in there, you will get a share. You can ask the UK scheme how many discretionary increases like this have been made in the last 10 years to give you an idea. Just keep in touch with the UK pension provider, so they know where to find you if things like that happen. They must, on request, let you know what you transfer value is, free of charge, once a year. Keep tabs on it.

The thing that worries me about NZ-based pension transfer companies is that their reason to exist is to transfer money. Yet sometimes it's not the best option and some British advisers were prosecuted in the 1990s for such reckless transfer advice. I am not convinced that NZ agencies that do this job for you will not research whether it is the best advice, and may well get you to sign waiver forms so that you can't come back to them in 20 years time when it turns out that this was not in fact the best thing to do.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.