The Financial Markets Authority (FMA) expects KiwiSaver fees to come down more aggressively than they have since the scheme was first introduced.

The regulator maintains the steeper drop will come as the scheme gains scale and a proposed law change, requiring providers to be more transparent in disclosing fees and projections of what members’ balances will look like on retirement, enhances competition.

The FMA’s KiwiSaver Annual Report shows in the year to March, KiwiSaver members paid $326 million in fees (administration fees, investment management fees, trustee fees and ‘other expenses’).

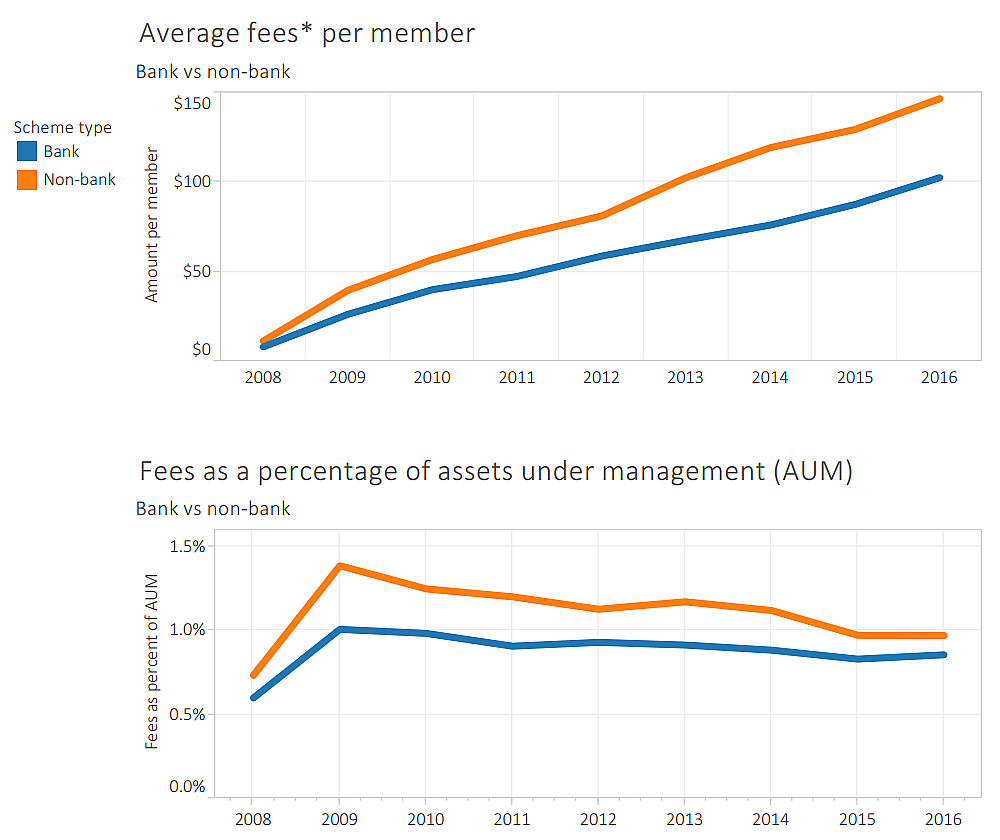

This made up 0.97% of the scheme’s net assets under management (worth $33.8 billion) - a drop from 1.03% in 2014, 1.08% in 2012 and 1.59% in 2010.

You can see the trend in the FMA graphs below. Note its figures are slightly different to those listed above, as the FMA hasn’t included ‘other expenses’ (communications to members, auditors, legal and custody fees) in its ‘total fees’ calculation.

While KiwiSaver providers have been accused of not reducing fees by as much as they supposedly could, as the scheme becomes established and economies of scale theoretically reduces their costs, the FMA’s chief executive Rob Everett says fee levels are “nowhere close to egregious” when compared to that of similar retirement savings schemes overseas.

Yet he believes the tide is changing.

More informed investors will spark more competition

The Ministry of Business, Innovation and Employment (MBIE) on Wednesday released a consultation document to KiwiSaver providers, asking for their feedback on its proposal to require them to include the following information in their members’ annual statements:

1. A dollar figure of the total amount the member has paid in fees. Currently fees are typically only shown as a percentage.

2. A projection of what the member’s KiwiSaver balance will look like when they retire, and how this will translate into retirement income.

Here’s a sample of what MBIE would like annual KiwiSaver statements to look like.

The FMA, along with the Commission for Financial Capability (CFFC), has been working with MBIE to advocate for these changes, which Commerce and Consumer Affairs Minister Paul Goldsmith appears supportive of.

“It is my expectation that any regulatory change required will be in place for the next annual statements and that KiwiSaver providers will already be working towards providing their members with the total fees they are paying,” he says.

Everett believes that if pushed through, the law change will impact fees “without a shadow of doubt”.

If KiwiSaver members can better understand what they’re paying in fees, they’ll ask more questions and spur greater competition among providers.

“We always felt KiwiSaver needed to get significantly bigger before competitive pressures would drive fees down. We haven’t seen any huge sign of that until recently…

“We think we are probably in an environment now where providers are going to have to differentiate themselves in a way they didn’t have to before.”

While new KiwiSaver provider, Simplicity, has endeavoured to do so by offering lower fees, Everett recognises other providers may choose to use other means, like engaging with their members more or improving the way they disclose information.

KiwiSaver members moving towards actively managed schemes charging higher fees

Everett recognises that with a number of people already in KiwiSaver, providers are turning their attention to getting investors to switch between schemes.

In the year to March, the number of people enrolled in KiwiSaver grew by just 4.8% - a drop from 9.6% in 2014.

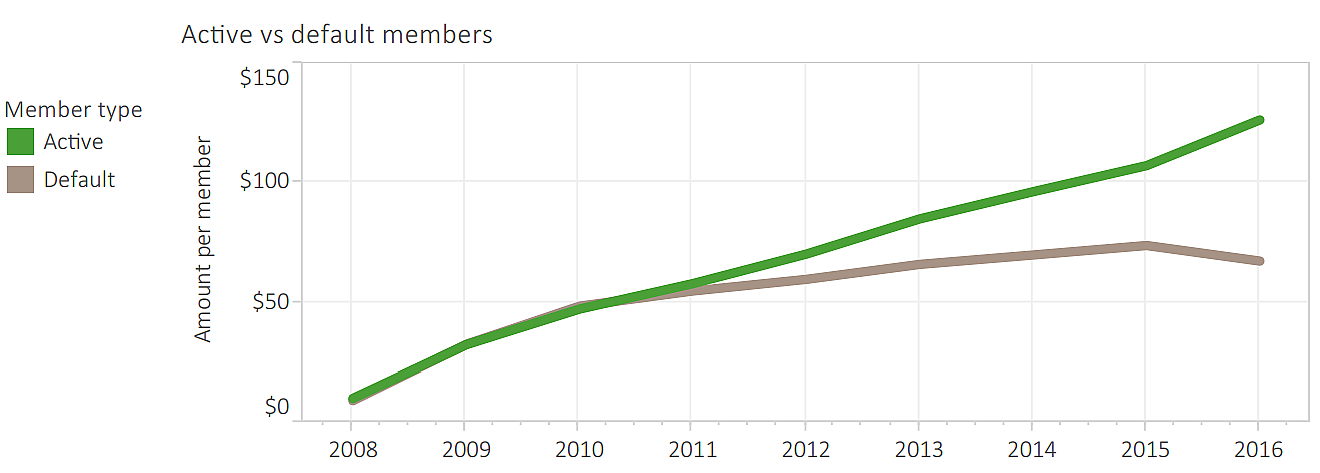

Yet there’s been a consistent uptick in the number of people becoming more involved in their KiwiSaver accounts and choosing to opt for actively managed schemes, rather than staying in default schemes. The portion of members in active schemes increased to 83% from 80% in 2014 and 77% in 2012.

While your returns are likely to be higher, you’ll also incur higher fees being in an active fund. On average, active fund members paid $126 in fees last year and made $520 in returns. Default members paid $67 in fees and made $394 in returns.

“Higher risk and allegedly higher return funds in theory require more work from the fund manager, because they have to work harder to find that return. It does have a knock on to what you’re paying,” Everett says.

Market forces to ensure fees are reasonable even if law doesn’t

The pinch is, more people are moving to active schemes (members not in default schemes), but the current legislation specifies the FMA is responsible for ensuring ‘default’ schemes have ‘reasonable’ fees.

Yet Everett is confident market forces will be strong enough to ensure providers are striking the right balance between fee levels and returns.

This is not to say we won’t see the emergence of more actively managed schemes, which charge even higher fees.

“The philosophy is that there’s going to be enough data out there on the schemes and on their returns and fees, for that competitive pressure to mean you don’t get to that point [where fees become unreasonable],” Everett says.

Asked at which point the FMA might consider fee levels unreasonable, he says: “We haven’t set ourselves a trigger point.”

He says the legislation doesn’t define what ‘reasonable’ is, yet notes the FMA has stepped in when it’s believed providers have set fee levels too high.

“If a provider can give a reasonable basis [for why its fee levels are what they are] and preferably disclose it… we probably wouldn’t push beyond it," Everett says.

3 Comments

I like these proposed changes and think that they will help. I'd also like to see people made more aware of what fees are chopping off their potential retirement balance.

Big KiwiSaver providers have had it too good for too long and have been able to make a mint by masking what they are actually charging. There's no way to justify 20% or more of your returns being eaten up by fees.

I've written about why I'm switching to Simplicity here: http://ryanjohnson.co.nz/why-im-switching-my-kiwisaver-to-simplicity/ It's my own unbiased opinion.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.