Assistant Reserve Bank Governor Christian Hawkesby says the RBNZ’s main focus at this point of the coronavirus crisis is making sure the banking system remains strong.

Echoing comments Governor Adrian Orr made on Tuesday around confidence and cashflow being key, Hawkesby said the RBNZ is looking at how funding markets and banks’ relationships with their coronavirus-affected clients are holding up.

“That’s really our first point of call and our main focus - at least in these initial stages,” he told interest.co.nz.

“We have a well-capitalised banking system and a well-funded banking system.”

ANZ NZ CEO Antonia Watson on Tuesday told interest.co.nz ANZ NZ is in a good position in a liquidity sense. Concerns in this area were a major issue in 2008 and 2009 during the Global Financial Crisis.

ANZ NZ’s chief economist Sharon Zollner on Monday said that if stresses in the financial system start to emerge, there could be a case for the RBNZ to lower bank capital requirements to help keep credit flowing.

Asked whether the RBNZ was considering pushing out the seven-year phase-in period for its new, more stringent capital requirements, which banks need to start implementing from July, Hawkesby said: “I think that’s a conversation for down the track. It’s not something we’re focussed on at the moment.”

OCR cuts can help increase demand, not create more supply

Hawkesby, like Orr on Tuesday, hosed down expectations of large, if not emergency, Official Cash Rate (OCR) cuts in the immediate future.

He said the government could move with more haste than the RBNZ, targeting those most affected by coronavirus.

Finance Minister Grant Robertson is working with banks on the potential for future working capital support for companies that face temporary credit constraints.

More details around this and a wage subsidy scheme will be revealed next week, when Robertson is expected to shed more light on his “business continuity package” being developed.

Hawkesby said: “What we need to think through is, to what extent is it [coronavirus] a supply-side issue around supply chains; around specific sectors being affected - in which case monetary policy can’t provide direct help.”

He said monetary policy would be useful if there is a spill-over effect and a lack of demand and confidence across the economy.

Asked whether the RBNZ would feel compelled to cut the OCR - not necessarily because it believed this was the most effective response, but because the government wasn’t doing enough - he assured: “We know the government is working really hard on this.

“We can see the amount of coordination that’s going on, we can see the amount of assessment, we can see the number of options that they’re looking at… we can see the will to deliver it, and that’s great from our perspective.”

Hawkesby said the RBNZ needed to “look beyond coronavirus” and consider its inflation and employment targets (which are currently being met).

As for moving in tandem with other central banks, in part to prevent the New Zealand dollar from appreciating and making New Zealand exports relatively expensive, Hawkesby said the RBNZ looked beyond short-term currency volatility.

He noted the New Zealand dollar remains weak against the US, despite the Federal Reserve cutting its benchmark rate by 50 points in an emergency move, as markets have already priced in an OCR cut of between 25 and 50 points for March. The OCR is currently at 1% and is next due to be reviewed on March 25.

Central government sign-offs required for deploying unconventional monetary policy still being worked through

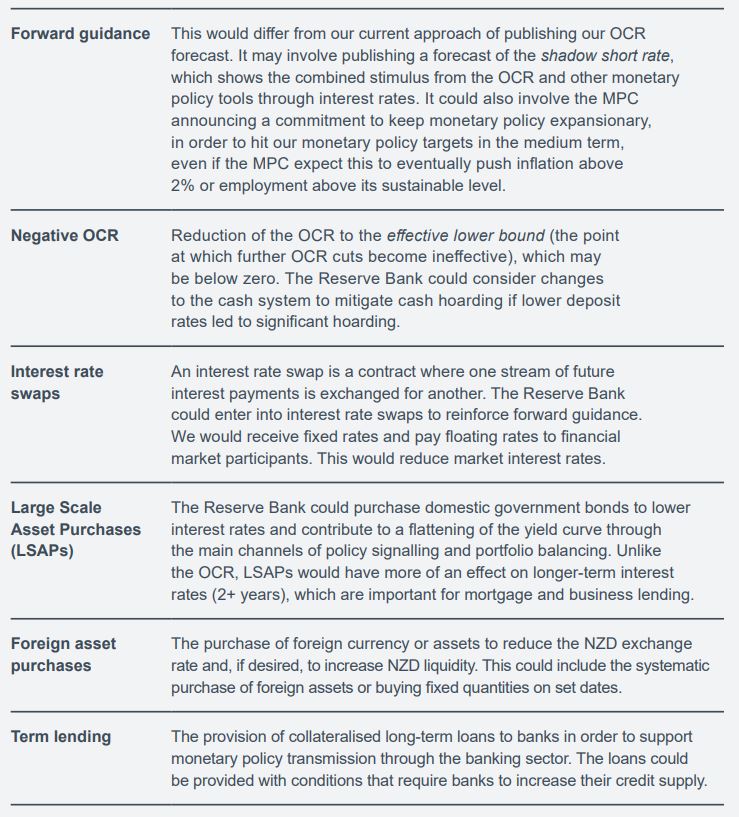

Hawkesby also ran through the unconventional monetary policy tools the RBNZ has been building capability around for some years. These are tools the RBNZ could deploy if the OCR falls to zero and is no longer useful in helping the RBNZ meet its inflation and employment targets.

Hawkesby said the RBNZ, Treasury and Minister of Finance were still working through governance arrangements around deploying these tools, so that “everyone knows where they stand in terms of what they have scope to make decisions on, what they are required to ask for permission to do, what they are required to keep another party informed about”.

The RBNZ indicated on Tuesday its preference would be using tools like forward guidance, a negative OCR, and interest rate swaps that work in similar ways to the OCR by mainly influencing interest rates.

Their side-effects are better understood and they’re known to have smaller financial impacts on the RBNZ and Crown balance sheets than the other tools in its suite - large scale asset purchases, foreign asset purchases and term lending.

Nonetheless, the RBNZ said the tools it may use will depend on what will be most effective, efficient and improve the soundness of the financial system.

Hawkesby and Orr stressed we aren’t at the point where unconventional monetary policy needs to be used.

Here's a run-down of the RBNZ’s unconventional monetary policy tools:

23 Comments

BoE just cut 50bps in emergency cut. But Orrs smarter?

https://www.cnbc.com/2020/03/11/bank-of-england-cuts-main-interest-rate…

BoE don't want to take the risk of sitting on their hands when they could have taken actions to protect employment. RBNZ and the New Zealand Government have demonstrated an exceptionally high risk appetite to date but maybe they have some additional data we can't see that indicates a reduced impact compared to other OECD economies? We will see if they are as clever as they think they are.

Under the RBNZ’s unconventional monetary policy tools "Negative OCR". That's hardly going to persuade people to keep their savings in NZ resident banks and would very much lead to "cash hording", due to:-

1) If saving rates drop to virtually nothing then there's simply no incentive for people to keep their money in the bank and everyone will look to move their capital in to alternative investment vehicles (such as gold) or may literally cash hoard and stuff it in to their mattress.

2) In NZ we still do not have any Term Deposit Saving Government Guarantee which the rest of the Western world has, so again there's no incentive for people to keep their money in a savings here. People will look to move their capital else where even off shore to a country that does have Government Saving Guarantee.

I have no problem accepting that crooks run banks, their ultimate objective being making more money for themselves and their masters (major shareholders are assume). And they do pump up property prices to continue lend more and more. But you have to explain why they prefer to lend money to property buyers. Their ultimate objective of making money is agnostic to the money being from whom and what the bank is lending to.

When you look at it, NZ economy does not offer many (if any!) serious economic opportunities. NZ is good at primary industries and those are invested to a saturation. We already have the farmers with too much debt problem and that sector is too risky to lend to with prospect of returns being what they are. Things like utility and other major infrastructure are not too bad, but these are not private and it is the government who decides what needs to be done. So not too much opportunity for the banks.

I know people hate increasing house prices, but this is the lesser evil (at least from the perspective of central bankers and politicians) than facing the reality of recession and stagnation. Kicking the can one more step hoping for a miracle is sort of the only response possible.

This is exactly right.

If returns get down to nil in NZ, I am more than ready and willing to move all my savings overseas (a good part of it being in term deposits expiring with the next three months), to a country (or countries) with deposit guarantee and a small positive return.

Being myself also a citizen of the EU, it would be extremely simple for me to do so. But this process would be quite straightforward for any NZ depositor.

The only disadvantage would be a one-off hit due to the currency conversion/s, but this can be minimised if done smartly, and it would be more than compensated in the medium term by better security and higher returns.

I currently have only 10% of my savings in shares, and another 10% in bonds. I am definitely not going to increase my allocation to shares (even though I know that I will regret this in a few years time, as there are very good bargains now in the stock markets), as my appetite for risk is quite low at the moment.

So can someone please explain to me how negative interest rates would help the economy ? How are they going to prevent cash hoarding? So they already know the response but still want to take that form of action? It really looks to me that dropping the OCR constantly over the last few years was a bad idea.

They want to follow the failed ECB policy and destroy savers and the bond market at the same time. All they need is a crisis like the virus to then use as an excuse/cover for getting rid of physical currency - a la the crook govt in India - and poof...the black economy disappears and govt tax take goes sky high. Or, at least that’s the genius plan...

The Government needs to step very carefully here. They are at risk of showing that they do not really support the common person on the street but only those with money. Negative interest rates will mean our banks can start charging us for having money on deposit. They already fleece us on fees for services. I for one will be working with cash and requesting to be paid in cash (look forward to see how that goes down!) if they go that far.

Negative interest rates do not and cannot help the economy, they just pass more power over money/credit creation to the banks, which ultimately passes more control of the economy over to the banks and out of the Governments hands. It is in effect a cop out by the Government. Having already screwed the economic structure of the country over the last 30 - 40 years they have now almost run out of options on how to manage it with out creating an awful lot of pain.

To be honest, dont think negative interest rates would do much. Firstly, even OCR becomes negative, the banks wont pay you to have mortgage as there is always a cost involved. Secondly, you might not be able to borrown much anyway as the lending restriciton would be even tighter. Thirdly, business confidence might not get better as people know if current economy situation need OCR cut to negative, our economy isn't performing well. Also it's will be bad for the banks as well. They need to come out a new plan on how to keep their client's money in savings when deposit rate becomes negative.It's a lose-lose situation for everyone except the existing borrowers. I agree with you Carlos, dont think dropping the OCR constantly for the last few years was a good idea. It seems we used our bullets way too fast.

OCR cut may benefit only the existing borrowers. Will it prompt people/businesses to borrow more ? Not likely in the present uncertain times. So reducing OCR is not a good idea and RBNZ knows it. That is why it is angling for more Government action, like priming the pump with cash infustion, budget assistance, etc.

NZ economy is not strictly like the major western economies. It needs its own medicine, not a generic one.

A reminder for those who may not have seen this from the RBNZ Financial Stability Report November 2017. The RBNZ has been highlighting potential vulnerabilities for a number of years, but most people ignored or dismissed them, as the economic environment was rosy, and house prices were rising, or expected to rise. Now a large negative shock has occurred, more people may choose to sit up and take notice.

Highly indebted households remain vulnerable to negative shocks.

The tightening of lending standards and slowing in housing credit growth have improved the resilience of the banking system to stress in the household sector. However, the growth and concentration of household debt leaves many households, and therefore banks, vulnerable to an increase in interest rates or a decline in household income.

Rapid increases in debt have often preceded past economic downturns and financial crises internationally, particularly when debt has been concentrated among borrowers who could not meet debt payments in more difficult financial conditions. In New Zealand, household debt has risen from 146 percent of disposable income to 168 percent over the past five years (figure 2.5). This debt appears to have become more

concentrated. The Reserve Bank estimates that the average debt to-disposable income ratio of households with mortgages is currently around 325 percent, up from 280 percent in 2012. It is estimated that only 8 percent of households currently own investment properties but these households account for around 40 percent of housing debt. While only a small proportion of household lending is currently non-performing (see

chapter 4), high debt levels imply that some borrowers are likely to have difficulty servicing their debts if interest rates rise or incomes decline.

Most property price optimists don't understand the vulnerabilities to the financial system. They are looking only at property price changes.

I notice that none of the property price optimists are commenting here, so they may be unaware and ignoring the risks being raised on financial stability.

Most people who have read and commented on this article are aware of the financial linkages here and potential implications on real estate prices.

Once again this is where the NZ economy is exposed as the malnourished street kid that it really is. Best thing we could do if it gets severe enough, which it hasn't here...yet, is helicopter money into mid to low earners bank accounts...a nice consumer driven impulse should keep the bones from rattling too much!

Ha - yep I picked it. They are preparing to drop their inflation rate targeting, to ensure asset prices remain as high as possible. In other words, back to the 80's, high inflation is a-OK!

In fact all of their plans appear to be "print money to make sure asset prices remain high!".

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.