By Gareth Vaughan

Is the weak oil price the catalyst for a global credit meltdown or economic crisis?

No, according to Bernstein strategist Michael Parker.

Parker, a Hong Kong-based ex-pat New Zealander, has a look at this issue in a research report entitled Apocoilypse Now...where did that US$3 trillion in oil savings go?

Parker points out the oil price fall from US$110 per barrel in 2013 to an average of US$30 a barrel so far in 2016 is a windfall gain to oil consumers, at the expense of oil producers, of US$3 trillion annually.

He notes the Apocoilypse is premised on the linkage of half a dozen negative market trends being rising trade and current account deficits in emerging markets (ie oil producers), emerging market capital flight, low inflation, falling corporate profits, and a still drowsy consumer. In the Apocoilypse the link between these trends is the falling oil price and rising US dollar.

Parker notes this theory is presented as a self perpetuating loop. Weak oil prices are bad for both oil exporters and the earnings and capital expenditure trajectories of oil companies everywhere. A rising US dollar puts pressure on debt servicing capabilities in emerging markets and US corporate profits and encourages emerging market capital outflows. And falling emerging market currencies export deflation.

"And the ongoing weakness in the oil price is used as evidence that whatever positive economic news you might wish to cling to (China's resilient consumption growth, the falling unemployment rate in the US), is false, temporary or both," Parker says.

Three problems

He cites three problems with the Apocoilypse theory. Firstly, this view requires that the benefit from the fall in oil price to everyone, everywhere is outweighed by the falling credit worthiness of oil producers.

Secondly, the view requires the lumping together of all emerging markets into the same category, - heavily indebted, current account deficit running commodity exporters for whom low oil prices are unambiguously bad.

And thirdly, the theory assumes current energy prices simply reflect macro economic conditions, rather than fundamental changes in long-term supply and demand of fossil fuels.

"Turning low oil prices into a global credit or economic crisis requires that the largest oil-exporting countries hold a great deal of external debt and little or no foreign currency reserves. That those countries are unable to service that debt given low oil prices and will therefore be forced to default, and that the magnitude of those defaults (relative to the size of the global financial system) is sufficient to undermine the workings of credit markets everywhere. In our view the math doesn't work," Parker argues.

'The four flawed horsemen of the Apocoilypse'

Whilst noting that not panicking is out of favour at the moment, Parker goes on to debunk what he calls the four flawed horsemen of the Apocoilypse. He argues expectations of a global economic crisis arising from the combination of weak oil prices, a strengthening US dollar and emerging market debt ignores four things.

Firstly, heavily indebted oil producing countries represent a tiny fraction of global debt, global economic activity and even a relatively small share of oil production.

Secondly, low oil prices are a benefit to anyone consuming energy, which as Parker puts it is everyone, everywhere.

Thirdly, the US$3 trillion reduction in oil proceeds between 2013 and today hasn't disappeared. It has just moved.

"It is a simplistic point but, while houses and bonds offer yield, they are primarily stores of value. Oil is a commodity. It gets consumed. And the businesses and individuals consuming oil either pay more or less for it. If they pay less, they have more to spend on something else. That US$3 trillion in 'liquidity' hasn't disappeared. It hasn't even disappeared from emerging markets. It simply now resides in different hands than it did in 2013," Parker says.

And fourthly, Chinese capital outflows have nothing to do with oil.

"Finally, the greatest problem with the linkage of oil, the dollar, Chinese capital flight and emerging market debt is the diminished role of oil demand growth in the global economy. With energy demand in developed markets falling structurally and China now a post-industrial economy (more than half of GDP comes from services), oil just isn't as important as it used to be," Parker says.

The Mavericks

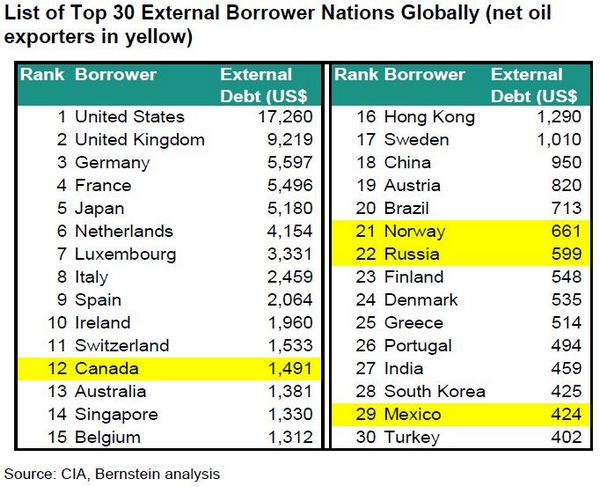

Based on the table below, Parker points out of the world's biggest 30 external debtor nations only four, Canada, Norway, Russia and Mexico, are net oil exporters. Thus every other country on the list benefits from low oil prices with corporate earnings and consumer balance sheets strengthened by falling oil prices.

"It would seem to follow that risk of idiosyncratic credit events in these markets is therefore likely to be falling at present."

Whilst acknowledging Russia - the second largest net exporter of oil in 2014 at 7.5 million barrels a day - as a "clear risk," he points out Russia was only the 23rd largest holder of external debt at the end of 2014 with US$600 billion in external borrowings, has US$400 billion in foreign currency reserves and had a current account surplus last year.

"Middle Eastern oil producers are - for the most part - either sitting on the proceeds from a decade of high oil prices (Saudi Arabia, UAE, Kuwait, Qatar) or - in the case of Iran - haven't been able to borrow externally over the last decade, or three," says Parker.

Whilst some oil producers' sovereign wealth funds may reduce assets under management, the unwind is unlikely to happen overnight and is a long way from the catalyst required for a global credit crisis, Parker suggests.

Excluding the Middle East, he notes the next biggest group of external debtors among oil exporting emerging markets are Mexico at 29 with US$424 billion, Kazakhstan at 39 with US$150 billion, and Venezuela at 49 with US$110 billion.

"Throw in the likes of Angola, Colombia and Ecuador, and the Mavericks (plus Sudan, Tunisia, Chad and Gabon) weigh in at maybe US$800 billion in net external borrowings in the context of total global external debt of US$66 trillion," Parker says.

"Apocoilypse Now! rests on the view that - with the dollar strengthening and the oil price falling - emerging markets, which produce oil and borrow in US dollars, have everything going against them right now. Defaults, devaluation and capital flight are viewed as inevitable. The upward pressure on the dollar, the downward pressure on the oil price and the squeeze across all emerging markets are supposedly self-reinforcing. Yet falling oil prices are a benefit to the US, Europe, Japan and to China, India, Indonesia, Brazil and South Korea. The problems begin and end with the Mavericks. Is that trouble? Yes, for those markets (countries). Is it the start of the global ApocOilypse? Probably not."

Parker also points out that whilst the US$3 trillion swing over three years is massive, it's still a zero sum gain for a global economy which is worth about US$55 trillion annually. Thus, he argues, the fall in oil price is about second order effects. Or how that US$3 trillion is spent or saved now it's in the hands of consumers rather than producers.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

7 Comments

Guess we could look at the milk price in the same way...bit of a wee problem for the producers but hey cheaper lattes all round!!

What this theoretician misses is that oil is THE uber commodity, and the oil price needs to cover not just the costs of extraction but ongoing exploration, and incomes and taxes to maintain a society that can function at the complex level needed for such a space age industry.

"'Or how that US$3 trillion is spent or saved now it's in the hands of consumers rather than producers."

.................this is what we call a garage sale isn't it?

.............

In Benjimin Grahams 'securities analysis' which gives an overview of the circumstances leading up to the great depression, a collapse in commodity prices was a key trigger for the fall in stock prices, and the reduced global demand that followed for years. Took a World war to and a spruiker of a president to spark demand and get them out of it.

Firstly, I'd like to say that this is a very good Internet site.

However, Michael Parker's analysis is extremely poor and flawed in many ways.

'Parker points out the oil price fall from US$110 per barrel in 2013'

Well, actually the big fall commenced in the second half of 2014:

Secondly, he ignores global EROEI, which has been falling for a century and continues to fall.

Thirdly, all oil is not the same; much of what comes out of Canada is not oil but is closer to bitumen, and requires dilution with refined products to make it pumpable. And the cost of extraction, both financial and environmental is horrendous.

Fourthly, the proportion of a nation's economy that is energy-related (and therefore hammered by low prices) is extremely important. Hence, Norway and Canada are 'falling off the cliff' because both have economies predicated on high prices.

Fifthly, global conventional oil extraction has been flat since 2005, and it has been the frantic drilling and fracking (mostly in the US) that occurred between 2010 and 2015 that increased global extraction; that kind of extraction is inherently unsustainable, and is in collapse as a consequence of low prices. In Taranaki over the past year, 'things have come to a standstill' in the oil sector, and it is primarily gas (captive market) that is still holding up. With oil majors like BP and Shell recording collapsed profits or actual losses, capex is very much reduced, leading to a massive decline in extraction further down the track.

Collapse of global oil extraction is not a bad thing when we look at the big picture because 'Oil Apocalypse' is actually here and now for a rather different reason: the use of oil and the combustion products from oil are the major reason for the Sixth Great Extinction Event and collapse of the global environment.

The atmospheric carbon dioxide level has never been higher in human history (404ppm) and has never been rising at a faster rate (about 3ppm per annum).

https://scripps.ucsd.edu/programs/keelingcurve/wp-content/plugins/sio-b…

{kind=link}

The effect of this is already utterly disastrous, and getting worse by the day.

Whereas ice in the Artic normally increases in area in the northern winter, in recent years we have witnessed some melting, and this year that melting is at a horrifying high level: not only is Arctic ice at the lowest level ever but the ice that is there is melting at an unprecedented rate.

47,000 km2 of ice has been lost in recent days, with the most recent update showing 11,000 km2 of ice loss [in one day].

http://nsidc.org/arcticseaicenews/

Should the present trend continue (and it is difficult to see any reason why it will not) we will be entering the 2016 melt season with the lowest ever ice cover (both in terms of area and thickness) and the highest ever atmospheric forcing.

Bearing in mind how close conditions were to ice-free in 2012, logical thinking indicates we could well witness an ice-free Arctic by September this year, and that would completely alter all long-established weather and ocean current patterns, and accelerate the rapid planetary overheating we are already witnessing.

And if it does not occur this year, then an ice-free Arctic is a certainty in the very near future because we can be certain that this issue, which is crucial to survival of the human species (along with most others species) will be completely ignored by politicians, economists, commentators and the mainstream media.

Needless to say, meltdown of the planet will have 'a serious effect on the global economy', i.e. annihilate it. However, ignoring the issue is easier in the short term.

In a few months we will have a better idea how bad the Arctic Sea predicament is..

It is interesting that very very many commentators out in the real world, away from the herd, did predict so much of what we see today. At the time they were variously shouted down, ignored, ridiculed and muffled.

Instead the finance glitter-arty gathered at the feet of the pope of the Church of Finance - one A. Greenspan. True believers one and all.

Reading these 'flawed analyses' confirms in me the belief that its not until crises hit that patterns change. Talking to the true believers ahead of the big event itself is just a waste of oxygen. Trouble is we are all (western civil.) on this Titanic.

So grab the popcorn, the snake of finance is eating its tail; otherwise known as share buybacks. Duetsche Bank shares anyone?

This oil price slump is far from apocalyptic , except for oil producers who have had it too good for too long, and they are largely a bunch of undemocratic , corrupt and dictatorial warmongers .

However , what is possibly apocalyptic are signs of widespread deflation in commodity prices , which may feed through to everything in due course

I dont agree on the "far from apocalyptic" Once or if prices collapse below the cost of production then the suppliers will go out of business, the direct effect is lost jobs, but it continues on. Since they have often used debt to finance the extraction and in going bankrupt the capital is lost that means investors, pension funds and Govns lose money in spades. Looking at how this effect is progressing in the oil producers it does actually look very serious, how serious I dont fathom yet but its not minor.

Well said AWkTTruth,

"The moon stays bright when it doesn't avoid the night,"

Rumi.

And thank you for your patience and persistence.

We have served our future generations and planet abominably, and even worse, the main perpetrators are still in denial!

Jesus was a very compassionate, patient teacher, by all accounts, but even he "lost the plot" with the Money Traders and took the whip to them!!

We are at the same place of exasperation now I think.

When science (independent from Big Financial Agendas) merely causes a rush for the Spin and Propaganda doctors, those so us who are still capable of independent thought, reason and analysis are reduced to shaking our heads in bewilderment at such continuous, financial- agenda-driven Wilful Blindness.

No surprise when we observe the "worship of the Serpents" in control of the "Circus.!"

Even more concerning is The tenuous, fearful Opposition, which merely reinforces the disastrous situation New Zealand has been Spun, Lied and Sucked into.

Our continual worldwide economic/financial disasters appear to have taught "the Masters of War" nothing that shakes some conscience or compassion into their leeming-like greedy, obsessive behaviour.

"ONLY WHEN THE LAST TREE HAS DIED, THE LAST RIVER BEEN POISONED, AND THE LAST FISH BEEN CAUGHT WILL THEY REALISE THEY CANNOT EAT MONEY."

Old Cree Indian Proverb

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.