By David Scobie*

It’s hard to believe that no-one on Earth had a smartphone until 2007. Today, studies show we check them on average about 50 times a day. Meanwhile our “connected lives” continue to broaden and deepen.

In this context, technology has been growing as a proportion of corporate activity and sharemarket capitalisation. In turn, it is increasingly influencing the risk and return outcomes of investment portfolios, whether we are aware of it or not.

This article assesses: Just how prominent is technology in an investment sense? How might that prominence be justified? And conversely, how might that be something to be wary about?

The growth of the FAANGs

It’s likely you’ve heard the term “FAANGs”. There are different versions of the acronym, but it’s a term used to group five of the leading Tech stocks on the market: Facebook, Apple, Amazon, Netflix and Google (now part of Alphabet). We could extend that out to other big Tech companies – Microsoft being the most obvious candidate, or the Chinese “BATs” as they are known – Baidu, Alibaba and Tencent. But let’s focus on the FAANGs for the moment.

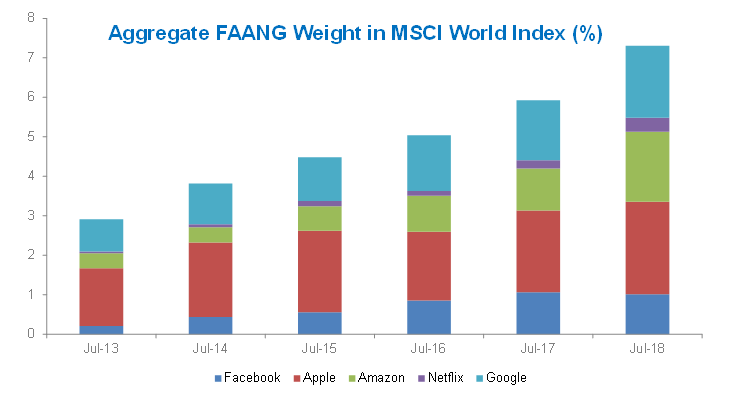

It’s clear that the FAANGs have been growing in importance as a proportion of the MSCI World Index. As the chart below shows, their collective market cap in 2013 was a touch under 3% of the Index. Five years on, that weight has grown quickly to nearly 8%. So there’s a fair degree of concentration occurring in a handful of stocks.

But the FAANGs didn’t get there by some sort of fluke of course, which brings us to our first positive – there has been some impressive performance going on.

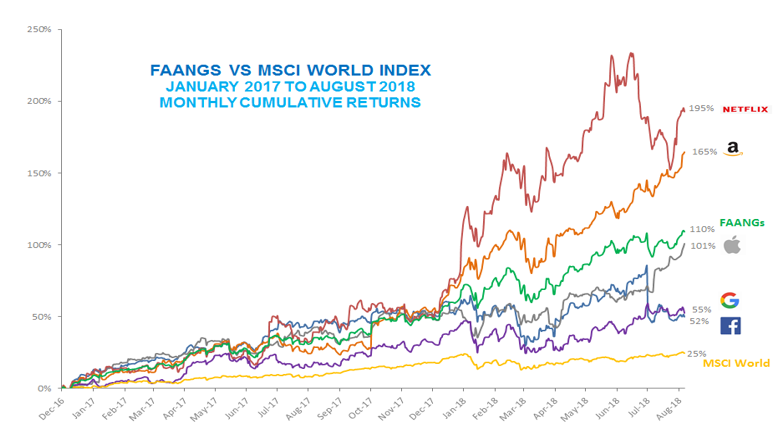

The chart below shows the share price growth of each of the FAANGs, and the wider market, since the start of last year. The MSCI World Index is up a solid 25%. However, the FAANGs have surpassed that figure, helping to pull up the overall Index. Leading the charge have been Netflix and Amazon which have risen by the better part of 200% over that time period. In fact, since 2009, Netflix has appreciated nearly 5000%! So it is not hard to deduce that investors not owning the FAANGs have struggled to generate returns as favourable as the overall market.

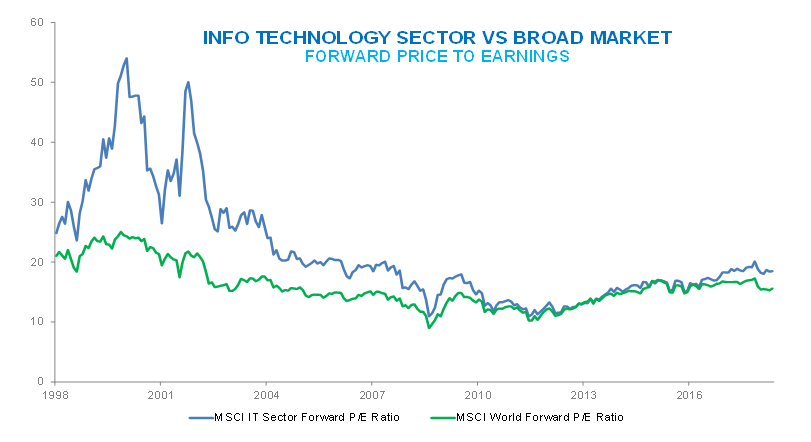

It’s worth noting that technology is not just a short-term performer. The sector has had its ups and downs but, taking the US as a reference, since 1990 an investor would have been materially better off having pure exposure to the tech sector than the S&P500 Index as a whole. We know things got rather heated for tech stocks leading up to the year 2000, which does bring to mind the question of whether we might be in a similar valuation scenario today.

The chart below shows the forward price-to-earnings (PE) ratio of the tech sector versus the wider global equities market over the past 20 years. We can see (to the left) that there was a clear disparity around the time of the Dotcom boom, with tech registering a Forward PE of around twice the overall market. However, that isn’t the case these days, where we can see (to the right) that the difference is relatively modest.

We have witnessed notable price increases of tech stocks, but earnings have been running strongly to underpin that. Taking Alphabet as an example, revenue last year was US$110 billion and is currently growing at 23% per annum.

It’s true there are some tech stocks that appear speculative on a PE basis, but among the prominent names, Apple trades at a respectable 17 times forward earnings, Facebook 20 times and Alphabet 24 times – so not as lofty as one might expect.

Tech stocks also have some notable tailwinds worth mentioning:

- They are capitalising on mega-trends. Think e-commerce, mobile payments, artificial intelligence, cyber-security and gaming. Disengage from those trends at your peril.

- On the economic front, part of the strength in FAANG stocks this year has been due to a belief that they are a relatively safe haven in a world of rising trade tensions. While not totally immune, we can expect the functions of streaming, social network posting and buying and selling online to carry on regardless of that threat. As tech companies are often service-oriented, they are less “tariffable” and are difficult to prevent from crossing international boundaries.

- Some of the balance sheets of the tech companies are in very good health. We know that low debt burdens are a helpful guard against uncertainty and the prospect of higher interest rates. Apple holds around US$250 billion in cash and liquid reserves, while Microsoft holds around US$100 billion. During the Dotcom boom, cash held by tech companies as a group was only a few percent of their market cap, whereas today that figure is well into the double digits.

Finally in the positive camp, the market concentration argument is perhaps a little overblown. The top five stocks in the MSCI World Index today are all in a broadly-defined tech sector, and as noted, comprise around 8% of the Index. While this may seem like a lot, it is not abnormal, and in fact is just below the average for “top five” stocks over the last 50 years. Other companies have been more dominant in years gone by, including IBM in the 1970s and AT&T in the 1980s - each of which had Index weights in the order of 4-5%.

Too much trust in tech?

So far the picture painted for tech stocks has been all favourable. However, no matter how rosy things might seem now, it can be dangerous to project good times too far into the future. Investors have had other periods of “perceived enlightment” over the years which turned out to run out of steam, be it gold in the 1970s, Japanese shares in the 1980s or Chinese shares in the 2000s. Humans being humans, we are prone to hubris from time to time. Meanwhile, the world and markets evolve. What is hot can become not so much.

On that note, it can be interesting to consider where investor money has been flowing in recent years, especially for those with a contrarian mind-set. If flows into tech funds carry on this year at the same rate as they have so far, 2018 will see flows double that of last year and substantially above prior years. To take the case of the largest technology Exchange Trade Fund - the QQQ which tracks the NASDAQ Index - the Fund has taken in over US$2.5 billion during the last year alone and is now the world’s 8th largest ETF.

Professional traders are also inclined to be heavily weighted towards the tech sector. Each month, Bank of America Merrill Lynch puts together a list of the “most crowded trades” for hedge funds. The FAANGs and the BATs have just spent seven months in a row at the top of that list. Tech is clearly a popular sector of the market to be betting on.

We touched on price-to-earnings ratios earlier, but how do the FAANGs look based on the measure of price-to-book value? Interestingly, for the global tech sector as a whole, the current ratio of around six times book value doesn’t seem too stretched at the moment versus history, especially compared to the Dotcom period where it peaked at double that figure. However, the FAANGs as a group have pushed well ahead in recent years, with their share prices on average now sitting at around 17 times book value (Amazon and Netflix are well out in front). The high ratio of the FAANGs may be justified by their strong brand values not being fully recognised on balance sheets, but history suggests some caution may be warranted.

History also tells us that markets can treat the tech sector harshly from time to time. Price volatility can be hair-raising, especially when investors get word of companies not delivering on high expectations. We saw that with Facebook earlier this year. The company’s share price ran into weakness in March, staged a decent rally, and then plunged 20% in late July after reporting weaker than expected profits. In a dramatic case of mass-unfriending, we saw FOMO (fear of missing out) quickly become FONGO - a Fear Of Not Getting Out.

It probably didn’t help that over 90% of brokers had a “buy” rating on Facebook prior to the July earnings announcement, but the experience tells us that when a stock like Facebook falls, it can fall hard. The company’s decline in value in one day of US$120 billion exceeded the entire value of the New Zealand sharemarket. It was also the largest ever one-day loss for a US public company. Of the other candidates across the years for that dubious honour, six of the top 10 are technology stocks, with 2nd and 3rd places filled by Intel and Microsoft - with their falls occurring during the tech fallout in the year 2000.

The other reason one might be wary about tech stocks is that they end up simply getting “too big for their boots”. The reality is that a greater sphere of corporate influence can attract greater scope for Government intervention. This might be in the form of regulation, or more drastically the breaking-up of companies as happened with the US telecoms monopoly in the 1980s. Recently we’ve seen substantial fines being imposed on Google in Europe for anti-competitive behaviour, and most of the FAANGs have been accused by authorities of underpaying tax by sizeable sums. All these factors have the potential to put a big dent in profitability.

We should also not forget the buzzword of the moment – “disruption“. Innovation is relentless and no tech company can afford to rest on its laurels - just ask Nokia or Blackberry. These days the major US players don’t just have to look over their shoulders; they have to look to the East which is catching up fast as the new Silicon Valley. China already leads the world in online payments, is there or thereabouts in AI, and is increasingly home to the world’s largest internet companies. The threat for the likes of the FAANGs is not just that Chinese companies might carve into their market share in the US, but that they might completely take out growth markets such as South-east Asia and Africa.

The last bite

When it comes to considering the merit of any group of stocks, valuation will always matter, so as to protect the investment downside. And we can’t assume that today’s tech titans won’t have their market leadership positions seriously challenged over time. We only have to look back a few decades when investors paid sizeable premiums for the so-called “Nifty Fifty” stocks - iconic businesses of the day such as Polaroid, Xerox, GE and Texas Instruments. The stocks were often described as "one decision" trades in that, in theory, you could buy them and hold them for life. The trouble is, their fortunes faded, and now stand as a warning of the heavy price to pay for over-enthusiasm regarding the long-term outlook.

But for all that, it can’t be denied that technology will continue to dominate the face of economic progress. And in contrast to the Dotcom era, today’s FAANG phenomenon is powered by big companies, with strong revenue streams and credible business models. It’s a brave person who says the tech sector doesn’t justify a significant place in investor portfolios.

In summary, keep your eyes on the trends, but don’t be too afraid to get your teeth into the FAANGs!

*David Scobie is Head of Consulting at Mercer Investments, based in Auckland. He advises institutional clients on their investment policies, structures and fund manager selection, linking in with Mercer's global research capability.

This article does not contain investment advice relating to your particular circumstances. No investment decision should be made based on this information without first obtaining appropriate professional advice and considering your circumstances.

Data source for charts: Datastream.

2 Comments

This is an opinion and not written to offend the author.

The FAANG's have been inflated well beyond the realities of their medium term earnings capability (P/E ratios) and with the exception of Apple (which I do not hold) seem incredibly expensive by any recognised valuation metric - none pay a dividend and all are relying on growth with prices well beyond any ability to pay a dividend for some considerable time. The word bubble could just as easily be applied here as it could to Bitcoin before Christmas 2017. (except 'Bitcoin's are rat poison' Warren Buffett, April 2018)

'In summary, keep your eyes on the trends, but don’t be too afraid to get your teeth into the FAANGs!' is advice that is echoed by a number of institutional investors at the moment, it will be the 'mum and dad' investors that end up picking up the tab in a reversal. Be cautious with the FAANG's they could bite.

NB. I hold no position in any of the above mentioned stocks either ownership or 'short'

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.