By Gareth Vaughan

Moody's is warning a fall in the asset quality of dairy loans on the heels of Fonterra's reduced payout forecast would have a material effect on New Zealand's major banks, although the credit rating agency doesn't expect non-performing loans to increase as much as they did last time the dairy payout dropped sharply.

Fonterra cut its 2014/15 season forecast payout for farmer-shareholders by 60 cents to $4.70 per kilogramme of milk solids last week, which is well down on the record $8.40 2013/14 season payout.

Daniel Yu, assistant vice president and analyst at Moody's financial institutions group, unsurprisingly warns the reduced Fonterra forecast is credit negative for New Zealand banks. Because a lower payout reduces the income farmers receive, this threatens the asset quality of banks exposed to the dairy sector, says Yu.

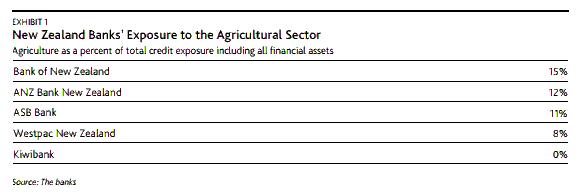

He notes among New Zealand's big five banks ANZ and BNZ have the biggest exposure to the agriculture sector with dairy loans comprising an average of 69% of banks' total agricultural loans as of March 31 this year.

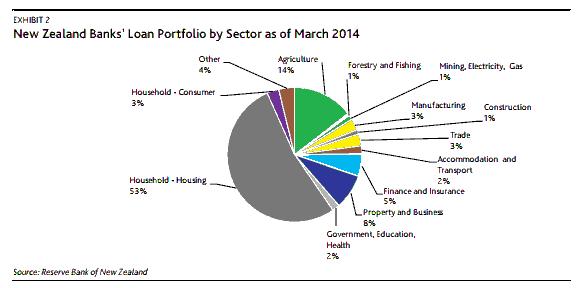

"A deterioration in the asset quality of dairy loans would have a material effect on the banks," says Yu. "New Zealand’s agricultural exposures comprised the second-largest sector concentration in bank loan portfolios as of March 2014, after housing loans," says Yu.

"When the dairy payout last dropped sharply in 2009, banks’ agriculture non-performing loan ratios, which include impaired loans and loans 90 days past due, spiked to 3.92% of total loans at September 2010 from 0.20% at September 2008. Moreover, a weakened dairy sector risks having a meaningful second-order negative effect on New Zealand’s economy," he says.

Nonetheless Yu says Moody's doesn't expect non-performing loan ratios to return to September 2010 levels because farmers have become more cautious since then and didn't respond to the record payout this year by significantly increasing spending and debt.

"Furthermore, farmers knew well in advance that 2015 prices would be lower than 2014 levels, allowing them to manage down expenses and defer any significant capital expenditures."

Yu says another important factor is Fonterra’s payout price is an average price for the season.

"Fonterra’s forecasts rose progressively during the 2014 season, implying that farmers would have received additional income at the end of the season to compensate for the lower price they received in the early part of the season. This additional income late in the 2014 season should provide some buffer to their lower expected 2015 income. In addition, if milk prices were to recover in the 2016 season to the long-term average of $6.00, it would contain the challenge to bank asset quality from Fonterra’s 2015 price drop."

"Declining milk prices are a result of demand and supply factors. Slower economic growth in China, a major export market for New Zealand’s milk producers, has weakened demand. Exacerbating that effect is the strength of the New Zealand dollar. Meanwhile, last season’s high milk price has resulted in more investment to increase the global supply. At the same time, Russian import restrictions have closed a major market to milk producers in the European Union, adding to the global milk glut," Yu says.

Moody's has Aa3 ratings on New Zealand's big five banks - ANZ, ASB, BNZ, Westpac and Kiwibank - with stable outlooks. See credit ratings explained here.

No chart with that title exists.

9 Comments

It's not so much the debt per se but no money (at this point) being paid by Fonterra in July/August/Sept/Oct for retrospectives. Retrospectives = cashflow. No cashflow = potentially more debt. Payment for milk doesn't usually get to relevant amounts until Sept for North Island and October for South Island for Fonterra suppliers. Oct/Nov/Dec are usually the most expensive months for operational costs.

Interesting that the chart shows that, after a period of restraint, the agriculture sector suddenly borrowed $2bn in the last 6 months. This was during the period of record dairy payout. I thought dairy farmers were using the payout to pay down debt?

Total ag debt would appear to be about 200% of total ag GDP ($28.5 bn in 2012).

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.