Tower warns customers should brace themselves for further premium hikes, as it braces itself for another year of extraordinarily high weather-related claims costs.

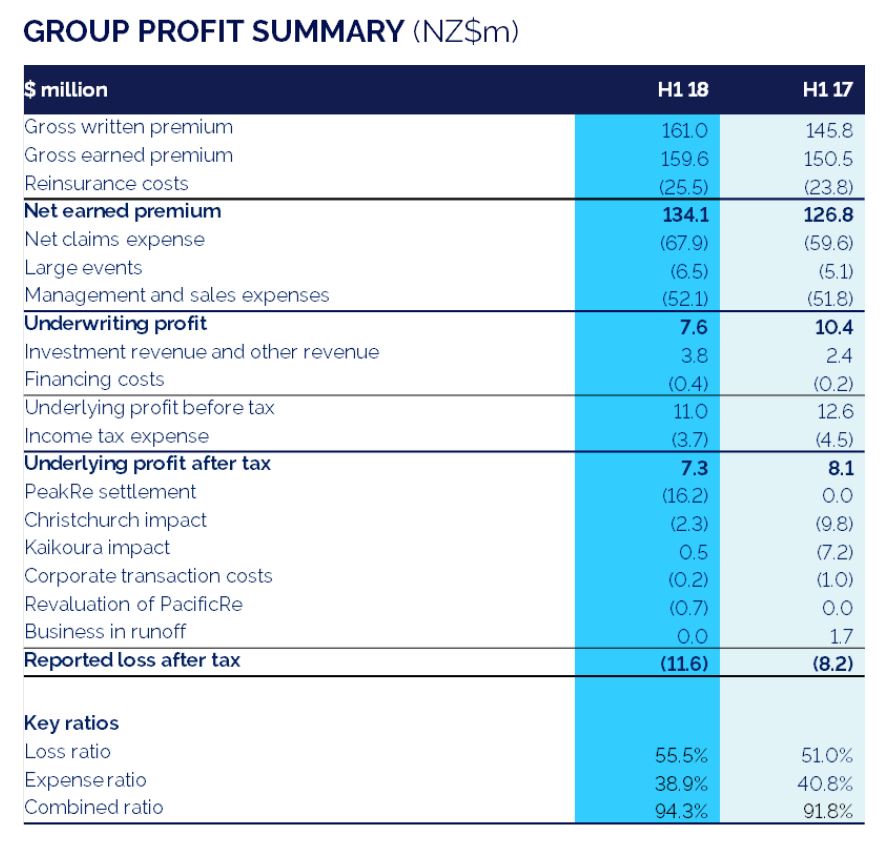

Weather events saw the insurer take a $5 million after-tax hit in the year to March 31, contributing to it widening its half year loss to $11.6 million.

Taking the April 2018 storms into account, Tower paid more in weather-related claims in the first seven months of the 2018 financial year, than it did in the full 2017 financial year, when it took the hardest beating from the elements in 25 years.

Tower expects it will have used up its “non-catastrophe reinsurance” by the end of the financial year, so plans to buy more reinsurance to keep it covered for the rest of the year (note is should have “catastrophe” reinsurance to cover it in the event of an earthquake).

Tower recognises in its results that the more costly its claims, the more expensive its reinsurance becomes, and thus the more it’ll charge policyholders in premiums.

“Tower is putting in considerable effort and taking all appropriate steps to preserve capital and reduce any volatility from these short-term weather abnormalities,” it says.

Risk-based pricing gets underway

Tower’s results show the extent to which it - like other insurance companies facing the same issues - had already hiked premiums in the half year to March.

A change in pricing saw gross written premium (GWP) in its core book increase by 10% in the half year (compared to the first half of 2017). Meanwhile policy volume growth saw its GWP increase by 5.6% - the total core book increase being 15.6%.

Further to it in its 2017 full year results suggesting improved technology would see it use more granular data to better price risk, Tower says it’s managing its claims costs through “better risk selection and underwriting processes”.

It is also “working harder” to attract new customers, “particularly in attractive segments which are actively targeted”.

Looking ahead, Tower’s GWP will be affected by a new “risk-based pricing” model for earthquakes which it introduced in April.

It says this will “provide significant competitive opportunity in lower risk areas, and deliver fairer, more equitable pricing across all of New Zealand”.

Tower in April said that under the new system the “vast majority” of its customers wouldn’t see any significant change in their premiums, yet less than 2.5% would see the insurance risk part of their premiums increase by more than $250 in a year.

Asked to go further in providing a granular breakdown of how its pricing would change, Tower told interest.co.nz that 1% of its customers would see increases of more than $2,000 - of this one quake-related component of their premiums.

Tower wouldn’t reveal the portion of customers that would see increases of between $150 and $250, and importantly, the portion that would enjoy premium decreases.

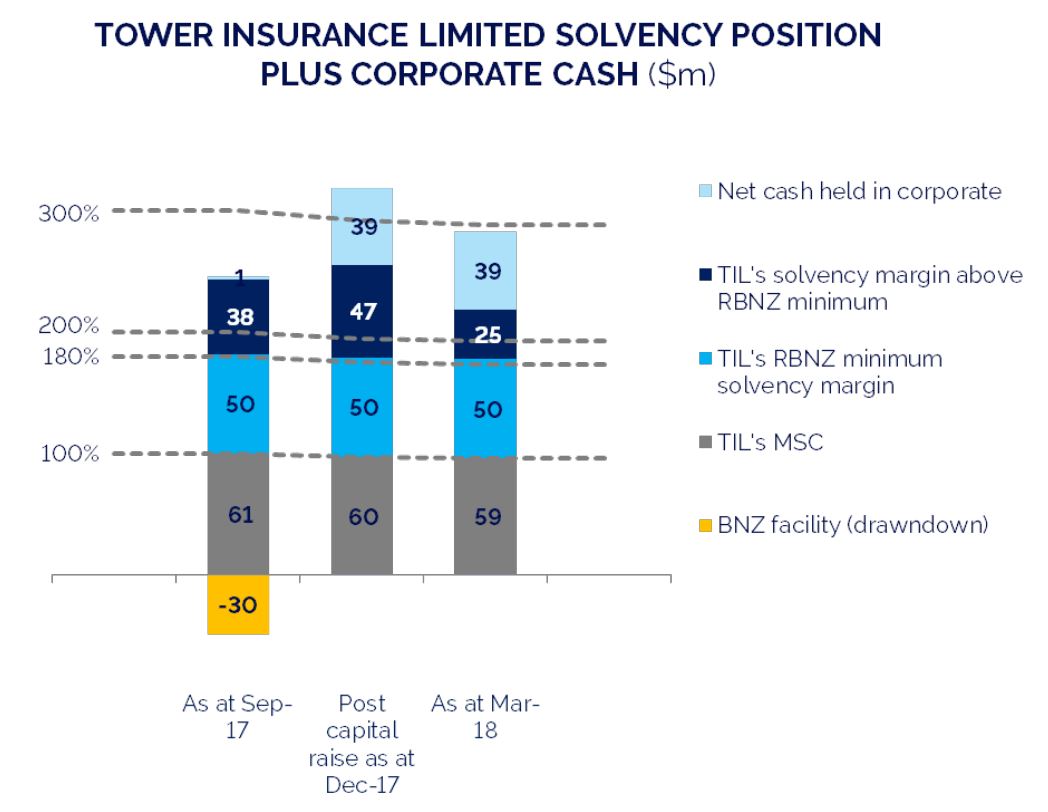

Solvency position stable - for now

Looking at the solvency position of the NZX and ASX-listed company, the capital raise it completed in December has left it in a much better position than it was in a year ago.

Further to 88% of shareholders taking their rights in the raise, it had $64 million of capital above the Reserve Bank’s minimum solvency requirements as at March 31.

As at March 31 2017, Tower had only $5.2 million above the minimum, so took out a $30 million loan from BNZ, which it has since repaid.

Nonetheless, the settlement Tower reached further to a dispute with Peak Re in the wake of the 2011 Canterbury earthquakes, eroded much of the wiggle room its capital raise provided.

Tower in March announced the agreement would see it receive only half ($22 million) of the amount of reinsurance it had recognised as a receivable in its financial statements.

The Peak Re settlement had a substantial $16.2 million impact on Tower’s half year loss.

However, disputes with the Earthquake Commission (EQC) mean Tower is not yet in a position where it can breathe easy.

It has recorded $66.9 million of receivables from EQC, which it expects to receive once it has worked through a range of issues with the government agency.

While Tower says this $66.9 million is a conservative estimate of what it’s owed, anything less it receives will cut into its $25 million solvency margin.

If $66.9 million is received, $18.5 million will be payable to reinsurers.

Tower says it remains confident in its position, based on the legal advice it has received.

Tower’s half year results announcement saw its share price drop from 80 cents to 77 cents, before picking up a little to 78 cents. It is down 14% from a year ago.

1 Comments

With the successful raising of new capital Tower has bought some time financially and that should be of comfort to policyholders and outstanding claimants, EQ ones in particular. The the Peak-re reinsurance outcome, from holding somehow to, what was it $44mill, on the balance sheet as a CURRENT ASSET, and then only receiving half of that cannot be an acceptable accounting practice.There is though some particular irony in how this played has out for, one imagines, a whole lot of unhappy Tower EQ claimants. Because it might be, in their opinion, that Tower has been done unto by Peak-re as Tower has done unto them [the claimants.]

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.