Here are my Top 10 links from around the Internet at 10 past 11 am brought to you in association with New Zealand Mint for your luncheon reading pleasure.

I welcome your additions and comments below, or please send suggestions for Thursday's Top 10 at 10 via email to bernard.hickey@interest.co.nz.

I'll pop any surplus suggestions I get into the comment stream under the Top 10.

1. Now Forbes is sniffing around - US fund manager Christopher Pavese has written in Forbes about the housing bubble in Australia and the risks for the Australian banks. HT Hugh P via email.

We've had a few of these warning signs lately from foreign observers of Australia's housing market. The Economist has done it, as has Jeremy Grantham.

The Australian powers-that-be simply say it's different in Australia because of a lack of housing supply and land restrictions.

We'll see. Sydney and Melbourne prices are certainly off the planet and the debt is real.

There isn't much margin for errror.

Despite the growing and increasingly obvious risks cited above, Australian banks are still trading at extremely rich multiples, particularly when compared to their US counterparts.

The average price-to-tangible-book values of two major lenders on our radar is roughly 3 times, double that of their American peers. It would appear that the banks are enjoying an undeserved premium, as investors are led to believe that lower charge-off rates and delinquencies are the result of more prudent management teams and more conservative lending standards. More likely, it is simply an issue of timing.

What happens if home prices don’t go up forever? The two banks with the largest exposure to Australia’s housing market have aggressively increased housing loans in recent years, such that residential real estate exposure now represents more than 11 times tangible equity. Not exactly what we’d call a margin of safety.

Our analysis indicates the potential for severe stress should housing prices revert to normal, let alone overshoot. We wonder how the currency would react should Aussie officials be forced to recapitalize the banking system.

2. Chinese demand for logs - This piece in Canada's Globe and Mail on how Canada's logging industry has tripled exports to Mainland China over the last two years is well worth a read.

There's great detail on how it happened and what Canada is now planning for. To convince the Chinese to use lumber rather than steel and concrete in construction, they went as far as setting up a college in China to train carpenters.

Is our logging industry doing the same?

Even optimists acknowledge that right now the hype obscures the extended slog ahead. “The story in China’s being oversold,” says Russ Taylor, president of consultants Wood Markets International in Vancouver.

“It [sounds like] a great story: All you hear is China is short of lumber and B.C. is the solution.”

In fact, China’s overall demand for wood of all kinds has been flat over the past few years. Much of its appetite is for raw logs that go into the country’s factories to produce other goods. Russia is a fierce competitor for those sales, as are China’s own wood producers, who are expanding their plantations.

The great new hope is that China may begin using wood to construct apartment buildings. Last year, Canada Wood and Forest Innovation won approval for a new wood-building code in Shanghai for six-storey apartment buildings. This year, three of the biggest B.C. forest producers – West Fraser Timber Co. Ltd., Canfor and Tolko Industries Ltd. – are coming together with smaller suppliers to construct a demonstration building in Beijing.

3. Tbe hottest debate - As America swelters in a hot summer, the debate ahead of November's congressional elections is focused on whether the government should try to to borrow and spend its way out of trouble or cut and tax its way out of trouble. It's the Keynesians vs the Hawks.

There's no clear winner at this stage. I'm a hawk because in the end consumers and taxpayers know in their bones if the borrowing and spending is affordable in the long term and adjust their spending accordingly.

If they think tax hikes and more recession is inevitable they won't spend any tax or spending windfalls anyway. It's all about confidence and underlying debt levels. A Keynesian attempt to borrow and spend won't fix those problems.

Tne Wall St Journal has a nice summary of the debate here. HT Nicola via email. The research suggests cutting deficits actually boosts growth in the long run.

In 107 periods since 1980 when governments cut deficits, doing so tended to quicken economic growth, not slow it. But this study focused on periods when central banks could offset deficit cutting with lower interest rates. The Fed has exhausted that avenue.

Carmen Reinhart, a University of Maryland economist who has studied the fiscal aftermath of financial crises, says more stimulus could be counterproductive because it could lead the public to expect even higher taxes in the future.

Instead, policy makers now need to convince the public that they are committed to reducing future deficits, without acting on that commitment right away, she says. That could hold interest rates down, without yanking money from an ailing economy too quickly.

"We are not in an easy position," she says. "Credibility is going to be difficult to achieve."

4. Faith in metal money - There's a lot of talk about money printing undermining faith in Fiat money. But what about conterfeiting. No one thinks about counterfeiting of coins, but it's such a big issue in Britain that the Royal Mint is thinking of scrapping all the one pound coins in existence and starting again, the Daily Mail reports.

One in 36 British pound coins are now thought to be fakes. The problem is the fakes are so good. HT My lovely wife via email

Jonathan Hilder, the chief executive of the Automatic Vending Association of Britain, representing snack and drinks machines which take £1.6billion of coins every year, said: ‘Ironically, the fakes are so good that it isn't yet causing a problem for consumers. Because they don't usually spot them, the trust in the coin is still high.

‘But if fakes continue to rise, reminting will have to become an option.’

5. Why Europe is so important - Tyler Durden points out at Zerohedge why the potential freeze or demise of the European savings banks, in particular the German Landesbanks, is so important in the global financial system.

It turns out they were key component in the shadow banking system that caused so much grief before the Global Financial Crisis hit in 2008, and are still bigger than the actual banks.

As even the New York Fed acknowledges in its recent paper "Shadow Banking", by Zoltan Poszar, in which there is a whole section on the critical Landesbank function in the shadow economy, "As major investors of term structured credits “manufactured” in the U.S., European banks, and their shadow bank offshoots were an important part of the “funding infrastructure” that financed the U.S. current account deficit," the proper functioning of the Landesbanks is crucial to maintaining a stable and efficient market funding structure.

This is actually extremely important, as for years most economists and pundits have considered only the non-shadow banking funding aspect of the massive US current account deficit (a topic most critical now that even the US is embarking on fiscal austerity, and the government sector will be unable to further fund the multi-trillion deleveraging ongoing in the private sector, thus pushing the topic of the current account to the forefront as Goldman did recently). Generically, everyone has always looked at China and Japan as those parties responsible for funding the US Current account deficit. Alas, that is only (less than) half the truth.

As the New York Fed suggests, the shadow banking system is likely a more important economic funding factor than even China and Japan combined when it comes to the CA. Which is why the all time record decline of over $1.3 trillion in shadow banking liabilities should be a far greater warning sign than any month to month change in China's US Treasury purchasing pattern.

6. Now comes the fund raising - The Wall St Journal has a thoughtful piece here on what happens now the European stress tests are finished. Now the European banks have to raise a stack of long term funds, potentially pushing up longer term interest rates.

This reminds us all that our banks face much higher funding costs in years to come, which will be passed on to us in the form of relatively higher interest rates.

HAVING passed the stress tests, most big European banks must now raise billions of dollars in long-term funding to finance new lending. At stake may be Europe's tentative economic recovery. Unlike the situation in the US, a large majority of companies in Europe depend on banks for finance.

Unless the banks can tempt investors in the bond markets, they won't be able to make long-term loans to allow businesses to finance investment. Non-financial businesses in the euro zone depend on bank credit for around 70 per cent of their debt-financing, whereas US businesses do about 80 per cent of their borrowing on capital markets, according to the European Central Bank.Funding shortages also reflect a shift in habits of US money-market funds that is unlikely to be reversed, according to UBS analyst Alastair Ryan.

The funds, historically a steady source of cash for European banks, have lost their appetite for risk and are shying away from them, partly because of new US regulations. And under pending global rules, insurance companies, another common liquidity provider to European banks, will face higher capital requirements for holding bank debt. “Wholesale markets are likely to be both more expensive and less reliable for banks in general for a prolonged period,” Mr Ryan said in a recent report. “In essence, many of the pots of money historically available to banks are either gone or constrained.”

The Bank of England warned last month in its semi-annual Financial Stability Report that banks worldwide - but especially in Europe - face a “substantial challenge” of renewing funding that is set to come due. The bank estimated that lenders worldwide have about $US5 trillion ($5.58 trillion) of funding due to mature in the next three years.

7. Don't waste stuff - This pile of Yellow Pages was left on a pallet in America with a note saying; "Dear Yellow Pages. We have a thing called the Internet. Please stop wasting stuff."

Right now a consortium of banks is trying to sell New Zealand's Yellow Pages and looks like losing upwards of NZ$800 million on a deal done just three years ago.

8. The collapsing US middle class - Michael Snyder writes at Yahoo about the systematic destruction of the US middle class. This is all topical as we head into the US elections.

The 22 statistics detailed here prove beyond a shadow of a doubt that the middle class is being systematically wiped out of existence in America.

The rich are getting richer and the poor are getting poorer at a staggering rate. Once upon a time, the United States had the largest and most prosperous middle class in the history of the world, but now that is changing at a blinding pace.

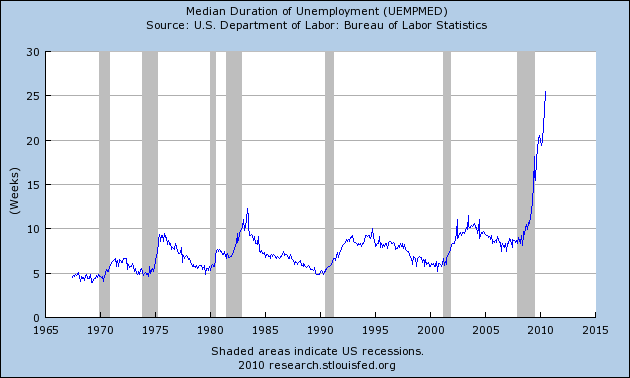

9. A deeper kind of joblessness - Umair Haque writes at the Harvard Business Review about a deeper kind of joblessness in America where the median duration of unemployment is now the longest it has been in a century.

He talks about the race to the bottom and suggests the quality of jobs (and the size of wages) is dependent on the quality of demand. He's onto something here. He suggests consumers should consume less, more expensive things that individually provide better value and therefore support more people on higher wages.

Low quality demand, then, means that we buy cheap, but the price is invisibly steep: it ignites a global race to the bottom, what a complexity economist might call a dynamic equilibrium of negative consumption externalities, consumption that results not just in joblessness but a loss in the quality of jobs.

The quality of a job is sparked by higher quality demand; or, valuing more than just the dollar price of a thing, but also its human and social impact. When we have low-quality demand, we have low-quality jobs. When we value McDonalds, the result is McJobs. A living wage is a small, halting — and perhaps even thoroughly misguided — step in a great reset of those self-destructive preferences.

Yet a step it nonetheless is. Contrast it, then, with what you might call high-quality demand. Shifting jobs to lower-wage countries is a tremendous boon to the impoverished. But it would be an even bigger boon if it weren't a double whammy: if, sneakily, we didn't also denude jobs of quality as they were shifted overseas; if the wage differential itself was enough, instead of exploiting a lack of governance and legislation as well; if that which makes a job more than just mere work didn't get, ever so conveniently, lost in translation.

Were that not to have happened already, people around the globe might have had more to spend, and more time to invest in spending it, with less risk — and so perhaps the global economy's problem of aggregate quantity of demand might currently be less severe. As Ford presciently saw a century ago: "well-managed business pays high wages and sells at low prices. Its workmen have the leisure to enjoy life and the wherewithal with which to finance that enjoyment." Yet, even that depends on a more fundamental cause: higher quality demand.

Because to generate higher wages, more leisure, better standards, work that affords space for passion, care, and respect — to offer that to, well one another — we might just have to learn to value the human, natural, and social more, first.

10. Totally relevant Cartoon

6 Comments

Interesting piece here from Zerohedge comparing the Gold/S&P price now vs the Depression

http://www.zerohedge.com/article/sp-priced-gold-comparison-between-great-depression-and-now

cheers

Bernard

Yep. That's why New Zealanders have stopped borrowing much more personally.

They certainly know in their bones now that they are saturated in debt.

Check out the growth rates here. Fallen off a cliff in the last two years.

http://www.interest.co.nz/charts/credit/housing-credit

cheers

Bernard

More on the European bank funding crisis from The Economist on British banks being addicted to cheap government funding

The problem is their addiction to government-supported funding: £165 billion of it through a Special Liquidity Scheme, which lets them refinance mortgage securities and other assets at a discount to market rates; and £120 billion more raised through bond issues bearing a government guarantee. These two schemes are due to come to an end in 2012, presenting the country’s big banks with a refinancing mountain. And other wholesale debt is also falling due—perhaps as much as £480 billion over the next three years. At the moment the banks are raising funds of around £12 billion a month, only half the rate they will need when the other bills are presented.

http://www.economist.com/node/16645083?story_id=16645083

cheers

Bernard

They were encouraged not to feel it in their bones by the marketers and the polititians.

Now the hard truth can no longer be disguised. Higher interest rates and the sheer saturation of it have convinced NZers to stop increasing their debts.

cheers

Bernard

John Key says student loans are a disaster economically. Only 53c collected for every dollar lent. But he's still backing it because the voters (well some young ones) want it. Just imagine if we all made our decisions via focus group.

Should I take out the rubbish? Let's see what the focus group think...

http://www.stuff.co.nz/national/politics/3963867/11b-student-loan-debt-a-disaster-says-Key

cheers

Bernard

And here's another thinkpiece on the idea that resource depletion is the real reason for the globe's economic problems. The 1929 Depression was just a preview of what was to come. HT Murray...I think...

cheers

Bernard

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.