This is a re-post of an article that first appeared the the July 2016 RBNZ Bulletin. It is here with permission.

------

Seven times each year, the Reserve Bank of New Zealand makes a decision about the appropriate level for the Official Cash Rate (OCR), to achieve the goals in the Policy Targets Agreement (PTA).

With four of these decisions, the Bank also releases a Monetary Policy Statement (MPS) that discusses the outlook for interest rates, economic activity and inflation.

When making OCR decisions, the Bank uses a system that promotes sound decision making, to help achieve the goals of the PTA. A robust system is needed to address the inherent uncertainty the Bank faces when making monetary policy decisions. This uncertainty stems from three broad areas.

1. The Bank doesn’t have perfect knowledge about the current state of the New Zealand economy. Major economic data are often released with a significant lag, and remain subject to revision for some time after release. In addition, variables that are important for the conduct of monetary policy are not directly observable. This includes concepts such as the output gap, the neutral interest rate and inflation expectations.1

2. The structure of the economy and the transmission of economic events are difficult to know for certain and can change over time. Research into these topics can help improve the Bank’s knowledge, but can never fully eliminate such uncertainty.

3. Monetary policy needs to be set with the future in mind. Monetary policy influences inflation with a significant lag, so when setting the OCR the Bank must take into account its views about the likely future path of the economy. However, unforeseen events are always pushing the New Zealand economy in new directions and the Bank will never be able to foresee all these events.

A clear consensus on how a central bank should make decisions in such an environment is yet to emerge amongst academic economists,2 but inflation-targeting central banks have adopted some common features in their decision making. These common features include policy discussion within a committee, considering of a wide set of information, a focus on transparency and clear communication to stakeholders, and generally modest moves in policy settings that are regularly reviewed.3

The Bank has designed a decision-making process to best manage the inherent uncertainty faced when setting monetary policy, guided by the practice of other central banks, academic literature and the Bank’s own experience. Specifically, this process is structured to:

• reduce uncertainty as much as possible;

• characterise the uncertainty that remains;

• help decision makers understand and balance the consequent risks;

• communicate the decision, underlying judgements and risks externally; and,

• ensure that the Bank’s policy stance and judgements are constantly reviewed in the face of new developments.

This paper outlines the decision-making process in detail by highlighting how the Bank reaches a decision on the appropriate setting of the OCR and the publication of a Monetary Policy Statement.

2. Making a monetary policy decision

The Bank’s process to reach a monetary policy decision and publish a Monetary Policy Statement follows four steps:4

1. Gather and process information: Bank staff gather and process a broad range of information about the New Zealand and global economies, and domestic and international financial markets.

2. Reach a decision: staff assess this information to draw conclusions on the implications for monetary policy, and present the information and implications to the Bank’s relevant policy committees. The Bank’s Governing Committee uses this information to come to a recommendation about the appropriate setting and outlook for monetary policy – with guidance from the Monetary Policy Committee.

3. Communicate: the Bank decides on the best way to communicate this information to key stakeholders.

4. Review: the Bank continually reviews its knowledge of the economy, assumptions and past policy decisions.

|

Box A Groups involved in monetary policy advice and decision making at the Bank The analysis behind an OCR decision and the publication of a Monetary Policy Statement involves a wide range of Bank staff and two policy committees. Five key teams are involved in monetary policy analysis. These include the four teams of the Economics Department, and one team from the Financial Markets Department. Where required, these teams are supported by other teams at the Bank, including contributions on relevant financial stability issues from the Macro-Financial Department. These teams help prepare the background material required for the Bank’s policy committees to reach a decision on the OCR and publish a Monetary Policy Statement. The Bank’s Communications Team also provides advice about how to communicate the Bank’s policy messages. The key committees relevant for monetary policy are: The Governing Committee: This group consists of the Governor, the two Deputy Governors and the Assistant Governor. This group deliberates together on all major policy decisions made by the Bank. This committee is chaired by the Governor. The Monetary Policy Committee (MPC): The MPC is made up of senior staff from the Bank’s policy departments, two external advisors, and the Governing Committee. It currently has 13 members. The two external advisors have extensive experience in an industry significant to the New Zealand economy. These external advisors are appointed by the Governing Committee, and usually serve on the committee for two to three years. This committee is chaired by the Bank’s Chief Economist / Assistant Governor. |

Steps one and four are ongoing processes, happening constantly in the background between the Bank’s regular policy announcements. Steps two and three are more structured and intensive – occurring largely during the two weeks before a Monetary Policy Statement. The following sections of this article provide more detail on these four steps, how they interact, who is involved and how the different steps help to promote sound policy outcomes (see box A for a summary of the Bank’s key staff and committees involved in a monetary policy decision).

2.1 Gathering and processing information

Reaching a policy decision starts with constant monitoring of the New Zealand economic landscape. To operate monetary policy effectively, the Bank needs to build and maintain in-depth knowledge on three aspects:

1. The current state of the New Zealand economy.

2. How the economy has evolved in the past, and why it has evolved this way.

3. Where the economy is likely to head in the future.

Understanding the current state of the economy

The Bank monitors a diverse array of data in order to gauge the current state of the domestic economy. The data includes official statistics, survey data, financial market information and international data.

The Bank’s analysts assess what recent data mean for the New Zealand economy and monetary policy. One important aspect to this work is to discern the underlying trends relevant for monetary policy from the surrounding statistical noise in the vast array of economic and financial data.

Assessment of the macroeconomic and financial data is supplemented by meetings with the business, financial and analyst community.5 These meetings help us identify emerging trends in the economy, understand the transmission of monetary policy to financial markets, cross-check the signals being given by recent economic data and learn about the structure of certain sectors of the economy, along with any sector-specific developments that are important for monetary policy.6

An in-depth understanding of the economic and financial landscape helps the Bank to: minimise uncertainty in our understanding of the state of the economy; characterise the uncertainty that remains and the assumptions that must be made in making a policy decision; understand the consequent risks around these assumptions; and review past assumptions, forecast errors and policy decisions.

Understanding the evolution of the economy

As well as monitoring new developments, the Bank needs a firm grasp of how the economy has evolved and why it has evolved that way. Analysis of incoming data often reveals emerging or continuing trends that are relevant for monetary policy, while longer-term research contributes to the Bank‘s understanding of the structure of the economy. Both of these research streams help the Bank understand how monetary policy should respond to new or unexpected developments in the economy and also help us to forecast the future path of the economy. If we understand the current structure of the economy, and how it has evolved in response to developments in the past, we can make better assumptions about how the economy is likely to respond to future events. Research also helps the Bank to understand the limitations of its own knowledge, the assumptions required to address those limitations, and the confidence we should place in those assumptions.

Understanding the outlook for the economy

The Bank also needs an idea of how the economy is likely to evolve in the future. There’s a significant time lag between the announcement of an OCR decision and the subsequent effect on the economy and inflation, so the Bank works to understand where inflation is heading over the medium term in order to make an appropriate assessment of where the OCR should be set today and in the future.

The Bank uses a number of techniques to produce forecasts for the economy. Analysts use a combination of data monitoring, feedback from meetings with businesses, structural modelling and statistical modelling to form a judgement about the likely path of key variables over the next six months or so.

Beyond these near-term forecasts, the Bank uses a forecasting model called NZSIM.7 This is a structural model that describes the key sectors of the New Zealand economy and how they influence inflation. NZSIM is used to produce forecasts for the economy, inflation and interest rates. These forecasts are cross-checked, and altered where appropriate, using a range of other models and judgement from the Bank’s staff and policy committees. These cross-checks include the output from other structural models, our suite of statistical models and forecasts by external analysts.8

The Bank’s forecasts and policy decisions are model assisted, rather than model produced. Models help us to collate information, ensure internal consistency, test competing theories, understand the structure of the economy and in some cases improve forecasting performance. A large degree of judgement from the Bank’s staff is still required in order to reach a policy decision and publish a Monetary Policy Statement. This judgement is collated in a systematic way, through various committee meetings, which are discussed further in the following section of this article. NZSIM acts as the way to codify the collective judgement of Bank staff, allowing the Bank to be systematic and consistent across time.

The insights from all of our analysis are regularly communicated to the MPC, which meets regularly to discuss the current state of the economy and the implications for monetary policy. The state of the economy and the appropriateness of monetary policy settings are under constant review. The regular meetings of the MPC, about every two weeks, are one avenue for the committee to discuss monetary policy developments.

2.2 Reaching a decision

All the information that we have is ultimately used to help the Bank’s Governing Committee reach a consensus on the appropriate setting for the OCR.

The Bank’s staff, MPC, and Governing Committee are involved in a regular process working towards an OCR decision and Monetary Policy Statement publication every quarter. The meetings in this regular process are designed to bring a diverse range of views to the decision-making process, help us to understand limitations of the Bank’s knowledge and the judgements required, and collate this information and judgement in an effective way.

The process starts in earnest about two weeks before publication of a scheduled Monetary Policy Statement. In a series of ‘pre-MPC’ meetings the staff involved in monitoring the economy and producing economic forecasts present to the Economics and Financial Markets Departments on the current state of the economy and the economic outlook. The pre-MPC meetings involve a discussion of current economic and market developments, presentation of a full set of forecasts, discussion of key risks and judgements that make up the forecasts, a discussion of alternative scenarios and policy options, and the key issues that staff intend to present to the MPC.

Staff then suggest changes to the economic projections and areas where further work or research may be required. The forecasts and analysis are then further refined to reflect these suggestions, and staff decide on the key aspects of the projections to highlight to the MPC and the Governing Committee.

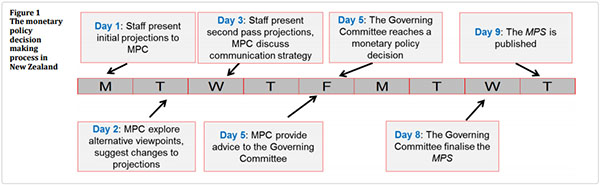

The MPC and Governing Committees then begin a process working towards the publication of the Statement and OCR decision. This starts about eight working days before the publication day (figure 1).

The process takes advantage of the benefits of committee decision making. A group of individuals with a diverse and differing set of useful information should make more informed decisions than an individual can make.9

The Bank has long used committees as a way to provide advice to the Governor when making a monetary policy decision. The degree of committee involvement in the monetary policy decision making process has evolved since the implementation of inflation targeting.10

In 2013, the Bank extended the role of committees, making committees more important in decision making.11 The Bank now relies less on the formal single decision-maker model. The Governing Committee was formed, with this committee responsible for reaching a decision on the appropriate setting for monetary policy, while the Governor retains statutory responsibility for policy decisions. The Governor’s decisionmaking responsibility is similar to the arrangement at the Bank of Canada, which has a single decision-maker model in its legislation, but makes policy decisions within a committee framework.

The monetary policy decision making process starts with a series of meetings, bringing together the Bank’s staff and relevant policy committees. Day one is devoted to presentations about the current state of the economy, economic forecasts and alternative scenarios. Within the Bank these are called ‘first-pass projections’. The focus of MPC members is on understanding the information presented by the staff. The MPC chair ensures that questions from members during this stage are focussed on technical clarifications, and discourages discussion of policy opinions. This initial focus on information helps avoid group think and helps ensure that all relevant information is considered before members begin to voice their policy preferences.

Staff and committee members have a vast array of information available to them. Presentations by staff are focussed on the key uncertainties and assumptions underpinning the projections, while papers written by staff provide additional background information, covering issues and trends in the international economy, key sectors of the New Zealand economy, financial markets and credit markets.

One key source of uncertainty for the Bank is the current state of unobservable variables that need to be understood when making a policy decision. These unobservable variables include the neutral interest rate, inflation expectations and the output gap. The Bank has created frameworks to estimate these variables, consider as much relevant information as possible and to characterise the uncertainty around these estimates.12 These frameworks are also included as additional information for the staff and committees.

At the end of day one, staff and committee members are given a survey to complete. The survey asks committee members to highlight the risks they see to the projections and the uncertainty around these projections. The survey helps ensure that all staff and committee member views are considered. The survey results are also used to help focus the discussion on day two.

Day two is focussed on testing the assumptions within the forecasts and exploring alternative viewpoints. The survey results from day one are used to guide areas of discussion. This is supplemented by forecasts from external analysts and the Bank’s suite of statistical models. This information helps highlight areas of uncertainty and disagreement. Questions from members during this stage are usually focussed on the assumptions underlying the staff’s projections. Committee members will highlight areas of disagreement and propose alternative scenarios and research avenues to be explored. These discussions help ensure a wide range of competing viewpoints and information are considered.

During these discussions, the chair encourages the Governors to speak last when debating a topic, to encourage a wide range of views to be presented. In addition, the MPC contains two external members to add diversity and give outside perspectives.

At the end of day two, the chair summarises the key issues raised in regard to the projections. The MPC, led by the chair, then decides which areas that were discussed should be incorporated into the projections. Bank staff are directed to make any required changes to the projections and present on the results of the changes the following day.

Day three begins with presentation of the new, revised, set of projections, which are known in the Bank as ‘second-pass projections’. The presentation may result in further refinement, but the ‘second-pass’ is usually close to the final published projections. From there, discussion is usually focused on how the Bank can best communicate the key aspects of the projections to the public. Members of staff then begin to draft the Monetary Policy Statement, in light of the guidance provided by the MPC.

The MPC then reconvenes, without other staff in the room, to consider and give formal policy advice to the Governing Committee. This occurs on day five, four working days before the publication of the Monetary Policy Statement. The MPC and Governing Committee spend time discussing the key monetary policy considerations. Each MPC member is asked to comment on what they see as the key issues, with the Governors speaking last. Each member of the MPC, including the Assistant Governor and Deputy Governors, then submits written advice to the Governing Committee on several aspects, including:

• the preferred outcome for the OCR at this meeting;

• the preferred outlook for the OCR over the forecast horizon;

• key risks and judgements to consider over the forecast horizon; and,

• any potential communication issues that should be taken into consideration.

This advice is not a binding vote, but is a way to combine the significant volume of information presented to the MPC into a form that is useful for the Governing Committee. The advice is submitted anonymously and without collaboration between MPC members, to ensure that independent viewpoints are considered. This helps the Governing Committee to consider and understand a potentially diverse array of viewpoints and helps to avoid group think.

Later that day, the Governing Committee makes its decision on the appropriate setting for the OCR, the outlook for interest rates and the key messages to be included in the Monetary Policy Statement. The Governor retains statutory responsibility for monetary policy decisions, and retains the final say on appropriate monetary policy settings, but in practice, the Governing Committee aims to make the policy decision by reaching a consensus.

The Governing Committee is a collegial committee, in that it aims to reach consensus on appropriate policy settings through debate. The collegial approach helps the Bank to sharpen the communication of a policy decision and provide a clear and consistent message to financial market participants and the public.

The Governor begins by summarising the written advice received from MPC (including members of the Governing Committee). The Governors then discuss the MPC advice, their own views, and points of difference. If there are competing viewpoints within the Governing Committee, the members have a chance to reconsider their positions. Once the Governing Committee has reached a consensus, the Governor then formalises the decision.

If the Governing Committee is unable to reach a consensus view, it will go with the majority view where one exists. If the views are balanced, the Governor will have final say on the policy outcome. Each member of the Governing Committee adopts the finalised outcome as their own position when speaking in public.

Any persistent areas of disagreement that arise during the consideration and decision making process likely reflect significant sources of uncertainty in the forecasts, which the Bank can present as alternative scenarios in the Monetary Policy Statement. The Governing Committee will return to these areas of disagreement at the next policy decision when more information is available, with an aim of reaching consensus.

Once a decision has been made, the minutes of the meeting of the Governing Committee are provided to the MPC. These minutes help to highlight the rationale for the decision, areas of uncertainty and potential areas of focus when drafting the Monetary Policy Statement.

The decision may result in further changes to the projections. The Bank’s staff will update the projections if required and present a finalised set of projections to the policy committees and for signoff by the Governing Committee.

2.3 Communicating the policy decision

The next stage of the process is to refine the communication of the decision to the public. The Monetary Policy Statement is the main way that the Bank communicates the important information behind its policy decision. The document is described further in box B.

The Governing Committee decides on the key messages to present in the Monetary Policy Statement. To help with its communications, the Bank talks to financial market participants to collect their views on how different policy scenarios are likely to influence financial markets.15 A summary of these views is reported to the policy committees. In addition, the Bank’s Communications Team advises on how the news media is likely to interpret different aspects of the forecasts and the Monetary Policy Statement.

The Governing Committee drafts chapter one of the Monetary Policy Statement. This chapter highlights key aspects of the OCR decision and doubles as the media release on publication day.

After guidance from the MPC and the Governing Committee, Bank staff draft the remainder of the document, receiving regular feedback from the MPC and Governing Committee in drafting meetings.

On day eight the Governing Committee make final edits to the Monetary Policy Statement and sign off on a final version. The document is then prepared for publication.

|

Box B The communication aims of the Monetary Policy Statement The key communication and accountability document for monetary policy decisions is the Bank’s Monetary Policy Statement. The aim of each Monetary Policy Statement is to communicate to the public: • the Bank’s central outlook for the economy and interest rates; • the key considerations and judgements that make up this outlook; • key risks to the outlook, and how policy may respond to the crystallisation of such risks; and • a review and assessment of past policy decisions. Effective and transparent communication helps the Bank’s Board, Parliament’s Finance and Expenditure Select Committee, the wider government, financial market participants, news media and the public, all play a role in effective oversight of the Bank.13 Effective and transparent communication also helps improve the effectiveness of monetary policy. Most importantly, if financial market participants have a good understanding of how the Bank will respond to new developments in the economy, then interest rates should adjust to levels consistent with medium-term price stability without the need for constant comment and intervention by the Bank.14 The Monetary Policy Statement includes a number of features to help convey the Bank’s outlook, judgements, risks and assessment. In particular: • The document includes a full set of economic projections, covering the next few years. This includes the Governing Committee’s central outlook for the 90-day interest rate. • The text of the document highlights key considerations and judgements made to arrive at the interest rate outlook. Where relevant, further details are explained in highlighted boxes in the Monetary Policy Statement. • Alternative policy scenarios are often included, that help highlight the key risks and judgements the Bank is making in its central projection, and illustrate how monetary policy would be likely to respond if these risks were to crystallise. • A summary, review and assessment of past policy decisions in included in box A of each Monetary Policy Statement. |

The Bank publishes a Monetary Policy Statement and makes an OCR decision every quarter. The OCR is also reviewed once between each Monetary Policy Statement (excluding between the November and February Statements). As a full Monetary Policy Statement is not published with these interim OCR reviews, the Bank adopts a scaleddown version of the forecasting and decision-making process discussed above. In the scaled down process, the presentation and refinement of forecasts occur in a meeting two or three days before the OCR announcement. The MPC submits advice to the Governing Committee that day, and the Governing Committee subsequently reaches a decision on the appropriate setting of the OCR. The Governing Committee then drafts a media statement outlining the decision, which is finalised the evening before the OCR announcement.

2.4 Reviewing the Bank’s decisions and frameworks

The process above does not end, but is continually reviewed and refined every quarter when the Bank makes a new monetary policy decision. The Bank is constantly reviewing its policy decisions, assumptions, knowledge and processes to help promote sound monetary policy outcomes. Continual review helps the Bank to improve its knowledge of the economy and learn from past errors.

The Bank’s Board is officially tasked with monitoring and assessing the Bank’s performance. To help make its assessment, the Board is given the background material used in the Bank’s policy deliberations, including supporting analytical papers, meeting minutes, and policy advice provided by the MPC to the Governing Committee. The Board devotes a large portion of its monthly meetings to discussing economic developments and reviewing the Bank’s OCR decisions.

The Bank is also held accountable by several other external stakeholders, including the New Zealand public, Parliament, financial market participants, and the news media. Financial market participants assess and respond to the Bank’s communications and the news media comments on the Bank’s performance. Parliament’s Finance and Expenditure Select Committee questions the Bank following the publication of every Monetary Policy Statement.

The Bank also conducts regular internal reviews. These reviews include analysis of the Bank’s forecast errors,16 the suitability of past judgements, and ways that the decision-making process can be improved in order to achieve better policy outcomes. External reviews of the Bank’s decisions and decision-making process are also occasionally commissioned. These have included reviews from experienced international central bankers, academic economists and Parliament’s Finance and Expenditure Select Committee.17

3. Conclusion

The Bank is faced with significant uncertainty when conducting monetary policy to achieve the goals of the Policy Targets Agreement. This includes uncertainty about the state of the economy, the underlying structure of the economy and the economic outlook. To help promote sound monetary policy outcomes, the Bank has adopted a process to address this uncertainty.

The Bank’s monetary policy decision-making process is designed to: reduce uncertainty as much as possible; characterise the uncertainty that remains; help decision makers understand and balance the consequent risks; communicate the decision, underlying judgements and risks externally; and ensure that the Bank’s policy stance and judgements are constantly reviewed in the face of new developments.

This paper outlines the current state of play when it comes to the Bank’s monetary policy decision-making process. However, a key element of the process is the need for constant review and innovation, and the Bank’s approach to decision making will continue to evolve over time.

Notes:

1. The Bank has recently published a range of research on these factors. For more information see Richardson and Williams (2015), Armstrong (2015) and Lewis (2016).

2. See Schmidt-Hebbel and Walsh (2008) and Bernanke (2007) for a discussion of research into effective monetary policy decision making under uncertainty.

3. For a discussion of the decision making process at other advanced economy central banks, see Moutot, Jung and Mongelli (2008), Federal Reserve Bank of Philadelphia (2008), Warsh (2014), Qvigstad (2010) and Murray (2013).

4. From July 2016, the Bank is adopting a new timetable for OCR decisions. There are seven scheduled OCR decisions every year. Four of these decisions are accompanied by the publication of a Monetary Policy Statement. The Bank will publish the Monetary Policy Statement on the second Thursday, in February, May, August and November. Each Monetary Policy Statement includes an OCR announcement. There will be three intervening OCR Reviews, to be released on the fourth Thursday of March, June, and September. See http://www.rbnz.govt.nz/news/2015/08/rbnz-mps-ocr-fsr-datesfor-2016-2017. The Bank also has the option to make unscheduled changes to the OCR in response to unexpected or sudden developments. To date, this has occurred only once, following the September 11 2001 attacks on the World Trade Center in New York.

5. Each year, Bank staff make about 120 formal presentations to business groups and other audiences. Bank staff also visit about 150 businesses each year as part of our business liaison programme.

6. Insights from our business liaison programme are often presented in the Monetary Policy Statement. For example, see RBNZ (2015).

7. See Kamber, McDonald, Sander and Theodoridis (2015).

8. See McDonald and Thorsrud (2011) and Bloor and Matheson (2011) for an example of the Bank’s approach to statistical modelling.

9. For a discussion of theory and evidence, see Blinder (2004).

10. Policy discussion and advice in a committee setting has been an important aspect of the bank’s decision- range of competing viewpoints and information are considered. making process since the early 2000s. For a description of previous approaches to decision making at the Bank, see RBNZ (2001), Brash (2001), RBNZ (2007).

11. Wheeler (2013).

12. Recent research published by the Bank highlights aspects of these frameworks in detail. See Richardson and Williams (2015), Armstrong (2015) and Lewis, McDermott and Richardson (2016).

13. See Ford, Kendall and Richardson (2015) for further discussion of central bank oversight.

14. McDermott (2016).

15. These interviews take place prior to the monetary policy decision. Market participants are asked for their views on what type of policy decision and Monetary Policy Statement would cause interest rates to rise, fall or stay the same on the day of the release. No information is provided to the market participants on any aspect of the OCR decision-making process during these interviews.

16. For example, see Lees (2016) and Reid (2016).

17. Past reviews include Svensson (2001) and RBNZ (2007).

Adam Richardson is an Adviser in the Policy Analysis team at the Reserve Bank of New Zealand. He joined the bank in 2007 and has also spent time in the Bank's Forecasting team and Financial Markets Research team. The full Bulletin paper, with all References, is here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.