Many households will be in for an unpleasant economic shock over the next couple of years as the low interest rate party comes to an end and people are left with an ugly financial hangover.

The biggest hangovers will be for those who have borrowed up large over the last few years to fund everything from the purchase of their first home, to renovating their existing home or buying a new car.

Younger borrowers are likely to be especially shocked by the change in circumstances because mortgage interest rates have been in more or less steady decline for the last 14 years.

Cheap finance, underpinned by ever rising housing values, is the only economic environment that many younger people have ever known.

And that situation has persisted for so long that many older borrowers have probably forgotten what it is like to live in an environment where house prices are flat or perhaps even falling, while borrowing costs are rising.

They are in for a rude awakening.

The 14 year slide in mortgage interest rates came to an end in May last year when the average of the two year fixed rates offered by the major banks bottomed out at an all time low of 2.52%.

Since then it has moved higher in each and every subsequent month and finished up at the end of last year on 4.21%.

To put that in perspective, that is still relatively cheap by historical standards because it only takes mortgage rates back to where they were about three years ago and they would have been considered cheap at the time.

So anyone who took out or re-fixed a mortgage about three years ago and is due for another fix about now, probably won't notice much change in their mortgage payments.

Those who took a longer term punt and last fixed their mortgages for a five year term and are due to refix now will probably get a reduction in their mortgage payments because they'll be re-fixing at a lower rate.

But they are likely to be a small minority, with most people fixing for shorter terms.

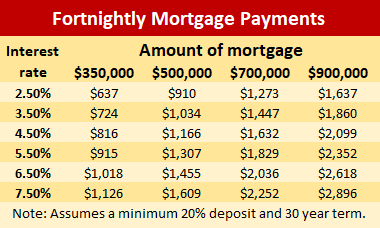

So in everyday dollar terms, what will rising interest rates mean for most mortgage holders?

The table below shows how changing interest rates could affect the fortnightly payments for different sized mortgages.

It suggests that someone with a $500,000 mortgage who last fixed about two years ago ago when the two year rate was around 3.5% and is looking to re-fix this year at closer to 4.5%, could be looking at an extra $132 a fortnight in mortgage payments.

If their mortgage was $700,000 they could be looking at an extra $185 a fortnight.

It seems likely that mortgage rates will keep rising this year and could go above 5% for popular fixed terms next year, so some borrowers could be facing even bigger increases further down the track.

With cost increases now prevalent on a wide range of household goods and services from petrol to groceries, the effect of even modest increases in mortgage payments should not be underestimated.

The people most at risk in this environment will be those who borrowed the absolute maximum they could afford when interest rates were at or near their lowest point in the middle of last year.

They will be squeezed especially hard and the worry is that some may find it difficult to keep themselves financially afloat.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

Comprehensive Mortgage Calculator

125 Comments

The scenario of a FHB borrowing 700k last year at 2.5% and then refinancing this year at say 5.5% won't be rare, and as the table shows will be painful - an extra $550 per fortnight.

How many will have seen it coming and fixed longer? I know I did.

I don't know what the breakdown by term is, but if large numbers fixed for 3+ years would that mean OCR has to go higher than expected to achieve the desired effect?

We might get a "2 speed" recession, experienced very differently depending on how long you fixed.

Don't know. I suspect, given how hard it has been for FHBs to buy a house, that many would have gone with the short term, lower outlay option ie. 1 or 2 year fixed.

But that's only a hunch, I guess there will be a mix.

I'd agree. I imagine most would have chased the lowest possible rates given the size of the debt many took on.

The 2.5% mortgage rates were an historic low, and should never have been expected to last for long by any prudent borrower. 6% should always be the consideration if you are considering borrowing large sums of money. The 2.99% 5 yr offered last year was the smart move.

Yeah that probably was the smartest move. But I guess time will tell.

I think many will struggle with interest rates above 5%, but most will probably survive but with a FAR less comfortable lifestyle.

We should be more worried about businesses relying on discretionary spending, rather than households who will have to tighten their belts a lot but will probably survive.

Whatever, FHB’s and other mortgagors will fight hard to keep their homes/trophies - and the vast majority will remain winners. 🎖

But there’ll be some casualties. The stresses caused through tighter household budgets in the face of higher mortgage repayments will lead to some relationships failing - and the inevitable “broken marriage” listings/sales. 😪

TTP

Budget...that's something we haven't heard for a while. With debt having been so cheap and easy to get, it's how many have been living a lavish lifestyle & 'keeping up with the Joneses'.Take that away and reality bites for sure.

Growing up.. my family was in the middle at best (in terms of wealth). I have no idea where that saying comes from. Shouldn’t it be ‘keeping up with the Keys’ or something?

Nifty1...cut it out mate......being a Boomer myself (most hated species) l will not mention Avos.....and l do agree it was a lot easier back in my my day ...l was a carpenter , 1 income , had 3 kids , no bother.....but we never bought any crap...only things we really had to have.....when l was a kid in the 60s we had dripping on Bread every sunday nite....dont think my kids would eat that....

Dripping on bread is something I’d quite happily eat. I’d do about 20% of the household cooking. But when I do I cook like a 50s Mum. Make my own stock and all!

Pete I've got not idea what you're on about, my comment had nothing to do about boomers in the 60's. We're in 2022 mate.

Debt is a curse on the society and the poor. Individual greed is reason for debt in society. If we really believe in a team of 5 million, then I do not see the need for anyone to take debt and pay interest. Rich can help poor to get up the ladder. But what is told to the poor is a mirage shown to keep them slaving. Middle class thinks they are winning but how mistaken they are and do not know they are the bull on the bull cart pulling a fat rich arse sitting on the cart.

So yeah keeping paying the debt until die and then your next generation will take on the reigns of the same cycle.

This is human nature. It's all just a game of deception and lies. The constant mantra of "Kiwis helping kiwis" and "Support local kiwis" is just a another scam. If the wealthy and corporations helped everyone else, they'll lose their grip, power and profits over the common class however, this is the capitalistic society we all live in [not that I agree or disagree with this] which is why socialism and communism ideaology has been prevalent as of late [albeit at times too extreme]. Unfortunately, most Western economies operate in a same modus operandi of money is what matters most and survival of the fittest.

When your New World and Countdown supermarkets are charging more for the same locally produced goods than what it is sold in Europe and fact that employers fail to pay a large bulk of their workers marginally higher than minimum wage, you know there's something wrong in this country. It's when the landlords scoop up all the real estate whilst increasing the rents on everyone and force the unemployed and single parents with all their kids to live in a Honda Odyssey in South Auckland. This is clearly viewable from a outsider's perspective because when you've taught, trained and grew up in the box, you simply don't know any different.

Unfortunately, its the false narrative and passive aggression that kiwis are told amongst one another that leads to the frustration and torment of many whilst living in quiet desperation. It's the same when someone is saying that they're trying to help you when they're trying to take your last dollar you have or when government says we're opening up the country whilst placing more restrictions on businesses and workers to comply with their mandates.

Well that’s just untrue.

What CFO would recommend an equity only funding model.

Debt is extremely useful. Bad debt is crippling.

Ngk,

then your next generation will take on the reigns of the same cycle. Reins, not reigns.

You have a case, but vastly overstate it. For most people, taking on debt( a mortgage) is fine and gets paid off at or before retirement. Many who start a business have to go into debt initially.

Where you certainly have a case is the ease of consumer related debt-debit/credit cards, BNPL, long-term hire purchase. I am of course an old fart, but we just didn't have such easy access to consumer debt and our parents had lived through both the Depression and WW2. Their aversion to debt came down to us. Apart from a mortgage I have never had debt and was fully debt-free at 53.

If their mortgage was $700,000 they could be looking at an extra $185 a fortnight.

I can't help but wonder how anyone would struggle to find an extra $90 a week. Are people really living that hand to mouth?

Some are.

Some will cope with that, but will need to massively tighten discretionary spend.

Watch out for hospo and retail to be whacked this year, especially with omicron breaking out.

Yeah. I don't mean to sound dismissive, it's still a significant increase. I just find it incredible how little wiggle room people leave for themselves in their budgets.

I don’t think the little wiggle room is by choice, I think its more oh i want to have a basic life and own that crappy little 2 bd room place so we can raise 1 child one day.

Its not by choice, but by credit. They see something they want, cell phone, car etc and they see they can afford the repayments, but that reduces the wiggle room, then something unexpected happens like interest rate hike, or medical bill or car repair and suddenly that wiggle room becomes a deficit, they pay penalties and it just spirals out of control.

Geez mate, you sound very entitled and out of touch. Along with the price of everything else going up, for many even $50 is out of reach, and mostly through not fault of there own. You only have to fall behind on a few payments and then you're in a whole world of catch up trouble. (insert eye-roll here)

I think your out of touch. Plenty of people will be stretched to the limit already and $90 is huge if it starts cutting into the weekly food bill.

But they're all stress tested to at least 6%. They'll do it easy.

The 'stress test' doesn't care how well you eat or whether how much free time you have for your mental health or whether you can afford to do anything or go anywhere if you do have it. The 'stress test' is 'does the bank still get their money' and not a whole lot more than that.

Exactly the bank doesn't care if your eating baked beans 7 days a week as long as your paying the mortgage. I was unemployed a couple of times during the course of paying off my mortgage, didn't even bother to tell the bank they don't give a rats as long as you make the payments.

I would also add the stress tests are done at the same time as the expenses assessed (on loan application) so prior to all this inflation on household spending.

No they will not because at 6% the bank didn't tell you that you will have no life other than work to pay off the mortgage. Its an expectation now to have a couple of new cars, dinners out and trips to the Cafe and that new iPhone every year so its going to come as a bit of a shock when that all goes out the window for the majority of people. A few will fold before 6% but beyond that it will be exponential defaults and anything approaching double digits will be catastrophic for recent buyers.

Your circle of acquaintances must be small if you think those things are 'expectations'. I am late thirties, most if my friends are relatively well paid (top tax bracket), and no one I know buys new cars (let alone had two!), buys a new phone every year (let alone an I phone), frequently goes out for dinner, or spends a lot of money in cafes. Second hand everything (clothes, furniture etc) is the norm.

We are used to not being able to afford things. First as students, then as new graduates paying off student loans, then saving for a house while paying ever increasing rents, then paying unavoidably large mortgages.

So your friends earning $180K+ a year are buying second-hand stuff and not frequently going out for a bite to eat? I've never earned anywhere near that yet even now, if I want to eat out, I eat out....and - call me a snob - I just don't buy second-hand. Yikes, I knew things were bad but I didn't know they were that bad (for people earning that sort of money!)

I forgot the new top tax bracket was 180k - I was talking about people earning generally between 70-100k.

To an extent, some of this is by choice - I.e., wanting to keep contributing to kiwisaver rather than spend that money on dining out. But still, the idea that multiple new cars and iphones are expectations is definitely not the norm.

People seem to forget that to buy second hand, someone had to buy it new first, although I see you can buy some clothing new second hand(deliberately distressed).

I am that guy.

Had 2 jobs ( professional and a family business). Freehold at 41, and at 55 my retirement is secure. $1500 car, no cafes/coffees, 2nd hand clothes or K-Mart for tee shirts/underwear etc.

The upside is I sleep well at night and my enjoyment comes from reading in my hammock with the tuis singing behind me. Exercise costs very little so I grind away daily.

Too many kiwis fall into the trap of consumerism. The other plus of being a scrooge is not having anything worth stealing -2nd hand IPAD, polar watch :-)

The issue is how you spend money is part of your nature. Even when you finally come into money you cannot bring yourself to spend it if you didn't just waste it for decades, it becomes part of who you are. Strange that I also have a hammock and enjoy the bird life, took a bit longer to become freehold. Will be buying that new car next year however, unless Covid kills it.

100%. My frugality came from my upbringing. Now when I could spend more I have zero urge or desire. My work sends me to global conferences and I go to company paid fine dining. Has zero value. I’m happier now cooking some ribs on my bbq than sitting in a Parisian restaurant which cost more than a good pair of running shoes. It’s wasted on me, a simple guy with very little taste. Can’t tell the difference between a Pinot noir and Cab Sav. Stay frugal, gives you the freedom of saying “F you” to the employer with no worries about private school bills, A8 Audi on tick or the big mortgage on the Omaha beach house. It’s a game. The guy who cashes out first is probably the winner.

The self congratulatory narcissism is strong with this one and they brag about luxuries they can access being cheap options without realizing most kiwis cannot even access those. It is like a person bragging about affording prime meat while more and more families have to turn to foodbanks for even a single meal. Oh wait it is exactly that.

"With this one"

What a rude way to talk about someone. Of course all as you dissect and judge them, which in itself is quite bad

You obviously never read Steal This Book and are living a life of extreme luxury compared to most NZders these days. For instance you can afford to access employment, housing, buy new clothing from a store and have more than one meal consisting of more than bread a day. Too many kiwis fall into the the trap of ego and self congratulatory narcissism. Try not to be that type again. Here is a rule if you did not get it from the trash and can afford the most basic housing with safe access to a bathroom or work you are lucky compared to many kiwi families these days. If you did read Steal This Book you can see exactly the path NZ is going down now with higher risk of crime and preventable death before retirement for those in poverty. Growing inequality rarely ends well for those on the bottom of the heap or the middle.

For many they are a lot worse, even with $150k many people are still homeless as homes are more inaccessible than ever and discrimination against disabled people is rife. Medical costs like a trip to the dentists in an emergency is severely unaffordable and transport costs for disabled people can be over $100 a day easy. Not many disabled youth or those in their thirties able to afford transport to education or work. Hence many cannot afford to get to work, cannot afford the most basic bread and have no homes in NZ they can rent. Even those with jobs of $150k (household incomes greater) the cost of getting to a necessary work training function or doctors appointment means they cannot get food that week. Then there are those disabled who have a home but are on incomes below the median (most people live below the poverty line). Many cannot afford to even cover the cost of doctors appointments when internal bleeding and sepsis is likely, hence the early death rate before the age of retirement and the lack of coroner investigations (because if you don't look the outcomes from systemic societal discrimination does not need to be fixed). There is a reason many people actually used to pick up "new" belongings (e.g. clothes, necessary furniture like a fridge) from inorganic waste and why you never see a community run free shelf lacking for customers. It is just a shame it costs so much to be alive in NZ as access to basic medical services and housing is not seen as important by any government MPs or even social departments in charge of ensuring it. Access to free clothing and furniture you just need to stop by the local tipping points. But access to banking or government services and you need tech capable of modern internet services and access to necessary medical services requires more than a weeks food budget.

Sorry, if someone cannot live adequately on an household income of $150,000 there is no hope for them. I just don't believe it.

I still struggle to reconcile those views - which I agree with - with your forecast of house price increases!!!

I have asked, but no one has been able to tell me how a bank works what you have to do to meet the stress test. Does it include converting assets into cash, cashing in Kiwisaver, working longer hours, or cutting costs like health insurance, etc?

Its far more simple than that. Bank inputs into calculator loan amount applied for, test interest rate is applied. Input all expenses income etc then basically its over $0 approved. Minus $0 declined. Obviously the manipulation comes in the inputs and how you can mitigate not including some expenses etc

In a sense, that is not what will happen.

The common existing borrower might not have issues in finding extra 90$, but banks will take in consideration that they will give you circa 400$ less per month, with the same salary/income. (this is going to happen to everybody)

Houses are going to be sold anyways. Developers won't stop developing (but if they do an entire legion of people making income on buildings will suffer, which translates to more pressure on incomes). People won't stop dying, and their children will need to split the property so they will sell. Somebody will just need money, etc, etc etc...

In practice that will set a new cap on house costs on new sales.

Investors will smell crap, and some of them will count on the "long run" (wrongly) but the smart ones will sell now and live happily with a lot of money invested in things that cannot be created or by nature deflationary (gold was a good one for 10000 years ago and will be a good one for 10000 years more)

Why the long run is a bad idea? well... I do believe in automation, and believe me there are not many jobs that can not be automated (deflation by progress), I also believe that there is a loooots of space in NZ to build (and there are many technologies to do it cheap). Also... houses age, they get old, the long run is an expense.

Somebody might say that they will reopen for wild immigration, that is a political suicide. But let's pretend they do... poor people will not be able to afford a house if they don't have a very good salary... rich people can, but in an highly inflated city the low pay workers will start disappearing, so they will live in expensive cities without enough services or with very expensive services (again ++ inflation)

the system is screwed

interest rates are easy to put down, but that is burning the future

and soon or later tomorrow became today

I think today is that one

You are looking at this with a ceteris paribus mindset. Sure, finding $90 a week might not be the end of the world, but what happens when other living costs also increase.

Using anecdotal prices (as a rough example), groceries are already up maybe 10% (let’s assume an extra $30 there). The car now costs $150 to fill instead of $120 so an extra $30 there too.

Suddenly it’s an extra $150/week (from post tax income). Was this taken into consideration when loans were “stress tested”?

Interest rates are just being normalized, and we should bear in mind that even with an OCR at 3% they still would be stimulatory. Actually, in the current situation, the OCR should already be at around 4%. So it is not the end of the world, but just a slow returning back to financial and economic sanity. The current reckless over-stimulatory policy was simply not sustainable, and commentators who think that interest rates will return to recent lows, and structurally stay at those low levels, are nothing short of delusional.

The last few years of abnormally low interest rates was just a temporary phenomenon that will not repeat itself in the short and medium term. This normalization process is structural, and higher interest rates are coming and here to stay.

The delusion that debts can be paid at virtually zero interest rates is going to be destroyed. Welcome to the real world. Reality is finally going to bite whoever thought they could sustainably live beyond their means or get an easy buck out of housing speculation. There is only so much cheating that the central banks can do, before economic fundamentals start reasserting themselves.

The only way to create wealth is through innovation, hard work, productivity increases, entrepreneurship and risk-taking in the real economy. Everything else is just parasitic and only an illusion.

The world has been overspending in all areas,the cheap money has driven up prices in shares ,houses and other assets all around the world.

we have gorged on cheap junk from China, then filled up our dumps with the cheap junk that only lasted a short time.

Now we see commodity prices at record highs and we wonder why, we have plundered the planet for resources which we are now running short of, climate change is now having a huge impact on our world with parts of the world now unable to grow its own food,inequality is now at the highest level in history. Inflation is back with a vengeance, the cheap money is slowly being taken away.

welcome to the new world

I wouldn't be so glum. Climate change is changing where food can be grown. And with moisture it sure grows well.

There are p[arts of the planet where life has always been a struggle. And where charity is necessary in order for people to remain there. Clearly unsustainable. But conversely there are parts which are doing well and are crying out for people.

The baby boomers will also want a good return on the term deposits as they sell their over priced houses.

As a rule; in this country govt policy is aligned with the interests of the boomers

Nah. Look at tax (plus fiscal drag) and council rates (incl targeted rates and water) increases. Hardly pro boomer.

Just pure profligate spending. And this includes crazy welfare spending.

Yes the dream scenario now for an over 65 investor is to be able to sell this year at the record highs and move the funds into a 5% TD. The question is can that be achieved. By next march we will know.

Well said and right on the money IMO.

Should be interesting to see how many buyers are going to cough up 1.3 million for a lousy terrace cube in the back of Whenuapai at 6% mortgage rates.

Not many. If any.

Unfortunately, too many buyers have bought into the housing Ponzi in the recent past and have coughed up ridiculous prices for questionable properties. It is a humongous bubble for sure.

Not quite a terrace cube, but 5000m2 1bath 3bed lifestyle 30km from nearest small town. One of my kids wanted it and thought $1m but no more, quite serious. They heard it's had an offer of $1.5m.

Interesting. Do you have a link for that property Redcows?

Had a friend purchase, 24 ha, approx 250000, sq meter 4km from centre of a cool rural town for 1.25 million in April who had an approach to buy it off them for 2.5 million…thinking hard as worried about interest rate rise after the first year…

The problem is for those already in the market recently and on short fixed terms. The large recent house price gains have just cut a huge chunk of FHB out of the market permanently and rising rates will now keep them out even if house prices remain flat so they don't need to even worry about that 1.3 million dollar house.

You believe prices are going to remain flat at worst?

That's cute.

Yep, still expecting single digit growth in house prices for 2022. Will let you know when Homes.co.nz starts going backwards. Moved up another $20K for January. Still waiting for it to flatline let alone drop.

How any one can foresee anything else than a price decline is from another planet to be honest.

possible growth from the top end of the market (maybe), but the bottom and middle of the market are hitting a brick wall.

Forgive me. If boomerhub.co.nz says so it must be true.

We have talked about the worthlessness of that website recently.

I cannot find boomerhub.co.nz can you post a link please, hey second thoughts I'm not old enough to be able to log in. Nothing wrong with Holmes.co.nz, of course the more recently the house sold the more accurate the price is, what else do you expect ? they don't come round every month and value the house for you. It just uses modeling for house price increase/decrease percentages for what sold around you, sounds pretty logical to me to be able to put your house value in a band.

Homes.co.nz is completely off the mark and algorithme highly biased, but off course like religions homes owners don't want to see reality.

Carlos how do you know prices went up 20k in January? I think they will go down quite quickly from January onward down 20% in next six months and down another 25% six months after.After that it depends on inflation and interest rates.

Sounds very much like my prediction of housing going down 25% at the start of Covid, didn't work out to well for me.

You forgot to put your browser into incognito mode.

Never heard of an algorithm. I'm only a lowly software engineer.

It’s does allow RE override on a listed house which has been the issue. my experience though is the valuation metric is generally less than for Core Logic and auction prices in a fluid market generally it’s been in the range indicated for properties in urban areas…

Homes. Co. Nz valuations are a joke, our place is $1.3m on homes, but the ANZ app is around the $1m mark, and it was about that before they switched from corelogic to valocity too. So either valocity and corelogic are both 25% low, or homes is 30% high.

I would not base "real" house values on homes.co site, yo much manipulation by RE agents. I am hearing more of homes sale prices lowering, this year will see carnage I think.

Not very interesting tbh. Realistically, how many FHBs are spending a few hundred thousand over the average price for a house?

Interest rates still need to get back to 6 to 7% before it really starts hitting hard. Anything over that and the effect would be exponential. If people have time this year to fix for 3 years like my partner did back in November then that will delay any possible problems. I wouldn't be surprised to see the RBNZ hold off even longer so people get the message and fix to help kick the can down the road for another few years.

Ya dreaming mate….,

Not really it all depends on the OCR revision on 23rd February. Looking at the figures and the huge lag it should go up 1.0% immediately but you know it won't. Then what another few months at 0.25% increases is plenty of time for people to refix right now. Its a joke really and all those that bought a house are laughing all the way to the bank.

Oh ok, I was just agreeing with Brock that not many FHBs are going to spend $1.3m on a townhouse.

Agree. 2022 will be a year of reckoning.

People have forgotten the word "mortgagee sell" and also many have only experienced stock market boom and are now surprised to see the crash (Many had heard but experiencing first time).

With the speed the stock prices went up, have crashed with the same speed and now it is the turn of housing market, which has already started to falter and if in coming weeks auction result falls below 40%, will pick up the downside momentum with speed as those who have to sell will sell at best available price at that time thereby setting new price benchmark and this time on the lower side.

Watch for Auction result.

So I'm in my mid-thirties and I have lived through the BNZ crisis in the early 1990s, the Asian Financial Crisis, the Dotcom Bubble, the GFC, the China Credit Walkbacks and now a (second) global pandemic. I can also recall NZ being a terribly quiet, expensive and boring place to live where everything closed at 2pm on Saturdays and shops weren't open on Sundays.

This whole "many have only experienced stock market boom" thing only applies to people who are twenty or younger, and even then that's just because they were too young to remember the GFC.

So you were around 5-10 yrs old in the 90s when the Asia had debt problems. More likely you were following Captian Planet tv than the "Asian crisis".

Get a grip.

many have only experienced stock market boom and are now surprised to see the crash (Many had heard but experiencing first time).

You realise the stockmarket crashed in 2020, right? Anyone who was old enough to have Kiwisaver has experienced a crash.

March 30. Great week if you were dollar cost averaging your spare cash. I work with an individual who transferred most of his superannuation from high risk to low risk in this period. The losses were locked in and the upswing was missed. Sad.

I'd say you're older than your mid-30's if you can remember the dot com bubble because that happened in the mid '90s. And Sunday trading was legalized in 1980, and further liberalised in 1990. In the '80s shops closed around 1pm on Saturdays.

Saturday morning trading pretty much killed the late night shopping which used to be a fun experience with whole families going into town at night.

But the crash happened in the early 2000s. Someone in their mid-thirties now would have been mid-teens at the time, old enough to plausibly have been aware of the crash.

It’s all about unemployment really, and with all the boomers retiring (with tons of money to spend), it’s hard to see unemployment going very high.

Rampant inflation is probably a bigger risk for loan arrears and defaults than interest rate increases, if households continue to experience inflation at circa 6% (or higher!) it will rapidly erode the safety margin banks have build into their test rate calculations.

The very small 25bps rate rises have been too late and slow to impact inflation.

https://i.stuff.co.nz/business/300506042/reserve-bank-may-be-forced-to-…

Now we are facing the consequence of central bank over .....

yes a 0.5% OCR rise on feb 23 must be under serious consideration by RBNZ.

Yes I'm even thinking the fed might do the same in March. Powell didn't deny it the other day.

Justa . correct . need to keep ahead of the Fed or our NZD going 1 way & inflation the other..

definitely, we need to get the NZ/USD back to .70 or else oil inflation will go right thru our economy.

Right, we will just get someone to move that FX dial to 70 or whatever.

Simple, really.

I agree I have been picking 0.5 for the last rise and they did not have the balls. The end result may have to be 0.5 rises, two in a row both Feb and April. Its going to be a kick in the balls and a kick in the teeth.

Rbnz would be 'nuts' to lift the cash rate half percent. There is inflation but the housing market is not skyrocketing. Will push up the exchange rate and be detrimental to exporters.

It already has skyrocketed. Now comes the big BOOM.

Hitting all over NZ but not aust... there is a good reason for that

Short term problem. As growth drops and unemployment returns govts will soon be back to brrrrr and rate cuts, on their way to currency destruction.

Ok maybe.

Another possible outcome is that oil keeps going up making inflation even more entrenched and the RBNZ has to keep raising. At the same time the US may have to raise rates faster than expected causing a further fall in financial markets and strengthening of the USD making imports here even more expensive. So RBNZ will need to keep raising to control inflation and support the dollar which they may fail on both. I think it's easy to see how this could play out.

Or a better outcome is that supply chain issues get sorted out and people stop buying so much stuff and there is a drop in inflation. Not sure how oil is going to fall though when we aren't even flying again yet. Also Omicron is just starting to spread in China which won't help.

Yes, inflation certainly tracks oil prices, and in the long run I expect oil to get way expensive as the looming energy crisis closes in. I was thinking medium term when I made my comment - rates are rising now, but I see a big switch back in the medium term.

Steven Van Meter sums up this view today - he sees inventories rising, prices being rejected, employers already starting to lay off staff despite "labour shortages" still fresh in our ears. I can't see much of a bounce back in oil-powered travel under those circumstances.

https://www.youtube.com/watch?v=fURFhngqdkM

I think conditions (in the medium term) will flip really fast and govts will panic (there is always an election coming up) and overreact again. Manic swings are indications of the end of the debt cycle.

I watched the video and always like to hear another view. He does call himself a bond king I see so that generally puts him as more of a perma bear. Still I may follow what he says in the future. There still could be inflation with a falling economy = stagflation.

Often the short-term ( perhaps fixed for 1 year) low rate dangled is nothing but a bait. To hook the unwary borrower. What happens at the end of the fixed term? Wanna escape & go elsewhere? Sorry, break-in fees has trapped the borrower.

Closing swap rates yesterday are interesting. Flat on the 1 year, down 1 basis point at 2 years, up 16 basis points at 3 years and down slightly at all longer durations. I'm no rates market specialist, but all I can think of is this looks like either a mistake in the published 3 year rate, or at least one major market player was desperate to make a significant swaps deal at the three year duration yesterday. Does anyone feel qualified to comment?

Enter Audaxes, stage left.

This is the same as if you keep someone on a steroid for long and after stopping it there will be withdrawal symptoms.

Sanity must prevail no matter what the price is. Also, these types of articles are based on hypotheses and have not linked to reality.

The economy was also good when the OCR was 4% to 6% & no one struggled to pay off their debts why now?

Hope there will be an article soon that supports 3% OCR so that we can go back to normal it is already been more than 2 years. How long Orr wants to keep the policy loose.

Uh, I'm going to go out on a limb and say living costs for all the other stuff people have to pay for were a lot lower than when the OCR was 4% - 6%.

I only just got around to watching The Big Short last night.

"Boom"

Great movie but like just about everything in the USA they do it differently to the point its actually annoying and banking over there is very different.

A friend re-watched it recently with his wife, who was watching it for the first time. she exclaimed "did this really haappen", and he confirmed it did. I figure 90% of the population has no idea and just rides the rollercoaster. the 90% is just catching up now....

How is this. A 700k Loan increasing from 2.5 to 5.5 percent is a 120 percent increase in interest rate. But the repayments dont increase by that amount, far less, only just over 40 percent. Everything seems stacked in favour of asset owners.

The repayments don't have to change at all but the term will stretch out. Its just the interest plus what you want to repay on the principal each month. The whole thing is not linear thats why you look like your repayments are getting you nowhere for the first 10-15 years then the amount you owe goes off a cliff. Its all about smacking as much as you can afford on weekly or fortnightly repayments. The interest is a killer to start with some 75% of the repayment is interest and 25% principal and later on it switches to the other way around. Your bank can print out all the graphs its quite interesting.

Having recently read a financial article on Stuff and going over the comments it has made me realise what a fantastic website and forum Interest.co.nz is, with some very intelligent and financially literate reporters and commentators alike.

It is clear reading some Stuff comments (not all but a many) that a lot of people are simply glancing over a headline and combining that with office/social media gossip to create their views and clearly have little understanding of the subjects they are commenting on.

I used to agree with you, then covid came along and this site is now swamped with more stuff commentators and so called experts than a packed Waiheke ferry filled with gold card holders.

The really scary thing is they can all Vote.....

Mortgage rates in developed countries are still 1 to 2%.

https://www.statista.com/statistics/1211807/mortgage-interest-rates-glo…

Cannot understand why more did not take the longer term low rates on offer last year. 4 and 5 years around 3%. Herd mentality maybe... assuming they'd only keep falling.

Well to be fair we had plenty of people on here banging on about the possibility of negative rates so that was a bit of a smoke screen. The longer term rates are higher than the shorter term rates and your always tempted to go with a "special" so I guess thats why many people end up on 1 to 2 year fixed terms. If 60% of mortgages fall due this year then that tends to suggest that a 2 year fix is the most popular. I mean even now when rates could skyrocket you have that little House Mouse in your head going "rates could peak then crash again" so really its all a gamble.

I have happily fixed mortgages over the past18 months for 5 years ranging from 2.99% - 5.05% which was my latest fix last Friday. Yes rates may at some stage drop but even at 5.05% this is historically cheap. I will consider any premium I pay (in the event of a drop in rates) as an insurance premium for certainty.

A couple of reasons to take the shorter terms - this had been optimal for a long time. Doing the optimal play for 7 years and it being bad for 2 is still an optimal play.

Longer terms are a pain if you are aggressively tackling your mortgage.

Those who fixed long before the rise can look forward to inflation eroding their debt.

I fixed about 8 months ago and now have 3.39% interest rate for another 4 years. :)

Gonna be hard times for some FHBs. Rising rates on an overpriced property plus inflation eating into purchase power. Eek.

Also going to tough for interest only highly leveraged portfolio builders.....

Don't know what all the drama is about. A bank wouldn't agree to a mortgage if the borrowers couldn't afford a 3% rise, so why do we assume there'd be many FHB's who are going to struggle? If they do, it won't be because the mortgage increased, it'll be their other spending that is out of whack.

What may also be likely is that FHB's who bought in 2020/2021 with less than 20% deposit, and would therefore being paying a high LVR fee of 0.5~1.5% on top should be getting their properties revalued. They might find they now have more than 20% equity.

$700000 house. $100000 deposit for 14%. $600000 mortgage for 86%. You have 14% equity so extra fees apply.

House is now worth $900000. Mortgage is still $600000, but you now have 23% equity so extra fees no longer count.

Note that banks WILL NOT VOLUNTARILY look at this and adjust mortgage payments. You have to push them.

Banks only look at expenditure at the time you get your mortgage and refix etc. So imagine a 3% rise which we are getting close to for some borrowers (taking up the "slack"), but expenses have gone up 20% or more because of inflation. And their income is still the same as it was. So the UMI figure shrinks dramatically, or even goes negative. At which point people won't be able to afford their loan...

I guess the dreaded recession will be here when RBNZ tries to raise its OCR again.

Another blow to aspiring FHBs.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.