By Craig Simpson

The last quarter has proven to be one of the most active for funds moving up and down our various performance tables.

Across the various sectors, we've noted Fisher Funds Two (formerly Tower) has been one of the biggest improvers along with AMP.

Aon has firmly entrenched itself as one of the leading managers in KiwiSaver across most of the sectors. ANZ remain a strong proposition despite some of their returns slowing. ANZ's single sector funds continue to rank highly.

Mercer remains the best Default fund based on our regular savings return calculations.

Milford, Generate, and QuayStreet (formerly Craigs Investment Partners) are all leading managers in various categories and over different time periods. These schemes are not eligible to receive our 'best in class' award as they have not been going for the full period of our analysis.

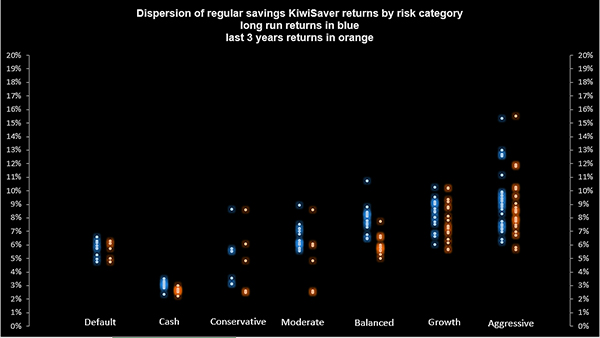

Overall, returns over the long term remain strong across the leaders. Those with KiwiSaver funds in the bottom quartile will not be so happy as their returns continue to lag. The gap between the top and bottom in each sector is still wider than you would expect from a competitive market. This is shown graphically in the chart below.

In some of the more conservative sectors of KiwiSaver, the difference between the top funds and the equivalent Default funds has shrunk. Investors in schemes with a risk profile of Balanced or below (i.e. Conservative or Moderate) are facing the prospects of not being rewarded for taking on additional risk.

The top performers continue to be those with exposure to NZ shares, listed property, and bonds.

Hedging has also played a part in this quarter's returns. Funds which have a majority hedge back to NZ dollars received some additional return pick up as the NZ dollar firmed against many of the major currencies.

Our September 2016 reviews of the Default, Conservative, Moderate, Balanced, Growth and Aggressive funds can be found here, here, here, here, here and here.

Best of the best

The funds to be awarded our special 'best in class' badge across all the various categories are listed below. These funds are the best-of-the-best as at the end of September 2016 based on our regular saving return calculations.

This is the list of the top funds at September 30, 2016, based on our regular savings return model. For comparative purposes, we have only used those managers who have been in existence for the entire analysis period of April 2008 to September 2015.

Default: Mercer Conservative Fund

Conservative: ANZ OneAnswer NZ Fixed Interest

Moderate: Aon Russell LifePoints Conservative

Balanced: AMP Nikko AM Balanced

Growth: Aon Russell LifePoints Growth

Aggressive: ANZ OneAnswer Australasian Property

The table below highlights the best funds in each main class and the range of returns between the top and bottom performers.

| Category | Top 3 Funds | Average of Top Five after fees after tax |

Average of Bottom Five after fees after tax |

# of funds invested for full period |

Top long-term return after fees after tax |

| Aggressive | 12.4% | 7.4% | 19 | ||

|

ANZ OneAnswer Australasian Property | 13.0% | |||

| #2 | Milford Active Growth | ||||

| #3 | Aon Milford | ||||

| Growth | 9.2% | 6.8% | 15 | ||

|

|

Aon Russell LifePoints Growth | 9.5% | |||

| #2 | AMP ANZ Default Balanced | ||||

| #3 | Aon Russell LifePoints 2035 | ||||

| Balanced | 8.4% | 6.9% | 14 | ||

|

AMP Nikko AM Balanced | 8.8% | |||

| #2 | Aon Russell Lifepoints 2025 | ||||

| #3 | Aon Russell Lifepoints Moderate | ||||

| Moderate | 7.0% | 5.8% | 12 | ||

|

Aon Russell LifePoints Conservative | 7.5% | |||

| #2 | ANZ OneAnswer Cons. Balanced | ||||

| #3 | ANZ Conservative Balanced | ||||

| Conservative1 | 4.6% | n/a3 | 5 | ||

|

ANZ OneAnswer NZ Fixed Interest | 5.7% | |||

| #2 | ANZ OneAnswer Int'l Fixed Interest | ||||

| #3 | Kiwi Wealth Conservative | ||||

| Default2 | 6.0% | n/a3 | 9 | ||

|

Mercer Conservative | 6.6% | |||

| #2 | ANZ Default Conservative | ||||

| #3 | ASB Conservative | ||||

1. The Conservative Fund data in the table excludes cash and default funds.

2. There are now nine default funds, however, only five have been in existence for the full period of our analysis.

3. Insufficient number of funds to provide data.

For explanations about how we calculate our 'regular savings returns' and how we classify funds, see here and here.

The right fund type for you will depend on your tolerance for risk and importantly on your life stage. You should move only after receiving appropriate advice and for a substantial reason.

8 Comments

Please remember that past performance is no guarantee of future performance .

I really wish this was the case.

It would save so many econometricians from having to construct annoying cointegration models.

no guarantee, but could be a guide to likely future performance under similar conditions

My usual comment applies here: compared to what?

There is little use looking at these results without a benchmark to compare them to. It would be straightforward to create a passive benchmark portfolio to show whether these kiwisaver managers are adding value after fees. All this data tells me is that risk is correlated with reward.

At least with Simplicity entering the marketplace, we will have a pseudo-benchmark to compare against.

ASB are already there if you wanted a long-term peer group benchmark. Investors need to move on from trying to benchmark against indices which invariably are either not appropriate or don't reflect. More merit in looking at the risk adjusted returns.

As I said, it is clear that more risk gives higher returns and more volatility. This has been long proven. This does not help you understand who is generating alpha. All the growth funds could deliver more than the conservative funds but if they all under-perform the market (after fees) that is not a good result.

ANZ fund managers have already stated that their goal is to deliver 2% above the index so that even after fees they come out ahead.

Investment returns would need to have all the hedging impact stripped out of them so you could compare the universe on a level playing field and work out who is actually adding value.

I disagree. Hedging should be neutral over the longer-term. Managers should have to justify their hedging strategy if it is causing them to underperform.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.