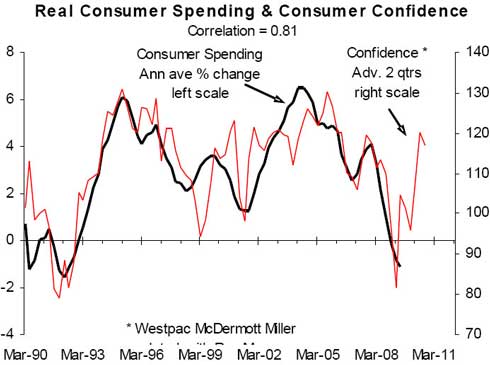

Bernard Hickey picks out 10 charts from 2009 in a series of videos to play over the Summer break. In this video he looks at the close connection over a long period between consumer confidence and consumer spending. This chart moves forward confidence to show how it is a strong predictor of consumer spending. Consumer confidence has risen sharply in the second half of 2009, indicating a sharp rise in spending through early 2010, yet the Reserve Bank is sanguine about such an increase. Rodney Dickens argues here the Reserve Bank should be more wary of such a growth and that the close connection has not been broken by consumers changing their ways.

[caption id="" align="aligncenter" width="490" caption="http://www.sra.co.nz/pdf/HousingLegacy.pdf"] [/caption]

[/caption]

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.