In its latest Gloabl Housing Market review, credit rating agency Fitch Ratings is saying:

"Australia, New Zealand and China, the markets with the region's biggest recent price rises, will experience a pronounced and overdue slowdown. We expect them to record single-digit house price growth, rather than the double-digit growth experienced last year. However, stable or improving economic growth and employment, coupled with low interest rates, limited supply and continued population growth, will support price increases in all but one of the six APAC economies covered in Fitch's report, even though prices are now out of line with incomes in several markets. Only Singapore is expected to see house prices fall, with Fitch forecasting prices to drop by a further 4% after three consecutive years of decline."

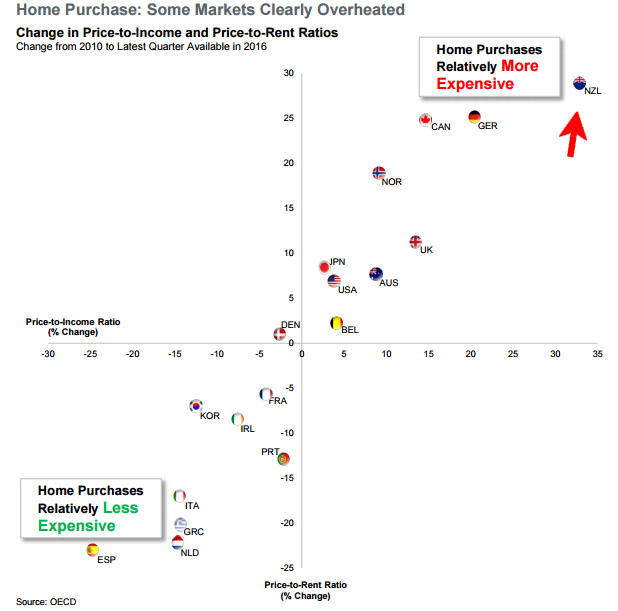

"Demand for housing in New Zealand remains strong, particularly in Auckland and surrounding areas, but we expect nominal house-price growth to slow to 5% nationally on affordability pressure and tighter regulation. Measures of relative home price expensiveness have deteriorated more in New Zealand since 2010 than in any other country covered by our report. New Zealand also had the largest regional price-growth disparity over the last four years, with a difference of over 80 percentage points between Auckland, where prices increased by some 76.3%, and those on the West Coast, which saw prices fall by 5.1% over the same period."

Here is the New Zealand component of their Report:

Home Prices: Regional Price Growth

Demand for housing in New Zealand remains strong, with the fastest home price rises occurring in regional centres outside of Auckland. Auckland increases were pegged back to 12.5% in 2016 by loan-to-value ratio restrictions reducing the number of first-time buyers and investors. Hamilton (20%), Tauranga (24%) and Wellington (20.5%) recorded strong growth in 2016, following a long period of stagnation.

Fitch expects home price discrepancies between regions to continue, with moderate growth expected in areas that border the main metropolitan areas. New regulations which impose higher deposit rates, particularly for investors, may have slowed price growth. Favourable economic conditions will likely continue to stimulate demand outside of Auckland, where there is a greater supply of affordable housing.

Affordability: Diminishing Prospects for First-Home Buyers

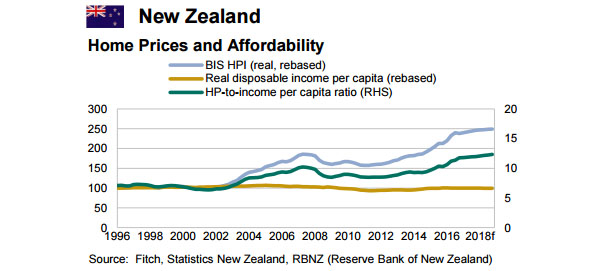

The house-price-to-income multiple in New Zealand is among the highest in the developed world. New Zealand’s rampant home price growth has affected the larger regional cities in 2016, following Auckland’s growth in previous years. Affordability pressure has started to become more evident in Auckland, particularly for first-home purchasers, where home prices are over nine times income. In other parts of the country, prices are 6 times income.

Fitch expects price growth to exceed wage growth in 2017 in a period of low rates. We expect real wage growth, which is currently about 1.5%, to increase but at a much slower pace in 2017. The introduction of limits to the loan-to-value ratio (LTV) will place an additional burden on first-home buyers trying to enter the market, particularly in regions that have experienced significant growth in 2016. We expect to see moderate nationwide home price growth of around 5%-8% in 2017.

Mortgage Performance: Stable Outlook Expected

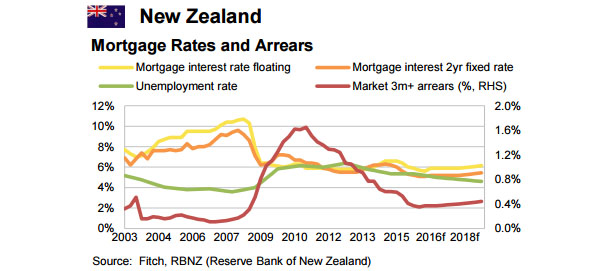

The central bank cash rate has trended downwards in New Zealand, with rate cuts of 0.25% occurring in March 2016, August 2016 and November 2016. This has provided a significant stimulus that supported strong mortgage performance in 2016. The impact of low commodity prices on the dairy sector has not hampered mortgage performance in 2016, as reported 30 plus day arrears figures indicate. Rising tourist numbers and a buoyant construction sector, combined with low unemployment, have been fundamental in driving stable mortgage performance.

Fitch expects the current performance trend to continue into 2017 supported by a rising housing market, low interest rates and a tight labour market. We expect a rate reduction of 25bp by early 2017, with potential for a rate rise to 2.25% in 2018. Fitch does not expect the future tightening cycle to create significant mortgage stress, as the economic outlook is likely to remain stable. We expect unemployment to fall by around 0.2% in 2017, with a further moderate reduction expected into 2018.

Mortgage Lending: Demand to Remain

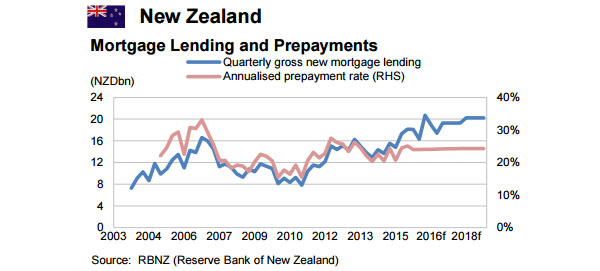

The buoyant market has prompted the Reserve Bank of New Zealand (RBNZ) to tighten the restrictions placed on banks’ residential lending, by extending the LTV limits for properties in Auckland to the rest of the country. The introduction of these limits has slowed the housing market to some extent. This will likely push sentiment lower in the regions, and have a similar effect to that which occurred in Auckland when the restrictions were initially introduced. Auckland suffered a reduction in yoy growth of 10.6%, as at October 2016. However, if low interest rates persist over an extended period, the move is more likely to fuel further home price growth and lead to higher levels of household debt.

Fitch expects lending volumes to grow, but at a slower pace with banks likely to compete via attractive offers in 2017. However, tighter underwriting and decreasing levels of affordability will moderate volumes into 2017-2018 to around 5% yoy. Stretched affordability is likely to suppress demand from new mortgage applicants, particularly in Auckland. Growth will likely come from the larger regional centres.

Regulatory Environment: Regulatory Intervention to Continue

The limits on high LTV mortgages were revised in October 2016 and a new limit was imposed. The new framework restricts low deposit lending to investors and owner occupiers by imposing minimum deposits of 40% and 20%, respectively. Further restrictions limit banks’ exposure to low deposit lending to investors and owner occupiers to 5% and 10% respectively, as a proportion of the bank’s overall mortgage portfolio.

Fitch expects that the roll out of the LTV restrictions may not have a lasting impact, as previous efforts to moderate price growth by the RBNZ by implementing LTV restrictions only had a temporary impact

The full Report is here.

54 Comments

Difficult to disagree with much of this. Returns from the property market are going to be much lower going forward. Affordability and Govt imposed restrictions will make sure that is the case. About time too!

In Auckland we will see an acceleration of the flight that has started.

Some young aspiring first home buyers will move to Hamilton, Tauranga, Wellington or smaller regional centres.

But the biggest shift out will be ageing baby boomers who:

1. Are petrified of intensification enabled by the unitary plan (don't underestimate the paranoia around this)

2. Can cash up their Auckland property asset, and retire early

An ageing baby boomer in a upper value Auckland suburb will sell their home for $1.5 million plus, they could move to say a very nice townhouse in Napier for say $600K, or a lifestyle property for say circa $1 million.

Will these factors crash the Auckland market? Possible, but I doubt it. But I think they will be factors in limiting any price growth from here

Clearly makes sense for many baby boomers to cash up and go out of town. However I do subscribe to what they have said about the London market for decades that once you are out it is very difficult to get back in...that's if you want to of course!

The emphasis is now on the baby boomers to downsize and help out their children since they are the ones who have had the free ride for the last 2 decades.

There is no free ride.

It is called work and sacrifice.

The Youf of today should get off thier telephones and other electronic gismos and actually do some real work.

Boomers built this country.

"The overwhelming message is that the ratio of New Zealand to OECD per capita has been decreasing throughout the post-war era."

http://homepages.paradise.net.nz/eastonbh/oecd800x600.gif

{kind=link}

Boomers built this country like a sandcastle so lovingly crafted - then stomped to smithereens when it's time to pack up and go home.

When the boomers joined the workforce, they could afford to buy a house on one salary, with a stay at home parent. University was free. Global competition meant a more highly paid and more stable working environment and every study conducted has shown that pure luck is what afforded the boomers their current boon. It might be true that the Millienials have been far too complacent about the security and prospects of their future, that many have been lulled into the notion that they could follow their dreams and follow their heart in terms of employment (although I doubt boomers would have been any different if they had been born in the age of the internet). However, surely the last 5 years have well and truly killed off the Millennials optimism for the future? They know they are fucked and it's not very nice of any Boomer, after the luck, stability and privilege of their birth to say hateful thing about "Youf". After all, the huge population boom of the post war years, never ever seen before or since, in all of human history are now retiring, and economists suggest that burden will still be being paid by future generations for decades to come.

"luck, stability and privilege"

Yeah?

We didn't eat out at restaurants while our children were young. Never coffees. Still don't!

When they were young we were a 1 (small) car family.

In the late 80s companies were closing down all over NZ.

There were some fees at University remember. OK not as high as now.

Sure, mortgage rates coming down from 15% over time. (But until recently, that was still happening). That, and the defined benefit govt super (required a 6.5% employee deduction) were the only "luck" things.

No one scrimping to try to get a home is frittering their money away these days either. But it doesn't help them - it doesn't change fundamentals in the market at all.

Mortgage rates were only that high when inflation was also massively high - if rates hadn't been high the principal would've been devoured quickly by inflation.

Super is being paid in tax, with Kiwisaver for one's own pension replacement on top of that.

(On that note - makes zero sense for young millenials to be paying a universal pension to their wealthy landlords, on top of rent.)

Boomers didnt build this country - cheap energy & abundant resources (per capita) did. This is why they were/are the lucky generation.

Those two things have gone and aren't coming back.

What a crock - the sacrifices of the post-war generation built the country (including government builds), the boomers got nicely affordable education, housing etc. - then decided to lower their own taxes to the point they couldn't pass the same on to the next generations. Pulled the ladder up from the next generations.

(And yes, it's tremendously confuzzling that computers now fit in the palm of one's hand, are affordable, and are a necessary part of employment and everyday life.)

Here, Here, I am sick of the Youf of today blaming Babe Boomers. There is no free lunch, their I am entitled I am entitled atitude all the time

You're right no free lunches. Therefore the "Youf" of today should stop paying tax to provide the super annuation benefit, no more food for baby boomers, no more baby boomer bludging.

Clairvoyance at work - singing the same song - again - pay attention Fritz

Fritz says:

"we will see an acceleration of the flight of ageing boomers out of Auckland that has started"

Said it yesterday - predicting the beginning ....

http://www.interest.co.nz/opinion/86049/harmoneys-justin-soong-where-wo…

Yesterday advice it started a long time ago - no more evident today than yesterday

http://www.interest.co.nz/opinion/86049/harmoneys-justin-soong-where-wo…

"But the biggest shift out will be ageing baby boomers"

I wouldn't count on people cashing up and leaving Auckland as they get older. Check out all the retirement villages being built in some of the nicer suburbs in Auckland. (Mostly sold out)

No different to 2004/2005, interest rates 7-8% heading to 10%, everything around negatively geared, Auckland slowed to 5%, as is predicted here; Provinces continued to grow at 20% p.a for another 2 years as they played catch up - but hey the news these days considers Auckland as a synonym for NZ, which is fine lots of gains still going to be had off the radar in places like Palmy - still selling like hot cakes in low 20 days (mid 30s to sell in Auckland)

To stop speculation and policies supporting speculators and overseas buyer important to vote national out.

But who do you vote in?

Not a single party will actually do anything.

#VoteForNational

Ha ha, you've got to be kidding!! No way man!

Zachary, ever the consummate troll.

Think about it. What have the others got that would make you vote for them, Spend , Spend, Spend taxpayers money. NOt Bl---y likely mate

#RentTillYouDie

You have to be willfully ignorant of opposition policy -to keep spouting this falsehood, but its a comment I often hear from National voters, as weak justification - to continue voting for a bunch dishonest chancers.

Someone hasn't been reading policies - just been watching TV?

An approx 5% increase on an average Auckland house is still quite substantial and at the same time a lot more balanced growth rate compared to crazy previous years.

Yes 5% is huge. Its higher than inflation. The only thing it will be lower than will be rates increases. Rates in the broader sense ie incl the "extra" (over and above the huge amount going into the tunnel) required for routine transport funding.

Interest.co's article last week , regarding the FIPS article , with the statement that most borrowers,already having DTI ratios of between 9-12, surely needs clarification or at least some investigation.The majority of commentators were surprised Understanding that there may be some confusion on whether net/gross metrics are used, (the RBNZ generally uses gross),whether these are new originations, it is simply stunning that New Zealand , and undoubtedly Auckland has reached such extreme levels. I have used various bank mortgage calculators in an attempt to borrow such amounts , no kids, no car and noodle diet , and have come up woefully short of 9-12 ratios.

Yeah I agree with you, I also ran a check using various bank websites to see how much a good average salaried Aucklander could afford property wise. So if a couple on an average combined salary of $120k with a reasonable sized deposit. The most they can afford is around the $650k to a max of $800k and god help them if they've got kids then your options really drop.

So the only ones that I'm aware able to borrow at such high rations were Overseas Investors and in some case new immigrants that could still access mortgage credit from abroad. Though with recent events since late December last year China has now but a stop to that by clamping down on capital flight. This would also explain the sharp drop in NZ property sales in the last few months.

Basically without pressure at the top end of the market sales and prices will naturally have to come down.

good points.

And with flight of asset-rich boomers out of Auckland, that will put pressure on the top end of market.

Totally anecdotal, but I know of at least 5 baby boomer couples who have either left Auckland in the last 6 months or will be leaving in the next 6 months.

Certainly there will be many who love Auckland and never want to leave, but I reckon the exodus will be quite significant, especially if strong population growth and its associated problems continue.

I did the same - I think something must be lost in translation if "most borrowers" are 9-12 DTI but none of the banks would appear to let you borrow at that level...

FYI, on the 9-12 DTI comment from KPMG last week. I have added a comment to the initial story on this here; - http://www.interest.co.nz/personal-finance/85999/bank-bosses-see-debt-income-ratio-between-5-and-7-ideal-any-new-rbnz-macro#comment-904284

The central bank cash rate has trended downwards in New Zealand, with rate cuts of 0.25% occurring in March 2016, August 2016 and November 2016. This has provided a significant stimulus that supported strong mortgage performance in 2016.

Hmmmm....

Which begs the question, just what was the RBNZ targeting, if not asset prices? Read more

We substituted middle class jobs for eurodollar-driven credit; now that there aren’t as many eurodollars, the economy obtains neither credit nor jobs. One could replace eurodollar with NZD bank credit collateralised by overvalued residential properties and not much else. Read more

RBNZ have pushed interest rates further than what even the banks can tollerate. Given the banks have a poor understanding of the risk they have taken on then where does that position the RBNZ's understanding of risk?

Dictator - is that an off the top of your head comment, otherwise I'd be interested to know what facts or greater knowledge and experience you have to suggest that about banks that are about a couple of hundred years old

I'm not sure where you are getting age from. It's all about understanding of financial risk. You may want to clarify your question.

e: If our banks were doing a good job at maintaining financial stability they wouldn't have had a credit rating downgrade to AA. If the RBNZ was doing a good job we would have had inflation long ago and house/share prices wouldn't be inflated with all the additional money.

Dictator youre surely joking - longevity is everything in terms of competence. Theyre aren't many businesses, if they all had a credit ratings, that wouldnt range fairly widely in that rating througout economic cycles, especially servere ones - are double/triple A ratings expected in a depression or servere recession ? - you are joking? Lets get rid of the dairy industry for instance right now!. And uninterested is correct, there had been at least one NZ "bank" (BNZ) that proved incompetent before being rescue ultimately by the Aussies, and many incompent NZ finance companies (who weren't banks).

No actually your question was unintelligible. You talk about RBNZ and NZ banks claimed they are 200 years old. That is not true and doesn't even make sense. The RBNZ was founded in 1934.

Longevity does not equal competence. I've seen plenty of US companies over 150 years old fail, and a number of those went in 2001 with the tech bubble. So your argument doesn't really stack up.

When I talk about risk I am talking about Basel II and III mostly and how some of those regulations are contrary to good risk based processes. Those regulations were applied from 2001 and contributed heavily to the problems in 2007/2008 with the credit rating agencies amplifying the problems by changing credit ratings to realistic values. These regulations are applied internationally and are used in part in NZ (for those aspects RBNZ have taken on). Given that these regulations only went into use in their current form less then 10 years ago the longevity of banks is rendered irreverent.

Your argument does not make any sense in this context. If you want to ask me a question please state it clearly and don't spend time claiming that our banks and RBNZ are over 200 years old.

The BNZ bailout is one example. More recently the banks acknowledge that they were naive in believing the evidence presented to them concerning the amount of foreign income that foreign people had.

At the time BNZ was carrying a lot of very questionable debt and the Government bailout meant that BNZ ripped off the entire country. I'm waiting to see what unfolds with the mortgage books here, there could be a cashflow timebomb burried in there.

Except popular provincial city house prices - which are still steaming ahead.

Fuelled by Auckland flight and 2008 catch up.

And some strong economic & job growth.

The graph wonderfully clearly illustrates the way in which Ms Market end-runs stupid politicians.

The immediate cause of the 2002-3 jump in unaffordability was a choice by the newly elected Labour Gubmint to 'help' poor people into their homes. The Welcome Home scheme was a typical politician's gesture to cement its electability.

Unfortunately, this was achieved (to the extent possible - the number of WHL's eventually taken up is in the low thousands) at the much wider price - gently hinted at in this 2007 article http://www.stuff.co.nz/southland-times/news/34275/Southlanders-welcome-… - of cementing in much-increased price floors all over the country.

As the article suggests but does not pursue, if a guaranteed loan (criterion for issue - can ya Fog a Mirror?) of say $100K is plugged into a market where low-end prices are well below that, then what's a vendor gonna do?

That's right, folks, tack a '1' in front of what they were asking for the shack in question.

And once ya starts this boondoggle a'rollin', it gathers speed (higher prices), it affects most of all the exact constituency it purported to assist (the poor Labour voter) and the only way out of the mess is to raise the value of the loans on offer. Which promptly sets off another round of asking-price inflation.

After all, what vendor is not going to sell for the available guaranteed-loan value plus a Modest Margin?

The secondary cause of the price inflation was the familiar one thrashed about on these here august pages for a decade: the dreadful co-incidence of spatial planning (supply limits) and more regulation (Building Act, revised in 2004, Elfin Safety mania). The planning debacle conferred a Planning Gain to developable land (paid for by the buyer, who else) and the Regulation mania increased construction costs substantially. But that only affects new builds - the price explosion I am focussing on here is for existing older stock.

A personal example will suffice - I would invite an Auckland example (where the whole thing has exploded most spectacularly) to sit alongside my experience.

We bought a shack in 2001 for my son, just around the corner, in an eastern suburb of Christchurch, for $47K. Yes, Virginia, prices like that for 'needing TLC' properties were not uncommon. We straightened it up (it had a pronounced lean to the Left as viewed from the front - ironic, innit) tarted it up with paint, ply, grass and improved the stormwater drainage plus added a foundation to replace the rotted stumps that greeted us. All Like-for-Like, all done by my son and yours truly, a nice if small unit (around 70-80 squares, we never did measure it up) basically in our spare time.

We spend around the same amount - $40-odd K - to achieve of all this, so it owed us perhaps $85-90K.

Then, mirabile dictu, the Welcome Home scheme came along. In Christchurch, the loan offered $100K.

Overnight, quite literally, it was impossible in the whole of Christchurch to buy anything that did not start with a '1'. Vendors treated the WH scheme as a universal pricing signal.

Acting economically rationally, we cashed in the little house for $123K and split the proceeds 50/50.

This proves the point about screwing up the low-end market by a naive and economically dopey funding scheme. Only 18 months prior, a deserving young FHB could have gotten it at auction for $47K - it was quite livable as is provided one trod lightly over the missing-stumps bit.

That difference - $47 to $123K or 161% in original cost - is exactly what the stoopid politicians wrought by introducing a massive re-pricing incentive. And, of course, offset by the improved condition that we provided.

And the real pity is that as noted, the pricing structure and particularly the price floor that this triggered off was universal, whereas the WH Loan applied only to a comparative few.

If one had the figures and divided the overall price adjustment NZ-wide (the increment to all house values across the region and the country stemming from the re-pricing) by the number of WH beneficiaries (accumulated all time to date), the figure would shock and horrify.

It is most probably in the hundreds of millions or even low billions per such WHL recipient. Not the sort of calculation any Gubmint cares to make....

Ms Market is indeed a stern mistress.....

Its surprising just how many "do-good" type policies that have been brought in, have had unfortunate unintended consequences. To list them all would take days. Once brought in, they are hard to remove without the perception that the party who proposes this, is evil.

I think you’re overly critical of intervention. When I was living in Australia in 2003 there was a “First home buyers grant”. A dirt poor friend of mine was finishing his PhD got his first unit with that 10K. Even though the economist Steve keen ridiculed the scheme as a first home “Vendors” grant, I saw first hand the positive effect it had on the lives of one couple.

Another friend of mine in wellington got his first home with the welcome home scheme you mentioned. He told me that he wouldn’t have been able to secure a mortgage without it.

You’re right though, those schemes likely affected the market price to some extent. BUT, what were the effects? How do quantify the value of someone owning a house who wouldn’t have owned a house otherwise? What are the long term effects? I would argue that it’s a progressive redistributive wealth transfer, and it can have enormous positive effect on the lives of the beneficiaries of these policies.

Look at it another way, What's happened in Auckland? The complete opposite! In a few short years with a National government hell bent on zero intervention, Chinese capital flight has basically destroyed the lives of people in their 30-40’s who don’t yet own real estate. National has effected a titanic regressive wealth transfer just by doing nothing in the face of rapidly changing global events. That will have huge repercussions for New Zealand society for many decades.

I’m just saying, narrowly proscribed thoughtful interventions can have great outcomes for society.

Government intervention causes varying degrees of chaos or progress. Home ownership does seem to be a really good thing and should be encouraged, the question is how best to do that. If the government had been able to gut the RMA in their first weeks in office, and, as you say, severely curtail the inflow of capital from overseas, then presumably things would be going along quite nicely by now.

National just kept Labour policy alive, making cosmetic changes so as not to appear radical or reformist, or daring or courageous, or any of those scary things the statist bureaucrats warn them about.

https://www.youtube.com/watch?v=WU1HWdlkABw

Agree, National has behaved in a disgusting manner overseeing the self-off of Auckland to foreign ownership, displacing young Kiwis from ever having a chance.

And this after they campaigned in 2007 on the need for urgent action on the housing crisis, the very existence of which they then denied for the next three terms. Disgusting, dishonest conduct.

A young person voting for National is a young person voting to rent till they die.

So if someone cant or wont commit to a loan 14x their household income, its because they are lazy and dont want to work. Nice that youll volunteer to waive your millennial subsidized welfare pension cheque.

Yeah I'm going to bite too.... Trying not to but my 50cents (inflation).

My wife and I purchased almost 10 years ago for 370k with 25k deposit saved. I saved 1k a month from the day I started work and lived with the in-laws. I did have a computer and saved hard to upgrade my phone from time to time.

We sold and from that purchased another property. In the 7 years we owned the property it went up in value approx 44K a year. After tax my wife and I would never had 44K left over a year to put towards a deposit......

Yeah, older folks who castigate young Kiwis for having a flat white or (worse) smashed avocado - that segment of the population who does - miss the fact the maths is just not on their side of the argument. Today a young couple would need to enter the workforce, often pay off their student loans first, then save almost $200,000 for a deposit on a median Auckland house through incomes of probably $40-70k over the initial stages of their careers. At which point property prices would've gone up again.

Their only hope is to find a political party that is prepared to take REAL action, not just pay lip service to only the supply side of the market.

Why do they need a student loan?

Are they stupid? Must be.

There is an excellent education to be had in in school of hard knocks.

Sorts out the wheat from the chaff.

Teachers, universities and (grand)parents need to stop telling their children that they must get a higher education. For a large number going into a trade would be better.

No wonder the standard of living is dropping in this country compared with others when you consider your comment and dictators.

In our lifetime we had Prime Ministers that didnt get past standard 6.

So what has changed?

I have to agree a lot of people are being punished with student loans that in a number of case will never be paid back. We should be reducing some of the graduate numbers where there's a major oversupply. Where there's a massive shortage noone is aware of or wanting to do the degrees. It's a damn shame.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.