Here's my Top 10 links from around the Internet at 12.30 pm today in association with NZ Mint.

As always, we welcome your additions in the comments below or via email tobernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must read today is #1 from Leith van Onselen on the RBA's surprisingly large blind spot on housing affordability.

1. RBA wags the dog - Leith van Onselen has written an excellent rebuttal at Macrobusiness.com.au to the Reserve Bank of Australia's Glenn Stevens' 'Lucky Country' speech on how affordable Australian housing still was.

Stevens said Australia's house price to income ratio was down to around 4 times income, whereas Leith points out this implies the Australian average wage would therefore be around A$105,000.

Both the Australian and New Zealand central banks appear to be in denial about how massive lending growth over the last decade has inflated property values and is distorting the economy.

They have stuck to their inflation-targeting mantra and their naive belief that free floating exchange rates without capital controls won't distort their economies.

How long before they look at the data showing New Zealand and Australia are both suffering an extreme case of Dutch Disease combined with QE-itis?

Here's Leith highlighting the RBA's group-think on housing affordability:

Indeed, only recently RP Data published research confirming that the RBA’s ratio is significantly understated. Using household income figures derived from the 2011 Census, RP Data estimated that the national median capital city dwelling price to median household income was 6.3 times in 2011

Moreover, the calculations used in Glenn Stevens’ speech directly contradicts those of the RBA’s then Head of Research, Anthony Richards, who in 2008 provided the below chart showing “Australia’s median house price to income ratio [to be] quite high by international standards”. Note that the ratios shown for the other nations are also prior to the global house price crash.

2. Brazilian stimulus plan - BBC reports Brazil is feeling the pain of a slump in commodity prices as China slows down. It is also being hammered by the strength in its real currency.

Now Brazil's government is planning a US$60 billion stimulus package, including building 8,000 kilometres of new roads and 8,000 kilometres of new railways.

So what is New Zealand planning to do to cope with the same high currency and low commodity prices?

Further announcements involving investment in ports and airports are expected in the coming weeks.

Growth in Brazil is predicted to be less than 2% this year, the weakest annual performance since 2009 and a sharp slowdown from an impressive 7.5% rise in 2010.

3. Spain's Zombie banks - FTAlphaville reports on Bank of Spain figures showing how almost completely reliant Spain's banks now are on loans from the European Central Banks.

Other banks won't lend to them.

4. Now that's some paperclip - Mike Watson reports at Stuff the Taupo District Council spent NZ$520,000 on 13 giant paperclip information boards. Some ratepayers aren't happy. HT Andrew Patterson via email.

Jack Laugesen wrote in a letter to the local paper that the clips were a "disgraceful waste of money". It was no wonder the town was indebted and homeowners were paying high rates, he said.

Another resident, Bill Lomas, said he could not understand the expense being approved when Taupo was heavily indebted. "We are the second-most-indebted council in the country. I cannot believe the cost and where the value of money spent is.

5. The case for an early Euro-zone divorce? - Nouriel Roubini has argued in this Project Syndicate piece that it may be time for an early breakup.

If a gradual process of disintegration eventually makes a eurozone breakup unavoidable, the path chosen by Germany and the ECB – large-scale financing for the eurozone periphery – would destroy the core central banks’ balance sheets. Worse still, massive losses resulting from the materialization of credit risk might jeopardize core eurozone economies’ debt sustainability, placing the survival of the European Union itself in question. In that case, surely an “orderly divorce” now is preferable to a messy split down the line.

CommentsOf course, a breakup now would be very costly, requiring an international debt conference to restructure the periphery’s debts and the core’s claims. But breaking up earlier could allow the survival of the single market and of the EU. A futile attempt to avoid a breakup for a year or two – after wasting trillions of euros in additional official financing by the core – would mean a disorderly end, including the destruction of the single market, owing to the introduction of protectionist policies on a massive scale. So, if a breakup is unavoidable, delaying it implies much higher costs.

CommentsBut politics in the eurozone does not permit consideration of an early breakup. Germany and the ECB are relying on large-scale liquidity to buy time to allow the adjustments necessary to restore growth and debt sustainability. And, despite the huge risk implied if a breakup eventually occurs, this remains the strategy to which most of the players in the eurozone are committed. Only time will tell whether betting the house to save the garage was the right move.

6.A battle of wills - Caixin reports on how central and local governments in China are locking horns over property taxes and incentives, given local governments have based their financial structures around land sales and property development.

China is in political flux in more ways than the current national once-in-a-decade changeover at a national level.

Over the past six months local governments have introduced various policies to stimulate real estate markets, which they see as a source of much-needed funds. This is in contrast to efforts by the central government, which in 2010 implemented controls to cool the market, something many fear was a dangerous bubble in the making.

Local governments pay lip service to the central governments curbs, but at the same time have made efforts to boost the market. This is a sign that they see the need to balance central government policies with finance needs.

On July 16, Shenzhen, the bustling special economic zone in southern China, said home buyers could get loans of up to 800,000 yuan from the city's Housing Fund Management Center and enjoy interest rates lower than what commercial banks offer.

Three days later two ministries said there would be no relaxation of housing control policies and governments at all levels should firmly combat rebounding home prices. Then in late July, the State Council, the country's cabinet, sent eight teams to 16 provinces and cities to supervise the implementation of its housing purchase and mortgage restrictions.

7. Inside China's graft - Caixin also reports on the now-disgraced Railways Minister Liu Zhijun and how he managed to rort the system and have a lot of fun with the ladies along the way.

Several of the charges were connected to a close associate, Shaanxi businesswoman Ding Shumiao. Ministry prosecutors say Liu helped Ding secure supply contracts worth 3 billion yuan and allowed middlemen to take kickbacks during contract procurement.

The investigation into Ding, which started in January 2011, is also finished, a source close to the inquiry said. The amount of kickbacks that Liu and Ding shared will be a key factor in determining the money involved in Liu's graft charges, a source close to the situation said.

Ding also facilitated Liu's love affairs, the notice said. The investigators found that Liu had sexual relationships with a number of women, some of them introduced to him by Ding.

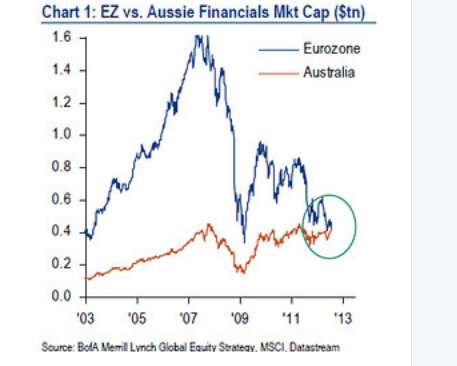

8. Way too big to fail - WSJ's Gillian Tan points to some BoA Merrill Lynch research showing Australia's banks and insurers (red line) are now worth more than the entire Euro-zone's banks and insurers (blue line).

Crikey.

“Investors seeking big dividend yields will find them in Eurozone telecommunications, Brazilian materials, Australian financials and Taiwan technology,” Mr. Hartnett said. Australia, along with Canada, Spain, Hong Kong, Singapore, China, Turkey and Indonesia, carries at least a third of its market weight in financials.

9.Finland and the Euro-zone - BBC reports Finland is having its doubts about staying in the Euro-zone.

"The Euro or Not?" That was the question posed by the front page of a recent edition of Finland's leading news magazine, Suomen Kuvalehti.

It continued: "Finland's return to the markka [the national currency before the Euro] is not impossible."

10. Totally Jon Stewart on Paul Ryan's budget plan

40 Comments

Re # 5

Council urban design and development manager John Ridd said $224,000 was spent in the development stages..

The remaining $297,000 included $199,000 for manufacturing and installing the clips, and $98,000 for work done on the project by council staff.

"If we were to make and install more clips, the cost would be only $15,000 each,"

WTF is wrong with NZ's councils - are they all required to employ MORONS or maybe there is certain quota imposed by equal employment requirements --- I wonder what the direct impact this idiotic " initiative" [ ???] has on the annual rates charged in Toopo....?

Sadly the endless criticism of LG performance over the years means that all work is now usually tendered out. In this case it is likely that even design and project management were tendered. So on the one hand you can be assured that this is the market rate but, on the other, Councils usually end up turning small jobs into big ones because of the formalitiesof the tender process.

The actual impact on rates will be either be nil or lost in the noise (see further comments below).

someone did really well out of the development budget.

Hell yes:

- the designers

- TDC in the form of resource and building consent fees (not kidding)

- Possibly consultants to research signage 'needs' and maybe consulting with the business community

- someone to draw up the tender document and administer the tender

- possibly external consultants to assess the tenders

Many a mickle makes a muckle

Bernard has been banging on about Capital Controls to help with our currency fluctuations for months and months. I have no idea what he means.

It would be a bit more professional if he were to use one of his thought pieces to set out in detail what regulations he has in mind and how they would work. He obviously lies awake at night thinking about them so he must have a crystal clear idea of who the winners and losers will be , what the impact will be and how the losers can be stopped from circumventing them.

Waripori

I've been talking about and writing about the types of controls that could be introduced for a year or so.

Here's the latest

And the one before that

http://www.interest.co.nz/opinion/60116/why-governments-are-looking-hig…

And here

http://www.interest.co.nz/opinion/59921/we-are-world-leaders-policy-dow…

I've argued in favour of loan to value ratios around the 80-90% mark, as used in Singapore and Hong Kong, or limits on affordability ratios such as servicing cost to income ratios that are used in Canada. I've also argued for a 100% local Core Funding Ratio which would mean local banks have to fund their local lending from local term deposits.

cheers

Bernard

I've read all those Bernard. I did not realise that the Reserve Bank's monetary policy targets or restrictions on who can buy a house counted as capital controls. I'll concede that moving to 100% local core funding for banks would be a capital control in that I presume there will need to be a regulation forbidding them from funding offshore including any internal funding from their parents. I dont recall you advocating that but I must have missed it.

Any idea what a move like that would do to their funding costs ( and hence lending rates) or how the ratings agencies would view a prohibition on support from their parents?

That is what I meant by a reckoning on who wins and who loses from the regulations you propose? Borrowers lose, savers win, consumers lose, exporters win in the short term anyway.

Any other ideas?. How about devaluing the currency and fixing it against a basket of trading partners currencies?

What about a 1% levy on any foreign currency bought into New Zealand? Presumably if exporters keep their proceeds offshore the currency would weaken. Might make it hard to pay wages though.

Waripori,

You ask some pretty good questions in terms of the likely consequences of any proposed controls; and what further actions those consequences would likely require. As I understand Bernard's suggestions, I personally am supportive, and imagine the consequences of the 100% local funding requirement as follows:

First it would need to be a transition, with no further net overseas funding. I don't imagine Bernard would insist on them repatriating all overseas funds they currently have overnight. As some matured they could be replaced by local funding.

All else being equal that would you would think lift savings and lending interest rates, and possibly limit the amount of funds available in the New Zealand market, which could be recessionary. The Reserve Bank could easily fix that by providing the banks with new $NZ at whatever interest rates it deemed sensible to meet funding needs so as not to be recessionary, or over inflationary.

All of this activity would also likely keep the $NZ at more competitive levels. The overseas funders would not have to be buying $NZ in order to loan them to us; or buy our assets. So demand for $NZ would be less. That drop in the NZ$ would have its own consequences- mostly positive, but happy to give my views if anyone cares.

I personally would change the chicken and egg in this process. Print the money first, fixing the dollar; and supply it at interest rates that would mean the banks would not look for overseas funds. Lean on them if they defer.

Happy for Bernard's or anyone else's views on whether I have the process correct; and whether it would be desirable.

Christchurch CBD land grab:

http://www.stuff.co.nz/the-press/news/christchurch-earthquake-2011/city…

Staggeringly the government won't have to offer the land back to owners (section 53 CER Act) but they do have to offer it to Ngai Tahu (section 59 CER Act).

Absolute insanity. How does this fit in with the Bill of Rights and the law against unreasonable seizure of property? How is this earthquake recovery - tossing out land owners, driving up prices, forcing development into areas where there is still 2 years of demolition to take place?

Are we being led by lunatics?

I see an abyss on the horizon...

On the first point, Leith is wrong. The RBA article referenced actually has a note at the bottom saying they use ABS National Accounts income measure, which includes non-wage income (from savings interest, other investments etc). When you divide this income figure into the national median dwelling price you do in fact get a ratio of 4x. So the RBA chart is correct, when using that measure of income.

More details here... The Truth about Australian House Price/Income Ratios

Leith also refers to another RPData report that shows a 6.3x ratio, but this is for capital cities only, not all -Australia, so those two ratios are not comparable.

Cheers,

JM.

How many of those incomes are underwriten, ex the housing they're being related to?

Too simplistic.

#5. $40,000.00 per paperclip. Bernard will be very happy with the stimulus approach. And quite estatic if it works out that the who $520,000.00 was borrowed. Congratulations to the Taupo DC for implementing Bernards policies.

I'm thrilled KH ;)

cheers

Bernard

#4 Understand LG finances first before you criticise them.

By all means criiticise this spend on aesthetic grounds - plenty of scope there. But let's take a look at the numbers before getting too excited.

This $0.5m expenditure will be amortised over at least 20 years judging by the heft in those steel tubes. So about $25k annually. Contrast that to Taupo's roading budget. LAst year they budgeted:

- $10.5m for operating expenses (repairs, depreciation etc but excluding finance costs)

- $9.5m for capital expenditure

And roading probably only represents 20-30%of the average rates bill; then there's the libraries, water, rubbish etc.

As I have said before, debt is a good idea (within reason, of course) in local government because it is the most efficient means of passing a fair share of today's capital costs to future beneficiaries of assets.

"debt is a good idea (within reason, of course) in local government because it is the most efficient means of passing a fair share of today's capital costs to future beneficiaries of assets." Ok, i agree with this principle

but correct me if I'm wrong Kumbel... You think this is a financially sound "investment" of signposts for a heavily indebted council, because the rest of their operating expenses are so massively beyond what they can afford that this latest spend is a drop in the bucket?

To a household analogy: "Hun, we haven't been able to pay the mortgage, we never will be able to, we've already used 4 out of 5 credit cards to pay through the last few months... We still have this Visa though, may as well get something for ourselves. Maybe we can send the kids out robbing a few more houses this week to cover the shortfall?"

How many LG's in this country, have the faintest idea about what is coming?

One or two far-sighted Councillors up and down the country (Jinty MacTavish on the DCC for instance) who could ascertain what is sustainable in the long term.

Most - both elected and executive - think in terms of 'more of the same, indefinitely'. Those folk will leave a unmaintainable infrastructure, a debt, and a permanent need to triage.

What I understand is that if you havent got it you dont spend it. Also, just because its budgeted doesnt mean you are obliged to spend it.

Two simple questions should be asked for every council project.

1. Do we really need it ?

2. If it were our own personal money would we spend it ?

You only need to look at the sorry state of local Govt finances in the Eurozone to see where these clowns are taking us.

Of course sense has to prevail the only point I am making is that sensational reports like this do not automatically mean that TDC is populated by morons. You have to find out the particulars before you leap to judgement.

midgetkiwi:

- I have no idea whether it is good or bad (because I haven't read the last ten years of budgets) except to note that Taupo relies heavily on visitors for its economic well-being.

- Government is not a household. Governments do not die or break up or move on. They do not lose their jobs or suffer injury. You cannot compare household management directly to government financial management. The main job of territorial authorities is to own and maintain important local infrastructure for you to use and your children and your grandchildren.... Their financial practices reflect this.

Kermit:

- Broadly agree- in theory the officer's reports in support of projects like this should basically answer those questions

pdk

- Spot on. The major problem with any form of public sector planning is that is generally based on linear projections based on recent history. Sadly you can't ever be found to be 'wrong' if you take this approach. How often have you heard 'we could not have foreseen that'.

- Generally councillors are takers not makers - the staff do the heavy lifting

You cannot compare household management directly to government financial management.

Correct. Most householders have to live within their means, and cannot simply mandate the provider of their income (ie their employer) to give them more.

The main job of territorial authorities is to own and maintain important local infrastructure for you to use and your children and your grandchildren....

Someone needs to point that out to them....hopefully the Govt will get a backbone and bring them under control. Council rates as a % of GDP have doubled in 10 years...thats a pretty big handbrake on the economy.

householders cannot simply mandate the provider of their income (ie their employer) to give them more - it's one hell of a privilege all right which is why we give the community the right to elect people who will exercise that privilege with care. Why is that every single councillor in 70-odd Councils has failed to exercise that right since 1996? Or maybe they have and actually this is what it truly costs to own and operate all this stuff.

Council rates as a % of GDP have doubled in 10 years - they have? I must have missed that - have you got a pointer to the data? Just kidding - I know you are exaggerating for effect and that data doesn't exist.

For what its worth:

- Householder rates only provide a portion of COuncil income, fees & charges are big and government subsidies can be significant in rural councils

- Pull apart your annual plan/LTCCP and you will find that your rates are 70-80% going to roads, water, sewer, stormwater, parks and sports facilities. Add libraries and you will be very close to 85%. The next biggest item will be democracy (elected members) and the rest (5%-ish) is all the other rats and mice.

He he. So that's why John Banks keeps getting elected (to anything).

I must have missed that - have you got a pointer to the data? Just kidding - I know you are exaggerating for effect and that data doesn't exist.

You might wish to Google "council rates as a percentage of GDP". Wont take you long to find that rates have climbed from 2% of GDP in 2002 to a touch under 4% of GDP last year.

There is plenty of talk about moving investment away from housing to the productive sector....think of the additional investment in the productive sector NZ inc could make with that extra 2% of GDP.

Once you've done that perhaps you can enlighten me as to whether or not the Auckland Council spending the thick end of $ 5,000 per m2 to replace a toilet block in a Nth Shore Park is good value for ratepayers money...or sending 36 delegates to a Local Govt conference in Queenstown.

Yep found the Business Roundtable graph showing rates moving from around 2% of GDPin 2002 to around 2.9% in 2009. And forecast to rise to about 3.9% by 2019. Rates are not expenditure which, in turn, is not expense.

Also found the LGNZ graph showing total expenditure rising from 3 to 3.8% of gdp between 2006 and 2011.

There's no doubling anywhere that I can see.

Re Finland .... Kiwis dont know much about Finland its a bit off the radar .Typical of Northern European nations, Finland is an extremely successful little country with a well run economy , and a highly edcuated and productive workforce.

Their Germanic approach to fiscal discipline has stood them in good stead and they would be quite right to quit the Euro .

Cool. I've still got some Finnish markka that I bought back to the country in 2001 and no-one was willing to exchange into NZ$ :-)

I think this is the key point:

Only time will tell whether betting the house to save the garage was the right move.

One bum can't ride two horses, so for better or worse they must see it through for the next furlong at least.

Well that's Solid Energy off the block.

Pity - it's the one with the most liabilities pending.

Too cryptic for me. Can you expand on why Solid Energy is off the block?

Wasn't Solid Energy the one with the recent accident which injured a miner, which had the potential to be fatal? Being investigated currently i think...

This should be interesting to anyone interested in the monetary system:

IMF Paper Backs Full Reserve BankingYou can read more here: http://www.positivemoney.org.uk/2012/08/imf-backs-full-reserve-banking/

4. Surely any Council does not need to pay anyone for a design. Why not advertise what they want, where, and the area for it to cover and just say the successful design, with not being obliged to accept any design, will have the designers name on it when it is built.

Perhaps their Reserve Bank lent it to them as ours did in 1935. A country doesn't have to borrow overseas you know.

Bring back the old Ministry of Works, and all the old Govt Depts, long since privatised.

Ministry of Works could have whacked a sign up there for a couple of grand, no consultants, fancy pants designers etc, required. WTF, it's only a sign.

Way too many hangers-on in LG these days.

Especially since they can't even afford to run the outfit without mountains of debt.

Maybe because MoW didn't suffer the twin burdens of the cult of the manager and neo-classical the market is always right crap.

There is no doubt that a few items used to fall off the back of MoW trucks.

But the value was commensurate. A shovel here, a chainsaw there ......

Not so for PPP, where councils act like kids in a lolly shop, buy now - pay later.

Except, it's the ratepayers that have to pay & pay & pay .....and that's just the interest.

#1. It's fascinating that the US sub-prime housing market blew up at a house price/income ratio of only 3.5. I guess the explanation is that income inequality in the US is higher than here. It does make you wonder though about how far Aus and NZ house prices could fall in a recession.

I don't think the NZ Gov't will allow residential house prices to fall. That's the reason they are allowing non-residents to buy property here. If house prices did fall the NZ Gov't would probably bail out the banks similar to what the Irish Gov't did. Whatever they do NZ is screwed.

"Just wish they had to have some sort of economic understanding to qualify to run a country"

It is not a prerequiste and therein lies the problem.

The Toopo paperclips are way over the top in terms of the costs involved -

I have many years experience in designing /costing and fabricating similar light engineering projects such as street furniture and from what I can see in the photos the price should have been around $6-7K absolute max per unit fully installed by the supplier - No BS about resource consent etc and absolutely no way would the design costs be anything like what has been claimed - 224k is a ludicrous sum and if anyone was to suggest otherwise they would need an in-depth head examination !

I am glad you have posted on this matter as I have some experience in engineering but have been out of the field for a while. The prices seem way over the top to me though, and your estimate would be generous for what the manufacturing, finishing and installation invovled. Hell I reckon I could get the long radius sections rolled then weld and paint the rest in my garage, there is nothing complicated involved in their fabrication. With my Architecture studies thus far I would not have too much trouble with the design and research phases either. Three months work all up tops.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.