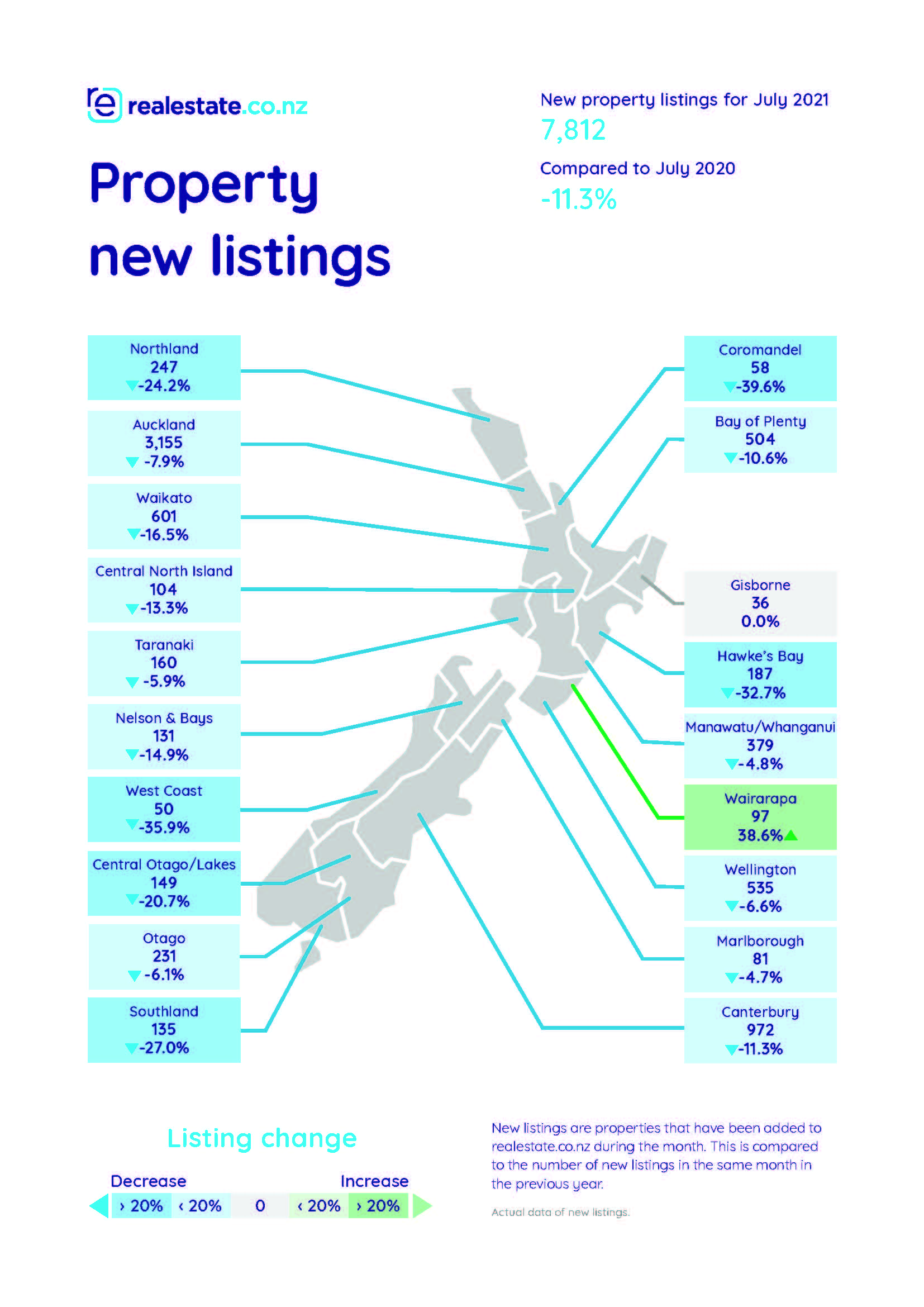

The number of people deciding to put their homes on the market appears to have flattened out in July, with property website Realestate.co.nz receiving 7812 new residential listings in July, up just 0.6% compared to June.

Around the country new listings in July were up compared to June in eight regions - Auckland, Waikato, Bay of Plenty, Central North Island, Wairarapa, Nelson, Canterbury and Otago, and down in 11 - Northland, Coromandel, Gisborne, Hawkes Bay, Taranaki, Manawatu/Whanganui, Wellington, Marlborough, West Coast Central Otago and Southland.

Compared to July last year, new listings were substantially lower, with a decline of 11.3% nationally, with all regions recording a decline in new listings compared to a year ago, apart from Gisborne where the numbers were unchanged (see the table below).

Help us keep our content free. Support us by choosing ad-free. Find out more.

However, real estate activity in winter last year was at elevated levels as the market recovered from sharp reduced activity from March to May due to the pandemic lockdown restrictions.

Compared to July 2019, new listings in July this year were up 6.6% nationally and up 28.7% in Auckland.

Price expectations remain firm, with average asking prices increasing in all main centres, pushing the national average asking price up to a new record of $870,395 in July, up from $861,411 in June.

However, while price expectations were firmer in the main centres they were weaker in the provinces, with July's average asking prices down compared to June in Coromandel, Gisborne, Wairarapa, Taranaki, West Coast, Nelson and Marlborough.

The comment stream on this story is now closed.

58 Comments

Supply squeeze. People can't live in housing consents; they live in real houses.

Be quick.

Be quick for what exactly?

The next leg up in prices, when borders are reopened and all those people still being approved visas and residents permits pour in.

Anecdotally (from a few migrants on working visas) that most of them plus friends are actually eyeing off Aussie. Both countries need migrants but the general consensus is

1. Fewer hoops to jump through for migrants into Aussie - especially European and British migrants who now have a streamlined process into Australia.

2. Wages are considerably better over the ditch

3. Housing including renting is significantly cheaper and better quality than NZ

So I wouldnt immediately assume when borders open that everyone will rush to NZ - the neighbours have just as much if not more to offer.

Yes many have already left. When the bubble was closing there were 20,000 Kiwis in Aus that hadn't yet returned since the bubble opened. I expect that a large number of them aren't coming back. The RBNZ is very arrogant to think that they can pump up the market like this and people won't escape to Australia.

The same thing is happening in Australia.

Rookie numbers compared to here though.

the current housing problem is the concentration of house ownership towards investors.

no matter how many new houses hit the market, they will be purchased by investors.

housing supply increases but rate of ownership keeps going down.

It does seem obvious that you can have 'enough' houses and still rising prices, if investors are buying up the supply. We could build any number of houses and still have a 'shortage' if there are enough willing investors and they can borrow enough money. Is this actually happening? My instinct says yes, but I'm not sure how you'd prove it, I'm not a statistician.

What we can be sure of is that investors won't stop piling in until they get a strong signal from the rental market that they *can't* get tenants to pay a rent that will cover their outgoings. That will always be a lagging indicator. There's also the risk that the Gov't will find new ways to prop up rental prices to stop that from happening - to stop that signal from ever being sent.

A very big lagging indicator. Investors can find tenants now, but in 12 months time? With borders closed, we rely on natural population growth. Births @ 54k per annum/4.5k p/month 18 yrs ago. FHB = 3k purchases/m, potential 3-4k people leaving rentals. Investor purchases (C31) over 3k p/m. Assume 50% add to stock & 3 per rental that's 4.5k extra people housed.

4.5k + 3k (conservative) FHB = 7.5k "bedrooms" added to supply a month. With a need for 4.5k assume 100% of 18 year olds need to move into a rental.

Going as far back as 2013 I've thought that we've never really had a housing supply issue. Its more that we've haven't had enough houses available for property investors to speculate on using equity in other previously owned properties.

Perhaps we should have built separate provinces where property investors could play their game of debt speculation with no residents/tenants (they're simply a pain in the arse anyway aren't they?). Could call it fools paradise. Then have other provinces where young families can live and buy 'homes' to live in and live normal lives without having to compete with debt speculators simply to own a basic necessity of life (shelter).

Yep and low interest rates have made the situation even worse and there is still no end in sight. Even if the RBNZ takes the OCR to 1% in August its still not going to fix the problem now. House price gains have simply been epic, there are currently no reasons to expect it cannot continue.

Well there are reasons if there were rational market participants. But markets aren't rational, nor are many people particularly across western society at present. So perhaps you are right.

It may get to a point, if we're not there already, that the price of living in NZ makes it a very unattractive place to live (if you are born here) or move to (if from overseas). When we get to that point and existing people leave and new people don't come, then the downside risks are massive. And it won't matter what the government nor the RBNZ do - it will simply be beyond their control (in equal proportion to how it has been in their attempts to control price inflation on the way up - i.e. completely ineffective).

Animal Spirits by Shiller and Akerlof is a good read on this topic.

Unfortunately New Zealand will always be attractive to people from India or Mainland China while horribly unattractive to people from the rest of the developed world.

Our demographics are already reflecting this and its going to continue deteriorating.

Not exactly. South Africans and Brits keep coming as well. They just don't have the shear population size as China/India does.

South Africa isn't really part of the developed world anymore. It's a basket case and it feels like NZ is heading in the same direction.

Plenty of Brits, but not so many that intend to stay long term. The UK is generally a better place to live.

That is pretty harsh, it's a cheaper place to live perhaps but not better in relative terms. There is however a slightly better chance of owning a home there (65.2 vs 64.5 here in 2018) but there is nothing in it really.

Relative terms like what?

Air quality, food quality, water quality.

Much cheaper ammo there tho which is good cos your gonna need it for your 9 mil.

Air quality is a bit worse, granted.

Food quality in the UK is quite a bit better than here, with much more selection and cheaper prices.

Water quality... I guess there is a lot of limescale in the south east otherwise water is water.

Much better career opportunities. Warm housing. Cheap and easy travel. Much cheaper consumer goods. Amazon. Better health system. Better transport. Always tons of things to see and do.

Britain can be a marvellous place to live if you have a good job and a decent wedge of money.

However certain "underprivileged" areas of New Zealands' most populated city are paradise compared to the utter squalor and deprivation in many UK cities and towns.

Yeh... they all just want their PR or Kiwi passport and they be going along their way until they turn old and wrinkly, in which case they will all come back.

Good safety net for them folks who want to retire in lush greenery and quiet scenic views. Sorry to say this, but NZ is essentially becoming more and more like 'white privilege & rich privilege'.

Totally agree IO. I think there’s a total lack of entrepreneurship here in NZ where you think you’re an entrepreneur if you own a rental property or two. There are serious unforeseen consequences heading our way.

Yes what scares me are the people who have become 'wealthy' but they don't even know why nor the social implications of their windfall.

Hit them up about it and clearly you are simply 'envious' as opposed to worrying about social cohesion and the well being of society and the prospects of futures generations who chose to stay here....(and all I can do is facepalm).

I agree. When I talk about this I feel very miss-understood, it's like people can't comprehend why I think about the bigger society impacts and I must be just upset about the situation because I don't own a house. (I can buy one if I choose but I move a lot and invest in stocks instead).

Landlording is the world's second oldest profession. As such, it's here to stay indefinitely. And does in fact, have very useful social implications.

Care to list a few?

Building homes for those who are unable to house themselves. This has always been the case since the Industrial Revolution. Landlords have an asset that they rent to others for their use.

"By 2018, just over 1.4 million people lived in houses they did not own, including 120,000 children under five years of age. Although private renting predominated for all age groups, almost one-third of renters aged 65 and over lived in social housing." Only 1/3 of people renting live in social housing.

Do you have any data on what proportion of investment properties were built to rent? My feeling is that the vast majority of rental properties in NZ were bought as existing properties and that most investors just buy houses that already exist and put them into the rental pool, with no net effect on housing supply.

I could be wrong and maybe the stats are different up in Auckland with people buying apartments off-plan to rent - very curious to know if you have any data to support your argument.

I don't have that specific data but I have other data.

1.7 million houses are privately occupied, housing around 4.3 million people. Around one third of New Zealand’s homes have been built in the last 20 years.

Homeownership peaked in the 1990s, at 73.8 percent of households, but by 2018, homeownership had fallen to 64.5 percent of households, so lets average that out and say home ownership is an average of 69%. Therefore 31% of all homes are rentals.

I have built 80% of the houses I own in my own rental business and amongst the investors I know it is about 50% on average.

Interesting. I'd guess that your peers and especially you are rather higher than average but I don't have the data either. Given the new regulations, I think the numbers of build-to-rents will increase which I think is more socially useful than buying existing properties to rent. I've also seen some institutional interest in build-to-rent, such as KPG on the NZX.

More generally, I'd like to see us head back towards that 70%.

There is certainly a use for landlords - university students don't want to buy a property, many businesses don't want to own their properties, etc. No arguments there.

In NZ, we're way beyond the share of housing that would be 'useful' and into 'parasitic' territory. You certainly can have too much of a good thing.

Xero, RocketLab, Zuru, Weta Digital...

Or maybe we could legislate much higher LVR's, DTI's and interest rates for "investers". Maybe 50% LVR, 3x DTI and interest rate set at business loan rates.

Even a simple DTI ratio of 5-6 without any ability to claim rent as an income would bring the investment train to a juddering halt. Suddenly it becomes very difficult to buy more than 1 rental property every decade or two.

“ no matter how many new houses hit the market, they will be purchased by investors.”

Nail on the head.

People who can’t afford will never be able to afford no matter what (low price or high supply)

Only works of there is an undersupply in housing, if there is an oversupply the market will collapse. Luckily local councils and government can be relied on to maintain an undersupply.

A rational market will collapse.

An irrational market may continue for a very long time until catastrophie.

New builds in Auckland Eastern suburbs are mainly quite low quality. $5.5 million paid for newish good property after 2 days on the market. Sold to retirees not familiy. Apparently more higher quality new builds required but landowners/developers not willing to spend the money.

Are they not built to the housing code? If so they will not get their CCC. If they are built to code then they are being built to the highest quality standard we have ever had.

@JustAnOpinion,

I am going to assume you are being sarcastic in your response. CCC and the overall quality of finish are two very distinctive things!

It's almost as if there is a tax that will hammer some people for selling now and will drop to zero if they wait a little bit.

RE NZ Auckland listings for houses and townhouses last Sunday was: 4199

August 4th 2019 it was 5695.

Down 26%.

Orewa was 103 in August 2019. August 21 it was 68

Red Beach 2 years ago was 45. This August it was 16

Millwater was 100 two years ago.. Now it is 53

yes, that is inventory, not new listings. But not looking good is it??

Why is stock so low, why is no one selling when mania remains?

Brightline Test?

Why would you sell when the cost of buying another house is so prohibitive (all those tax changes coming home to roost)? Is there a better asset to get into than housing?

Upsizing, downsizing, relocating, divorce, death a few reasons why you'd sell...

Yes. Also more now are owned by investors as the percentage of rentals in NZ has increased.

It is not just New Zealand where listings are low and falling , and demand appears to be out pacing supply. Ireland, with some of the toughest LTI and LTV measures in the world is also seeing rapid price growth, a very low level of active listings and available mortgages around the 2 percent level.

Daft gives its latest quarterly update https://ww1.daft.ie/report?d_rd=1 and https://ww1.daft.ie/report/2021-Q2-houseprice-daftreport.pdf?d_rd=1

If you are selling the house you live in you are going to have to buy in the same market, hence there's little appetite to do so, unless one is downsizing.

Nice stats, thanks Mike.

Surprise surprise. Supply goes down, Demand remains high, and Prices continue to creep up even with all these strict regulations in place (and also with the knowledge that interest rates are going to go higher from here on out).

People are surprised? What did you expect really? Damage has been down and it prices will not fall. Record money printing, low supply, low interest rates, and nowhere to spend your hard earned savings... Of course people will plow into accumulation of assets. Holding cash at the bank loses you money (inflation is going to be 4%, and term deposits get you a mere 1%?). You be better off spending your money on assets then holding cash.

Congratulations to the FHB who saved for many years and finally got a house during these record low interest rates. Well done and well deserved. For those FHB who did not make it this round, keep on saving but don't wait for a "market crash" - as it wont' be happening anytime soon (if it does).

New property listings largely flat in July but asking prices still rising in the main centres

Why Not.......Mr Orr and Roberstons, even nearly after six months still waiting for effect on housing policy announced in March.......Wait and Watch...........really.....

Every month house prices are touching new height and both are waiting on sideline .......WAITING FOR WHAT ???

Very few have asking prices on them as they are usually tender or deadline sales.

Interest rate rises are really the only way to affect prices unless the government brings in taxes

I am seeing houses in some smaller regions not selling and asking prices dropping a little bit. But it is like a Mexican standoff. I think prices in some areas became too expensive for investors and this has had a knock on effect.

It doesn't take too much for smaller regions to experience price fluctuations. Like Bitcoin, if you make money in the regions, realise the gains and get out before it drops overnight.

Not so much an issue in Auckland or bigger towns.

Team,

The NZ housing market is following what's happening in other developed countries.

With the minimum wage going up each year, materials hard to come by, land being drip fed, no extra overseas builders to come to help fill the void as builders retire, don't expect prices to drop, or even flatten in major NZ cities, until the world comes back to some kind of normality. Whatever normality is.

The fact that I made 260k in 8 months, and now 100k (and going... I estimate 200k when it is built) on another build that's commencing soon, you might as well get on the bus if you can and enjoy the ride. This is a once in a life-time chance to make your money work harder for you and deliver quick results.

Update: 260k realised gains, not some estimate. It's sitting in my bank account.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.