By David Hargreaves

The Real Estate Institute of New Zealand (REINZ) says the housing market "roared into life" in October with sales volumes rising 32.6% from a year ago and the median house price surging NZ$9,000, or 2.4%, from September to a record high of NZ$380,000.

Auckland's median house price rose 2.9% in the month to a fresh record high of NZ$530,000.

The national median house price is up 5.8% compared with October last year, while the Auckland median price is up 14% compared with October last year.

REINZ chief executive Helen O’Sullivan, said although there had been a "springtime surge" in new listings, this was struggling to keep pace with buyer demand.

This had led to a further drop in the average number of days taken to sell to 32 days from 33 in September. The 32 days time to sell recorded in October was an improvement of three days compared with October 2011. For the month of October, Canterbury/Westland recorded the shortest days to sell at 28 days, followed by Auckland and Otago with 29 days. Over the past 10 years, which includes the boom years of 2002-2008, the median time to sell in October has been 33 days.

Sales volumes rose across the country in October, with 6,640 unconditional residential sales, an increase of 1,633, or 32.6%, compared with the same time last year and an increase of 17.5% compared with September. There was NZ$1 billion more worth of property sold in the month than in the same month a year ago. However, price rises are not occurring evenly across the country.

"The market is very much in two parts," O'Sullivan said. "The metropolitan regions of Auckland, Wellington and Christchurch - where prices are rising - and the rest of the country where price trends are mixed."

"Within Auckland, most of the activity is in close proximity to the central city, the northern suburbs and eastern beaches. Buyer enthusiasm is less evident in South Auckland and the rural fringes north and south which is reflected in smaller increases in the median price and a longer time for sales to be achieved."

'Keen appetite for more expensive homes'

Buyers are showing a keen appetite for more expensive homes.

The REINZ figures show that in the past year, sales of houses in the NZ$600,000 to NZ$1 million band increased 73%, while in the over NZ$1 million band, sales rocketed by a staggering 96%.

On a regional basis the highest lift in prices during October was recorded by the Canterbury/Westland region, up 3.9%. Auckland came next with its 2.9% lift and then Otago with 2.1%.

Compared with October 2011, Auckland recorded the highest lift in prices with an increase of 14%, followed by Canterbury/Westland with 4.3% and Otago with 3.4%.

In terms of volumes for the month of October compared with the previous month, the top numbers were recorded by Taranaki, with a 56.7% increase, followed by Wellington with a 27.2% rise and Hawkes Bay with a 23.8% lift. All regions did report increased volumes during the month.

And likewise, all regions had gains in sales volume compared to October last year, with Central Otago Lakes recording the top rise of 54.4%, followed by Northland with 52% and Hawkes Bay with 47.7%.

Stratified index at record high

The REINZ Stratified House Price Index, which adjusts for some of the variations in mix that can impact on the median price, is 6.9% higher than October 2011 and is at another record high.

The House Price Indices for Auckland and Wellington also set new record highs in October.

Auctions are proving an increasingly popular way to sell houses. Nationally there were 1,343 dwellings sold by auction in October representing 20.2% of all sales, up from 689 sales in October 2011 representing 13.8% of all sales.

This is a new national record for the percentage of sales by auction and beats the previous high of 20% reached last month. Auction sales in Auckland also reached a new record with more than 38% of all sales in the region in October sold by auction, or more than 1,000 sales.

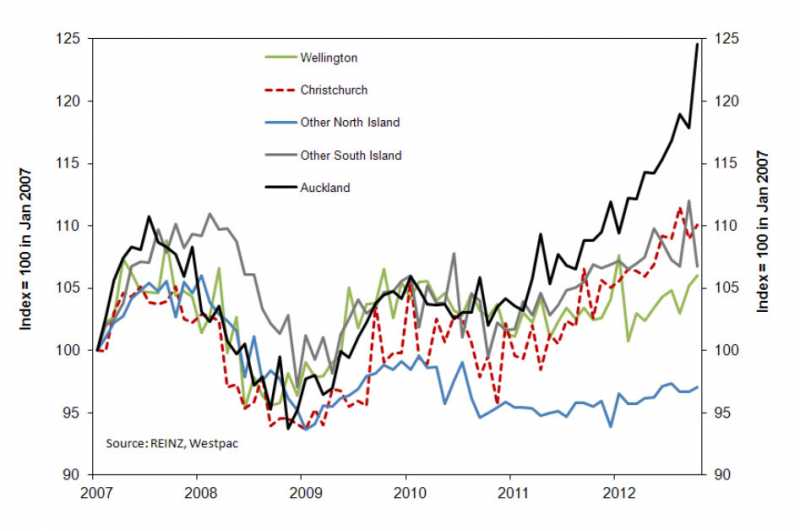

See a Westpac chart below showing Auckland house prices sprinting higher since early 2009 and accelerating through 2012. Other North Island prices are flat, while South Island prices have also been rising since the Christchurch earthquakes.

'Demand, not supply'

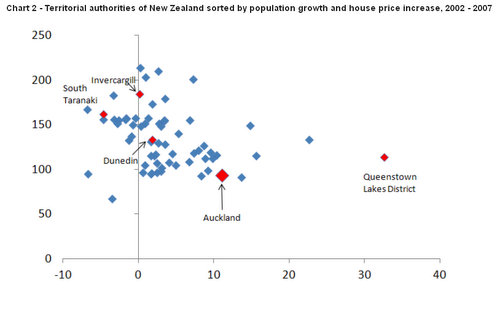

See Westpac chart below showing house prices not necessarily linked to population growth, challenging the suggestion that migration to Auckland and supply shortages are the main reason for house price rises there.

See comments here from Westpac Chief Economist Dominick Stephens on the REINZ figures, which he described as a stunning but not surprising acceleration. He also argued demand side factors such as low interest rates were more important than supply.

I seriously doubt that supply measures will do much to bring house prices down. That's because financial factors have played a far greater role in taking house prices to where they are than physical supply or demand. Consider the evidence from last decade's house price boom. Regions with unusually high population growth actually tended to have lower house price inflation (see chart 2 below). Auckland's population rose 11% over six years, and house prices rose 93%. Compare that to South Taranaki, where the population fell 5% but prices rose 161%. Or Invercargill, where the total population increase was 100 people, yet house prices rose 181%. Restrictions on land supply didn't seem to matter last decade. Dunedin has a famously expansive urban limit, and was the largest city in New Zealand by land area until the Auckland super-city was founded. Yet Dunedin house prices rose 133% over six years, much faster than "restricted" Auckland or Queenstown.

The fact is, houses are a long-lived asset. As such, their price is strongly influenced by interest rates, taxation, and people's expectations of future price changes. In my view, low interest rates will continue to drive house prices higher for some time. But by the same token, an eventual increase in interest rates could have a large negative effect on house prices. So be careful out there!

Stephens said he had also compiled the same data for the 2007-2011 period, which showed physical supply factors were more influential in house prices in recent years. Here's his comments:

The places with low building and high population growth were the places with the highest house price inflation in 2011. Also, unlike last decade, rents are rising strongly in Auckland and Christchurch. This points to physical factors playing a role, because physical factors should affect rents in the same way as they affect prices.

However, I also think that interest rates are playing an increasing role this year. For example, Auckland population growth has slowed and building has increased since 2011. Yet house price inflation has accelerated, not decelerated.

(Updates with details, reaction from Westpac, charts)

House price index

Select chart tabs

94 Comments

Is anyone really that surprised that if you make credit cheap (emergency lows for interest rates) and readily available (banks lifting restrictions on the amount they will loan) that the housing market takes off? When credit was constrained between late 2007 and mid 2009 (initially due to high interest rates then due to the GFC) prices fell by anything up to 10%. Now we are seeing the reverse. All this waffle about planning restriction etc is just a diversion - housing bubbles are a function of mispriced/misallocated credit. It would appear that the only policy that either the government or the RBNZ (I should really drop the 'or' as they are really the same thing)can come up with to provide the appearance of 'growth' is to reflate the housing bubble.

andyh - I am sympathetic to your view - but the RBNZ household housing lending statistics don't stand up to boom scrutiny - and in fact they are no where near as strong as the 2002 -06/07 ann. credit growth property boom #s of ~14.00% plus.

I can only think transfer payments from excess government borrowings in the form of contracts to preferred consultant elites etc are leaking into the housing market.

The boom is only in the top 4 deciles. Change in decile median prices from July 2007:

/*-->*/

1 = - 6,000

2 = -10,500

3 = -25,000

4 = - 250

5 = 5,000

6 = 250

7 = 44,000

8 = 45,250

9 = 43,500

10= 59,000

Is it time to blame investors? Are they buying?

I haven't seen them, what is your experrince? Where are they buying?

Absolutely, cheap credit , dumb lending criteria, media telling everybody nows a great time to buy with low interest rates and 90% of the public being sucked in. Now there will be panic buying so they don't miss out fueling more price gains. Quick you need to rush down the bank and get a massive loan !

This bubble effect may not just be New Zealand. Goldman reports a new housing bubble in a number of selected countries, caused by the monetary easing in the world.

http://www.cnbc.com/id/49740329

No excuse for the government and RB to ignore it though; and the report notes that some controls outside OCRs are the best/only way to deal with the situation.

Face it, the people running the Reserve Bank are just useless pencil pushers. Hoping for anything but the status quo was our first mistake.

But if the Reserve bank raises interest rates to combat house inflation it will attract in even more hot money as New Zealand's interests rates will be so much more than Japan, US and Europe. This will cause our exchange rate to rise even more. The high dollar and interest rates will crash our already fragile economy. Unemployment will surge past 10%.

This is New Zealand's policy makers conundrum. You either solve house affordability directly by something like Hugh's proposals or Bernard's massive rebuild of state housing.

Alternatively you change monetary policy, you tighten credit supply to the housing market while easing it for business investment, Gareth's idea. Or you allow the Reserve Bank to intervene in the foreign exchange market to reduce the exchange rate, as the Greens etc are proposing.

Wheeler seems to be indicating that the government should try Hugh's solution to solving the problem. That if housing supply constraints were removed we wouldn't have house price inflation. He has indicated the Reserve Bank will not solve this problem for the government.

Whatever happens we are fast reaching a turning point. The do nothing option is not looking very attractive.

Stop foreign nationals buying residential property in NZ would pretty much quench 80% of the current boom in one.

Thatr's why, despite modest credit growth, we have a booming property market, because a large chunk of the market isn't even related to local credit! I'm unconvinced that even raising interest rates or enacting LVR restrictions would make much of a difference since such a large proportion of this property boom is driven by foreign money.

Auckland up 3% in October - will this inflation moderate or are we heading from froth to bubble territory.

SK, We have been in bubble territory for some time now, the bubble is now stretching to bursting point...

really - so you will be cashing up any day now?

I dont agree with the above comments.

Rising house prices are the result of money printing in most other countries with investors all looking for a home for their cheap money. This is what the USA wants (but weve got it instead) in order to make the average joe feel positive and start spending again.

Lifting interest rates will not help NZ, our productive sectors are struggling with a very high dollar and weak demand.

House prices can only properly be controled by sorting out the supply side which is constrained by poor planning, GST, lack of development finance, lack of skilled labour and high building costs and far to many leaky homes.

NZ will/is become a destination for the rich purely because of its geographic safety and sound agr based economy (compared to some). This alone will distrot our house prices due our very small market. Simple supply and demand rules.

Could you then please explain what was different about the supply side between late 2007 and mid 2009 when house prices fell 10%?

Was there a huge flood of new houses built and marketed during that time? No

Was there a sudden relaxation in the planning process? No

Was there a sudden change is the availability of skilled labour? No

And yet house prices fell markedly.

In fact there were no changes in any of the factors that you allude to as determining house prices - yet house prices fell markedly and were on course to fall further UNTIL emergency low interest rates were introduced.

Really this meme about supply side constraints needs to be challenged vigorously.

Its all about credit.

One further point about your claim that rising house prices elsewhere are simply due to money printing.

If that were the case then why arent house prices booming in the UK - the nation that has been printing perhaps most actively (in terms of per capita)?

According to the 3 principal UK measures of HPI house prices are stagnant or falling - yet they have printed billions.

Why?

Simple - because although the UK banks are flush with money they are refusing point blank to loan it on new mortgages - mortgage lending is at ultra low levels (indeed interest only mortgages, previously so important, have almost all now been withdrawn). The net effect is that there is virtually no credit available to stimulate the UK housing market (the opposite of what we have here in NZ).

As a result the UK housing market continues to drift down, DESPITE all that printing by the BoE (all the excess money is simply going into buying gilts).

As I said "other Countries are printing money", we are not - investors in these other countries are busy moving their money to countries that arent printing (NZ, Australia, Canada) in order to preserve the value of their asset i.e money printing depreciates the value of their cash. And in the case of England there is a total loss of confidence so due to the uncertainty most wise people will divest there asset base (property) (therefore more supply on market and less demand as those sellers are not returning back into the same market) and move there funds elsewhere e.g. NZ farms and property, or gold etc. Until confidence is gained back in the UK market house price there will go nowhere - in time this will turn around and demand will come back which will drive the market up again.

common Andy!!!! Its about supply AND demand.

07 to 09 demand went down, pure and simple, So although supply was still weak, prices fell because of the fall away in demand.

At the moment, demand is booming and supply is stagnant, hence the rise in prices.

But you hint at a good point, in that to truly address the problem both supply and demand solutions are needed. Thats why I advocate suppply side measures ie. more housing, as well as demand side measures ie. less immigration, LVRs

Theoretically, supply or demand side messures in isolation could both be quite effective, but in reality a combination is best

You're correct Matt it's supply AND demand that must be addressed. But the supply problem is long term and will take several years even in ideal circumstances to turn around. The demand however can be fixed tomorrow. Change the sentiment, the euphoric expectations and the demand could evaporate in a month, much as it does in a economic crisis like the GFC or 1998 Asian crisis. All it would require is Wheeler announcing some prudential measures for the Auckland market around lower LVR's and bank funding ratios and the government mentioning restrictions on foreign ownership and immigration. No interest rate rises required

Sure credit is part of the mix but only one part of it - in 07/08 there was a cataclysmic event - there were few buyers and lots more sellers hence the price fall. From there few new houses got built to supply a still growing popuation resulting in what we see now - demand exceeding supply .......... simple.

Low interest rates were introduced as demand for new credit dropped - this was done to encourage borrows (demand) back into the market - all to get the ball rolling in a world reliant on money supply and the merry go round.

andyh:

Has the whole of NZ which has access to this cheap credit experienced price growth in the last year or is it limited only to the supply constrained cities (see the QV reports from yesterday)?

Have the supply restricted markets elsewhere in the world seen their prices rise higher and fall further than the less restricted markets (e.g. California vs Texas)?

Have the markets with ZIRP experienced massive house price increases since 2008 (UK/Europe/US/Japan)?

House price inflation is not a simply down to one factor. Supply shortages, if not the cause, certainly magnify the the pain for everyone. The shorter the supply, the faster the price rises and the bigger the falls when they come.

The sensible solution is to fix both the supply and demand sides of the problem. Sensible, but probably not palatable.

I think if you look at todays REINZ report (the QV report lags the actual market by several months as I recall) you will see that Wellington has now joined the price rises which initially were restricted to Auckland, and then Auckland and CChurch ie the price rises are starting to ripple out from our biggest conurbation initially. Unless I am mistaken that is pretty typical of how house price bubbles inflate initially (metropolitan outwards) - there is nothing unusual about this.

Re: ZIRP etc - see my reply above regarding the UK which clearly indicates that you must have BOTH a) cheap credit and b) access to cheap credit (which we have here now in NZ) for bubble inflation.

I agree with andyh here.

The bubble we're currently seeing is speculative and hype. Currently the greedy with easy access to credit see that either there's a chance to make money quickly or, in the case of first home buyers, they've got to get in now before prices begin another eight years of massive growth.

There's no supply constraint. Rental housing is actually pretty easy to come by (as someone who was recently shopping for a rental) and in the last year, finding a place to rent in Auckland seems to have gotten easier. We're TOLD there's a shortage, but i think this is just patter from the landlords and the press designed to maximise their dollar and get better returns on their investments.

To my mind, the main drivers of the big-city booms we're seeing at the moment (in order of importance) are.

1. Money coming in from foreign sources and non-resident investors buying up large chunks of urban stock.

2=. Low interest rates and an upswing in prices triggering latent first home buyers into action.

2= Banks loosening their lending practices, allowing 95% and (in some cases) 100% home loans again. Higher rents are encouraging many people into housing as you don't need much of a deposit and owning is superficially almost as cheap as renting, so long as you can rely on capital gains and low interest.

4. Prohibitively expensive compliancing costs for new builds inside our urban centres (anecdotal evidence that to subdivide a section and build a 3-bedroom house on it can require up to $180,000 in fees and taxes to the council before you've turned a sod of earth or hammered in a nail)

5. The media and the REI, doing as they always do and fanning whatever flames they can find.

The above creates a perfect storm, with the inevitable upward pressure on prices. The trouble is that it's not got a grounding in a solid economy so what you're seeing is just vapour and won't be a protracted boom, more a sharp bubble that's going to burst and leave plenty of people far more exposed than they'd like.

I certainly agree with you re: the hype. The NZ Herald website certainly pumps up the so called good news stories like rising house prices much more than it does bad news like the appalling unemployment rise. Have a look at its website now. Its a joke.

I've been quite shocked at how much more balanced the Aussie newspapers are on these matters, as I had been led to believe both the Aus media and public and media are as obsessed with housing as kiwis. From what I've seen, they are not. Much healthier..

I also agree wiht your last comment that this looks very much like a dangerous bubble that could turn nasty

I will riot when these bubble creators (those who sign up for massive mortagages) inevitably get into strife and want a bailout. People need to have their eyes open and do their mortgage repayment calculations on 10% p.a.

So much pain is on it's way - rest of the world suffering - NZ bidding like mad at auctions with other peoples money. Crazy.

green eyes

He's jealous because his financial prudence will be penalised through higher taxes to bail out those who have been financially reckless and profited from it?

Yeah, okay.

If Esprit's availability of rentals feedback is reasonably correct then it is quite pivotal.

It is my belief that what we're seeing here, similar to USA '01 to '08, is largely a shift in hitherto renters buying due low rates. All the other factors; population, supply, incomes (except rises created by rising property prices) etc seem to have remained too static to match price movements upwards.

A quiet increase in the amount of rentals available is proof.

Good to see NZ funds are going into existing unproductive assets and the money earned from interest is heading over seas along with our working talent?

1st law of bubbles: You won't see the peak until it is past

2nd law: The bigger the upside, the bigger the downside

3rd law: Prices drop 3 times faster than they went up

Just wait for someone to tell you that we are not in a bubble and current house prices are the new paradigm. Then sit back, relax and watch the carnage unfold.

Yep. This AKL RE action is looking remarkably similar to crude over last couple years (or in fact, many others); On it's way up, people found or created reasons to justify it, and so its momentum became the trade for the time. Now it's sitting just above half where it peaked and continues to trend down.

Very few markets can avoid being elastic, or in other words, if they become too expensive, other ways will be found.

AKL is unlikely to be different and at this point has become too stupid to buy into, keeping in mind it's not deep, and once the sell signal is obvious it will be too late to try.

Ollie's advice to "buy with your ears pinned back" is righteous, but only after a correction and when peeps are licking their wounds and have sworn off it.

In meantime, if there are any knowledgeable and creative punters who have ideas on how to short, I'm all ears... If there is a reversal, somebody is going to pull off a John Paulson.

All I know is that these big price movements are viewed cynically by market movers around the world as simply a trade. Nothing more or less. And once exhausted, the next trade is to push it all the way back...

Surely shorting is selling the houses you own with a view to buying back cheaper? later so you rent in the meantime.

The problem with that is, where do you store your capital safely for the time when you can buy back?

If it goes as badly as I think then I'd expect 1 or more if not all of the big 4/6 banks to have been nationalised....with huge losses for depositors.

The only thing I see is selling to clear out debt, because debt will still be owed on matter what...aka Bernard H.

regards

Gee, I hope not, mate. If the banks do get nationalised, then I would expect it is because the govt has to print up funds to cover depositors. Without that, faith in everything else will fail. Yep, being cashed up is to short housing, on 1:1 ratio, while those with big balls might leverage a dropping NZD, buy options on things that would spike (say debt collection, or caravan sales), sell or write options on things you're reasonably certain will drop. Unfortunately Weldon's NZX is not exactly useful for this or much else, so you have to try to do this synthetically on more sophitcated exchanges overseas. Not easy. 99% of people at the time thought Paulson was mad to put on his big shorts... It's all just whimsical lady luck, evidenced by his performance since. That to me is why cash is always king, and while right now every man and his dog is trying to get rid of it, in this crazy world it don't be surprised if it makes a big comeback.

It is in NZ Inc interests to see inflation occur as it is a natural process of the economic system we operate by.

No market is 100% efficient so they are therefore never "balanced". All we are seeing in the residential property market is a lift in values based on decreased supply and increased demand which is all due to numerous factors that nobody can ever control.

The doomster's (or green eyed monsters) here need to look at history to see that this has all happened before but it is meant to happen as it is a "market". Stop trying to control it because the market will always win in the end e.g. property development compliance costs will become cheaper over time and developers will find funding and more supply will hit the market or NZ will have a foot and mouth outbreak and then noboby would want to be here!!! Who knows what will be will be - play the game if youve got the nouse........ those that have have made good coin have done well................. only time will tell if they can keep it :)

Wow Grumpy are you asking "please give me inflation"? I would you next time you go to purchase anything from a merchant with a charity box put 5/10/20% of the bill in the charity box. You will quickly feel the pain of inflation.

Wages/Salaries are going no where. Unemployment is rising fast. The dollar is crippling our foreign earnings. But we have kiwis importing like mad and bidding up prices on property.

Your invitation of inflation is paramount to treason. "Play the game if you've got the nouse" hell tell that to the 15 year olds who will have to pick up the financial mess being created.

There will be plenty of McJobs for the 15yr olds - do not worry.

Do you respect your elders? I think that it's really important that we raise generations that do respect those who came before them.

Your comment I hope is tongue in cheek (although I read you regularly as a property bull - hoping for average prices to reach even higher), you seem to have no worry to run down the future generation.

One day you will be reliant on these younger generations, they will be your carers, doctors, dentists, suppliers and politicians.

and tenants.

These two words make you look terribly shallow.

For someone who is 'absolutely most certainly not a slave to banks and mortgages' - you are rather serious.

anyway thats enough - see everyone at coldplay - even though they are a bit Middle Of The Road.

Not a bank slave - Look at history and tell me its not a fact that inflation has been dominant over deflation for a long long time.

As long as the population growths exponentially we will get inflation (in a normal economy).

Yep I agree the dollar "at the moment" is a problem, employees dont know how lucky they are with the spoon feed system NZ has.

I think if you have a closer look, that parts of the current hot property market in NZ have alot of foriegn influence which is certainly helping the market.

Ive got 15 year old kids and they have been (or are been) taught how to play the game we are all in - get educated, get a good job, invest in gloom and sell in boom, and play the greater fool game but make sure they are not the fool.................. And most of all learn to adapted to change.

I know plenty of sharp young people that are playing the game and have their own house - there are planty of ways to skin the cat as long as they dont want to start at the top.

Treason my arse - welcome to the real world !!!

My parents had a government loan at 2%. They built brand new in Wadestown in Welly. Dad worked in a book shop, mum was at home, they had six kids. This was normal. Now there is zero chance of this happening, why? Was it a bad thing? Is NZ better off that houses have rocketed to massive financial burdens?

Grumpy your comment is flawed - re read it. "I know plenty of sharp young people that are playing the game and have their own house..." Grumpy it's not a game, it's a genuine need - kiwis need to have a chance to put down roots and own their own home. For my Dad it wasn't about being "Sharp" it was about raising a family, contributing to our country.

Think of the reality of raising a family the burden of debt required to get in anywhere. Think of what is better - NZ where property was normal/manageable or now where owning is a crippling activity.

This is your "real world" and it sucks. It sucks that the younger generation have "play the greater fool game but make sure they are not the fool...". These are your words and they condemn this modern NZ where in a few generations the reality of home ownership has become a dream.

Mr Grumpy;

1. Inflation requires full employment, something I'm not sure is possible any more what with automation, peak this/that and the "population growths exponentially" thing you mention. Pure deflation is upon us all, held back only temporarily by low rates and a collective mania happening right now, which always seems to preceed a big ouch.

2. The Turkish slave-driving owner of LA-based commodities house I worked would declare during his daily rev-ups, "You should all be in the top 50% of the team." WTF? Did somebody forget that we had to pass Series 3 exams to be there, which were tough enough to foil overly confident math majors when I started? Point being; Somebody has to be the fool. So if it's not ideal for your kids to end up the fool, does that make it OK for it to be your brother's kids, or somebody else's? That boss? Well, like MF and PFG, he was shut down by the Feds for being a fraudulent POS and in his case is lucky not to be getting a stripey suntan. This being long after I left of course.

Sir idlebumski;

1. Inflation doesnt require full employment, it comes in may different forms (exchange rate, droughts, scarcity of resources etc etc). Most of the western world economies are busy printing to stop deflation happening. This in itself will push inflation into the NZ economy at some stage in the future. The simple fact that the world is growthing exponentially means that inflation will continue to occur until the world can grow no longer - who knows when that will be?!?!?!?!

2. The deregulation of the banking/finance industry in the 1990's (the free market) throughout the western world and lack of statutory controls let this sort of thing happen, yes it was bad but the wise and lucky saw what was coming and got out. Sure that may sound arogant but the fact is theres alot of sheep following each other around rather than doing their analysis and make their own decisions and moving a differnet way to the herd. Thats is my point re the greater fool and that is the game we are all in - understand a market, understand the financials, understand the business, understand human greed and you are well ahead of the pack.

@idelbumski

Series 3 exams

Lol - I sat that one too back in 1982 - three hour paper. I suppose you also sat the screen based multiple choice NASDAQ exam.

Hi Mr Hulme. Yes, back in '04 with W beating Op Iraqi Liberation wardrums, it seemed a no-brainer to get into the biz of trading crude et al, given nothing much else was lucrative or accessable. Could only go a couple of years though, once it was obvious I had entered the my clients' capital destruction biz for benefit of mafia who run the US exchanges and sociopaths who often run boiler room brokerages. Glad for the experience I suppose, but am happier to now have the inside knowledge of how instruments traded on these markets work and affect our world. Series 3 for us was combo of futures/options mechanics, plus rules and regs; 70% (or above) score required to pass. I have noted your similar background and as such, always enjoy and respect your posts.

Hi Mr Grumpy. Actually love all posts, including yours, but have to admit those from the holders of AKL RE who seem to think it good karma to laugh at anybody who is a landless peasant, can be a bit enraging. Anyway, I would just like to suggest most of what is going on right now is directly due TO no more growth. Why else dump money into treasuries or the Kiwi equilvilent, being AKL houses? That we all have different opinions is what makes this board such a reliable brain trust.

Idlebumski - I agree with your last comments maybe its time to leave the herd and run the other way? Time to get short treasuries and anything related to property?

Off on a bit of a tangent here regarding the situation with the Kaipara Council. Saw Campbell Live the other night and an older bloke, about 87 said a beauty "The younger generations should pay for this, we've paid our taxes". This is where this country is heading LET THE NEXT GENERATION PAY FOR OUR STUPIDITY. Human nature at its finest haha

I see this all the time. The 'haves' generate this idea that the next generation is "different" to them. They see the world as foreign to them and that the youth are bad - that they'd be different.

This is because deep down they know that they truly grew up in a blest country where everyone had a real chance of making it, where you could own a house and raise a family on a basic job. Deep down they know that the prices they get from the same house in the same town has robbed the youth of those same opportunities. They know when they sell one of the rental portfolio that the younger people will need two salaries (sorry no chance for raising kids younger generation) and many many more years to pay it off.

Deep down they know that they hold the houses, they run the bylaws, they have little/no mortgages (hence don't worry when interest rates trend back up).

"The younger generations should pay for this, we've paid our taxes" this meme see young people as totally different - not really kiwi, not really worth the worry.

Not a bank slave - Alot of the "haves" (as you call them - r your eyes green?) I know have worked very hard to get to where they are (sure some havent but these ones tend to be the ones that loose it).

The supposive system you talk off controlled by the haves is bullshit - most of the planners in councils are from the UK or are fresh out of Uni - most of these guys are not well off. The "system" we all live in is far to complex to control - the market will always win!!

The younger generation needs to get of thier little white arses and make it happen - drinking and playing on the computor isnt going to do it for them and money wont fall out of the sky.

Typical "older generation" comment. People work more hours on average now than they ever did back in previous decades. Moreso, home ownership used to be realistic on one salary, something that's now a pipe dream.

Sure, you can work hard and buy a house, but not without taking on a mountain of debt an order of magnitude greater than your income. "Work harder" is a misnomer from a byogne age...... most people are already working more than one job, or more than the institutional 40-hours, just to make rent.

We don't exist in a true market. We have so many interferring factors. The game (your word above) is stacked against the younger generation.

The reality of property for most is that they want a home. Most of the older generation set out in this regard, purchased their home and paid it off (and couldn't care less about the latest headlines). But for the younger generation they see the market as an impossibility (a primary reason so many give up on NZ).

All the risk sits with the younger generation. If they buy now they run the risk of a drop wiping them out (unlike the older generation sitting mortgage free). If they buy now they run the risk of rates going up and increasing larger amounts of income go into paying back interest.

Few of the younger generation get started in property (unlike previous generations) where it was the norm. If you reply "yes but we had to beg the bank manager, we had to save 30%" - I would say great this is the way it should be now.

In following with this theme I'll chip in my 2 cents as a Gen Y, this country has gone to the dogs. Absolutely. 40-50 years ago NZ had so much promise and I can imagine you could get by on a one income family, paying mortgage and looking after children, on an average wage. These days its a struggle for people to get by on two incomes, with children, mortgage etc. If that doesnt say anything about the quality of life in NZ now then I don't know what does. I have a mate thats a lawyer, well paid, good deposit, all he can afford is a shoebox in Otahuhu. Or Otara. Its quite pathetic. The only promise that people of my generation see is moving overseas. We have a wonderful country, and if you're born here, you have a RIGHT to own a home and have a family. IMO

Also with regards to property bulls I would just like to say that its not a game, its not a boatload of fun having to find an appropriate home for your family, the fact that you treat it as such is odd to me. Also I love the green eyes thing lol

Is your lawyer mate trying to buy without a mortgage? If not, has he got a big enough deposit? A 300-350K shoe box in south Auckland should be affordable/mortgage servicable by someone on 6 figures??

Lack of deposit seems to be the biggest barrier to getting on the ladder.

No, high prices seem to be the biggest barrier. Banks will happily lend 95% to most people.... 100% in some cases.

Yeah his deposit would be pretty sizeable I imagine. No he has to get a mortgage. I would also like to say that sometimes I have the pleasure of company that is a lot older and wiser than myself, 50-90 age bracket, and pretty much all of these people think whats happening in Auckland is absolutely ridiculous, and these are mostly rich folk from the eastern bays, they cant believe whats going on. It wasn't this tough in their day, so they say.

A few months back I was doing some work at an older 1880s house, and found some newspapers from the 1950s pasted to the walls.

It was the letters to the editor, and the letter (written by lady of mature age) was, to paraphrase, a lamentation of the high cost of housing and the fact that young people would never be able to purchase their own home.

To be honest, what was she on about?

What are you lot on about?

Housing is only ridiculously expensive if the yield is below the real interest rate (which at the moment is probably less than 2.5% (nominal interest rate less inflation rate)), OR if the yield's at those levels and you're in a location that you would expect to decline in price relative to rest of the market.

$1m for a home that costs $900pw to rent, in one of the most desirable suburbs of NZ's biggest city, doesn't sound like a bad deal in an environment of 5% interest rates and 2.5% inflation.

$300,000 houses that rent at $500pw in good suburbs sound like a bloody good deal. (Other cities exist outside Auckland!).

Maybe the whingers and whiners could realise that houses cost money to build and replace, and that you can't be expected to be able to afford one if you're idea of a days activity is blogging on a website like this...

Friday, 5 o'clock, the day is gone...

for someone who whinges regularly about the state of the Christchurch rebuild, I would have thought you would have had more sympathy for the disenfranchised young Aucklanders. People who will probably never be able to buy a home in the city they live, work and pay taxes in... but it seems you are a whiner about the 'injustices' of your life, without stopping to consider the impact of lack of leadership and home building in the Big City and the lives of people here.

Firstly, I have no sympathy for first home buyers who believe they deserve the first home to be a stylishly character home on its own site in a tree lined street in Epsom or Mt Eden, and that it should be cheaper than renting...

But I certainly think that there should be a different approach to building, however that mainly needs to be around council development costs and what the government is doing with its straightjacket of state housing (which is driving up prices within the state housing belt and restricting organic growth of the inner Auckland suburbs).

In fact, I am increasing supply of affordable homes as we speak (well it's what I should be doing right now instead of mucking around here...), working on plans for 2 new "mini" houses. Both smaller 130m2 plus garage on 200-300m2 inner ChCh suburban sites. It will be interesting to see the final costings but realistically I'm not expecting them to be under $220k each excluding land.

Personally I don't think Auckland property in unachievable. North Shore real estate is reasonably cheap. West Auckland is very cheap. Yes Central Auckland is bloody expensive but opportunities still exist (at the start of this year I looked through a number of character properties in Onehunga, Sandringham and Mt Albert for under $550,000. Remember that you don't rent much for under $600 or even $700pw (which would pay a hefty mortgage).

By the way today I looked through half a dozen very good properties in ChCh priced in the $200s. Some were even in the $100s and below if you are brave...

I have no sympathy for people who think they should be allowed to be carried along on other peoples shoulders due to asset (house price ) inflation. Asset inflation isn't wealth creation it simply creates a hole that has to be filled (by selling to a rich Chinese person or over charging a Kiwi).

Markets decide pricing for themselves. Prices can go down too, but there are fundamental reasons why that is not the case for property in prime locations at this point in time.

In the 1950's there wasn't a globalised property market or an immigrant servicing sector. There was no Harcourts Shanghai. The population was low and people had quater acre sections with fruit trees, hens and vege gardens.

Savings Working Group

January 2011

“The big adverse gap in productivity between New Zealand and other countries opened up from the 1970s to the early 1990s. The policy choice that increased immigration – given the number of employers increasingly unable to pay First-World wages to the existing population and all the capital requirements that increasing populations involve – looks likely to have worked almost directly against the adjustment New Zealand needed to make and it might have been better off with a lower rate of net immigration. This adjustment would have involved a lower real interest rate (and cost of capital) and a lower real exchange rate, meaning a more favourable environment for raising the low level of productive capital per worker and labour productivity. The low level of capital per worker is a striking symptom of New Zealand’s economic challenge.

”

http://www.treasury.govt.nz/publications/reviews-consultation/savingsworkinggroup/pdfs/swg-report-jan11.pdf

Our council tried to build a new mulitmillion dollar library using this arguement. Luckily there was a public outcry.

And they are thinking of reducing interest rates further due to the high unemployment, but this won't any difference to the economy or dollar apart from pushing the price of houses up further. People are investing in houses simply becuase that is the only safe investment that is producing any real gains, and it also has the advantage that it will have a tax free capital gain. Banks also are not interested in people saving, they just want to lend people money, as they have a lot of cheap money to lend at the moment. I went into a bank to setup a new savings account, and they weren't interested, and said I would need to come back next week and make an appointment. I wasn't going to bother with that.

FYI this guy wasn't really a have, he had a freehold home in a rural town and would be on the pension, but I see where you're coming from.

Quite right Sore-loser the Counils are the developers.

and he would have a comparatively free ride on the public systems of his time.

The guy is 87. He would have been 20 years of age in 1945

List the "public systems" that were available then in the 1940's and 1950's, (during his family formation years) that he could have had a free ride on. Give your statement some credibility SK

So much for those who are demanding cheaper credit from the RB...more likely to be going up...

It never ceases to amaze me the number of nay sayers that fill these columns, despite evidence to the contrary (literally) staring them in the face.

Yes, house prices in Auckland are going up, and are going to continue to go up and I'll tell you why. One of the most basic and fundamental rule of economics is supply and demand and it's effect on prices. Supply of Auckland houses, very low and getting lower. Demand for Auckland houses, very high and getting higher. Effect on prices, they go up, it's that simple.

Interest rates we are experiencing at the moment are more in line with what the rest of the western world pays, higher in fact. So the current rates are very likely to become the norm, in any event, high interest rates did not stop the boom from 2003 - 2007. In the current environment the NZ govt can't increase interest rates without killing our rural and export sector (due to the inevitable increase in the NZD which would follow) so an increase in house prices are seen as very much the lesser of two evils.

Auckland is a very young city and it's only just starting to develop the way all other western cities already have. In most cities in the world first home buyers start life in a 1 or 2 bed apartment or flat and work their way up to a house. Kiwi's seem to think it is thier right that thier first home is a 3-4 bed house on the city fringe for only $350K, this is laughable. Auckland is currently going through this development and more and more we are going to see our young people buying apartments; which by the way are still very good value.

"Demand" is largely psychological though, and influenced by so much more than just the need for housing. It's influenced by the job market, the amount of easy credit, the performance of economies around the other side of the world, the perceived likelihood that the market is about to go up or down.

Much of the demand at the moment is speculative... ie, buying for no other reason than the expectation that the market is going to gain. This s largely driven by hype, certainly not good economic fundamentals. The kiwi family is getting poorer by the day (wages not keeping up with inflation) and their ability to pay down ever-larger debt is decreasing.... ergo, the fundamentals (other than hot Chinese money flooding our market) is pointing to lower demand.....

If you can't see the divide you're either blind, naive or your eyes are wilfully shut.

Demand is not largely psychological, people need to live somewhere.

By looking too much at average incomes your ignoring the people who are currently driving the demand, they are people inheriting, money coming in with people finishing OE's, money coming from generous baby boomer parents and people who accumulated equity in the naughties boom (a boom I bet you sat on the sidelines for while the rest of us made our fortunes).

Lets let the market settle this argument for us; I'll see you back here in 4 years time and we'll see what prices have done.

Yes, people need to live somewhere, but let's say (hypothetically) that all of a sudden LVR requirements drop to 70% max and the interest rate jumps to 10%. What do you think would happen to property prices? They'd drop like a stone. The DEMAND hasn't changed, just as many people need to live in just the same number of houses, but the available cash in the market has dropped, so prices will fall.

Now, what do you think will happen if the conditions remained the same but people THOUGHT that the above scenario was about to happen? The same thing, there'd be a rush to sell-up while the going was still good.

The media, the REINZ and the government can all talk up the market as much as they like, and this breeds PSYCHOLOGICAL confidence, which boosts the market.... now what if none of these positive sentiments have any grounding in truth? Things like "surprisingly" high unemployment numbers, dud-numbers coming out of China all point to things not being quite as rosy as a lot of the powers that be would have us believe.

The average person cannot afford a house in sensible commuting range of Auckland any more without saving for ten years, and then taking out a 30 year mortgage... this won't continue, no matter how much many homeowners would like it to.

Reality is that NZ would be in a much healthy state if we had had no bubble in property and that you could purchase a home for 3x income. There would be disposible income to spend and save.

It would be interesting to calculate the GDP that would need to go to cover the interest on mortgage if interest rates were at 10% (hell only 5 years ago). I'm picking we are getting in well over our heads.

LVR requirements are not going to drop to 70% max and interest rates to 10%, we don't live in Somalia. You focus too much on the average Jo and not enough on the people actually buying houses. The people buying the houses are not on average incomes and do not take 10 years to save a deposit.

I've been flicking through the comments on this story and just realised that you've been at this all day ! ! Have you got nothing better to do? Are you one of those unemployed I keep hearing about?

I can still read the words you type whether they are in CAPS or not.

What's your incentive to try and talk down the market? You trying to get on the ladder?

Hypothetical situation, extremes to make things clear. Of course I know they're not going to happen, but the undeniable truth is that housing affordability has gone down the toilet in the last decade, and the only thing that's keeping house ownership possible for kiwis, is a combination of irresponsible lending practices (where did that get the world in '05-'07?) and government handouts (WFF).

You also said it yourself, home ownership used to be out of reach of the poor. Now it's out of reach for the average. How much longer before it's out of reach of the vast majority? How much longer before the lion's share of our property market is in foreign ownership, bought with funny money, and all but the wealthiest 10% are tennants in their own country? Because that's the road we're headed down.

And no, I'm not unemployed, and I do what I like thankyou. Thankyou for being so patronising about the use of caps.... perhaps you'd prefer if I used bold or italics to emphasise points... or will you be patronising about them too?

I have no incentive to talk down the market. I'm not silly enough to think that something I say on here has any affect whatsoever on the market. If the market were more sensible, yes I'd be trying to buy a property in Auckland to live in, but I'm not looking at ladders.... simply a place to lay my head at night and start a family.

I could buy a house tomorrow if I wanted, by the standard of most, I could buy a nice house in a nice suburb.... I just feel that now is nto the right time and that it's not wise to buy into the hype.

As the saying goes, the smart money gets out when everyone else is getting in.... and the smart money goes in when everyone else is getting out. Given that every man and his dog seems to be clamouring to get onto yor much-vaunted ladder right now, I think my money is better used elsewhere for the time being.

Fair enough argument Esprit, just a few comments......

"If the market were more sensible, yes I'd be trying to buy a property in Auckland to live in,"

The market is what it is, I did all my rental buying between 2008 and earlier this year in Auckland. The fundamentals are now of course out of wack at the moment but Mr Market will do what it wants........http://en.wikipedia.org/wiki/Mr._Market Its a great time to sell (especially if you couldn't sell in 2007) and its also a great time to hold. There inevitably will be a slow down, but I believe this wont be for a we while and now 2013/2014 (or beyond) will be referred to as the 'new peak.' Larger parts of ex-Auckland City houses will now be out of reach for most punters (just as parts of it has always been). If you did buy now you could/would be 10% better off next year. If you don't well your deposit will keep growing :)

In the mean time you say "I think my money is better used elsewhere for the time being", care to devulge where, please don't say bank deposits.......;)

What did you buy?

Stand alone 3 beddys of traditional and non-leaky material, close to schools, public transport and quiet streets- easy renters. Only have had 4 weeks of non-vacancy across all the properties in 4 years. Not game enough to buy units, apartments, or home and incomes :)

Problem one is that incomes haven't risen at the same rate as they were in 2003.

Problem two is that extra capacity of people taking on the mortgage (now you pretty much find two incomes are needed - one to live off one to pay the mortgage).

Problem three is rates are dramatically higher now than 2003, as is insurance, rates, maintenance, petrol...

Supply is lower as the council have deliberately suppressed amount of land, up the development fees and slowed down the process. Supply also lower as council allowed leaky houses to be built.

Yes I think that a 3 bedroom house out of town at 7 times the median income ($50k'ish) is fair. If there was regulation that you needed 50% deposit then this would be the norm.

Aucklands growth is the result of government policy which promotes population growth and bugger the consequences. This policy plays into the hands of the powerfull realestate sector. They get away with it because progressives these days believe in open borders and disown the consequences.

***PROPERTY PANIC***

Says the herald this morning.

I wonder if there is any correlation between the fat advertising cash they get through the shiny property ads - and the hysterical property articles.

Cynical? SK?

Let's put it this way SK. If you saw the full front page of the NZ Herald, dedicated to showing folks piling into the sharemarket,or commodities, or whatever. What would you think?

Personally, I would think it's the time to get the hell out of there.

Mm the shoeshine boy theory. Or maybe the taxi driver theory - for today.

Shall we wait for the taxi driver to tell us about how he has just bought 5 apartments off the plans etc etc.

Thing is with the sharemarket - it doesnt have the populist appeal. And shares arent a necessity to live. NZX has hit highs recently but thats not going to make the front page - doesnt effect everyone in the same way.

Thought I would see what all the fuss about housten being so affordable was about so I did a bit of a goole search. Heres what first came up

http://www.homes.com/listing/170150546/11714_Quail_Creek_Dr_HOUSTON_TX_…

Not bad at all. Five bed rooms and 4 bathrroms for $180000 and their average wage is $60000, needs a coat of paint inside but still its a Remurea style mansion. In Auckland a mearly average house is $600000 grand and the average wage is about $50000!!!

In Perth the average wage is over $70,000 and the median house price is $80000 lower than Auckland (460000 vs 530000). No wonder the kids all leave. Hell if you take into account wages,cheaper public transport and gas @ $1.50 a litre even sydney leaves Auckland for dead (not to mention all the fun to be had there).

Tonight, a pumped de Roos tells his audience that he wants people to invest in property and write to him 12 months down the track and tell him they’ve “made one million or three million, or you’ve got 16 properties, or we’re taking six months off because our cash flow now exceeds our outflow!” He says, “I don’t know any other activity where the rewards are so huge. If you want to invest a million dollars in the sharemarket, you need a million dollars. If you want to invest a million in real estate, you only need $100,000.”

You can buy one property, get it revalued, use the equity to buy another property and then buy another and another. “And you do it all with OPM. Other people’s money. OPM. It’s like being high on drugs!” What’s more, the wonder of depreciation claims on the building and contents means “the government subsidises your investment! It’s delightful!”

http://www.listener.co.nz/uncategorized/house-of-the-rising-sum/

2003 - people were getting worried about the froth - still had 3 heady years to run.

Instructive to where we are currently in the cyle.

(Dolf ended up getting nailed on a sth island development I believe)

We ought to do the Houston Ponzi scheme thing

http://www.businessinsider.com/suburban-america-ponzi-scheme-case-study…

by the time people realise what happend we'll be retired on fully self suficient life style blocks.

Great link....in the meantime the ponzi developers here like Hugh are tying to get us to move to municpal bonds....making the "payback" even worse....joined of course by the libertarian loopies like no maths at all philbest....

regards

I thought I'd check out the house prices are the fault of planners interfering in the market for land meme being floated by the Koch Brothers and their associates and I discovered this research by Albert Saiz:

...................

I process satellite-generated data on terrain elevation and presence of water bodies

to precisely estimate the amount of developable land in US metro areas. The data shows

that residential development is effectively curtailed by the presence of steep-sloped

terrain. I also find that most areas in which housing supply is regarded as inelastic are

severely land-constrained by their geography. Econometrically, supply elasticities can

be well-characterized as functions of both physical and regulatory constraints, which

in turn are endogenous to prices and demographic growth. Geography is a key factor

in the contemporaneous urban development of the United States.

Empirically, most areas that are widely regarded as supply-inelastic were found, in fact,

to be severely land-constrained by their geography. Deploying a new comprehensive survey

on residential land use regulations, I found that highly-regulated areas tend to also be geo-

graphically constrained. More generally, I found recent housing price and population growth

to be predictive of more restrictive residential land regulations. The results point to the

endogeneity of land use controls with respect to the housing market equilibrium.

Hence I next estimated a model where regulations are both causes and consequences

of housing supply inelasticity. Housing demand, construction, and regulations are all de-

termined endogenously. Housing supply elasticities were found to be well-characterized as

functions of both physical and regulatory land constraints, which in turn are endogenous to

prices and past growth.

Geography was shown to be one of the most important determinants of housing supply

inelasticity: directly, via reductions in the amount of land availability, and indirectly, via

increased land values and higher incentives for anti-growth regulations. The results in the

paper demonstrate that geography is a key factor in the contemporaneous urban development

of the United States, and help us understand why robust national demographic growth and

increased urbanization has translated mostly into higher housing prices in San Diego, New

York, Boston, and LA, but into rapidly growing populations in Atlanta, Phoenix, Houston,

and Charlotte.

The Geographic Determinants of Housing Supply

Albert Saiz∗

(Forthcoming: Quarterly Journal of Economics)

January 5, 2010

Comment on the Saiz paper (Geographic Determinants of Housing Supply) from the Federal Reserve of Atlanta:

“The Saiz paper is forthcoming in a top economics journal, and its results are already being used by housing economists. We draw from it ourselves in a paper that investigates why so many economists missed the housing bubble.4 But we caution that one should not push the Saiz results too far. The Saiz paper concerns the slopes of housing supply curves in different cities. As a result, it says nothing about shifts in housing demand that might have occurred during the housing boom. For example, the Saiz results would predict that, during the housing boom, prices in high-supply-elasticity cities like Wichita would rise less than prices in low-elasticity cities like Boston. Sure enough, this is what we find in the data. However, this finding does not prove that the boom was caused by some uniform, nationwide increase in housing demand (arising, for example, from easier subprime lending, or from lower interest rates). It is true we would expect a uniform demand increase to have a small effect on Wichita’s prices and a big effect on Boston’s prices. But because Wichita has a flat supply curve, its house prices will be stable no matter what happens to demand there. To determine whether Wichita and Boston saw similar increases in demand, one would have to look not only at prices but also at quantities (that is, new construction). Researchers should therefore be careful when using the Saiz results to study the housing boom—a point we hope to revisit in future posts.

http://realestateresearch.frbatlanta.org/rer/2010/06/explaining-local-supply-elasticities-quantifying-the-importance-of-space-limitations-in-housing-pric.html

This though does suggest regulation has some impact on prices. Wellington v auckland might make good study cases....Assuming the regualtions are the same then you would expect higher prices in Wellington......lots to study.......moot anyway...

regards

See Westpac chart below showing house prices not necessarily linked to population growth, challenging the suggestion that migration to Auckland and supply shortages are the main reason for house price rises there.

very clever

The Savings Working Group two weeks ago released their report on New Zealand’s

savings problem warning that we stand on the edge of an abyss. That terminology is

somewhat sensationalist and hopefully hasn’t panicked anyone into leaving the country in

case we go the same way as Greece and Ireland. Actually we already did that back in the

1980s when the economy had to be deregulated to face a changed world and the

government had to get its finances back in order after years of ballooning deficits.

One of the claims made in the Savings report is that migrants push up house prices and

therefore maybe if some controls were placed on immigration prices would not be so high

and we Kiwis would save through bank accounts and such like rather than buying each

other’s houses. They report cites a particular study showing that about a 1% of

population boost in immigration lifts house prices about 10%.

However there is another study of migration and housing which finds that looked at from

a local as opposed to national level one cannot find evidence of more than about a 0.2%

- 0.5% lift in house prices. This study also suggests that maybe it is not the migrants

(foreigners) affecting house prices if such an effect exists, but returning Kiwis – which is

what we will examine here.

ofcourse the Savings working group were working for the people of NZ whereas.........

One situation which would be almost impossible to identify is the pressures from hot money (China, Russia, India) the bolt-hole effect (China, maybe Russia) economic refugee (maybe Middle East).

I would suggest there is not as much of a shortage of housing in Auckland as most renters and owner occupiers are interchangeable. Further the fact that most renters want to buy has been clobbered by the higher money available from those above plus local investors with extra euity in their house plus some spare cash.

The resulting higher prices than economically justified has a further rachetting effect and if that becomes a reversal the more soft the investment the quicker the slide.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.