Behind the interest rates we pay are many forces at work.

Benchmark policy rates are an important influence.

These impact wholesale money markets which respond relatively efficiently (over the medium term at least) to the major global economic forces at work.

But corporate borrowers in these markets must compete with each other, and sovereign borrowers as well.

Because bonds are issued over very long terms, it is difficult for any investor in these bonds to be certain they will get their capital back at the end. Bonds may be rated by credit rating agencies, but these assessments are expectations based on a borrowers track record. And everyone knows that the forward looking assessments can change dramatically as time passes.

The solution is that investors buy 'insurance' against the prospect of default in the long run. And borrowers pay that cost as an interest rate premium over 'risk free'.

This 'insurance' takes place with a credit default swap contract.

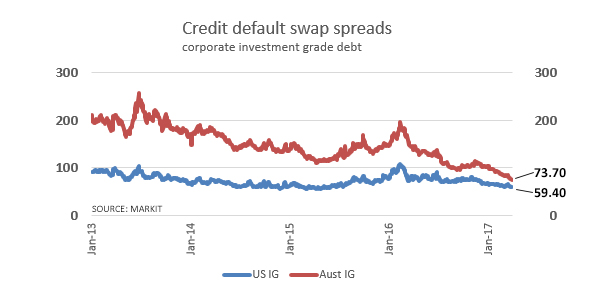

The price of a credit default swap is referred to as its “spread,” and is denominated in basis points (bps), or one-hundredths of a percentage point. For example, if the ANZ bank bond has a spread of 73.7 bps, or 0.735% that means that, to insure $100 of ANZ debt, you have to pay $0.737 per year. For $1 mln of debt the cost would be $737 per year. (Usually you see spreads quoted in USD, but that is more because the usual source, Markit, is publishing for an American audience.)

In fact, we don't actually know the specific cost for ANZ or any bank. That information is available to professional investors who subscribe to the Markit service. So all we know is the overall index for Australasian debt, which includes more than banks.

The point of this article is to point out that CDS swap spreads for Australasian investment grade bonds are falling, and are falling quite quickly.

They are currently at 73.7 bps, the lowest level they have been in over nine years (2006). We monitor this daily here.

And not only are they falling quickly, they are falling faster than equivalent American investment grade bonds.

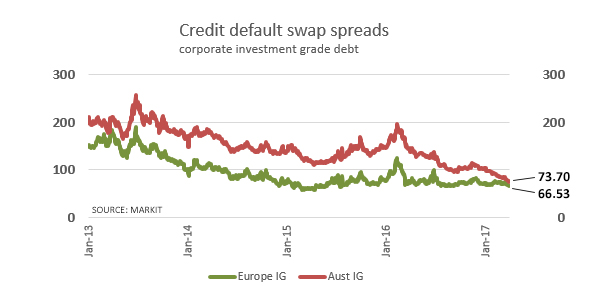

In fact, they are closing in on the level of spreads European issuers need to pay.

This is unusual. It has been a very long time since Australasian investment grade bonds have seen this low a level of credit risk assigned by the wholesale money markets.

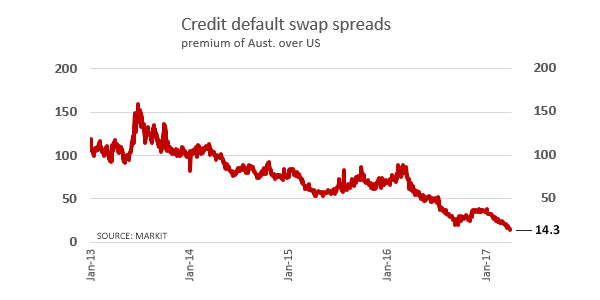

The premium over US equivalents is now just 14 bps. That is a major fall from just a year ago, and a massive fall from four years ago.

Investors love our investment grade bonds.

Part of this is local. We don't issue a lot, and the Aussies issue even less relative to the size of their economy.

Ever growing demand from fund managers who have conservative mandates (like KiwiSaver funds) bolsters local demand. Retail investors find it very hard to buy the quantity of bonds they would like. The cover rates for both Government and LGFA issues reinforce this point.

There is irony here. In a world awash in corporate debt, there are still not enough investment grade corporate bonds to meet investor demand. It is an irony that points out just how large risk-averse investor savings are. Regulation changes in the US and EU, plus growing risk aversion from baby-boomer retirement funds will only build that demand.

We do not know what our banks pay for this premium. The assumption is that New Zealand banks need to pay more than their Aussie parents.

But that may not in fact be the case.

And that is because New Zealand sovereign bond CDS spreads are currently 4 bps lower than for the Australian Federal government issues, and we have had that pricing advantage for quite a while now.

When a banker says the cost of their wholesale debt is rising, it may well be. We need to take their word for it as this is a very opaque environment. But with narrowing CDS spreads we can be sure that the cost of 'insurance' imposed by investors is almost as low as it ever has been.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.