By David Chaston

Depending on your tolerance for risk, a growth-balanced fund might be a worthwhile alternative to your default KiwiSaver.

The best Balanced KiwiSaver fund has returned +12% more than the best performing Default fund. That is a gain of more than $4,000 since inception - after all taxes and after all fees. In the past three years, that advantage has been more than +40% more. It demands your consideration.

This is an assessment of how Balanced KiwiSaver funds are performing and their track record since inception. (It is not an assessment of how they will do in the future.)

Balanced funds involve taking more risk than Conservative, Default, or Moderate funds.

The 'balance' referred to is a balance of growth allocations.

For Balanced or Balanced-Growth type funds there is more volatility in returns as they traditionally have higher exposures to equities or property than the more conservative funds. Sometimes, some types of bond funds deserve a higher risk assessment too. Although the losses in capital may be experienced more frequently, over the long run your capital value should grow more quickly than conservative funds.

In assigning our risk categories to the full range of KiwiSaver funds, we took these things into consideration:

- the target asset allocation (that is, where the manager plans to invest the funds),

- the current asset allocation,

- the exposure to smaller or mid sized companies,

- liquidity of the underlying investments,

- exposures to derivatives or alternative assets and

- potential for wide variability in monthly and annual returns.

We are not using the fund manager's label or naming of the fund type in this 'Balanced' category; we are using our own independent assessment.

| Balanced Funds |

Cumulative

contributions

(EE, ER, Govt)

|

+ Cum net gains

after all tax, fees

|

Effective

cum return

|

= Ending value

in your account

|

Effective

last 3 yr

return % p.a.

|

|||

| since April 2008 | X | Y | Z | |||||

| to June 2017 |

$

|

% p.a.

|

$

|

|||||

| Aon Russell LifePoints Moderate | B | B | M | 28,260 | 10,882 | 7.0 | 39,141 | 6.7 |

| AMP Nikko AM Balanced | B | G | G | 28,260 | 10,691 | 6.9 | 38,951 | 7.4 |

| Aon Nikko AM Balanced | B | G | G | 28,260 | 10,548 | 6.8 | 38,808 | 7.2 |

| ANZ OneAnswer Balanced | B | B | B | 28,260 | 10,503 | 6.8 | 38,762 | 6.2 |

| ANZ Balanced | B | B | B | 28,260 | 10,359 | 6.7 | 38,618 | 6.1 |

| ANZ Default Balanced | B | B | B | 28,260 | 9,674 | 6.4 | 37,933 | 6.2 |

| AMP Fisher Funds Two Balanced | B | B | B | 28,260 | 9,400 | 6.2 | 37,660 | 6.2 |

| Fisher Funds Two Balanced | B | B | B | 28,260 | 9,239 | 6.1 | 37,499 | 6.0 |

| ASB Moderate | B | B | M | 28,260 | 8,177 | 5.5 | 36,436 | 5.6 |

| Booster Balanced | B | B | B | 28,260 | 7,671 | 5.2 | 35,931 | 5.6 |

| AMP Moderate Balanced | B | B | B | 28,260 | 6,932 | 4.8 | 35,191 | 4.5 |

| and some funds who haven't been going for the full period ... | ||||||||

| Milford Balanced | B | B | B | 22,945 | 8,898 | 8.9 | 31,844 | 7.3 |

| BNZ Balanced | B | B | B | 15,702 | 2,631 | 6.7 | 18,332 | 6.5 |

| Booster KiwiSaver SRI Balanced | B | B | B | 10,958 | 876 | 4.8 | 11,834 | ... |

| --------------- | ||||||||

| Column X is interest.co.nz definition, column Y is Sorted's definition, column Z is Morningstar's definition | ||||||||

| B = Balanced, G = Growth, M = Moderate | ||||||||

This better performance is essentially down to the skill of the manager to select specific investments that outperform the benchmarks established for this category. Clearly some managers do better than others over the long run. And it is not only the specific investments, it is how they structure their overall allocations.

Here is a review of the current allocation structures.

| Balanced Funds |

------ how allocated, approx. ------

|

|||||

| at June 2017 |

Cash

|

NZ fixed

income |

Intl fixed

income |

Equities | Property | Other |

| % | % | % | % | % | % | |

| Aon Russell LifePoints Moderate | 12 | 48 | 40 | |||

| AMP Nikko AM Balanced | 14 | 14 | 48 | 5 | 20 | |

| Aon Nikko AM Balanced | 14 | 14 | 48 | 5 | 20 | |

| ANZ OneAnswer Balanced | 14 | 12 | 25 | 42 | 8 | |

| ANZ Balanced | 14 | 11 | 25 | 42 | 8 | |

| ANZ Default Balanced | 14 | 11 | 25 | 42 | 8 | |

| AMP Fisher Funds Two Balanced | 18 | 16 | 23 | 44 | 12 | |

| Fisher Funds Two Balanced | 14 | 25 | 11 | 42 | 10 | |

| ASB Moderate | 11 | 30 | 22 | 32 | 4 | |

| Booster Balanced | 9 | 18 | 19 | 48 | 5 | |

| AMP Moderate Balanced | 21 | 18 | 15 | 45 | 3 | 1 |

| Milford Balanced | 16 | 6 | 24 | 43 | 10 | 1 |

| BNZ Balanced | 5 | 11 | 34 | 40 | ||

| Booster KiwiSaver SRI Balanced | 10 | 18 | 20 | 48 | 5 | |

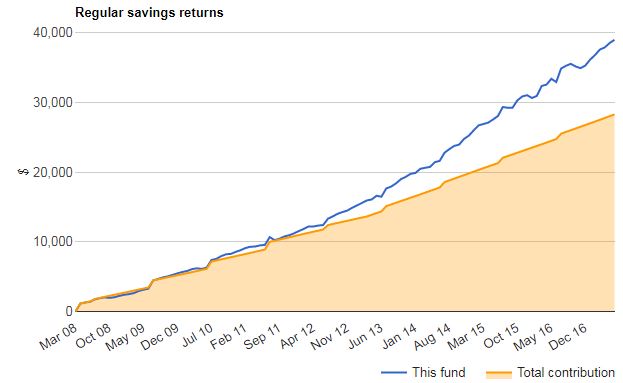

This is how a good-performing balanced KiwiSaver fund has gone ...

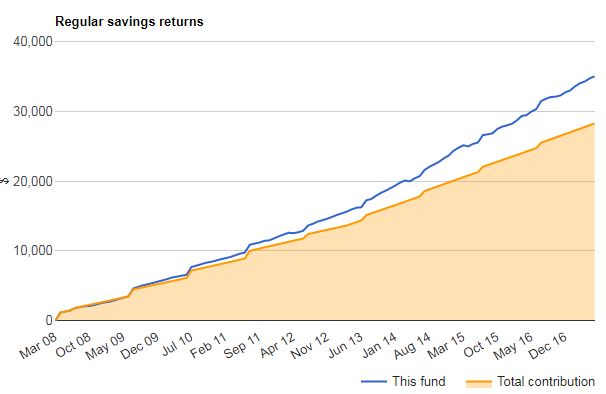

... and that compares with a good-performing default KiwiSaver fund, like this:

Comparing these two tracks, you can clearly see the Balanced fund struggled in the wake of the GFC, when the Default fund was able to maintain reasonable returns. But when the economic situation turned brighter, the Balanced fund has greatly outperformed the steady Default fund. This shows the benefit of accepting more risk. But if the economic situation turns, so will these charts, (although the Balanced ones would start that cycle in a healthy situation).

Some changes and updates

We have reviewed and updated some of the processes in our regular savings analysis of all KiwiSaver funds on www.interest.co.nz and as a result the numbers may differ from previous releases. The key changes are a downward revision to the monthly contributions a person on an average income and 28 years old in 2008 would have made, and an enhancement to the way in which tax liability for the funds was calculated. These changes affect all funds analysed equally, so there is no material change to the relative positioning.

For explanations about how we calculate our 'regular savings returns' and how we classify funds, see here and here.

There are wide variances in returns since April 2008, and even in the past three years, and these should cause investors to review their KiwiSaver accounts, especially if their funds are in the bottom third of the table.

The right fund type for you will depend on your tolerance for risk and importantly on your life stage. You should move only with appropriate advice and for a substantial reason.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.