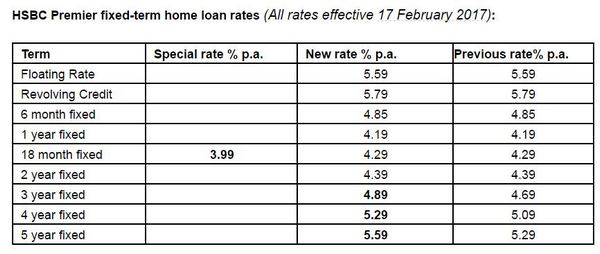

HSBC is offering a 3.99% per annum "special" interest rate on 18-month home loans.

The only residential mortgage rate currently under 4% from a New Zealand bank, is available from today (Friday). It's on offer to new HSBC "premier" customers and existing HSBC premier customers who borrow at least an additional $100,000.

To qualify for the offer, borrowers must provide an owner-occupied property as part of the security. The bank's minimum equity and deposit criteria apply.

An HSBC premier customer must have either a minimum combined home loan of $500,000 or $100,000 in savings and investments with HSBC.

"With market uncertainty having increased in recent times, we are pleased to be able to provide our owner-occupier customers with certainty over the short-to-medium term with this 3.99% p.a. 18 month-fixed mortgage offer," Glen Tonks, HSBC's head of retail banking and wealth management, said.

The 18-month special is available for a limited time, HSBC says.

See all banks' advertised, or carded, home loan interest rates here.

A snapshot from the key retail banks is:

| below 80% LVR | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| % | % | % | % | % | % | |

| 4.39 | 5.05 | 4.79 | 5.49 | 5.70 | 5.85 | |

| 4.59 | 4.75 | 4.79 | 5.09 | 5.49 | 5.69 | |

| 4.59 | 5.05 | 4.79 | 5.09 | 5.89 | 6.09 | |

| 4.45 | 4.79 | 5.25 | 5.65 | 5.85 | ||

| 4.59 | 5.05 | 4.79 | 5.09 | 5.69 | 5.49 | |

| 4.55 | 4.70 | 4.85 | 5.25 | 5.55 | 5.75 | |

| 4.19 | 3.99 |

4.39 | 4.89 |

5.29 |

5.59 |

|

|

4.45 | 4.75 | 4.75 | 5.09 | 5.45 | 5.69 |

| 4.45 | 4.75 | 4.75 | 5.05 | 5.45 | 5.50 |

In addition to the above table, BNZ has a fixed seven year rate which is 6.15%.

TSB Bank has a ten year fixed rate of 5.75%.

45 Comments

I am cynical about this, where are these funds being sourced by HSBC?

Its odd that they can offer mortgages at virtually ( almost) lower than we can get as depositors ?

Perhaps what is being offered by the other local/AUS banks is a shitty deal and they are all more or less in cahoots keeping things on a similar playing field so they all make a profit. Just take a look at mortgage rates that HSBC offer in the UK, far far lower than NZ.

But hey, why not be cynical.

I don't think there's any thing to be cynical about it's just logical considering that HSBC is a Chinese bank and what's happening in the Asian market at the moment with China trying to protect the renminbi that has fallen 5.8 per cent in late 2016, one of the worst years on record.

China has sold dollars from its foreign exchange reserves to try to curb downward pressure on the currency.

Well Its not Chinese in the strict sense , Its primary listing is in London , but the fact is its huge in Hong Kong and China

I think you'll find that they are a global bank: https://www.youtube.com/watch?v=JdSvBTbpnRo

Good enough reason for moving banks for me in April.

Thumbs up to HSBC.

Oh do u have 100 grand in savings or a loan over 500 grand?

April? Won't be here that long

You have to negotiate with them most banks can be flexible.

Just proves that the mainstream Oz banks are ripping us off using the excuse of increased cost of funds from offshore, when those funds can be obtained at less than 2%. At the same time one of the Oz banks announces more than half a billion profit for 6 months for their NZ operation. These banks are seriously taking the piss and Kiwis shouldn't stand for it. Let's hope this sets of a round of discounting - the Oz banks can easily afford to offer 4% fixed for 18 months. If not then move your business to HSBC!

If you have $100000 in your savings account. Sure. But then I don't think youd have a mortgage

Maybe they are just sticking it to their depositors - I see their 2yr TD rate is just 3%, versus 4% for other banks. The differential between TDs and HLs seems the same as main banks, so it shows me the other banks aren't grabbing margin.

Glad our loan is not so huge as to be eligible for this rate.

OR you have savings of 100k with HSBC to qualify. which would be a much better place to be in.

That depends on what your loan is used for, a) private consumption = bad, or b) wealth creation like a business that produces goods and employs people = good

YEEHAA ! Let's vote with our wallets, let's change banks to HSBC

Just gave them a quick call and the young lady who picked up said the offer would run through to at least the end of April. No rush I guess.

Thanks Squishy

I would get that in writing if I was you. Surprised they would hedge for this for over 10 weeks - that's a lot of time for wholesale rates to move!!

Still, pretty small mortgage book .... http://www.rbnz.govt.nz/statistics/g2 yet always sharper rates, so they must be worried!

On other hand HSBC 2 year 4.39% is also a good rate

Really?!

Surprised as I haven't heard anything like that for three years.

Which bank please?

It is a good rate. I note he didn't say he GOT that rate, but that it's a good one.

Perhaps its from the Bank of Trump which advertises "alternative rates"?

Depends when they negotiated and settled... We were offered 3 years at 4.39% plus cash in late November by ASB.

Sadly, we couldn't document at the time as settlement was last week and they could only document it 60 days out (early-mid Dec), by the time we could document, the best rate we could lock in was 4.65% plus cash...

Which bank was 4.39%, 3yrs please?

Sorry - typo - 2 yr rate is 4.39% at HSBC

Depends on what you negotiate ;)

Great job HSBC.

Great for owner occupiers....

Yes thanks HSBC I'm already considering switch to you. Really wish we could get their UK rates of 1.24% for a two year fixed, oh well wishful thinking. 3.99% is very good for New Zealand. :)

Imagine what a 1.24% interest rate would do to house values in NZ

Cause Boomers to credit themselves with even greater investment nous? (...All for being born at the right time.)

I'm coming for you too HSBC!

Read this big Blue.. https://www.nbr.co.nz/article/nz-banks-likely-scale-bank-lending-growth…

If its behind the pay wall.. basically refers to the fact that bank margins are shrinking off already globally low levels. So could they take a slightly lower margin.. probably. Is it a rort.? No. HSBC is putting this out at a teaser rate.. they would never do it if they were as big as ANZ/ASB etc

Bank margins shrinking yet ASB just announced a record 6 month profit of $525m

http://www.radionz.co.nz/news/business/324552/asb-bank-posts-$525m-prof…

So they can drop their interest rates no problem at all

Yip.. their margins also shrank (nearly 10%).. it was only because they lent a bucketload to mortgage borrowers (which i dont agree with.. the growth that is). But a business that is growing its profits through selling more of a profit, at a lower margin is not a rort. If anything.. it illustrates that despite massive demand for its product, there is competition their keeping margins under pressure.

The profit figure is very misleading.. that profit and the growth recquires a lot of capital (which no one ever talks about) and there is a cost of that. In this case, through being very efficient they have a good return on that capital.

3.99% p.a. lending sounds swell, but first a few caveat emptors...

1. HSBC Auckland branch has some of the strangest bank service I have ever encountered. Few frontline staff seem to be acquainted with the norms of bank customer service and there is a revolving door of staff meaning that you often wind up dealing with staff in training. I find that most staff seem unfamiliar with even their own standard bank policies and inter-office computer systems. Comparably, FWIW, UK HSBC staff are as helpful and professional as any of the NZ Big Four (yes, yes, truly never has such an insult been uttered). Therefore, it seems to be an Auckland branch issue. This is who you will be dealing with.

2. HSBC Auckland is a branch of HSBC Hong Kong. This becomes relevant should you deposit sums of money with HSBC. In the event (admittedly unlikely, but possible) of a HK regional or global HSBC bank collapse, Auckland deposits are structurally part of the Hong Kong business. Hong Kong banking regulations require a certain amount of capital returned to Hong Kong branch depositors before distributions to non-HK branches may proceed. This means that there is a risk that Auckland depositors would not see their capital returned in the event of collapse. See disclosure statement, HSBC company structure and HK deposit protection regulations for more information. It's an eye-opener and not publicised in NZ at all, beyond the disclosure statement (quelle surprise).

3. Large overseas banks have a history of cutting and running from NZ when the easy money is made. HSBC has reduced its NZ operations over time, more recently refining its customer base to those with more capital and who require greater lending. Late last year, letters were sent to customers who no longer qualified, informing them that they needed to make alternative banking arrangements. Should HSBC elect to leave the NZ business (or further "refine"), a borrower might find themself needing to refinance with another bank in rather a hurry. That could prove difficult under present banking conditions.

Still, fortune favours the brave. YMMV.

Customer service isn't well paid in banking, people with any degree of skill or competence will likely move on rapidly to better paid roles. It's strange really, banks are reliant on service for growth but extremly reluctant to actually pay people or train them properly to do it, yet throw money at marketing and the latest fintech startup fads or overseas "synergy." Weird business.

Unfortunately that is true of many supposedly customer focused organisations - I work for one and the level of training given to new staff is appalling. When I started I was given 6 weeks training - and no that did not prepare me fully for the job - I consider myself still learning - years later. New staff and now buddied up with another staff member to be shown the ropes....

I can appreciate your concerns OPR, Though as far as I'm aware isn't it true that if any of the other banks go down such as the Ozzy or Kiwi banks your savings deposits won't be covered?

The only Government that does protect it's citizens saving that I know is the UK were they will protect saving up to 70,000 pounds per deposit account.

The issue is not deposit protection. The issue is that, in event of collapse, HK depositors are paid out before non-HK depositors. HKers are preferentially protected by HK banking regulation. This means that, if there was a shortfall in capital to pay out unsecured depositors, HKers would get paid out first (up to a maximum which I can't remember off the top of my head), then the remaining cash (if applicable) divied up amongst all unsecured creditors - including HKers.

To put it bluntly, Kiwis would be at the back of the queue.

You mentioned deposit protection. Interestingly enough, NZ is one of the few Western countries without deposit protection. US, Canada, Australia, EU etc. Deposit protection is very, very common. The UK, for example, offers 85k sterling per person per firm - that's 170k for a couple with a joint account. Pretty compelling stuff. NZ is relatively alone in the advanced world in lacking such a scheme.

Us Kiwis are, indeed, brave. Perhaps fortune will favour us?

Yes your right it is shocking that NZ has no protection for it's citizens in the financial markets, though the UK figure you mention of 85k sterling was dropped down to 70k a year ago, still better than the zero protection that we get!

It was 75k sterling last year, but last month the limit was changed back to 85k sterling per person per firm.

https://www.fscs.org.uk/what-we-cover/compensation-limits/deposit-limit…

A truly delightful Christmas present to UK depositors. Aside from that unsightly inverted pound problem, of course.

The UK's limit is the same as the rest of the EU - approx 100,000 euros. As the UK still has the pound, it re-balances every now and then to be roughly equivalent to the rest of the Union. So the raising limit is due to the Brexit vote-induced currency fall, and who knows what will happen to the scheme in the UK once Brexit actually happens.

HSBC less sensitive to long term swaps rates than Aus banks as Aus banks have to borrow from third parties offshore. As a truly global bank, HSBC can source funds from their own network and not have to fund third party margins in their rates. Makes sense that they'd take advantage at this time.

You can negotiate a decent cash allowance along with a low interest rate of 3.99% with HSBC. Their online banking may not be the best (no app in NZ either) like ANZ or ASB but you can do instant bank transfers between HSBC accounts across multiple countries for zero FX transaction/banking fees! Very beneficial if you are an overseas based Kiwi.

HSBC only the rates are good .My experience if you want to fix mortgage with them start 6 months early they work in snail pace.Relationship Manager wont be able get back to you on time if you have anything critical .Customer service is very poor .As long you have the patience to wait and its not time critical you will be alright .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.