By Terry Baucher*

The Government’s response to Auckland’s housing [insert word of choice here] has focussed on the supply side of the issue. Ironically, many property owners may find themselves with a tax headache thanks to one of these key supply initiatives, the Proposed Auckland Unitary Plan, triggering a tax measure introduced to deal with another housing boom forty odd years ago.

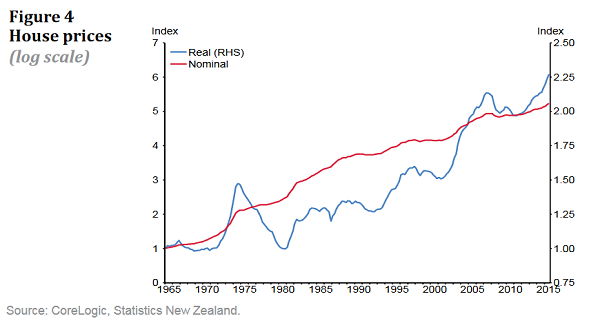

Housing booms are a fairly regular occurrence in New Zealand. The Reserve Bank of New Zealand’s January 2016 Bulletin identified “six distinct periods of high real price inflation” since 1965.

According to the RBNZ, one of the biggest of these booms was that between 1972 and 1974. During this period real house prices grew 22% on average per year with annual price inflation peaking at 31% (the highest in the past 50 years).

Norman Kirk’s Labour Government’s response was to initiate a huge house-building programme and to deal with speculation through a series of tax measures.

The Property Speculation Tax Act 1973 applied to all “dispositions” of land on or after 15th June 1973. Under the act any profit was liable to Property Speculation Tax when:

- The period between the date of acquisition and disposition was two years or less; and

- No exemption was available.

If that sounds vaguely familiar, many features of the Bright-line test introduced from 1st October 2015 are almost identical.

The Property Speculation Tax was a specific tax separate from income tax. Its minimum rate was 60% with a maximum rate of 90%(!), applicable where the period between the date of acquisition and disposition was six months or less.

The Property Speculation Tax didn’t last long and was repealed in 1979 by Sir Robert Muldoon’s National government. It was considered irrelevant following the introduction of specific income tax legislation taxing property transactions.

This legislation was enacted in August 1973 as section 88AA of the Land and Income Tax Act 1954. It remains in force as sections CB 6 - CB 23 of the Income Tax Act 2007.

The legislation taxes a series of property disposals, most notably any disposals where the land was acquired for the purpose or intention of selling or otherwise disposing of it. It also contains the “associated persons” or “tainting” rules, which tax certain disposals made within ten years where at the time the land was acquired the vendor was associated with a developer or builder.

In 1975 the Third Labour Government further expanded the property taxation rules by adding what is now section CB 14 of the Income Tax Act 2007. A rarely applied and consequently little known provision, it has the potential to become a huge headache for anyone selling land potentially affected by the Proposed Auckland Unitary Plan.

Under section CB 14, where a person sells land within 10 years of acquisition, any gains from the sale that are not taxed under other provisions (such as the Bright-line test), will be taxable if at least 20% of the gain results from one or more factors that occurred AFTER the land was acquired. Those factors include a change, or a likelihood of a change in the operative district plan.

Section CB 14 therefore almost certainly applies to properties rezoned for higher density or as Special Housing Areas.

There is a further nasty twist in the provision in that even if you reside in the property, its sale is not exempt unless the purchaser acquires it for residential purposes. So, if you were thinking of realising a tax free gain by selling your Special Housing Area zoned property to a developer, think again.

If section CB 14 applies, a deduction of 10% of the gain is allowed for each year of ownership. So for example, if a property is sold after five years of ownership, 50% of any gain would be a deductible expense.

Even if your property isn’t affected by the Proposed Auckland Unitary Plan, you should be aware that other factors which could trigger section CB 14 include the grant, or the likelihood of a grant, of a resource consent, or the removal of a covenant, designation or other restriction. Section CB 14 is so wide in its reach anyone considering selling land within 10 years of acquiring it should check with their advisor.

A likely response to section CB 14 is to delay disposals of land until the 10-year period has passed. The Proposed Auckland Unitary Plan intended to free up land for development may therefore unintentionally encourage land banking.

Although the Government has downplayed the role of tax as a means of dealing with house price inflation, the Bright-line test shows it’s not adverse to copying tax initiatives used to tackle another housing boom. Meanwhile provisions such as section CB 14 and the work of Inland Revenue’s Property Compliance Programme will catch many seeking to cash in on the housing market.

In the end it wasn’t tax measures or building that ended the early Seventies boom; it was an unexpected event in the shape of the Yom Kippur War in October 1973. That prompted the First Oil Shock which triggered a worldwide recession and a huge fall in house prices in real terms.

Let’s hope the modern-day parallels with the 1970s don’t include a similar unpleasant surprise. A Trump Presidency anyone?

*Terry Baucher is an Auckland-based tax specialist and head of Baucher Consulting. You can contact him here »

5 Comments

Just thought i would say thanks for the info. Its very interesting.

Indeed the world will be a far safer place under a Trump presidency.He is not interested in destabilising foreign countries.

I can't imagine the Americans changing after 50 yrs of foreign policy that has actively and covertly assassinated, attacked, propagandized and destabilized foreign countries. Why will Trump be any different?

Will he even be in control?

Interesting. In planning terms we call it 'betterment'.

Second last paragraph

"The first oil shock triggered a world wide recession and a huge fall in house prices"

That might be true on a global and macro basis - but on the specific micro basis it was a little different (in Auckland anyway)

I vividly recall the 1973 Oil Shock and what happened to Auckland property prices - prior to 1973 many of the wealthier had begun to migrate outward to the rural lifestyle blocks beyond Clevedon and Ardmore and the Hunua's, following the dream - particularly kiwifruit plantations

When the oil shock happened and carless days started and petrol prices increased, the nuveau rural lifestylers started dumping their rural blocks (where prices collapsed) and moving back into town where prices in areas like Ponsonby, Herne Bay, Freemans Bay, skyrocketed up not down

Aaaah - human behaviour

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.