By Kymberly Martin

NZ swap and bond yields declined by 3-4 bps on Friday following the Bank of England inspired moves the previous night.

On Friday night US yields closed 7-9 bps higher after a strong payrolls number.

There was little on the domestic calendar on Friday so NZ yields took their cue from offshore. Most downward pressure on yields was felt at the long-end of the curve. Heading into Thursday’s RBNZ meeting the market still fully prices a 25 bps rate cut. A trough in the OCR of around 1.62% is priced within the year ahead. This is a fair representation of current risks.

The RBA released its Monetary Policy Statement on Friday following its rate cut decision earlier in the week. The decision reflected a belief that while the economic outlook remained positive, there was room for even stronger growth, given inflation was projected to be below 2% over most of the forecast period. The Bank also appeared more relaxed about house price risks. Our NAB colleagues believe while inflation is projected to remain low the Bank will retain the scope to ease monetary policy further, should it feel growth is not evolving as forecast.

While there was not a significant market response to the release of the Minutes, the market still prices around a 70% chance of a further RBA cuts within the year ahead.

Friday night was all about the US labour market report. Payrolls were strong across the board for the month of July, with upward revisions made to June. Equities rose, led by financials and cyclical growth sectors, while rate-sensitive sectors declined.

US bond yields gapped higher across the curve. US 2-year yields closed up 7 bps, at 0.72%. 10-year yields closed up 9 bps, at 1.59%. The large move of the 10-year part of the curve may reflect speculative positioning ahead of the data release (long positions were at their highest level since end-2012 i.e. the market was positioned in anticipation of lower yields). The market is now pricing 6 bps of Fed hikes by September (or 24% chance) and 13 bps of hikes by December.

The move in US yields was also reflected in a 3-4 bps rise in German and UK 10-year yields and a decline in Australian bond futures. We anticipate higher yields and some steepening of NZ curves today.

Daily swap rates

Select chart tabs

Kymberly Martin is on the BNZ Research team. All its research is available here.

4 Comments

The market is now pricing 6 bps of Fed hikes by September (or 24% chance) and 13 bps of hikes by December.

The forecast for future US economic growth,real or otherwise, is absent in the charts that matter.

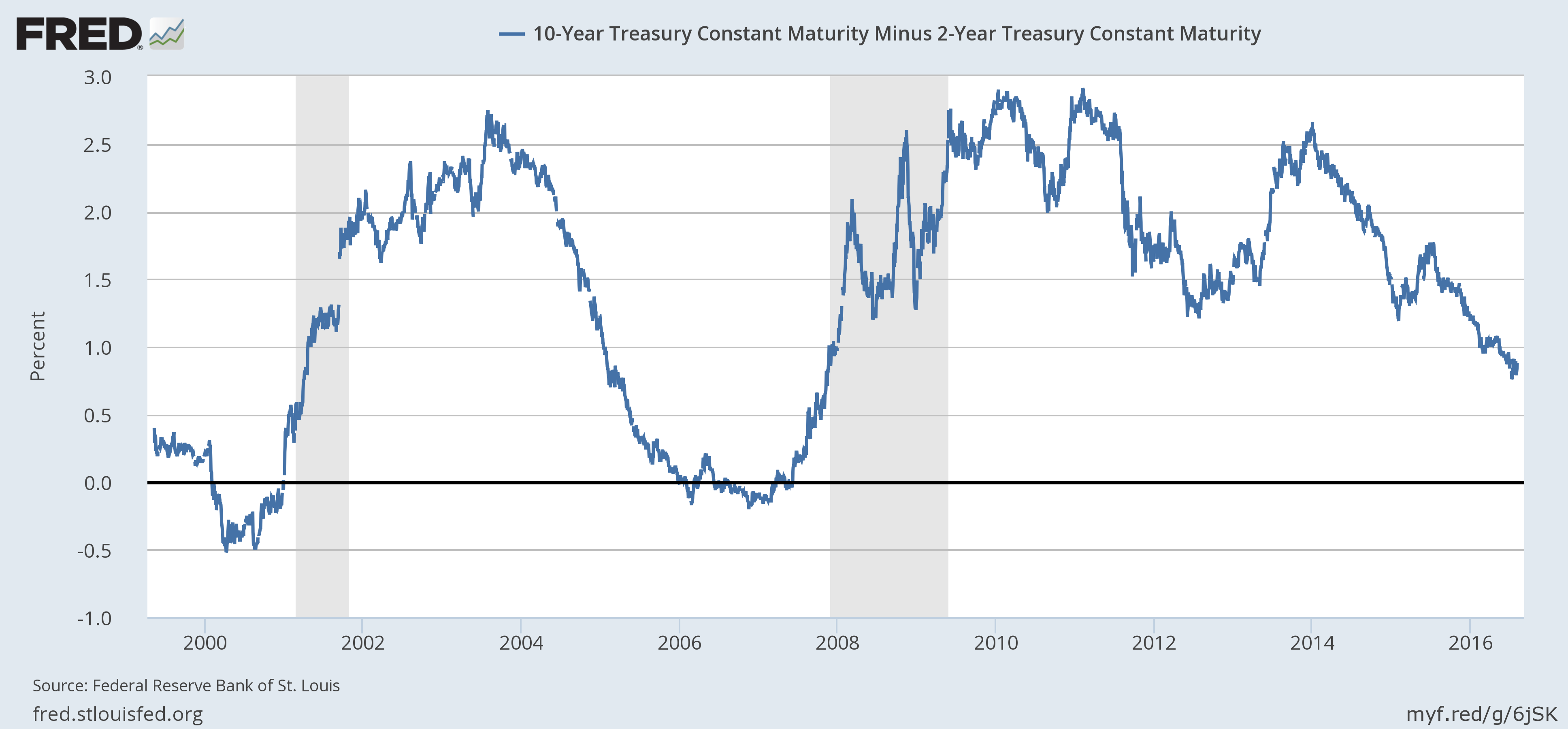

10-year treasury constant maturity minus 2-year treasury constant maturity

{kind=link}

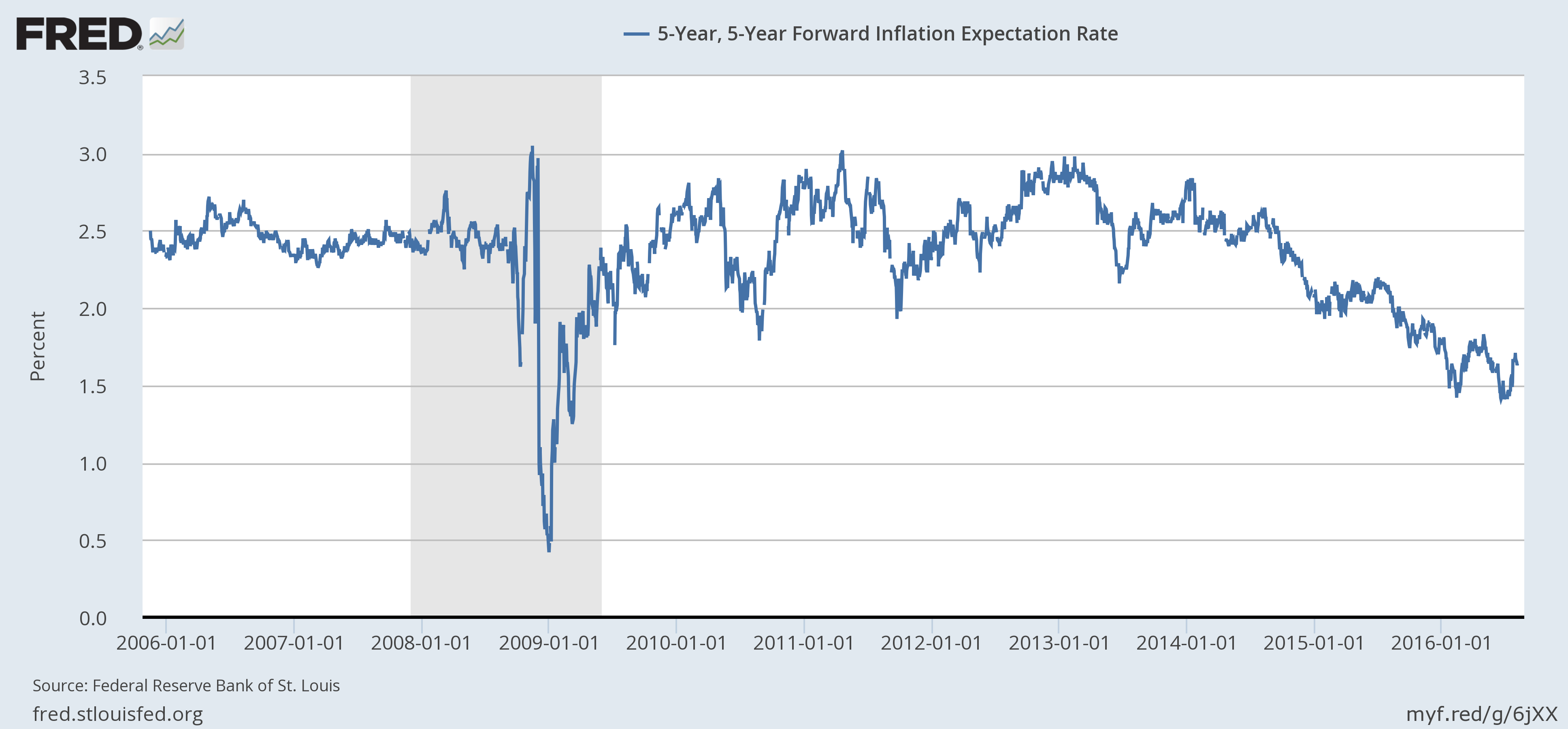

5-year, 5-year forward inflation expectation rate

{kind=link}

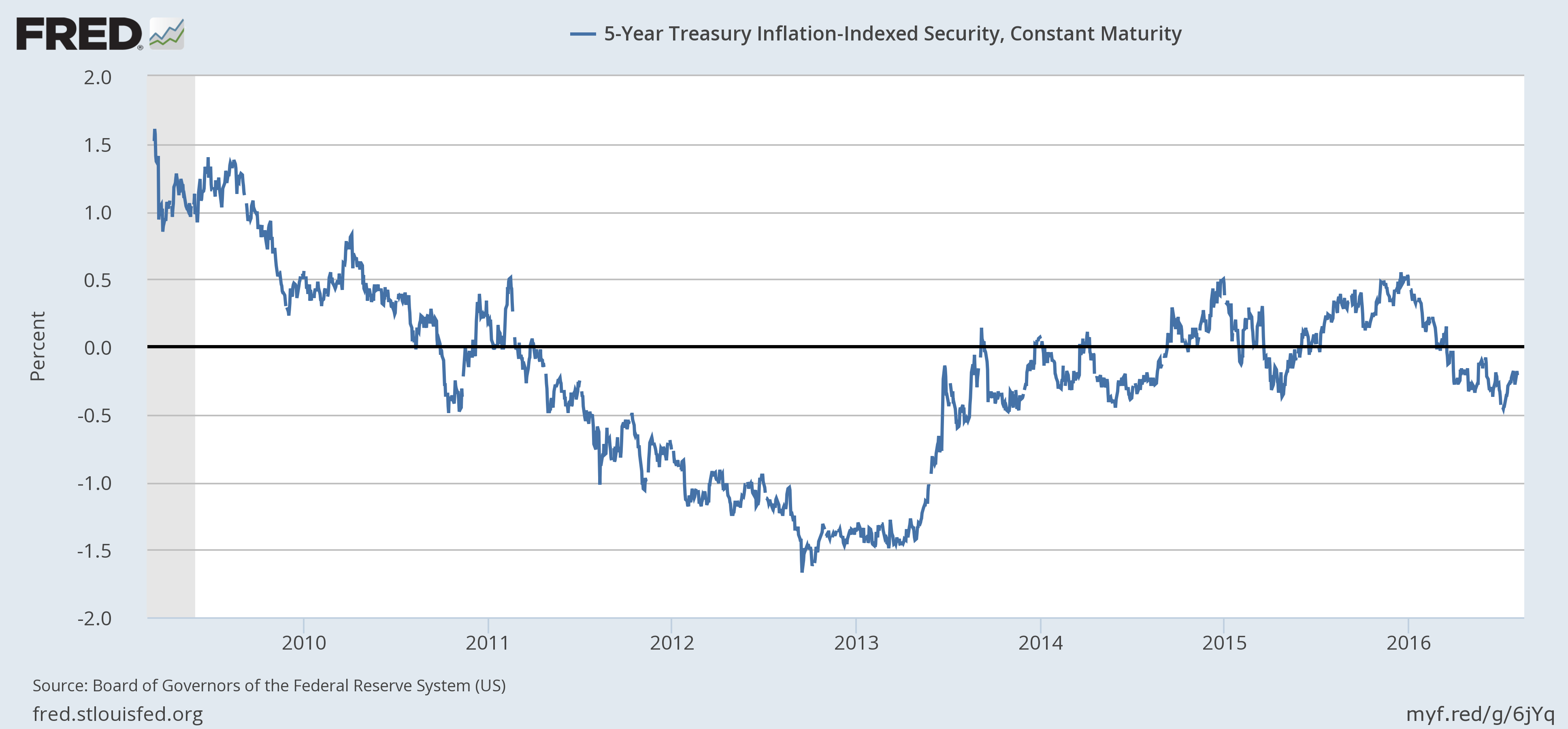

5-year treasury inflation-indexed security, constant maturity

{kind=link}

According to CME Group the chance of 25-50bps hike in Sept is now 85% down from 91%

http://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

Don't the 30 day Fed Funds Rate futures prices predict the target rate will more than likely (85%) remain as it is - 25-50 bps corridor? View Fed Funds data

That is the probability of it staying in that corridor, yes. The probability of going up 25bps is 15%

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.