By Jarrod Kerr*

We are in the middle of a seismic shift.

We are in the middle of a seismic shift.

The post‑war baby boom was the largest in human history. The baby boomers are now retiring. Their influence on interest rates is profound, and understated.

The three Ps of growth are in metamorphosis. The first P, population, is waning as fertility rates decline. The second P, participation, is declining as populations’ age. The third P, productivity, is also being weighed down by ageing populations.

Fed researchers say demography explains ALL the decline in real interest rates. We think this fits with other work showing the US real neutral rate is near zero and that market pricing for the Fed to only slowly raise rates to 2% is not too aggressive.

We are not all created equal. There is one differentiator. Immigration is the fountain of youth. Interest rates in high migration nations like the US, Australia and New Zealand, should diverge further from old Europe and Japan.

The risks are evening up and we see room for Treasuries term premiums to lift and take 10yrs to 3.0%. But the demographic story tells us we shouldn’t be looking for much more on a through‑the‑cycle view.

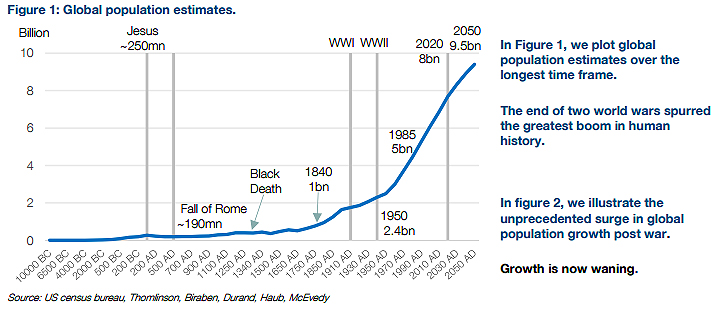

The end of two world wars spurred the greatest boom in human history.

We often hear of the impact of demographics. Demographic shifts influence just about everything we touch. We are in the middle of the largest demographic shift ever experienced. The seismic shift will keep a lid on potential growth and real yields. Yields can rise from here, off historic lows. But we are unlikely to see the levels once deemed “normal”, prior to the great financial crisis.

Interest rates experienced during the great inflation period of the 1970s and 80s are the anomaly – generated by the largest surge in population ever recorded. A population surge that boosted growth, put an enormous strain on resources, and caused inflation to spiral to levels no longer allowed.

Expansionary fiscal policy and regulated market structures, compounded by OPEC, no doubt contributed to higher interest rates. But, according to the US Fed, demographics explain ALL of the subsequent decline in real interest rates, and potential growth rates. That may be excessive, but it fits neatly with theories of a new normal that we think will keep interest rates and bond yields low. Notwithstanding some rise in term premiums to come.

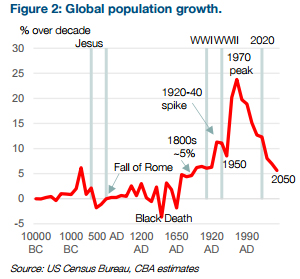

The population boom like no other, drove the never before seen spike in interest rates

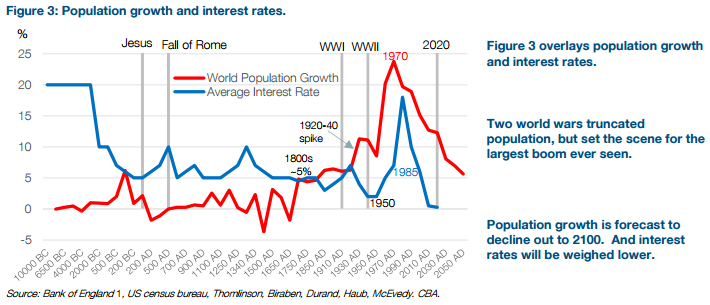

In Figure 3, we overlay global population growth with global interest rates back to 3000BC. What stands out is the baby boom, and the impact on interest rates. The peak in population growth is long behind us, so too is the peak in interest rates. We are now in a “new normal”, with lower terminal rates. We are not all created equal, however. Australia is much younger than most. And fertility is not the source of Australia’s youth. Immigration is the fountain of youth. Immigration policy influences the three Ps of potential growth, and suggests growth and interest rates will be higher in countries like the US, Australia and New Zealand.

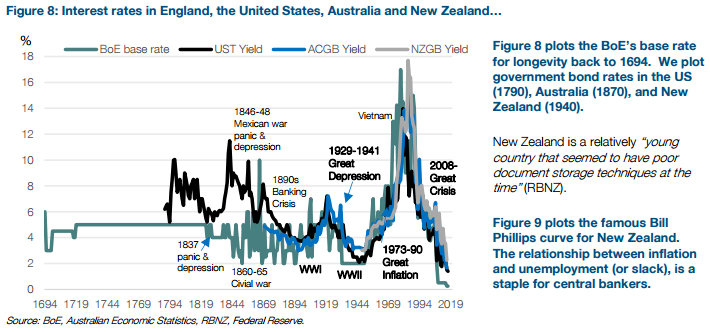

Early interest rate settings ~3000BC were between 20‑40%. Interest rates declined as markets evolved, and averaged a much more civilised 5.5% between 500BC and 1910. Churches and Kings were known to control interest rates, from time to time. By 1950, following two world wars and a great depression, interest rates had fallen to the lowest levels ever scribed. A record low that was smashed 66 years later with the advent of negative interest rates. The ‘great inflation’ period of the 1970s and 80s stands out. The spike in population preceded the spike in rates.

Global population jumped from ~2‑to‑2.5bn in 1945‑50, to ~4.5‑to‑5bn in 1980‑85. In just 35 years we more than doubled our population. The impact of the tsunami of baby boomers was profound. The surge in population induced the highest levels of interest rates in 5000 years. Interest rates peaked in the early‑80s. From 1985 to 2020, the subsequent 35 years, it is estimated our population will rise to ~7.7bn. That’s another 2.7bn increase, but off a much higher 1985 base of 5bn. The rate of growth has halved from that experienced in the baby boom.

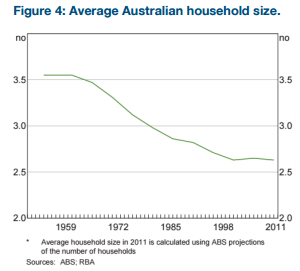

The decline in population growth has coincided with a 30 year decline in interest rates. Population growth will continue to slow for the next 35 years. From 2020 to 2055, the next 35 years, global population is forecast by the IMF to hit 9.5bn (+1.8bn). Population growth will halve again. Society has changed. Fertility rates have declined since the 1960s. Family sizes have declined (Figure 4). There has been a steady rise in childlessness, higher divorce rates, and later marriage. There has also been a healthy lift in female labour force participation. Reduced population means reduced pressure on resources and rates.

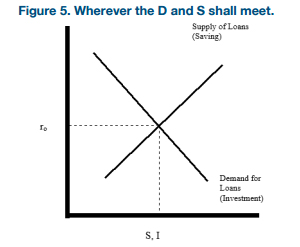

An interest rate is simply a price for credit. The two most beautiful lines that shall ever meet are supply and demand (Figure 5). The supply of credit, (savings), balances the demand for credit, (investment), at a price, (interest rate). Baby boomers became productive in the late 60s and demanded interest rate product. The greatest spike in global population growth preceded the greatest spike in global interest rates. A surge in demand for global resources, played out most notably in commodity markets, but also interest rates (the “D” line shifted out). The three Ps rose, real growth rose, real rates rose, but inflation pushed nominal rates into the stratosphere.

The demand shock for all resources took place at a more supply‑constrained time. Regulated labour markets and product prices, and geopolitical oil shocks (plus “peak oil” theories) were rigidities that took years to overcome. Rampant commodity price inflation fuelled the rise in nominal interest rates. Deregulation was the response of the 1980s. Global trade and competition took off as Eastern Europe, Asia’s tigers and China entered the world economy, with the impact exacerbated by disruptive technology and globalisation.

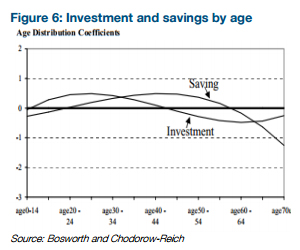

Fast forward to today. There is push‑back against immigration, competition and globalisation. That could give rise to an inflation pulse in due course. But more importantly, baby boomers have been retiring and supplying interest rate product. A large driver of the glut in global savings has been the saving of baby boomers into their retirement (the “S” line has shifted out). We do most of our savings in our working years, and savings accelerate into retirement (Figure 6). That wave of baby boomers may have reached “peak” savings in developed countries but there’s still a global wave to flow through as populations age in many developing countries.

The supply “glut” has occurred at a time of higher production capacity, globally. China’s export‑led investment boom has run into a western savings boom and a (related) global financial crisis, but it hasn’t yet developed a consumption model of its own. We’re simply producing much more for less. Labour markets are more flexible, prices are generally market driven, and the supply of commodities, globally, has now caught up and risen substantially. The increased supply of commodities has driven much of the decline in prices in recent years. Reduced commodity price inflation has reinforced deflation fears.

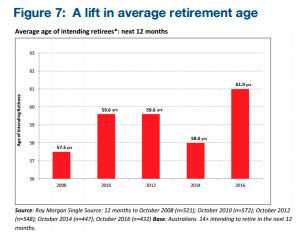

The next phase, is retirement, where savings declines (Figure 6). The baby boomers will slowly unwind their savings over the next 20‑30 years. Eventually, the supply curve (of loans) will contract back. But it will be a long, slow process. Roy Morgan recently produced the results of a survey on intending retirees in Australia. The average age of intending retirees has lifted from 57.5 to 61 (Figure 7). The average age rose post crisis, dropped in 2014 with the rejuvenation in financial markets, and has now blown higher with the continued decline in deposit savings rates. Not surprisingly, the survey of ~50k respondents showed that gross wealth (excluding owner‑occupied homes) of intending retirees is up just 3.6% since 2014.

The other, yet to be tapped, source of wealth is the family home. “A clear majority (85%) of intending retirees either own or are paying off their home, with an average value per person of $495,000 or 73% higher than the average ($286,000) in all other retirement funds.” The value of that dwelling has jumped 43.5% since 2008. Demographics shape property markets. Retiring owner‑occupiers supply large dwellings in search of small, high density, dwellings. Young families and migrants upsize.

The Bill Kerr example: there’s at least one in every family, probably four.

My father was born in 1947. He is the second of four baby boomers. He became productive in the 1970s when he joined the workforce, after a tour or two in the NZ navy. He demanded an interest rate, in the form of a mortgage, to build his first house. Later, he demanded another interest rate, to start his first business. Interest rates were in demand. Interest rates went well into the teens, some were above 20%. 35 years later the business has been sold. The family home went under the hammer. And the old boy has downsized and retired to Mangawhai Heads (north of Auckland) with a war chest of savings. He now supplies an interest rate. The interest rate he supplies, in the form of a fixed rate deposit, is far less than he had imagined.

Despite his son, an interest rate strategist, convincing him to fix into the falling yield environment, yields are much lower than any forecast a decade ago. And fixed rates only last so long. Risk appetite is something the old boy does not have, not at his age. Supply of term deposits are sticky for this age bracket.

Of course the four Kerr boomers had children of their own. But they had ~2 children each, not four like their parents. And the grandchildren are having fewer children than their boomer parents. We only want 1 or 2. Four children just seems inhumane…

Bill Kerr is just one man, one example, one in the millions of baby boomers now retiring into a low yield environment. Asset rich retirees have much lower risk appetite. Interest rates are currently on the rise. But the stock (supply) of global savings hunting yield remains high. Baby boomer savings rates will naturally run down, as retiree’s consume their nest eggs. And interest rates may eventually lift to higher levels. That may be a problem I’ll leave to my son Lachlan to figure out, on behalf of his old man.

Demography is destiny

The correlation in global interest rates has strengthened since WWII. Globalisation has strengthened the interconnectivity of markets. The great inflation period was case in point. All populations surged, all markets rose. Inflation was then deemed evil by central banks. Despite poor record keeping, the Kiwis were the first to directly target inflation in 1989. Don Brash, then RBNZ Governor, referred to the great inflation period as a great tax on savers. Brash also noted real estate as an inflation hedge, during the 1970‑80s. Central banks spent the next 25 years riding inflation down to targets of ~2%, successfully anchoring inflation expectations. Job done. Well, they did some of the job. It turns out demographics did most of the heavy lifting, on the way up, and on the way down.

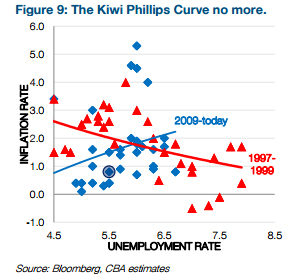

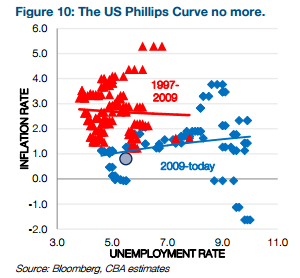

Phillips curves have now inverted. The decline in the Phillips’ curve can be attributed to demography, globalisation, and central bank behaviour. Inflation targeting anchored expectations. The decline in inflation was also driven by globalisation, or the rise of Asian manufacturing. The Asian rise has in part fuelled political discontent in the West (Brexit and Trump). Future inflation expectations have also become more backward looking2. Post‑GFC, the threat has been losing control of expectations to the low side.

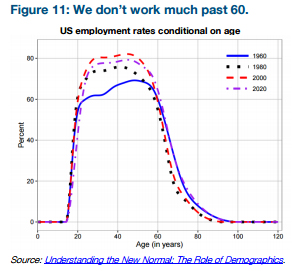

Demographic forces have ballooned in the last decade as baby boomers retire. The decline in inflation has been weighed down by ageing populations. Ageing populations have lower productivity and wage expectations. Figure 11 highlights the cliff in participation past the age of 60. A cliff that has worsened since the 1960s. Deflation was (still is?) the threat. And risk appetite remains impaired. Panicked investors still pay for protection of capital. Negative interest rates are an intergenerational wealth transfer. Negative rates “transfer” wealth from savers (elderly) to borrowers (younger generation). Negative rates are a tax of savers.

According to the US Fed, demographics explains ALL of the decline in real interest rates and potential growth rates. The Fed’s demographic model:

“accounts for a 1¼ percentage‑point decline in both real GDP growth and the equilibrium real interest rate since 1980 ‑ essentially all of the permanent declines in those variables... The model also implies that these declines were especially pronounced over the past decade or so because of demographic factors most‑directly associated with the post‑war baby boom and the passing of the information technology boom. Our results further suggest that real GDP growth and real interest rates will remain low in coming decades, consistent with the U.S. economy having reached a new normal."

The Fed notes that the influence of demographics has been “easily misinterpreted as persistent but ultimately temporary influences of the global financial crisis”.

The implication from the Fed’s research is “the persistence of a low equilibrium real interest rate means that the scope to use conventional monetary policy to stimulate the economy during typical cyclical downturns will be more limited than it has been the case in the past for a given inflation target.” Demographics explain much more than most dare admit. Policy makers may be at the helm of a ship, with a tiny rudder.

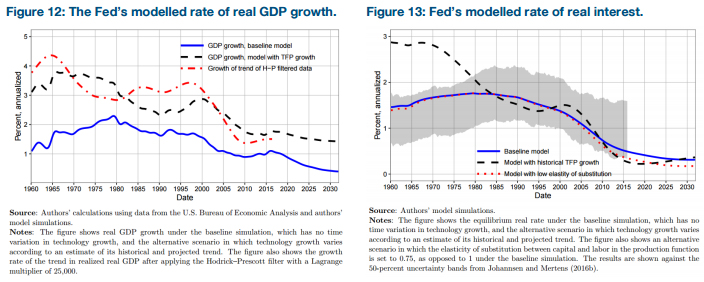

Figure 12 shows the decline in the real rate of growth from a peak above 2%, to a current rate sub‑1%, and a forecast decline to ~0.35%. Figure 13 illustrates a similar forecast decline in the real rate of interest from ~1.75% in the 1970s‑80s to ~0.35% out to 2030.

The Fed’s demographic work fits with other aspects of the ‘new normal’ theory, including Larry Summers’ ‘secular stagnation’.

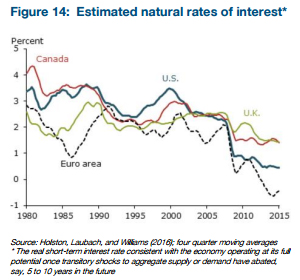

Figure 14 plots the estimated natural rates of interest since 1980. Natural interest rates had declined from a 2.5‑to‑3.5% range in the early 1990s to 2.0‑2.5% pre‑crisis. Following the GFC, the estimated ranges have collapsed to 1.5% for Canada and the UK, near zero for the US, and well below zero for the Euro Area.

The underlying determinants for these declines are related to the global supply and demand for funds, including shifting demographics, slower trend productivity and economic growth, emerging markets seeking large reserves of safe assets, and a more general global savings glut... Importantly, this future low level of interest rates is not due to easy monetary policy; instead, it is the rate expected to prevail when the economy is at full strength and the stance of monetary policy is neutral. - (Williams, San Francisco Fed).

We think very high global debt dynamics and abundant spare capacity in the global economy also explain why the real natural rate of interest has dropped.

Yellen believes “that monetary policy will, under most conditions, be able to respond effectively” to future downturns in the economy even if interest rates are much lower than in the past (through the use of more QE and interest rate guidance). But she didn’t sound confident. And she didn’t disagree with the notion that the real neutral rate is 0%. Which means she won’t be in a rush to raise rates to this level even if inflation ticks up.

“If the natural rate remains low, future episodes of hitting the zero lower bound are likely to be frequent and long‑lasting… This will necessitate a greater reliance on unconventional tools like central bank balance sheets, forward guidance, and potentially even negative policy rates.” - (Laubach and Williams, US Federal Reserve)

A real rate in the US that averages 0‑0.5% would equate to a nominal Fed Funds rate averaging around 2‑2.5%.

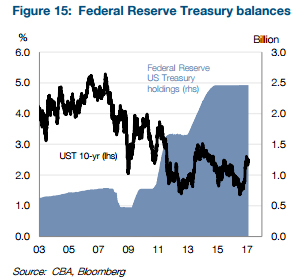

The Fed’s QE programme, or size of balance sheet, continues to exert significant downward pressure on US yields (figure 15). Fed modelling shows that QE has pulled the US 10‑year yield down by around 100bps. Ending reinvestments would cause a "passive" removal of this accommodation but seems a long way off. Still, Janet Yellen recently noted that even the current policy is resulting in a shortening of the Fed’s maturity profile that "could increase the yield on the 10‑year Treasury note by about 15 basis points... over the course of 2017… all else being equal."

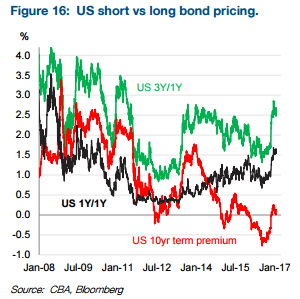

Figure 16 shows that normalisation of the term premium has been a source of the rise in bond yields over the last 6 months. But there is likely more to go. If the nominal Fed Funds rate averages around 2‑2.5%, a rise in term premium for 10‑year bonds back to 50‑100bps implies that yields on 10‑year US Treasuries may range between 2.5‑3.5% in the years ahead, averaging about 3.0%.

A lower term structure in the US means a lower term structure globally.

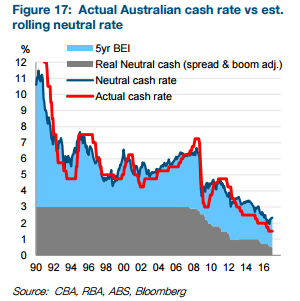

We think Australia’s real neutral rate has come down to around 0.75% (Figure 17, which updates numbers for analysis published in 2014, when we had the estimate at 1.0%). Adding a higher long‑term inflation target suggests there is a healthy margin versus the US of at least 1.0% in nominal terms and closer to 2.0% versus Europe and Japan (not that we expect Australia to be near capacity or the mid‑point of the 2‑3% inflation target for a number of years).

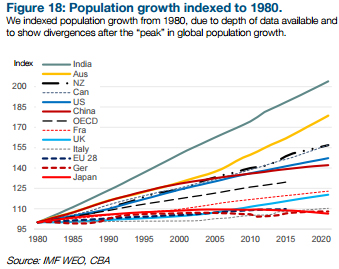

We’re interested in whether these divergences are likely to persist. The US has a relatively young population because the US attracts young migrant workers. Australia and New Zealand even more so. It’s a numbers game.

Figure 18 plots the stark divergences in population growth, indexed back to 1980.

Real rates in the US are higher than ageing peers such as Germany, Japan, and Italy. US rates will remain well above Japanese and European rates. Antipodean rates will remain above US rates. In this numbers game, migration matters the most.

Migration is the fountain of youth

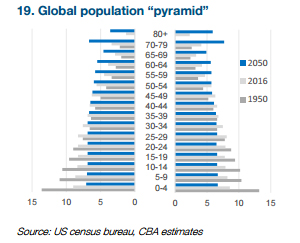

As we age, we participate less. The fall in participation rates across much of the ageing world is related to the rising share of people over 60. The ‘normal’ so‑called global population pyramid now looks more like a Trump tower (Figure 19, males on left, females on right). There’s a lot of advertising up top.

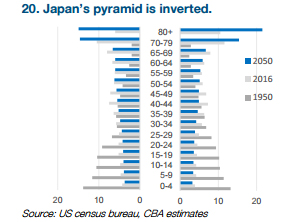

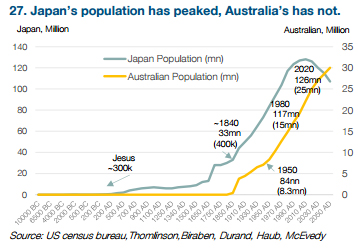

Figure 20 shows Japan’s population pyramid is now upside‑down. The remarkable, and difficult, swing in Japan’s population is the most extreme. In 1950, after WWII, 45% of Japan’s population was under the age of 20. By 2050, 45% of Japan’s population will be over the age of 60. Japan will have 15‑20% of its population over 80 by 2050. Germany and Italy also have much older populations (though Germany has rapid productivity growth and the Syrian refugee crisis will alter the population projections across Europe).

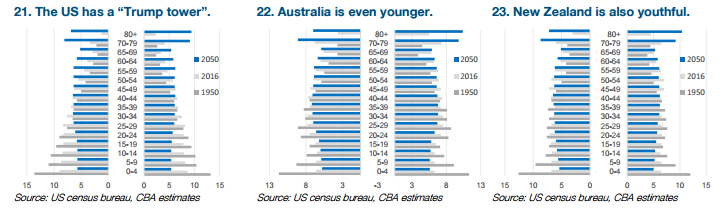

We may all end of like Japan, eventually… But not over the next 50 years. The US, Australia and New Zealand have much younger populations (figures 21 to 23). The most important difference is immigration. Migrant flow can solve (or at least postpone) a lot of our “first world” problems.

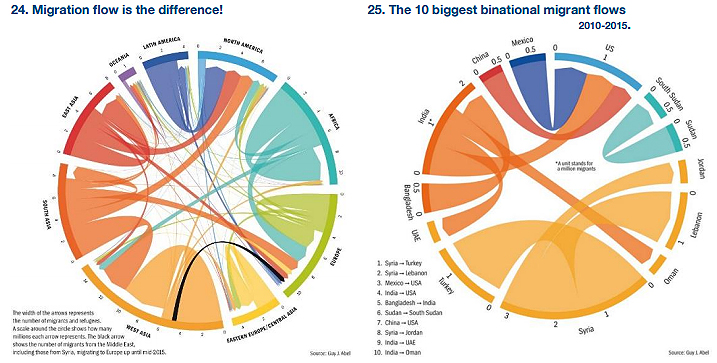

The best work I have found on migration comes from Guy J. Abel, Nikola Sander, and Ramon Bauer (http://www.global‑migration.info/).

North America attracts massive flow from Latin America, India, and China. African flow to the US is fourth. Most African flow remains on the continent. Most Asian flow also remains on the continent.

Migration paths do not lead primarily from very poor to very rich countries, but rather adhere to a graduated model. People move to countries where the economy is somewhat stronger than in their native country… from Bangladesh to India or from Zimbabwe to South Africa. - Guy J. Abel.

The largest flows on the planet come from the most populous places on the planet. Outside the Syrian crisis, the largest flows are Mexico to the US, India to the US, Bangladesh to India, China to the US, India to UAE and Oman. The US has been the largest recipient. But has just voted to build a wall to stop the flow. The potential growth rate of nations with higher immigration is simply higher. The population pyramids are fatter and younger. The growth in number of workers is larger and so is GDP, even if not on a per capita basis. The US, UK, and Antipodeans attract migrants. A flow Trump was voted to address, and Brexit voted to break.

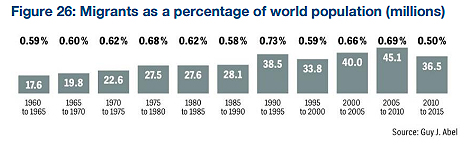

Figure 26 shows the number and percentage of 5‑year migration flows, back to 1960. Despite the Syria crisis, there are fewer migrants as a percentage of total population, dating back to the 1960s. In absolute terms, there are fewer migrants than during the 2000‑2010 decade. Abel and Sander note: “Our data suggest a stable intensity of global five‑year migration flows at about 0.6% of world population since 1995.” A finding that is contrary to common belief, which is that migration trends are on a larger and ever‑increasing scale. Abel and Sander show migration rates are holding, with recent numbers actually declining. It appears it is our tolerance of immigrants that has diminished.

Beware the wrath of a patient man

The relatively normal flow of migration is interesting, given the political revolt. Anti‑immigration sentiment defined 2016. Votes for Brexit, Trump and Australia’s Pauline Hanson are against globalisation. The revolt has arisen out of economic discontent, post crisis. Discontent in having to postpone retirement plans. Discontent in having to work without wage growth.

“Across Europe parties of the far left and the far right are seeking to exploit this opportunity — gathering support by feeding off an underlying and keenly felt sense among some people — often those on modest to low incomes living in relatively rich countries around the West — that these forces are not working for them… And those parties — who embrace the politics of division and despair; who offer easy answers; who claim to understand people’s problems and always know what and who to blame — feed off something else too: the sense among the public that mainstream political and business leaders have failed to comprehend their legitimate concerns for too long.” Theresa May, British PM.

One of the repercussions from the financial crisis and demographic shift, is isolationist actions. Professor Simon Hix from the London School of Economics, reduced the Brexit vote to an issue of immigration. Because the “leave” voters voted on immigration3. The vote was divided by class, education, age, and ethnicity.

Voters who classed themselves as “English” wanted to leave. “British” voters wanted to remain. Voters from lower social classes with lower levels of education voted to leave. Older baby boomers voted to leave. There was a great divide across skilled labour. Professionals voted to remain. Lower skilled workers voted to leave. “A revolt against the elite, the wealthy, and the immigrant…: “A class of people are very angry about mass immigration policies.” “In aggregate mass immigration is great for the economy... Cheaper costs for business. Great if you’re higher income… But if you’re a lower skilled worker, there’s much more competition for your job…” (Pr. Simon Hix).

“We’ve been ignoring the negative distributional consequences of mass immigration… [Immigration] Leads to pressures on lower skilled wages… Leads to pressure on local public services. Pressure on schools...doctor’s surgeries… local council housing… and social integration pressures with different languages, different cultures… this had all been ignored……We need public polices to address these distributional consequences” (Pr. Simon Hix). Immigrants are generally of high participation age, 20‑40, and they are generally cheaper. Studies show migrants are entrepreneurial, setting up a small business (taxis, child care, or stores). In good times, society enjoys cheaper migrant labour. In bad times, displaced locals regret migrant competition.

Tolerance of foreigners has fallen with weak income growth, and poor distributional consequences. Fiscal policy is needed to alleviate stresses on the system. Fiscal policy is the policy missing.

"Why has monetary policy been ineffective in bringing inflation up to target levels in the US, Europe and Japan? ...monetary policy effectiveness requires that...at low inflation rates interest rate declines generate fiscal expansion. The persistence of low inflation and low interest rates is not a surprise when, as has been true in fact, the low interest rates fail to generate substantial fiscal expansion[and thus aggregate demand expansion]." Christopher Sims

The lucky country. Lucky to be in demand

Australia fares better than most advanced countries.

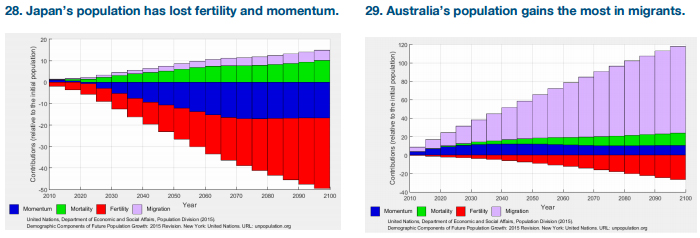

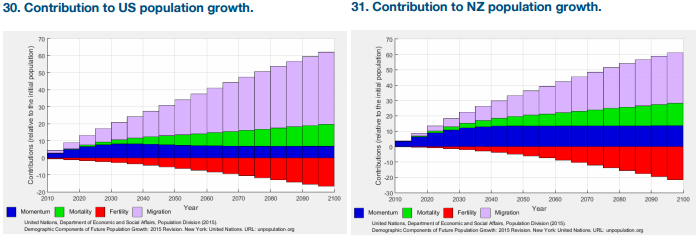

The UN’s population division projects the contribution to future population growth across four demographic factors: fertility, mortality, momentum and migration. “All four demographic components can have a significant impact, positive or negative, on future population growth.” The stark divergence between the oldest nation Japan (figure 28), and the younger nation Australia (figure 29) is momentum and migration. The US and New Zealand (figures 30 and 31) are similar to Australia.

The source of Australia’s migrant flow is important.

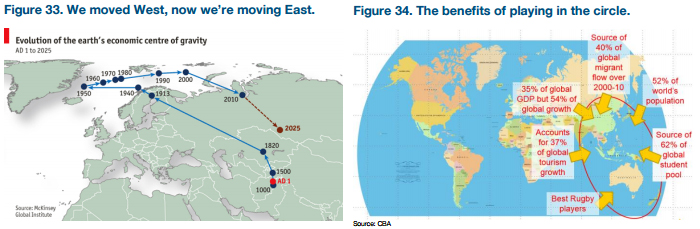

Australia’s proximity to Asia is increasingly important. Australia has one of the youngest populations because of proximity. Australia’s economic prospects are better because of proximity. Being at the end of the Earth was once a hindrance for economic trade. Australia is now closer to the economic centre of the world. Because the economic centre of the world is gravitating towards the greatest populous in the world.

We include the “economic centre of gravity” map from McKinsey Global Institute (Figure 33).

Our inner circle has most of the world’s population. Our inner circle generated most of the world’s economic growth. A large chunk of global migration flows are born in our inner circle. The world’s best cricket players, and the hardest rugby players, are forged in our inner circle.

Our inner circle, is where the cool kids play.

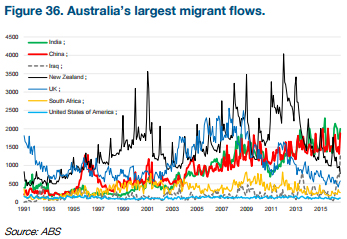

Figure 35 shows the 2010‑15 flow of migrants for Australia. The greatest change in Australian immigration flow has been the source. Australia now attracts more migrants from East Asia, South Asia and Africa than Europe. India sends the largest flow of immigrants, followed closely by China. When Australians leave, they go to Europe. That flow hasn’t changed a lot.

Figure 36, shows a time series of immigrants to Australia. The highlight has been the persistent rise in Indian and Chinese immigration since the late 1990s. Conversely, the sharp spikes in UK and Kiwi migrants have largely unwound. Kiwis are, for the first time in 25 years, leaving Australia.

So what’s the attraction?

Australia is a developed nation, with great beaches, reefs, and an old English game called cricket (the Kiwis took rugby).

Most of all, it’s safe. Ok, there are loads of creatures that will kill you on sight, but “she’ll be right mate”. It’s the drop bears you have to watch out for. There are many peoples attracted to the great down under. Most immigrants have been European, some Middle Eastern. But today, most immigrants are Asian.The greatest flow comes from India. For a poorer country like India, another former English colony, there’s a lot to love. Australia offers a massive upgrade, with the “simple” things like water, food and transport well catered. The Australian language is even similar to the English language, with just a slight twang. The education is top notch. There’s a common love affair with bat and ball. And the legal system is close enough. Being a Kiwi, I understand the attraction.

Then there is the Chinese flow. Again, the attraction is clear. Everything is cheaper in Australia. The water is crystal clear. You can drink it from the tap. The food is fresh. You have to wear sunglasses, because there is no smog to block it out. The quality of the housing is better, and far cheaper per sqm. And then there’s a little something called English property rights. I buy it, I actually own it. And I can bequeath it. Aussie apartments make for great safety deposit boxes. Matching the safety deposit boxes used in Singapore, Canada, New Zealand, and the source of those property rights, the UK. The Aussie apartment could also be used by children sent here to study hard at university. We know they’re safe. And the children will probably convince the entire family to move down later. No wonder Chinese developers in Australia ask us for our student visa forecasts.

The third flow of interest is the flightless bird. Kiwis come to Australia in the good times, and return in the relatively bad. I think the clearest signal of the current weakness in Australia’s labour market, is the exodus of Kiwis. Kiwis are the cheapest, most mobile part of the Australian workforce. And they don’t all show up in unemployment. Because they go home. For the first time in 25 years net permanent migration turned to an outflow in 2016. Kiwis are returning home after years of mining boom related work. The return of the Kiwi miner has induced a sizeable spike in Auckland house prices.

Another persistent flow has been South African. I should know, I married one. The reasons my wife, and her family of +50, left South Africa for Australia and New Zealand are sad and violent. Again, there is a lot to love about Australia. It’s safe.

Australia’s immigrants are from the power houses of the future. And they will strengthen our ties

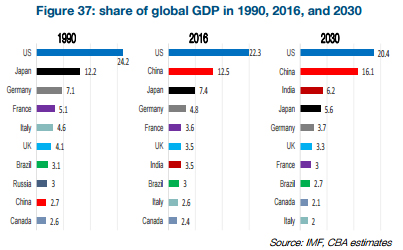

In the 1990s few took China seriously as an economic power. China barely made it into the top ten economic heavyweights.

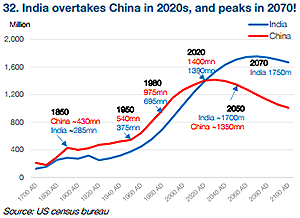

There is another relationship, with another country that deserves more airplay: India. India was not on the economic map in 1990, but had risen to 7th behind the UK in 2016, and is forecast to knock off Germany and Japan by 2030. India needs resources to feed and house the greatest population on Earth.

India will have more people than any other nation in 2022. India will be the third largest economy by 2030. It’s a numbers game, and India has more numbers than any other. When it comes to economic size (and importance), it is no coincidence that the oldest (most ageing) nations, Japan, Germany and Italy, are falling in the global rankings. Japan will slip from 2nd to 4th. Germany will slip from 3rd to 5th. Italy will slip from 5th to 10th. France is also ageing, and falling from 4th to 7th. The UK is holding tight to 6th position, with strong migration growth (at least up until Brexit).

Progressive economic policies and a lot of investment are needed for India to truly succeed.

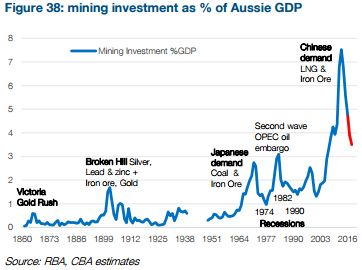

Australia has just been through the greatest mining investment boom in its history (figure 38). Australia has developed its largest ever stock of mining resources. And there are plenty of other holes that can be dug, at the right price. China’s industrialisation was far greater and faster than any forecast.

India’s industrialisation may mimic China’s, one day. If India develops, the emerging nation will demand a great deal of resources, including coal, iron ore, gold, and LNG. Mining investment in Australia, figure 33, could easily see an India induced spike in the 2020s, or 2030s. Developing nations also demand increasing food, education, and travel services. Australia is well equipped to leverage these three industries.

But the connections between Australia and Asia also mean that migration flows are likely to continue.

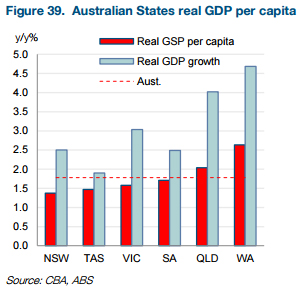

Queensland and Western Australia have out‑performed over the long haul due to their abundance of natural resources. But, for all of the claims made about relative economic performance, and who’s leading the nation, etc, it turns out that the difference in GDP per capita among the four remaining states is negligible. It is the difference in population growth that explains the difference in GDP growth. And it is that difference in population that growth that will mean Australia and New Zealand continue to average higher interest rates against the new normal of low interest rates around the world.

An attempted summary of what it all means

Over the coming decades the ageing of Australia's population and a projected slowing in the rate of population growth are expected to affect the nation's economic growth. The components of the above decomposition most likely to be affected by the population changes are average hours worked and the participation rate, as people get older and move into part‑time work or out of the labour force. Australian Bureau of Statistics.

Demographics explain much of the decline in potential GDP growth and real yields.

• We are in the middle of the largest demographic shock ever seen. The surge of the 1970s‑and‑80s was baby boomer induced. It can be argues that the decline in growth and interest rates ever since has simply been the result of slowing in population growth, and ageing in populations. Growth rates, inflation rates and interest rates will all be lower for longer as our population ages.

• Real rates are likely to remain well below 1% into 2050. Term rates globally will remain in a much lower for longer band. At least until the baby boomer savings unwinds. Policy makers must consider “alternative monetary and fiscal policies that are more likely to succeed in the face of a low natural rate.” John C. Williams

• There is a lot that can be done to prolong and improve our outlook. “Productivity isn’t everything, but in the long run it is almost everything.” Paul Krugman. The focus of policymakers, especially governments, must turn to productivity. Investment in education, technology, and infrastructure are all part of the equation. The investment requires large, long term, Government policy. The weakness in Governments, or lack of fiscal response is unusual historically. Voters want change.

• "The persistence of low inflation and low interest rates is not a surprise when, as has been true in fact, the low interest rates fail to generate substantial fiscal expansion.” Chris Sims. We need to invest more. We need to invest for productivity. We have ample capacity.

• Short of that, voters want inflation. More insular politicians are starting to deliver policies that will limit competition and supply flexibility, creating an environment where inflation pricing over and above on‑going low real interest rates should creep higher. Ourforecasts for higher bond yields reflect expectations for the term premium in the bond market to rise, not for much change in pricing of terminal policy rates.

• Embrace the ageing. Retiring at 65 doesn’t have to be. Innovative solutions to keep people employed for longer, through flexibility and technology, are needed to stem the tide. My father was bored out of his mind when he first retired. Now he heads the North Island Returned Services Association (RSA), and runs around more than he did when he was “working”. There’s a lot of untapped labour, with ample experience, should we want it.

• Immigration is the fountain of youth. Countries that attract immigrants will fare better than those with closed borders. The outlook for Australia is better than most because it attracts people, and at this point in time mainly Asians tapped into the world’s strongest growth story. Relative higher growth in population points to on‑going relative higher interest rates.

For all Notes and Sources, see the original piece

Jarrod Kerr is the director of interest rate strategy at the Commonwealth Bank of Australia, based in Sydney. This piece is an extract from this daily publication. It is here with permission.

51 Comments

Not one squeak about the impact of ever growing populations on finite and increasingly scarce resources and the climate. These areas will be the brake on any growth and bankers and finance experts will try to ignore them and provide alternate facts to explain events, the the fact remains - the universe will require a balancing of the books, and unless we do it ourselves the result will be ugly.

Exactly. The world is overpopulated and at some stage every country is going to have to go through the difficulties of an ageing population and low birth rate. The answer is to think of solutions to the problem, not try to defer it indefinitely.

I don't dispute the world has population issues. But I do think most people are pretty superficial when it comes to "overpopulation" concepts. The current world population is about 7.5 bln, and to many people that seems like an enormous number. But is it really?

Just as a thought exercise, if every person was allocated an area of 100m2 (ie 10m x 10m), you could fill the world's population into Chile, or Zambia. That would leave the rest of the work with zero population. (10m x 40m for a four person family is about the size of a smallish New Zealand inner city section.)

If you gave them each ten times that (ie each had the size of a rubgy field) the whole world population would fit neatly into Australia, or Brazil. For a family of four, that would be a lifestyle block - for absolutely everyone in the world - and the rest of the planet would have zero people.

We may well be managing our world population poorly, but it is not because the number is too high. At 7.5 bln it is not high at all given the size of the world's land area (150 mln km2), even the world's habitable land area. The "rats on sinking ship" image is pure urban myth.

Of course we are getting closer to "the limits" - and we always have been. But closer does not mean close. (And I know this will not persuade those who see the apolocypse just around the corner.)

My core point is that most people seem to be unable to comprehend really large numbers, and relate them to other really large numbers. The result is bumper sticker 'conclusions' and these don't help us make sensible plans.

I do agree however that we have a climate problem. And I agree that the climate problem is increasingly man-made. I even agree the way we are responding/not responding to a fast rising population is part of those issues. But I don't agree that 7.5 bln people are "too many for the planet". That is not our problem. Our problem is the choices we are making in how we organise ourselves.

Earth overshoot day:

"On August 8, 2016, we began to use more from nature than our planet can renew in the whole year.

We use more ecological resources and services than nature can regenerate through overfishing, overharvesting forests and emitting more carbon dioxide into the atmosphere than forests can sequester."

I hear the sound of many axes being sharpened...

(sorry, that was intended to be in response to DC's narrow view comments)

Be careful about promoting the UK's "New Economics Foundation" and their surveys. These are the people that claim Venuzuela is high up in their happy planet index ! Pretty nutty.

I came across this from the UNDP - Helen Clark's branch:

"Should the global population reach 9.6 billion by 2050, the equivalent of almost three planets could be required to provide the natural resources needed to sustain current lifestyles."

Big statement that!

http://www.un.org/sustainabledevelopment/wp-content/uploads/2015/08/Fac…

I guess this is saying, with our existing 7.5 billion and only one planet - if a projected 30% increase (although it didn't provide a source for that number) in population means we need three planets ... why would we be promoting the "development" part of "sustainable development" at all? Is the whole notion of "sustainable development" an oxymoron?

Perhaps SD (sustainable development) needs to be re-defined as ED (equitable distribution) - as the whole 1987 report that coined it as a new objective was about improving the lot of least developed countries.

However, the most developed/most prosperous countries latched on enthusiastically from 1987 onwards, using it to legitimise completely unsustainable practices in their own countries.

Share the wealth - save the planet.

I wonder if this would be a whole lot more simple and useful than the 16 Sustainable Development Goals.

Agree with all these oxymorons ... sustainable development, renewable energy etc

"Share the wealth - save the planet."

Unfortunately this is a fallacy. All the earth/economy physically produces each year is all there is to "share" each year. ..The pixels in bank accounts may represent a claim on a future energy flow ... but that doesnt mean it exists NOW

eg.Bill Gates may have billions in pixel wealth but he doesnt actually CONSUME this in a given year. He cant, because the resources dont exist. The pixel wealth flow to the very rich actually keeps NET consumption down

Not sure it is a fallacy. The correlation between lower birthrates and higher income is pretty strong although many questions still being raised;

https://en.wikipedia.org/wiki/Income_and_fertility

Notwithstanding: "share the wealth - save the planet" makes lots of sense to me.

David. The argument of fitting everyone into Australia at 1 person per hectare or Chile at 1 per 100m2 is spurious. We could fit everyone into Antarctica at approximately 1 person per hectare and what great lifestyle blocks they'd be! There is total land area, there is habitable land area and then there is productive land area; the latter of which is a very very small proportion of the total.

As an agriculturalist I can tell you that while I may be able to stock 2-3 cattle to the hectare in the Waikato, I would be lucky to get 1 cattle per 10 hectares in much of Australia. To put it plainly, Planet Earth is overstocked (for the lifestyle that everyone desires). Yes we can keep using up Planet Earth's natural capital (oil, soil, ground water etc) to maintain this overstocking but it is not sustainable and someone is going to eventually pay the price.

Exactly. Spurious at best.

It's frustrating that some people fail to understand that this issue is more complicated then "can we fit XYZ number of people into this much physical space".

I'm pretty sure most of us could physically fit 50-100 cows in our suburban yards if we crammed them in, has David ever stopped to wonder why this isn't done if it's physically possible?

The size of land doesn't tell the whole story, its what we are doing to the planet as a whole with our current lifestyle. Sure if we went back a few thousand years with this many people perhaps you wouldn't have the same issues, we would each be using the land to grow crops, there would be no cars and no pollution, the planet would be a totally different place. Ultimately the population growth has to stop and it will be forced into decline, its inevitable as the planets resources are finite.If I had to put a date on it, 2050 is about right for it to all hit the fan.

David - its actually not about land at all (although it used to be pre industrialisation). Its about energy availability and more specifically the use of fossil fuels (effectively ancient concentrated sunlight) to radically increase population. Land captures sunlight (energy) and fossil fuels are sunlight in a can. This series does a good job highlighting this (compare energy use versus population growth graphs)

http://anaxeinthehand.blogspot.co.nz/2016/05/wps-2-inventory-of-existin…

The reason we are far closer to the cliff than people think is because we need to keep the energy up to the machine. ie we need to keep adding debt so that Oil arrives so that the food arrives ... the financial system is likely to break before pure environmental limits.

While you may be correct David, about the amount of room for the planet's population, how much space is required per person to provide them with a sufficient balanced diet over their lifetime, shelter and warmth, clothing, a breathable atmosphere, drinkable water and sewage processing? This is the balanced view.

Our culture today, planet wide, is one of consumption, so resource needs exceed the basics by a significant margin - thus my conclusion and echoed by others here is that the planet just ain't big enough.

Don't be so smug David, populations behave in ways that are difficult for us to understand never mind predict. The record of collapse of formerly abundant species, the complete extinction of the American Passenger Pigeon or the collapse of the Grand Banks cod fishery for example.

The Earth is not just for people; we have countless trillions of other beings to consider, never forget that it is life, in all its glory, that makes life on earth possible. The current experiment with exponential human population growth is madness with zero reward and huge risks - pretty much as dumb as you can get.

Before we add more people or embrace an ever increasing population, wouldn't it be sensible to figure out how we can live with the population that we have. Based on the current evidence of global warming clearly we haven't figured it out. At our current rates of population growth and failure to address our pollution problems, it is a dangerous gamble to assume that we will solve the problem in time. At the end of the day nature will have the last word and the problem may well be solved by natural catastrophes as we have observed in the past when natures equilibrium is upset. Far smarter to do something about it before we get to that stage.

It's not the space of the person, but the space for the resources.

A person may take up 100m2 but the resources to sustain that person take up significantly more.

We could fit 10 bln into Australia. But 9.9 billion would either starve or die of thirst. There would be no consumables, no shelter, and the excrement would probably be waist deep after a year.

thanks for the math DC but I think math does not meet the issue. It's not a matter of how many square meters each of us needs to stand upon. Whether that be a double garage, football field or lifestyle block. And why would we maximise up to total possible capacity anyway. That seems dopey. Why is getting bigger even an objective.

I believe the world would be better with less people than we have now. If that means a couple of continents are uninhabited folk can probably just live in the nicer bits.

If New Zealand had fewer people we could abandon some regions. (South Auckland was much better when it had some paddocks between the townships.)

Bang on DC. Half of world's rapidly urbanising population already lives on 1% of the planets land area. That coupled with peak farmland, peak paper in 2013, peak baby in 1990 mean there will be more and more land freed up for hand wringers to fret over, "protect" and give them a sense of worth. The bed wetters just need to get out more and discover how vast this planet is. Drop the Nat Geo and "Scientific" American subs. and do some trekking.

"As discussed in a previous post, by 2100, the world’s population is projected to balloon to 11 billion. Looked at in isolation, that number seems astoundingly high.

Does the earth have enough room to accommodate so many people?

Judging by this map, the answer is a clear yes. While overpopulation may be a localized problem in some of the densely population areas of Asia (see population maps of Bangladesh/India and Tokyo), the vast majority of the world’s land area is actually very sparsely populated.

In terms of area, the black region covers 99% of the Earth’s land. Particularly in Africa, where nearly all of the population growth is expected to occur, there is an abundance of open space for more people to live.

Nearly all of the world’s population growth by 2100 will occur in Africa. By that time, the populations of Asia, Europe, and the Americas will be flat or shrinking."

http://metrocosm.com/world-population-split-in-half-map/

There are plenty of doers out there doing more with less.

Wasteland in to farm land.

"Australian desert farm grows 17,000 metric tons of vegetables with just seawater and sun"

http://inhabitat.com/australian-desert-farm-grows-17000-metric-tons-of-…

https://phe.rockefeller.edu/docs/Nature_Rebounds.pdf

the amount of children in the world today is the most there will be. We have entered into the age of Peak Child. The population will continue to grow as the Peak Child generation grows up and grows old. So most probably three or four billion new adults will be added to the world population - but then in the second half of this century the fast growth of the world population will finally come to an end.

Sorry, Profile, but all those bits of the world we haven't gotten our grubby fingers all over, are occupied by other species, if the human race does reach 11 billion it will be at the expense of even MORE of them.

Grubby? Why the guilt? What are you basing you opinions on? Notice how the price of paper has dropped year after year? Better genetics and management have made timber yields soar without the need for extra inputs. Fact being less inputs for forest and ag as time goes by.

"The animals vary hugely in their efficiency at producing meat. If

they were vehicles, we would say that “a steer gets about 12 miles per

gallon, a pig 40, and a chicken 60.“ (In that scale a farmed fish gets

80 miles per gallon.) Since 01975 beef and pork consumption have

leveled off while chicken consumption has soared. “The USA and the world

are at peak farmland, “ Ausubel declared, “not because of

exhaustion of arable land, but because farmers are wildly successful in

producing protein and calories.” Much more can be done. Ausubel

pointed out that just reducing the one-third of the world’s food that is

wasted, rolling out the highest-yield techniques worldwide, and

abandoning biofuels would free up an area the size of India (1.2 million

square miles) to return to nature.

As for forests, nation after nation is going through the “forest

transition” from decreasing forest area to increasing. France was the

first in 01830. Since then their forests have doubled while their

population also doubled. The US transitioned around 01950. A great

boon is tree plantations, which have a yield five to ten times greater

than logging wild forest. “In recent times,” Ausubel said, “about a

third of wood production comes from plantations. If that were to

increase to 75 percent, the logged area of natural forests could drop in

half.” Meanwhile the consumption of all wood has leveled off---for

fuel, buildings, and, finally, paper. We are at peak timber."

Looks to me you are talking virgin forest being replaced with harvestable forest/crops,and of course no mention of the burn off around the world to make room for palm oil, the demand for which will only increase if the world's population keeps increasing.

Nature gets pretty huffy about species that outbreed themselves and we are and we are not good at sharing.

I for one am not prepared to accept the human race will just gently fade away after 11 billion, we are far, far more likely to enter into war.

My guess is that by the time we reach 11 billion there will be no elephants or rhino and many other species for our descendants to see.

No pockets. Not talking about virgin forest at all. Plantation forest and agriculture. Plenty of tropical platation hardwoods grow at twice the speed of kiwi radiata. Have a read up on precision agriculture. Or even read some of the links above!

Once you have cheap productive plantation forests the demand from virgin dives. It is almost impossible these days to sell natural forest woodchip or a pulp mill that can even pulp it. The world has changed.

Nature gets huffy?! Stick to your guesses mate or perhaps read up a bit more?

"At first, the story of Costa Rica’s forests seems like a tragedy. In the 1940s, over 75 per cent of the country was covered in indigenous woodland, mostly tropical rainforest. In the subsequent decades, however, rampant and unchecked logging ensued as the nation’s valuable forest resources were transformed into cash profits. By 1983 only 26 per cent of the country retained forest cover, and the deforestation rate had risen to 50,000 hectares per year.

At this point, something amazing started to happen. By 1989 the annual deforestation rate had dropped to 22,000 hectares per year. The figure dropped even lower to 4,000 hectares per year by 1994 and in 1998 the deforestation rate had dropped to zero. Today forest cover has increased to 52 per cent (double 1983 levels), and the government has set the ambitious goal of further increasing this figure to 70 per cent and achieving carbon neutrality by 2021.

How did Costa Rica achieve such an astonishing reversal of trends?"

http://unu.edu/publications/articles/ethics-and-environmentalism-costa-…

Sorry Profile. Get over yourself with your insults. Because you can spot some places on the map does not means it's automatically desirable to fill them up. You can imagine living in a crappy overused world, but actually lots of people don't want to.

You've got it around the wrong way. You couldn't "fill up" the vast areas of sparse population if you tried. The opposite is in fact happening. More and more people are moving to cities and agriculture/forestry is getting more and more efficient.

"while the ratio of arable land per unit of crop production shows improved efficiency of land use, the number of hectares of cropland has scarcely changed since 1990. Absent the 3.4 percent of arable land devoted to energy crops (Trostle 2008), absolute declines would have begun during the last decade."

So if it wasn't for the bleeding heart greens and their bio fuels gravy train total arable land would have begun declining a decade ago. How ironic.

I don't want to live in a crappy over used world and not sure where I said such. Check out the article Nature Rebounds linked above.

https://phe.rockefeller.edu/docs/PDR.SUPP%20Final%20Paper.pdf

Profile - i imagine the debate to appoint Nick Smith ahead of you as Environment Minister must have gone into the small hours ... yes all is well

https://xkcd.com/1338/

http://www.worldometers.info/

http://www.truth-out.org/news/item/39197-monsanto-epa-seek-to-keep-talk…

http://rinf.com/alt-news/editorials/british-government-colluded-monsant…

http://europe.newsweek.com/glyphosate-now-most-used-agricultural-chemic…

Just looking for your own feeling on this question, but how many forests, how many other species are you prepared to see go by the wayside for our ever increasing population? How would you see a world minus some, maybe all of our enigmatic, majestic creatures. We are not the only earth inhabitants and every species we see off makes ours a bit poorer.

David,

You seem to be arguing that the world does not have a population problem,simply on the grounds of land area and that seems to me to be incredibly simplistic.There is the obvious fact that you cannot spread the population like butter on a piece of toast. Countries like Bangladesh and Pakistan will continue to become increasingly overcrowded,while Japan goes in the opposite direction. More importantly,you ignore the problem of resources-food,water,energy,etc to adequately cater for a population of 9/10bn.

I think Australia will experience significant resource issues as its population grows to around 35 million,almost all based in just a few cities and climate change will massively exacerbate these issues.

A truly excellent article. Usually if there is one interesting and stimulating idea in an article it is a win, and this had at least half a dozen.

In terms of population size, 7 billion is not big if we all sit around eating soy curd and live like termites but lets face it, that's not going to happen. As incomes grow (if they do), people will want to eat more exotic things, travel to more exotic places, and buy the latest status symbol. And other people will try to top those people and post it to Facebook. We have had major environmental problems in the run up to 7 bn, so god knows what it will be like when we get to 9bn.

We might as well put up a space elevator and leave the planet.

Hopefully the menu will be more palatable than that.

The world can certainly feed more than the current population, the projected 11 billion peak should also not be a problem. Ag science and Ag Tech already enable far higher production levels with less energy and land use than even a year ago.

Frankly, I will keep my faith in people like David Attenborough who have first hand experience of what we have done to the planet from the ground up. All you have to do is look at Madagascar and you do not have to go far back to see what we can do in a very short time. Turn back the clock and look here, even, but you would have thought by the time Madagascar was being razed to the ground we might have known a bit better, and it is still going on in Indonesia etc.

We are seeing growing clashes with people and wildlife in Africa and yet Profile himself has stated this is where much of population pressure will come from, oh but that's ok, we will reach 11 billion and then we will lose interest in sex or something.

We are now on the cusp of another very hard push into the environment for extractive industries, etc. I have this gnawing feeling that those who want to go hard exploiting the environment are gathering strength and I am predicting a new wave of environmental damage facing us. Is it a coincidence that these same people are the ones who seem to have issues with birth control, mainly for religious reasons?

Can anyone please explain what point there is in the human race reaching such proportions that we have to eat fake food and live in apartments many storeys up in order to fit us all in?

Not only living like termites but probably eating them as well

Great article.

It explains:

- whatever boomers suffered, boomers caused (I had a chuckle at that one)

- Interest rates

- Brexit

- Trump

- NZ immigration policy

- Why WP is so popular, and gaining

But it also spells out that we will keep being in demand, hence immigration will keep going up, unless there's a change in policy to slow down immigration growth to sustainable levels.

if not, this will keep adding pressure on houses and infrastructure, and our precious environment.

.

Hm.

Might start looking at property in Alaska.

What? With a place like Takaka in your backyard? :-). All it needs is a base hospital specialising in eldercare type health interventions - and hey presto - Tauranga II.

No offense to the soon-to-be-massive lot of retiring BBers, but I think we need to start thinking about luring them and their cash out of the main centres.

yup, top of south island appeals, too (right now, and for the next 15 years), but I was referring to NZ and AUS being part of the 'hottest clubs on the planet', so overall population will keep climbing unless we put the brakes on a little.

.

I'm just the right side of misanthropic, and I value the wide open spaces of NZ. If this get compromised, I'd like a bolthole in another empty territory with lots of forests and mountains.

What cashed up granny wouldn't move?

From this:

http://www.realestate.co.nz/2996577

To this

http://www.realestate.co.nz/2973509

Provided the hip can be treated locally and the grandkids can afford to visit during the school hols?

Can Granny be bothered with a woodburner and 4.5 hectares to look after?

I would, ideal size, and nothing like a woodburner to keep you warm when there's a power cut.

.

but then I'm not of granny-age. Yet.

I can think of a few reasons why not.

If it was so good, I have a feeling there would be a lot more oldies doing it.

That property in Takaka is too low. Wouldn't buy sea-level property (by the sea) anymore. Height is good. Access to your own fresh water would be even better

.

Possibly need a Toy Boy to do the manual labour...and drive her to the supermarket to hump the groceries....cannot be all bad.

Put up a Granny Flat too and house the bairns.....as they cannot afford to compete with the influx of certain Nationalities, that shall be nameless.

They they can inherit the lot, one day.. not lose the plot, when all is said...and done.

And all with no Mortgage...to bovver abaht....Sweet.

Clean air, clean living, no sweat equity....nah Problemo. Family living....as it used to be.

The end of two world wars spurred the greatest boom in human history.

Hmmmmm....

Instead, it would be more consistent that the global economy was positively “shocked” not by the spending actions to take out global conflagration but the re-imposition at long last of (more) honest monetary conditions. Bretton Woods took place in 1944, but will always be ignored by economists like Krugman and Summers because honest money is anathema to Economists who wish to be able to disrupt at their whim. Equating and soundly defining global monetary terms, for however brief (just 16 years), is a legitimate candidate for explaining in Krugman’s S-curve how the global economy skipped from the hugely costly equilibrium in depression to the utterly positive robust growth equilibrium that brought us, in good part, the Baby Boomers. Read more

The effective cancellation of all internal and external debt in Germany and Japan worked wonders.

If natural interest rates are low, with money freely available due to sustained demographic trends - there can never be justification for bailing out any bank.

The bailing out of the banks in the GFC was a complete waste of time and expenditure. There was never any chance of persistent financial instability, because the natural interest rates are so low. Bush/Obama could have saved the American taxpayer $trillions by letting Lehmann like collapses occur over and over. The end result would have been exactly the same.

Reading through this diatribe, the conclusion is the baby boomers needs a constant supply of young immigrants to fill their rentals and provide them with passive income, given growth is dead. Otherwise the (population) Ponzi scheme falls apart.

Im curious as to what these immigrants will actually do for a crust?

They run takeaways and bakeries for the growing numbers of immigrants, but seriously, have you seen one new business in some of these new areas being operated by someone who is clearly not an immigrant.

a perpetual motion machine - brilliant!

Hear, hear. This article also confirms my conclusion that our economy is simply a population ponzi scheme. I really think we need to press the reset button soon and reformat with a new OS.

Great analysis, many thanks

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.