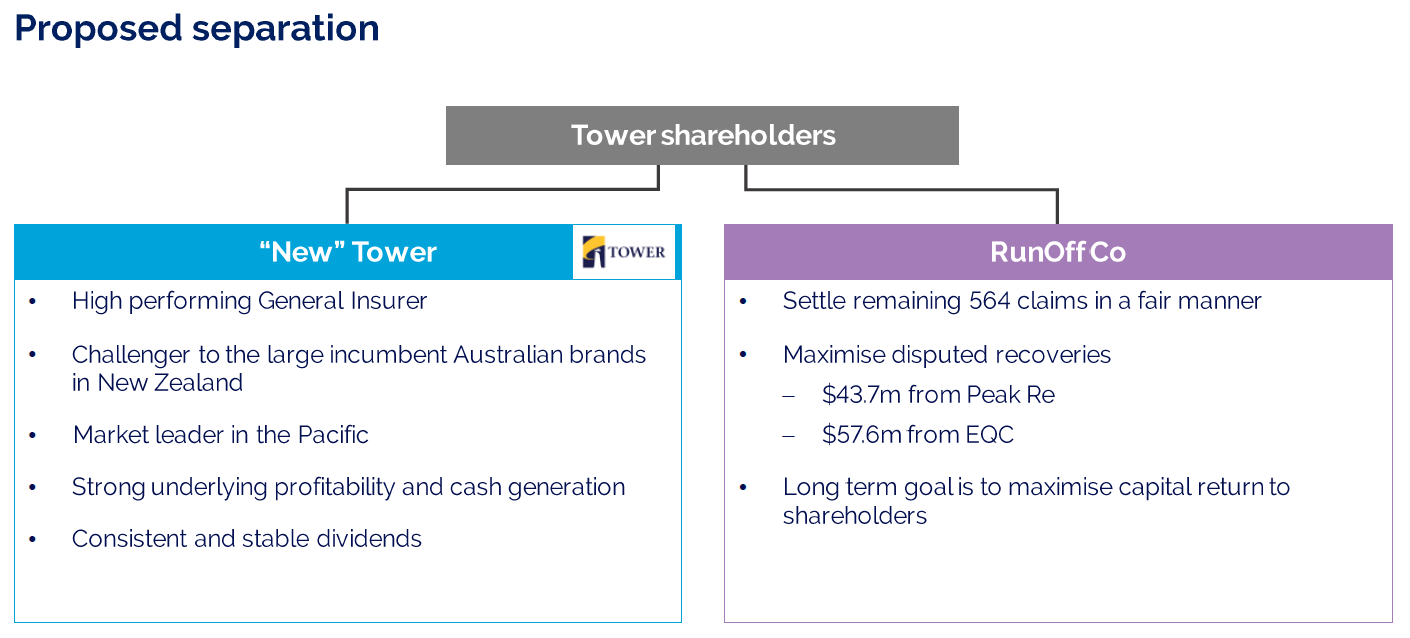

Tower is planning to ring-fence the part of its business still grappling with 2010/11 Canterbury earthquake claims, by forming a new company.

The insurer has announced its intention in its annual results for the year to September 30, released to the NZX on Tuesday morning.

Tower chairman Michael Stiassny says the legacy of the Canterbury earthquakes continues to overshadow the rest of the business, so the Board wants to create a separate company, RunOff Co.

“In our view, the industry model is broken with claims inflation continuing unabated, construction far slower than anticipated and little effective co-ordination between the EQC and insurers," Stiassny says.

“These are all symptoms of a system that can no longer do right by the people, communities or insurers it is supposed to serve.”

Loss creep and litigation

Stiassny says claims over EQC’s $100,000 cap are continuing to flow through to the insurer at a pace.

At the beginning of the financial year, Tower had 703 property claims remaining. By the end of the financial year, it had closed 534 of these claims. But in the interim, it received 297 completely new claims worth $22 million, and had to reopen 98 claims.

Furthermore, “An entire litigation industry has sprung up to agitate disenfranchised customers to demand not just fair resolution, but a windfall,” Stiassny says.

Tower is currently facing, or expecting litigation on up to 100 claims.

Over the course of the financial year, this loss creep and litigation has seen Tower’s gross claims costs increase by $78 million to reach $870 million.

This has had a net impact of $25.3 million after tax, which has largely contributed to Tower widening its loss to $21.5 million in the 2016 financial year, from $6.6 million in 2015.

Drawing a line under Canterbury

“We have therefore resolved to draw a line under the Canterbury legacy to benefit both policyholders and shareholders’ interest, enhance the prospects of our strong underlying business and enable Tower to accelerate its journey to become a high performing general insurer,” Stiassny says.

“Separation will enable the market to more transparently value Tower. The component parts - RunOff Co and New Tower - are undoubtedly worth more than the whole. Separation provides a vehicle to unlock that value.”

Both entities will be separately managed, with RunOff’s two objectives being to settle the remaining 564 Canterbury claims and recoup its “disputed recoveries”.

Tower claims one of its reinsurers, Peak Re, owes it $47.5 million, while EQC owes it $57.6 million. Securing these recoveries are vital.

Stiassny says the Board has “begun recovery action” and “will not resile from litigation, should it prove necessary to recoup what is rightfully owed to Tower shareholders.

“The successful resolution of these disputes will support capital returns for RunOff shareholders in the longer term,” Stiassny says.

‘Stakes are high’

He acknowledges the “stakes are high”, but believes the separation will enable New Tower to take on its Australian competitors that dominate the New Zealand market – namely IAG and Vero.

Tower has had preliminary discussions with the Reserve Bank about the separation.

“They have consented to the creation of two separate licensed entities subject to licensing criteria being satisfied,” Stiassny says.

Tower will also need approval from its shareholders. It hopes to present them with a proposal in March.

Tower’s full year dividend will be suspended as the Board is “evaluating a number of potential sources for capital - including strategic sources”.

‘Canary in the coal mine’

Speaking to investors in a conference call, both Stiassny and Tower’s chief executive Richard Harding point out Tower isn’t the only insurer that’s had to increase its quake claims provisions.

The likes of IAG, Southern Response and MAS have had to do the same.

“Unfortunately, as the only listed, pure New Zealand general insurer, it is most visible with us. In some respects, we are the canary in the coalmine,” Harding says.

“Six years on [from the Canterbury quakes], insurers like ourselves still do not have clarity on the number and value of claims that remain,” Stiassny says.

“We’re not the only ones concerned that the system is broken.”

Referencing an interest.co.nz interview, he says: “The world’s second largest reinsurer, Swiss Re, has fired a shot across the Government’s bow, pointing out how vulnerable the New Zealand economy is to the risk of reinsurers increasing premiums due to the uncertainty caused by the delayed EQC Act review.

“[Swiss Re] urged the Government to get on with the review to provide certainty to insurers and reinsurers alike. In turn, we want to provide certainty to our customers…

“Concluding this review and sorting out the EQC is critical if New Zealand homes are to remain cost-effectively insurable.

“In the wake of the Kaikoura earthquake... [this is] even more critical. The Prime Minister has signalled the Government is wanting to take a different approach to the Kaikoura recovery and we support this entirely.”

While the insurance industry has been calling for the Act to be amended in such a way that private insurers rather the EQC is a claimant’s first point of contact after a natural disaster, the Minister Responsible for the Earthquake Commission Gerry Brownlee has shot this idea down.

A bill for the review is expected to be introduced to parliament next year.

Kaikoura expected to reduce Tower’s solvency capital by $13 million

Tower has a solvency ratio of 214% and excess capital of $14.3 million above regulatory requirements. At a Group level, is has excess capital of $23.8 million.

It also has $12.2 million of cash that can be used for solvency capital if required, and has access to a $50 million undrawn liquidity facility.

Yet the Kaikoura quakes are expected to put a dent in its solvency capital.

Tower reports: “Tower’s reinsurance programme is expected to limit the impact of the Kaikoura earthquake to a $13 million reduction in solvency capital.

“Adjusting for this and other operational movements, as at 28 November, Tower Insurance Limited is expected to have $3.6 million of capital above regulatory minimums, and Tower Insurance Group would have $16.0 million...”

Looking at the insurer more broadly, its gross written premium is down 0.8% to $303.2 million, while its underlying profit after tax is down 33.6% to $20.1 million.

Its claims ratio – the amount it pays in claims as a proportion of the amount it receives is premiums – is up from 47.7% to 50.3%.

By late Tuesday afternoon Tower’s share price had fallen to 70.5 cents, a drop of 4% from 75c on Monday. It has plummeted about 60% over the year and is at a record low.

For background, see these stories interest.co.nz has written on Tower in recent months.

47 Comments

mmmm i wish i could do this... keep my cheque account and form a separate entity for my credit card bill, then in a few months ask the govt to bail me out.

Seems to be where they are heading. AMI, now Tower. The Taxpayer will soon be the default insurer.

Ah yes .so he's totally wrong, the industry model is just perfect. You know how it goes, Privatise the profits........

"In our view, the industry model is broken"

Yes, the industry model is broken. Insurance was never going to work long-term, when the insurable assets in the world are worth more than all the money ever seen in existence.

You think property prices are expensive, try rebuilding House, Driveway, Retaining, contents, etc.... What would the value of Wellington be? Let alone Auckland? Hundreds of Billions of dollars. The whole NZ industry would be bankrupt.

Now Imagine, New York? London? Tokyo? A large earthquake in Tokyo and you could well see a Trillion dollars in claims. It would be the end of the global insurance market.

Yes he has admitted that their focus on profits is the wrong stance and they need to change. The problem is they won't change it to the way it needs to be to operate properly as Insurance is supposed to.

of course it's broken. Insurance is a scam, we pay taxes we get things from the govt. If an earthquake happens in Kaikoura I'm happy for my taxes to pay for the rebuild. That's why we are a nation, not a consumer association. easy for the insurers to say the system is broken, when things go wrong

Agree, looking at all the Government is covering from Chch and now Kaikoura, it makes sense to have them provide Universal insurance.

Add a bit to the rates to cover property/buildings.

Add to the rego to cover vechiles/3rd party.

Business continuity, could be done via a corporate tax increase, or as it is now just pulled from the tax pool in general.

The rest of the stuff can stay private.

- Healthcare is technically free, so leave that as is if people want extras.

- Travel insurance (although repatriation of a citizen (or their body) could be socialised via general taxes)

- Contents

- Life insurance

..Obviously you are unfamiliar with the notion of moral hazard and why we have non standardised premiums in the insurance market.

What you suggest is definitely not a solution.

I am familiar with moral hazard. It was an idea rather than a solution.

However given we (The taxpayer) have already bailed out AMI, and are also providing business continuity (emegency funding) to Chch, Kaikoura, and Wellington, I fail to see how we aren't already doing this.

At least my idea above would formalize the arrangement.

At the risk of coming across as pedantic, natural disaster catastrophes are different to 'moral hazards' - the latter are confined to human behavioural elements. Geographic rating differentials across the country for natural perils such as flood, earthquake etc are not by definition moral hazard based.

How so? Home owners build on flood plains as the land is cheaper and they know that they are covered when the rain comes. No premium on insurance for living there provided by the govt guarantee to guard against them doing so. I would have thought its all the same moral hazard idea?

they shouldn't be allowed to build there.

I don't think a Natural Disaster excludes moral hazard.

- I should build a structure in line with the regulations,

- it should be well built,

- It should use suitable materials,

- it should be in a suitable location.

- it should be a suitable design,

- it should be suitably maintained

On Tokyo Noncents, they had a magnitude 9 earthquake in March 2011. They have significantly lower levels of insurance in Japan than New Zealand has, ie a lower percentage of the population is insured. Also the buildings in Tokyo are better at standing up to earthquakes. My friend who lived there in 2011 was on the 25th floor of a building when the quake struck. He didn't leave it and both he and the building survived intact.

Agree with the standards, and insurance levels etc..

However the Earthquake itself was over 350 kms away from Tokyo. To put it into perspective the recent Kaikoura quake is less than half that distance to Wellington.

Had it hit closer to Tokyo I imagine it would have been an entirely different story for your friend and his building.

Even then, the 2011 Japanese quake (with little to no damage to Tokyo itself) is the single highest insurance even in History at over $250bn USD.

Wasn't it also one of the biggest quakes ever recorded, at over 9. Also they had tsunami damage and a nuke power plant that would have costs billions to manage. We are just lucky we didn't go down the nuclear route, because it would destroy NZs economy and tourism and farming if it had a meltdown..

Yeah, I think third or fourth biggest ever. The Tsunami did most of the damage.

That's kind of my point though. Large disasters do happen, it is really just luck where and when.

A big disaster in the right place and the whole Global insurance industry would be toast. Imagine a tsunami on the East cost of the USA or a similar earthquake centered near Tokyo, Rome, or San Francisco.

I agree with your nuclear power statement. Given the geology of NZ it would be a disaster just waiting to happen.

Taken wider, the economic system was never going to work long-term... growing obligations are collapsing the system ...

"Debt is the thing that keeps pulling the economy forward.

There are a huge number of obligations that keep growing over time:

–Obligation to pay the elderly their pensions and health care costs

–Obligation to keep repairing electricity transmission lines; water and sewer pipelines; oil and gas pipelines; roads and bridges. If we don’t keep repairing these, we cannot keep civilization together.

–Cost of extracting oil, coal, natural gas, metals, fresh water, because of rising diminishing returns

–World population, because we have not yet figured out how to keep population level

–Repayment of debt with interest

Growing debt is what keeps the economy going, hopefully fast enough so that the “real economy”,(that is, the total economy net of all of the required subtractions, outlined above) can more or less keep growing, or at least give some kind of living to the people on earth. What tends to happen is that the people at the bottom of the employment hierarchy get “frozen out” first. We keep needing a more complex economy.

The economy collapses from low prices, because a large share of workers (and would-be workers) cannot afford the output of the economy."

"the insurable values of the whole world are worth more than all the money in the world" Yes indeed. But the assets don't all fall down at the same time. One in a thousand local houses burn down say. Which is why we all pay insurance - a contribution we don't expect to get back. But if necessary we get a lot back.

Entire cities fall down only occasionally. But the vast majority don't. Which is what internationally based reinsurance is for.

All our local companies need to charge enough to cover local mishaps. And reinsure enough to cover the disasters. And they should be required to by law. While that may end up giving us all larger premiums - it will give us cover. And the likes of Tower can't weedle out and pass the problem to the taxpayer.

That would work, given enough good law.

"But the assets don't all fall down at the same time."

That was the logic that got them into trouble in the first place. Recent global Natural disasters have proven that is not the case.

Take 2011, the three biggest global insurance claims in history. Japan (Earthquake/Tsunami), Thailand (Floods) and Christchurch (Earthquake). That was one year. Re-insurers upped their rates across the world, and I think it was Lloyds acknowledged then that maybe their models needed to be adjusted.

Looking at the costs, Chch doubled my insurance costs and I live in New Plymouth. The actual (realistic) cost of adequate premiums etc... would probably be double again, if not more - After all we are more prone to large scale disasters than many other places on Earth.

Do you really believe the average citizen could afford that sort of jump in insurance? I know I couldn't

Other option, is insurers reduce what they cover. Natural Disasters will be out.

So if they aren't covered, then like it or not, you would be forced into Govt (Taxpayer) coverage for Natural Disasters - We have had 2 major quakes in 5 years, can the taxpayer handle an extra $10bln or so a year to cover them?

Did you just contend that all the cities in the world were wiped out at the same time. ???

You list three in 2011. Can you just not think of more than that who had no problem.

I'm confused by what you mean exactly.

I am not saying all cities at once are going to be hit.

What I am saying is that 2011 had the three biggest insurance events in history. A combined cost of over $350bln USD in one year. Yet none of those events were in a major city, with a large insurable base.

As an example to scale it up. Without being insensitive - 9/11 was approx $40bln USD in insurance. That covered 3,000 lives across a few city blocks + some aircraft.

Now imagine that instead of Sendai, North/Central Thailand, and Christchurch being impacted by the disasters. It was Tokyo, Bangkok City, and Auckland. I.e. Hundreds of thousands of lives across entire cities.

The costs would be astronomical.

My point is that insurance is geared towards singular losses, i.e. my house burns down, or my car is stolen.

It simply cannot function at a citywide/national level after a Natural Disaster. The losses are simply too big.

This looks suspiciously like the Canterbury obligations are in financial trouble so best to start up a separate entity which can eventually go bust and leave claimants stranded. Nice one

So the only logical conclusion would be for all those nasty , near fraudulent, windfall claimants remaining to file proceedings ASAP. Otherwise they may find themselves stymied by the statute of limitations and/or filing against at an empty shell company into which their claims have been transferred. Get onto it while you still can!

Has it been confirmed that the re-insurance from Peak-re is going to be paid. If not that is just a pie in the sky as far as funding being available. If Tower are telling the truth as having 96% of the CHCH EQ's settled then why all this drama for the remaining 4%. Perhaps Tower are not good at telling the truth? That at least explains the high degree of distrust out there by the majority of Tower's claimants. This new financial structure means nothing. At the end of the day a balance sheet is a balance sheet. Oh yes, AMI had one like this too.

Classic good/bad business book separation, pending sale.

Towers resolution manager for most of the earthquake period recently moved on, now working for Vero.

RING FENCE......Isn't that the same tactic some of our now defunct FINANCE Companies tried !.

How did they work out?

Ummm,, really really well for the owners actually.

564 claims divided by $101m means $180k each for presumably the hardest to resolve claims. Is that enough. Plus minus admin costs over time as I presume the entity has no cash coming in.

The CFO did those sort of calculations, as too did the financial guru board member . Both have jumped ship.

$180K per claim is unlikely to cover their consultant and legal fees, let alone fix the damage

Central Response.

You have to give it to them for gall. Effectively encapsulating their Chernobylesque liabilities into a concrete tomb of a special purpose company ... that purpose being default, phoenix company, and to force the hand of the government (muggins taxpayer, here).

How can this possibly be permitted? Bus tickets are being dampened as we write.

It's time to let market forces prevail and clean out the stock holders. This one's a dog, and it needs putting out of its misery.

Doesn't the government have a precedent setting responsibility problem here?

It bailed out AMI who were in immediate difficulties (insolvent) in aftermath of the CHCH quakes

Meanwhile, Tower appear to have been OK at the time, but are getting blindsided and Trojan-horsed by EQC who are dragging the chain and getting revised over-cap claims that are being transferred back to Tower. Meanwhile repair costs have escalated ... what? ... 40% in 6 years ... on top of escalation in claims ... EQC seem to be the cause of some of, if not most of Towers problems

A mere triviality ... Tower were once known in another life as Government Life Insurance

The reality is Tower as well as others were very happy and complicit in leaving claims to rot in the EQC pot. It suited their cashflow & who knows some of them may never have come out again. In fact if Tower had fulfilled their responsibilities to their clients with true and proper assessments all these claims would not now be re-emerging to bite them at a cost hugely inflated from what it would have been at the outset.

We'll have to disagree that Tower was "OK". Tower evidently was not sufficiently reinsured. They have been in obvious difficulty for some time, managing to drag out their survival a little longer than AMI. Regardless of fault, businesses go broke due to bad luck all the time. We can't bail everyone out.

The shareholders and board must be held accountable in the most public financial sense. Moral hazard is getting out of hand and shareholders must be put on notice that investments in careless businesses will not be bailed out. Perhaps then shareholders and boards will pay more heed to the fundamentals.

You mentioned the problem of precedent. That is a serious problem indeed. If we continue down this path, we may find every NZ property investor with their hands out when the inevitable occurs.

The government may need to put together a package to assist Tower's remaining claimants, but that is another matter.

Toxic business must be allowed to fail.

Yes the remaining claimants, that's the rub. The Tower chairman implies that these are windfall claims. Suggest he refamiliarise himself with what his policy actually says & while at it go through too, the Skyward decision which Tower lost in the Supreme Court.

"Long term goal is to maximise capital return to shareholders."

It would be hilarious if it wasn't so grim for Joe Taxpayer.

Receivers. NOW.

It looks like the current system is broken. Maybe we need to setup a government insurance company again. Although that is more likely to happen under G-Labour than National.

Unless Tower has cut a deal with EQC, the $57.6m they claim to be owed may not be the confirmed asset Stiassny seems to imply.

It probably mostly arises from differences of view between Tower and EQC about how much each of them was liable for, in respect of each event. It may also include anticipated recoveries from EQC for land repairs where Tower was forced to carry these out to get rebuilds going, while waiting for EQCs land settlement team to do its thing.

Without more detail or confirmation from EQC that they do indeed owe this amount to Tower, it is impossible to judge how solid the recovery prospects for this $57.6m are.

Fair comment. So if the Peak-re & EQC anticipated contributions are the only assets for Run-off Ltd, what else possibly could there be anyway, that is at the least the mostly dodgy capitalisation of any company since Equiticorp. Run-off Ltd?! Tom Tom the Pipers Son, indeed!

Ha - you are drawing a very long bow indeed comparing Tower with Equity Corp. I think even the Hawk might not go that far!

Don't agree Towers capitalisation was 'dodgy'. They had to meet the same prudential capital adequacy ratio requirements as all insurers. 20/20 hindsighters will no doubt insist Tower fully understood the exposures in CHCH but took the punt and went short on their reinsurance anyway.

Reality is all insurers were blindsided by issues that could never have been anticipated although you'll never persuade shiny eyed idealists and conspiracy theorists of that.

But are we convinced that the recent insurer recapitalisation strategies, really are entirely due to sudden and unexpected increases in claims costs? With such high resolution percentages, it is a struggle to understand why the cost escalation is so severe at this very late stage.

One trusts the capital bolstering strategies are not instead to bridge the gap between previous erroneous reporting and the present requirement to actually pay the bills. Hopefully the story that they are due to genuine contingency cost increases not known about back then, is true.

Concede Equiticorp was a bit of a dredge. Feltex would have been more apt. Yes with 96% claims supposedly done & dusted it is an odd venture of unexplained circumstances for the remainder. That in its own right is downright dodgy.

What else would you expect from Nasty Stiasnny. Recall he is Korda Mentha so will be waiting in the wings to pickup the liquidation, but how about some accountability from the Regulator, ex CEO,CFO and Director who probably exited with bonuses - reapyment and perhaps some jail time is suitable.

Lol insurance boss says clients suing for windfall profits!

I bet if you ask each of those policy holders they'd say they had to sue to get what was righfully theirs because the bastard insurance company has been holding out on paying them what they rightly owe for 6 years now.

I see elsewhere its stated that they need to have a license to operate but have been given tacit approval from the RB.

I note they don't say how long the company will operate for. Even a two or three year time frame will mean Eight to nine years of waiting for some. And what sort of staff are going to work there for such a limited company? Highly paid ones I'd guess.

So much for the obvious questions the Peak Re and EQC issues raise, but no mention of how the liabilities transferred into RunOff Co are to be valued?

The actuarial profession haven’t covered themselves in glory predicting the ultimate cost of the Canterbury earthquakes. Actuaries are only as good as the people providing them with the information. They’ll say there are always limitations in interpreting data, especially translating into future performance. Of course, the greater the predicted v actual variation, the greater margin for error they add. But there are limits to that process, as well.

The way Tower are conducting their visible claims smacks of a head in the sand approach to ultimate cost. It is an obvious contributor to the constant increase in reserves. The EQC process is not the only cause. Deck chairs are also being shuffled with their previous CEO gone, their CFO having recently ‘resigned’, and Tower in the market for a new executive bench.

It would be a very brave actuary to put a number on the ultimate cost of claims transferred to RunOff Co. The auditor would likely only go as far as supporting the process rigour, not the conclusions.

The last notable time this valuation risk was highlighted was in the early 2000s with James Hardie and their self-insured workers compensation asbestosis liabilities. Not long after (in actuarial terms) the Board, having originally promised shareholders that the provisions were more than adequate, the amount had multiplied by a big number. The directors and CEO went through years of court action for having breached ASX requirements and misleading shareholders. In the end the CFO took the fall.

The liabilities in this example stayed on their balance sheet.

With Tower, NZX, the Reserve Bank and the Commerce Commission should be looking closely at this financial sleight of hand and the implied transfer of risk from shareholder to policyholder. GIven the high degree of difficulty in accurately valuing earthquake liabilities, I’d be favouring a regulatory approach that allowed those liabilities to crystalise within the existing Tower structure. If not, policyholders will be left between a rock and a hard place, i.e. negotiate now for, say, 0.80c in the dollar, or risk being left with 0.30c – 0.40c as RunOff Co plays hardball and the money is used up.

Watch this space……

Vague as it may be it would seen the liabilities for transfer to Run-off are calculated at about $140mill, at least as a starting point. So to cover that there is $40 mill or so existing re-insurance & then to come $44 & $57 mills from Peak-re & EQC!!?? As others have highlighted that averages say $180kK per outstanding claim and then there is all the outgo, staff,experts lawyers. Excuse the cliche but it is a lead balloon. The only way claimants can protect themselves is to file their claim in the high court now while the present Tower still exists. Like any other company in NZ listed or unlisted, Tower cannot form a seperate company so as to be able to isolate and bury legal proceeding in a worthless shell company. If claimants file now then they will be filing against all the existing assets of Tower.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.