The RBNZ has stopped updating its total mortgage lending data monthly (C5), moving to a quarterly series instead.

But is has introduced something more valuable in its place - monthly data on new mortgage lending (C32).

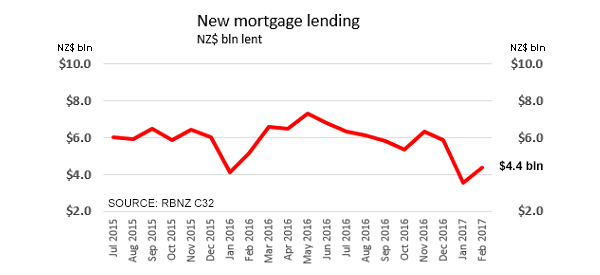

And the latest release shows that new mortgage lending is falling. It is down -15.2% in February from the same month a year ago. And in the twelve months to Febraury, $70.2 bln in new mortgages were granted, the lowest level since this new series began in July 2016.

New regulatory constraints and soft real estate market demand has put a lid of mortgage demand.

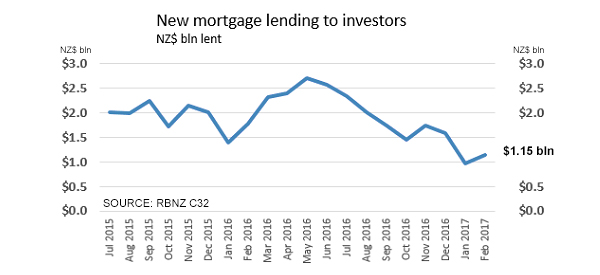

The $4.4 bln in February may be -15% lower than the same month a year ago, but lending to investors is actually -35% lower in the same period.

Banks are rejecting many more investor lending applications.

And interest-only lending, favoured by investors, is down by a sharp -27%. That is a shortfall of -$540 mln. And that is part of an overall -$787 mln.

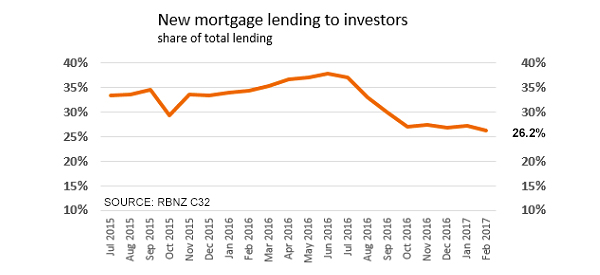

Quelling unsophisticated investor demand is a core element of controlling an irrational housing market. Property investing spuiking companies pop up to harvest the money of unsuspecting 'investors' and they bring irrationality to housing markets, often crowding out buyers who just need their own dwellings.

February 2017 has seen the lowest level of investor lending since this series began in July 2015 and probably for a lot longer.

The clamps are on investor lending and they are likely to stay on for some time yet.

With falling median prices, and more importantly falling lower quartile prices, first home buyer affordability is improving. In fact almost all of New Zealand except Auckland and Queenstown is affordable for first home buyer households.

Regulatory changes have helped this improvement.

While some may argue that Chinese capital controls also are having an effect, it seems unlikely that demand from this source is active, or has ever been active, in the first home buyer market in the same way RBNZ regulation has been,

If only RBNZ regulation could fix Auckland's housing shortage. Only Auckland Council can do that and there seems to be little real action on that front.

64 Comments

26.2% of new mortgages to "investors" is still high in my books. What do they expect? Capital gains or something?

Central government could also play their part in fixing Auckland's housing shortage / migration oversupply. Not much real action there either.

I'm curious based on what is the impact of Chinese capital being downplayed?

Basically because the most honest thing they've ever said is "We don't want to see house prices come down".

Therefore, you know outright they're prepared to sacrifice the home ownership prospects of whole generations of New Zealanders.

Not happy. Vote for change.

They should never have allowed them to rise so much, if they don't want to see them come down. If they do drop in value by quite a bit, then it causes financial stress for the borrowers and banks. But that is their risk. It seems that NZ as a whole has had to take the risk. Savers are the worst affected due to the low interest rates, and no deposit guarantee scheme.

House prices are unsustainably high, because interest rates are unsustainably low. Plus add on excessly high building and compliance costs, high migration creating high demand, and overseas investors.

'Investors' and real estate agents buy up real estate ,using existing property as collateral and interest only loans acquired thru 'reputable mortgage brokers', speculating on higher prices, forcing out FHB, reducing home ownership rates, and making it 'unaffordable ' for FHB to purchase, and the claim is always made that Auckland has a housing shortage. Will there be a housing shortage as prices fall.

It's the proportion of interest only loans that really troubles me. I would be very happy for that percentage to drop through the floor.

"If only RBNZ regulation could fix Auckland's housing shortage. "

hmmm.....as of this morning, ‘Auckland City’ area on trade me had 2493 properties listed. Same day last year they had 1630 listed. So that’s a whopping +53% surge of additional stock for sale.

It looks like the "shortage" is fixing itself at the moment.

useful statistic. I notice the total properties for sale in the region has grown from less than 10,000 six weeks ago to over 11,100 at the moment.

Housing in NZ is not unaffordable at all!

Get over the fact that Auckland is not the only place worth living in Nz.

You can still buy property in Christchurch that is cheaper than renting, and jobs are obtainable.

I have travelled a fair bit and can assure you that it is an extremely liveable city compared to,other major cities worldwide.

But really...I'm not sure that "just cede Auckland to foreign buyers and live somewhere else" is necessarily the best solution overall. What happens when Christchurch becomes the next best thing - all the young Kiwis should shift out too?

True, housing is unaffordable in Auckland but very affordable in most other places

What's your definition of "affordable," Yvil?

Up to 5 x average household income

I love it how you've increased the threshold of what's historically regarded as 'affordable'. Why don't you just make 'affordable' mean 10x average income, that way you could solve the 'housing crisis'.

My mortgage in UK was 3.5 times. Seems a sensible number to me and I could live within my means, even with a change in interest rates. Still tough, but 5 times would have gotten me a better house, but I would have struggled and if interest rates rose I would have been stuffed.

So I think 3.5 times.

Jobs are obtainable as people leave the city and situations become vacant. Rent rather than buy as houses in Chrstchurch are becoming cheaper by the month. Rents are also dropping. I do not know when Christchurch will bottom price wise but as interest rates rise houses there will get cheaper .

Gordon, jobs are obtainable if you are prepared to get off your butt.

Population in Chch is increasing Gordon, unless you have got the figures that you have never produced to validate your claims.

Rents have dropped a wee bit but interest rates have also dropped to what they were also.

Interest rates aren't going anywhere anytime soon.

Even if things do drop in value the standard of living in Chch far exceeds Auckland.

Things couldn't look much brighter Gordon, but you are better off staying where you are as we don't need negative people in Chch.

Gordon, jobs are obtainable if you are prepared to get off your butt.

Population in Chch is increasing Gordon, unless you have got the figures that you have never produced to validate your claims.

Rents have dropped a wee bit but interest rates have also dropped to what they were also.

Interest rates aren't going anywhere anytime soon.

Even if things do drop in value the standard of living in Chch far exceeds Auckland.

Things couldn't look much brighter Gordon, but you are better off staying where you are as we don't need negative people in Chch.

Things must be brighter for people down there as rents and house prices drop The Boy. I would not come down there because of the weather ,smog and quakes and the desolation. We had a small quake overnight and I did not enjoy the experience. I can see why so many people are leaving when you constantly experience them.

Have to say your experience is quite different to mine. Lots of benefits to living in Chch, great city, lots going on, great location for bike trails, mountains, tramping, rivers, nice stable house prices and falling rents. Weather is great, generally nice and dry which I like.

Smog hasn't been an issue in the few years I've lived here, I believe the earthquake repairs took the opportunity to replace a whole load of old fires with clean ones or heat pumps. Cold isn't an issue if you just put on an extra layer. If you're that worried by quakes then probably NZ as a whole isn't the country for you.

My field tends to do a lot of recruitment from overseas, and I can tell you Christchurch finds it much easier to attract people than Wellington, Auckland, Hamilton or Dunedin.

TM2 - do you have a (real) job? Or are you a full time 'property manager'?

"Jobs are obtainable if you are prepared to get off your butt." I've been job-hunting for seven months, and I've found maybe six or seven jobs in my field (GIS) in Christchurch in that time. That same amount is listed every 2 weeks in Auckland and Wellington.

I hope you have a contingency plan for when Christchurch has another earthquake and multiple houses of yours are uninhabitable or need repairs. Also, if Christchurch's population is growing then why are rents and house prices falling and the amount of houses for sale increasing? Surely more people in a region equals more competition which equals higher house prices and rents? E.g. Auckland and Wellington.

Well, the population is increasing according to the data I can see (for example https://www.ccc.govt.nz/culture-and-community/statistics-and-facts/fact… will show you a nice graph if you click on Current Population), although it may just be recovering the population lost after the earthquake.

Given the amount of new house building and repairs done over the last few years, there's no inconsistency in having a growing population and stable/falling prices and rents, the supply is increasing at least as fast as the population and the post-quake rent spike is deflating.

Absolutely agree that The Man should be diversifying both in terms of asset class and geography, but arguing this with him seems to be a lost cause. Perhaps he's happy with the inherent risks, or perhaps he's unable to see them.

Interesting. The StatsNZ site says the Christchurch population fell by 2% between 2006 and 2013. It's still hardly growing as the population isn't even back up to pre 2010 levels.

Chch growing at 2%, according to Stats NZ. But Selwyn growing at a whopping 6% as the city moves west outside of the current CCC borders.

http://www.stats.govt.nz/browse_for_stats/population/estimates_and_proj…

And you often find that those who say "Jobs are obtainable if you are prepared to get off your butt" left high school and were hired straight away by a company that then trained them for their new job.

On the other hand, any boomer who has hit unemployment in their 50s or 60s will have quite a different assessment of how easy it is to get another job.

Or where your field of expertise just doesn't exist there. There are 0 opportunities there in mine, and quite a few in Auckland.

Two things in this article. One, it only relates to loans, the article in stuff today shows how narrow that look is.http://www.stuff.co.nz/business/property/90861306/house-investors-hit-r…

Two, the only reason affordability is better is the current low interest rates, and they are so low that a 1% point shift will mean a 20% change in payment. And they will shift.

Thanks - so investors are purchasing a record proportion of houses in Auckland despite the regulations restricting access to mortgages for this group. According to the stuff article investors account for 44% of purchases, which seems a very large proportion. Is this similar to "large" cities in other countries? Or are we special?

The average across the country is 40.5% using the C32 figures. Auckland is likely similar to other cities even though it's a little higher.

Cheers! It is interesting that this is consistent across the country and not just an Auckland phenomenon. I wonder whether these levels comparable to other countries?

I also assume these rates can be used to project home-ownership rates(?) i.e. if the ratio of investor to FHB purchases is greater than 1 then home ownership declines (assuming investor properties are rented out) and vice versa.

Thanks, redcows. It really makes me question the data. If both articles' data is correct (loans to investors in Auckland reducing and purchases by investors in Auckland increasing) it means that there is a massive surge in cashed up investors (not needing a loan) buying in Auckland. I'm finding that very hard to believe.

David Chaston, any coments ?

Yes, that is what CoreLogic seems to be saying. My article was based on RBNZ data (which they get from detailed, regular data supplied by banks to them as regulator).

I read the CoreLogic report and they don't give a source. I am not saying they are wrong, but it is not clear where they get their volume data (converted to %) on pages 26, 32 and pages 38 to 46. They don't say.

Note that my report is of values, not volumes.

But it does seem that they classify "investors" as "multiple property owners". Their numbers are higher than I would have expected given the RBNZ value data. But perhaps they are right? maybe there are substantial numbers of realestate transactions going on without mortgages. Personally I would find that odd given that the latest data of the number of mortgages and the number of total residential dewllings are not too dissimilar. Many propeties will have more than one mortgage registered against it (floating plus a fixed one, for example), and many properties will be paid off. Still, given the REINZ sales transaction data, and the RBNZ mortgage total data, I would not have expected a recent rush of all-cash house sales transactions, which is what CoreLogic seems to be implying.

If there is, it is happening when REINZ dates data is declining quite sharply. And you would think it would be quite noticeable.

Thanks a lot for your reply David, much appreciated

That's a mighty big peak in 2016. We are going to wear the fall out from that for some time.

Independent observer, yes I am a full time proerty investor without other paid employment.

I provide quality accommodation for people that wish to rent rather than buy.

Christ, what do you do all day?

"People that wish to rent" is not the right phrase. "Have to rent or otherwise be homeless and also can't afford to buy a house because prices are outstripping wage growth" is a better description. How many of your tenants would rather own their own home?

Also, when did you buy your first house, what was the house price to income ratio of it, and how much help did you get?

Owning a house is not the path to financial security.

A house is a home, it is not business.

Yup, you're right :)

Your own house is a home, if you own other houses it's a business...

Your own house is a home, but if a millennial wants to live in it, it's a business (rental)

Its not financial security, but if you retire and you have other investments, you dont want your money to be spent on rent. So ideally you will be rent free. So I take it back, in a way it is financial security.

Wildcard and Gordon the chch population is growing as per mfd's reference

As for future earthquakes properties all fully insured apart from 2 and purchased for less than land value and equity just fine.

As for diversifying wouldn't touch shares again with a barge pole.

That's because you do not have the talent to own and hold shares The Boy. Your talent involves buying "as is where is " homes in Christchurch as you have admitted. Anyone can do that. My initial shares in my main investment cost me a dollar and now get 40 cents a share dividend with some imputation credits thrown in. Beats property every time.

Hey Gordon, do you have any advice, tips or pointers for a beginner investor? I want to dip my toe into the sharemarket but I'm not sure where to start, whether to go for mutual funds or ETFs, whether to use a broker or an online platform etc. Thanks :)

My 2 cents worth:

ANZ Securities or ASB Securities are good starter choices as online platforms which do all the basics. ANZ has multi-currency accounts, so you can put money in AUD, for example, when the exchange rate is good. When you sell a holding on the ASX, you can also have the cash put back into AUD, for example. Both charge around $30 per trade for NZX/ASX trades.

Smartshares would be a good place to start with NZ-domiciled ETFs. Keep in mind that apart from the bond funds, the international ETFs are not currency hedged.

The ASX has quite a lot of choice in ETFs alone, with things like short ETFs available (i.e. market index goes down, fund net asset value goes up--an option to reduce market downturn losses). If you include LICs and LIEs (actively-managed investment funds), then the choice gets even bigger.

Keep in mind that US shares are pretty high at the moment, so might be topping out. But who knows!

I'd advise spending some time reading first, before jumping in. Both NZX and ASX have useful articles on their websites.

Thanks for that JetLiner! I'll definitely read around and check out ANZ/ASB :)

Fair enough Gordon re the talent.

Have had shares before and are now toilet paper.

My wife does have shares and equities managed by a Financial Advisor to an extremely large value through inheritance!

Return for the past year was rather pathetic which is hard to understand when the sharemarket internationally has been strong?

Lies.

Well, unless you have managed to find the dumbest FA around.

Even the NZX50 index went up like 15% in the past year. American indexes have been going absolutely nuts. Given normal hedging, you should easily have been returning over 10%.

Silly man.

Nymad, don't come on here and say that I am telling lies!!!!!!

The return for the year ending December 2016 was 4 per cent thru a well know Financial Adviser.

The best returns was the listed property with international equities thru equity trusts were negative.

The amount invested is a few million.

A few million!!!!!!! LOL. And you expect us to believe that when you poo hoo equities. You certainly are one of the biggest frauds on this site The Boy.

Gordon, my wife is a quarter share of the family trust investments that were her fathers investments.

I don't like shares etc.

If you want to call me a fraud Gordon take me up on my offer!

A few million?

And your return was 4%?

You sure he didn't just take out a term deposit for you?

I'm sorry, but I just don't believe those numbers.

You're either getting screwed over or you are extremely risk averse.

Previous years father in law had returns around 10 percent.

I suspect the returns to the financial advisor were quite satisfactory though. The first place to look is at the fees charged on the portfolio. Remember a 1% fee might sound small, but that would be 20% of your profits if you achieve a 5% return. My choice if I wanted an easy life would be nice cheap index funds, spend a day researching and setting it up, then maybe 3-4 hours a year rebalancing and reassessing. For my sins, I prefer to invest actively and have done usefully better than most indices over the last couple of years, but obviously it's a long term game and dominated by luck.

I don't know about anybody else,but I'm fed up with the pointless mud-slinging between you and The Man. You invest in equities and he invests in property and there is no common ground between you. How about you both give it a rest.

I speak as primarily a long-time stockmarket investor,with one rental property. Why? primarily because I have been involved with the stockmarket personally and professionally for many years-mostly in the UK- and I feel more comfortable with shares. However,as I have found since coming here in 2003,most Kiwis are happier with property and I am not going to argue with them,it's pointless.

Totally agree with you Linklater.

Every time I say something this Gordon comes on and talks crap.

He states that CHCH population is diminishing when clearly the facts say the opposite.

He calls me a liar, when everything is gospel.

I have challenged him to a 100k offer that the loser pays the 100k as at yet he has not accepted!

The offer still stands Gordon.

If Gordon accepts I will contact Interest.Co. and prove the facts.

They will confirm or not confirm that "the man" is truthful in all his facts including the investments of the wife's.

If I am a fraud then I will pay up the 100k and Gordon can then go on about how I am a fraud, otherwise Gordon needs to pull his head in!!!!

I am waiting Gordon.

Well, us plebs can't afford houses so we have to make do with shares. I noticed the ETF for Aussie resources increased by 40% last year!

Try stopping by www.nzshareholders.co.nz, there's some good resources to get you started. As JetLiner suggested, do lots of reading! MoneyWeek on youtube has some basics videos which might be helpful too.

Thanks for the information rmnz :)

You mean who would probably like to buy but have been priced out by foreigners and investors using debt as their vehicle of choice. Otherwise seems fair.

dp

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.