Here's my summary of the key events overnight that affect New Zealand, with news of draconian export controls coming in Australia.

But first, the White House has launched its much-awaited 'tax reform' plan. It would reduce the corporate rate to 15% from 35%, and reduce the top individual rate to 35%. Lower brackets would be condensed and set at 10% and 25%. The plan would end deductions for state and local taxes, and the Alternative Minimum Tax (AMT) would be repealed. (The AMT was the only thing that caught Donald Trump and had him paying any tax at all in 2005.) It would also repeal some special taxes for people with in incomes above $200,000 per year, and repeal estate taxes for people with assets over NZ$8 mln. Itemised deductions for home mortgage interest and charitable contributions will be preserved.

And Trump is proposing a 'repatriation holiday' for cash earnings of US companies from their overseas subsidiaries. Basically its a tax-free pass. If it becomes law, it will drive the USD higher, and potentially reduce global M&A noticably. It will also see US shareholders showered with additional payouts.

Meanwhile, Congress moved closer to a deal to avoid a government shutdown at the stroke of midnight on Friday US time, as negotiators worked to clear away remaining disputes in a massive spending bill.

In the UK it is becoming clear that London will lose its status as the EU's main financial hub. Because about 80% of foreign exchange trading and 30% of all bank lending in the EU flows through London, most of that will need to be re-routed through an EU centre after Brexit. And that means a huge change is coming, according to the French finance minister. The biggest sector seen moving is euro-denominated clearing the huge value in derivatives products traded every day to insure companies against interest rate changes, currency fluctuations and inflation risk. The EU sees it as an issue of sovereignty and security of European monetary markets and are unlikely to compromise on the issue. After the EU's own institutions, American banks will be the first to make the switch. And that may leave London a shadow of itself in the financial world.

In Australia, the focus is going on 'rental affordability' especially in the key cities of Sydney and Melbourne. They define it as spending no less than 30% of take-home pay on rent if you are a low income household. And one group has declared Sydney in a 'crisis'.

And the Australian crisis over its domestic gas supply is reaching breaking point. The gas production companies are all committed with export sales and 'negotiations' to remedy the local situation have gone nowhere. So now Canberra is to impose stiff export controls to force the producers to divert supplies.

Back at home, Finance Minister Steven Joyce is giving a pre-Budget speech in Wellington just before 1pm today. He'll be making the first of the Budget infrastructure announcements. More on that later today.

In New York, the UST 10yr yield is down today and now at 2.31%.

Oil prices are slipping lower at now just under US$49.50 for the US benchmark, while the Brent benchmark is now just over US$51.50 a barrel.

The gold price is unchanged at US$1,263/oz.

The New Zealand dollar is lower again today at 68.9 USc its lowest level this year. On the cross rates the Kiwi dollar is at 92.2 AU¢ and against the euro at 63.2 euro cents. The NZ TWI-5 index is now at 73.7 a new nine month low.

If you want to catch up with all the changes yesterday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

35 Comments

Canada's Housing Bubble Explodes As Its Biggest Mortgage Lender Crashes Most In History

http://www.zerohedge.com/news/2017-04-26/canadas-housing-bubble-explode…

With a 10 percent interest rate plus other fees and charges, the company is effectively paying 22.5 percent on the first C$1 billion it borrows, which falls to 15 percent if it uses the full C$2 billion available to it, according to Jaeme Gloyn, an analyst at National Bank of Canada.

That will end well......

Would i be correct in saying that some of these depositors withdrawing funds must also have mortgages with the same outfit.

How will that work out.

Canada's mortgage debt stands at 1.44 trillion. On a per capita basis New Zealand's outstanding mortgage debt is 1.86 trillion.

You should always be sceptical of zerohedge. Their headline is wrong. Home Capital is a small player in Canad's mortgage market and far from their "biggest mortgage lender".

Home Capital manages C$28.9 in mortgages that are both on and off their balance sheet.

That is only about 10% of what TD Canada Trust has for mortgages (C$217.3 bln) or RBC has for mortgages ($C224.2 bln). And there are BMO, Scotiabank and CIBC also as majors in the mortgage market.

zerohedge's claim that Home Capital is Canada's largest mortgage lender is laughably wrong. But it does make a good headline to bait the gullible.

Any idea how that compares with Northern Rock? It does look almost identical at first glance.

Northern Rock owed the Bank of England about £26 bln when it collapsed in early 2008. Not sure what the exchange rate was at that time, but those 2008 C$ were probabaly about C$50 bln or something like that. Which compares with Home Capital's C$29 bln in 2017 dollars.

After it was nationalised by the Brits, Northern Rock has traded on. It did not fail in the sense that its borrowers were all forced to repay their mortgages by a liquidator. Rather, it had relatively little impact on borrowers. It was the taxpayer who covered the impact.

Canada's Home Capital is not broke (yet). It has just suffered a fall in its share price so far.

The Brits have a longer tradition of dealing with bank crises and a deep institutional understanding of banking. However, the first bank run in 150 years seemed highly significant to me. More than the canary in the coal mine, more like a collapse releasing explosive gas deep in the depths, looking for a match.

Zerohedge are masters at using sensationalist headlines to make you think WTF and do a double -take .

In any event there are early signs of cracks appearing in asset prices which which have been artificially inflated with cheap money.

It is always the weakest borrowers who crack first , and those are the ordinary folk , middle class homeowners who piled in to the market

It was also in Bloomberg but without the "biggest' healdine...but..

......... Other home lenders’ shares declined as well, with Equitable Group Inc. falling 32 percent, Street Capital Group Inc. down 7.5 percent, and First National Financial Corp., 8.5 percent.

"It is becoming clear that London will lose its status as the EU's main financial hub according to the French finance minister.. So Paris then, if Sapin is correct? No. Frankfurt is the obvious choice, but logically it should be Brussels, of course. London, might still be London after all of this!

I still don't think anything has become clear regarding Brexit whatsoever and I don't think reporting what a French finance minister has said makes anything clear! It would be like reporting something Boris Johnson said as clear. Someone who has such an obvious agenda, is never objective. This article has basically lifted this news story from the BBC but missed out the counter argument where London does billions of trade in USD without being part of a single market. http://www.bbc.co.uk/news/business-39716951 and arguments from major London players, that they have differing views.

Both sides of the Brexit negotiations are going to throw shade at each other, especially in the early stages of the divorce. That is how negotiations start. But we won't have a clear idea of what Brexit will do to the City of London until some of the cards are on the table. Maybe 2018/19? As is stands for April 2017? Nothing is clear.

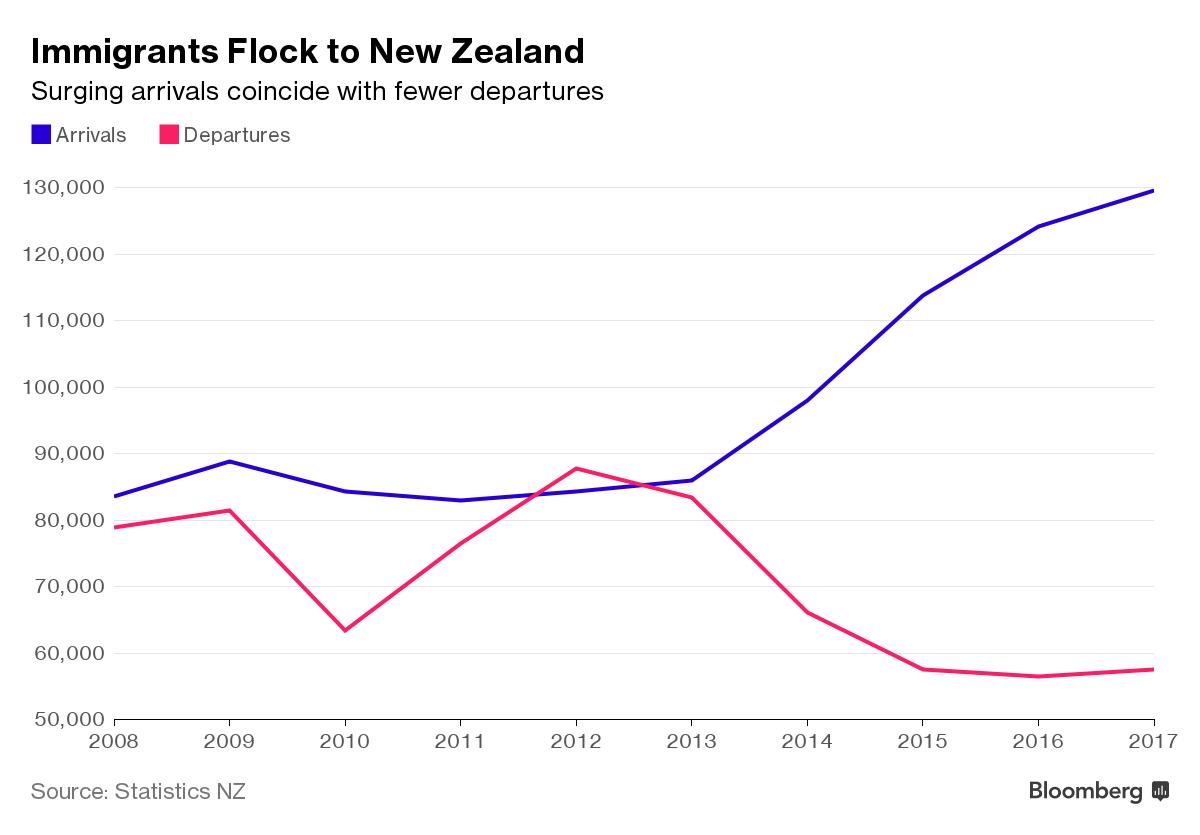

New Zealand's strong economy and isolation make it an increasingly attractive place to live amid the global uncertainties caused by terrorism, Brexit and Donald Trump's U.S. presidency.

Strong for the few. Why are the OCR and short term deposit rates below the recently declared CPI metric?

This is something that Milton Friedman also talked about, particularly in 1998 with regard to Japan. He called it the interest rate fallacy, meaning that low nominal interest rates signify "tight" money conditions, or what would be consistent with significant deflationary pressure. It is and remains a fallacy because economists like those at every central bank around the world have decided instead that low rates are only "stimulus."

To correct this view, Friedman pointed out the basic, non-trivial distinction between a liquidity effect and an income effect. Low rates can be stimulative in the short run (the liquidity effect), but over the long run their persistence means something far different. A yield curve is supposed to be upward sloping given the core time value of money and investing. That arises from opportunity cost, meaning the more plentiful the opportunities the greater the time value and the steeper the curve (the income effect). Yield and/or money curves (the eurodollar curve and even the history of the OIS curve) that collapse and remain that way unambiguously demonstrate that "stimulus" deserves only the quotation marks.

Policies that continue to be categorized in that fashion while the interest rate fallacy remains are devoted to the economy that "ought to be", not the economy that is. The danger comes as Keynes warned, in repeating mistakes rather than learning from them. The result is a trap of exactly what Bernanke described as never being able to happen here: recession, rising unemployment, and financial stress. Read more

Thanks for that. This chart says it all, and exposes our government lies that it is caused by returning kiwis:

https://assets.bwbx.io/images/users/iqjWHBFdfxIU/iuBXhAG8D6jM/v1/-1x-1…

{kind=link}

"People just keep turning up", says the prime minister.

He's a master of problem definition :-).

The French elite attitude to banking is that it is an arm of the state and that they know best. The City of London is not built on that, it is chosen by customers as it has enjoyed more protection from state interference historically. It is a classic clash of cultures, in essence it is Danish Common Law versus state control via Roman Law. The French enarques cannot comprehend that there is another way of thinking and acting and organising a country. Their attitude is that the whole world should be a colony of France, because, after all, they know best.

The City of London is chosen by the wealthy people of the world, as is Switzerland. All oligarchs and dictators, sorry, I mean absolute monarchs, are welcomed with open arms, as are wealthy citizens of France and Germany over the centuries, regardless of race, I might add. The City of London has a long history of defining it's relationship to the state which is central to its institutional culture.

https://en.wikipedia.org/wiki/Temple_Bar,_London

Since housing bubbles are topical. http://www.oftwominds.com/blog.html

"When bubbles are followed by echo-bubbles, the bursting of the second bubble tends to signal the end of the speculative cycle in that asset class. There is no fundamental reason why housing could not round-trip to levels below the 2011 post-bubble #1 trough. "

Echo bubble or dead cat bounce ?

Well I would think the distinction is that one happens on the way up to continue the trend, the other on the way down once the trend has changed to the downside.

I am not so convinced it is about to happen when the solution still exists to respond to a crash of a bubble with more money printing that caused the bubble. A crash is more likely to be led by inability to pay.

Will there be anyone left to pay taxes in the US? The concept of the government needing an income seems to be a Trump admin oversight.

They can and do just print the money. They dont need the taxes.

Normally a ponzi such as this would implode (sooner), but the rest of world is indebted in US$ and energy is sold in US$ so devaluation is of little concern.

They print and the rest of the world supplies them with actual stuff ...all courtesy of the military wing of corporate America. God bless.

As the world pie shrinks, the periphery suffers while the core (US) moves to protect itself.

Really?

Are you saying that the US could simply cut all tax rates to zero and just print dollars from here to eternity? I think not. QE has seen the Fed create money electronically and buy bonds from the big financial institutions. Much of this has then been deposited back with the Fed,rather than being lent out for productive purposes.

Really?

Are you saying that the US could simply cut all tax rates to zero and just print dollars from here to eternity? I think not. QE has seen the Fed create money electronically and buy bonds from the big financial institutions. Much of this has then been deposited back with the Fed,rather than being lent out for productive purposes.

The tax avoidance scam is alive and well in America. Some have it down to a fine art.

Some have just been made ruler to bend the rules some more.

Some Corp orates excel at fiddling the spreadsheets. Not what excel was really designed for.

Build a wall,using borrowed money....a few cracks in that example too...Not all it is cracked up to be??.

I am all in favour of tax cuts , BUT with the proviso they actually help the lowest earners , and the US has this problem of the working poor , which is fundamentally wrong , so lets hope Trump is sensible in this approach.

On the score of tax free profit repatriation , the tax system is flawed as it is , and has to get sorted to encourage US Corporates to distribute dividends rather than use them to acquire more companies .

I see Winston Peters has really got onto the election road , stirring up a hornets nest by accusing two "Asian " reporters of lying about the sources of our migrants , and the remarks have caused outrage , and even the Race Relations Commissioner has waded in .

Problem is , I read the article which says most migrants are Poms , Germans and South Africans and did not believe it (and I DID NOT look at who the authors were)

Fake News or an alternative version of the truth , take your pick

I believe you are referring to the article in the herald yesterday.

That was for skilled migrants, the numbers were official.

Once all visa types are included Chinese and Indian migrants are the highest

what WP was on about was the cherry picking of data to support a conclusion, somthing the herald is very good at nowadays, they are more a PR machine than good reporters.

take all the housing stories where they have been given a helping hand by parents,

or the uber driver did they not think he broke the law and check it out?

or the trucking company owner that underpays so need immigrants

as for their being called immigrants i guess like everything your backround will shape your thoughts so can cloud ones objectivety, and when i saw the reporter come out and say it was racist my first thought is why call it that if your work is above reproach, or are you hurt because someone called you out

I think the data is very, very valid. It is just being interpreted the wrong way.

Look at it this way. Most "Skilled" migrants are from the UK.

It's not the 6,000 UK immigrants buying property for ridiculous prices, nor is it them that settle only in Auckland. They tend to spread out more.

BUT

It is this, and only this visa that is being tightened by the Govt's tinkering.

They have left the student visas (i.e. man on the ground funneling money) alone.

The fact Winnie has ignored this, and also based on his interview this morning where he seems to have softened his anti-immigration stance (yes he still rants a bit, but he is not as adamant as before) , makes me wonder - will anyone actually stop the influx?

A point Winston referred to was the habit of a biased media never asking strong opponents of a policy for their view.

Even Interest.co.nz ends up getting into this with their regular propaganda articles from the "Research Fellows" (indeed) of the NZ Initiative on housing and immigration yet there does not seem to be any equal balancing from the organisations that assist the bottom rungs of society affected by these policies such as the Red Cross, AKL City Mission, WINZ and the like.

you just have to look at the backrounds of the NZ initative to see why there is a bias towards immigration.

its the same way i have a bias towards those born here come first before we look after outsiders

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.