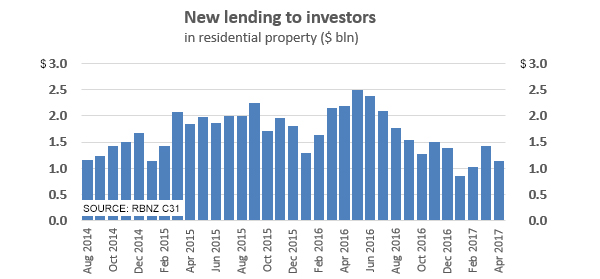

In April, banks loaned $1.143 billion to residential property investors.

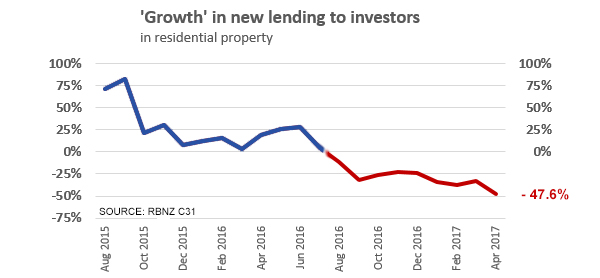

That was -47.6% lower than the $2.182 bln they loaned in April 2016, and is a drop of more than $1 bln.

New regulatory lending standards mean investors must now have much more skin in the game if they want any leverage in this market.

And the result has been a very sharp drop-off in loans.

But this fall has not yet allowed first home buyers back into the market - probably because house prices have not realigned themselves lower yet. The volume of transactions is lower, the number of unsold listings is higher, but seller price expectations are still based on historic levels.

However, the speed with which the clampdown on investors has happened will encourage the RBNZ that their policy and regulation signals are working.

The data that tracks new housing lending only started in August 2014, but even this shows how sharp the correction has been.

And given the banks cooperation in restraining this side of the market, the dive in lending will likely run - even increase - until at least Spring, and then level off at the lower levels.

The following chart is the year-on-year change in the data in the above chart.

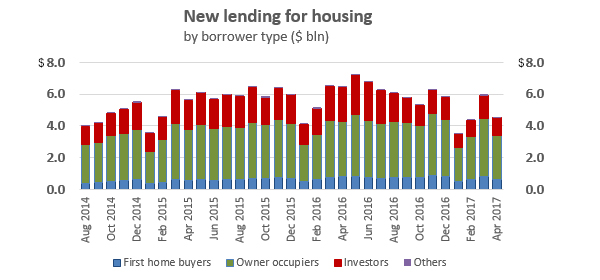

But it is not only new lending to investors that's declining. New lending to first home buyers was down -20% year-on-year in April, and that was the first month we have seen any decline. Lending to other owner-occupiers was down -21% year-on-year, and while this had also fallen in three of the six prior months, the April fall was the largest.

The unusual occurrence of public holidays in April 2017 will have contributed to the size of the falls. But they are unlikely to have masked a real shift lower.

102 Comments

Not exactly surprising!

Banks have changed the goalposts for all investors and now require all loans to be LVR 60% on all loans that they approved at 80%.

Hardly fair!

Life isn't fair, The Man. I'm sure you'll cope.

Besides, reducing property investing and speculating and household debt in NZ is a good thing.

Reducing property investing? So you don't want people renting anywhere?

Who do you think provides the housing in this country?

No, I'd like to see government initiatives and incentives to help foster home ownership and to stop investors simply leveraging unearned equity and capital gains to grossly distort the property market in favour of themselves and the wealthy and continuing to shaft young Kiwis and future generations. After all, the Boomers who got wealthy off property investing received advantages by the governments of their day that young Kiwis have successively been denied by these same Boomers.

this from a politician who has let the unspoken out of the beehive

The problem with the Accommodation Supplement was that it tended to be a subsidy to landlords.

"And actually, there's a pretty good consensus - even amongst National Party MPs - we are going to have to do something about it, because it's fuelling the wrong kind of response as a solution."

Davo36 are you suggesting that it would be beneficial for NZ society for the percentage of home owners in NZ to continue to decrease? What possible reason do you have for supporting that belief?

There is a direct correlation between the current housing bubble, increase in real estate investor share of the current housing stock, and a decrease in home ownership.

Why is that difficult to comprehend? And why do you think that is a good thing for NZ?

Ideally there would be a huge influx of affordable housing if there weren't any restrictions on building, e.g. the free market solving the issues of supply.

This would drive down house prices, and corresponding rents. Sure, many people will always prefer to rent but that doesn't mean that the current property valuations and rental costs need to be maintained.

Ah, you don't think land owners, developers etc, anyone with a stake would make sure supply was always restricted to keep prices up, do you, by any chance? I suggest to you, that supply would NOT meet demand as land owners and developers looking to have prices drop would really be a bit like turkeys looking forward to Christmas.

Then there is the little matter of infrastructure, water, sewage etc, there is more than town planning in the mix you know

The fact that land owners and developers have a choice in restricting land supply is a problem in itself. We really need to issue some long term infrastructure bonds or something to develop faster than we think we need, rather than playing catch up all the time.

Sure - a great thing - until you work out that the number of new builds funded and generated by FHB is extremely low - in fact negligible . The majority of all new builds and developments are financed by investors who purchase off plan, put up the majority of working capital and underwrite these projects. At 50% less lending - you can bet that probably means a large reduction in new builds being commissioned and funded.

happy to lose the speculating - and a harsh shock would get rid of many of those speculators but the investors are in for the long run and will ride it out - and they are needed to fund the massive amount of new builds required in the next ten years

"Banks have changed the goalposts for all investors and now require all loans to be LVR 60% on all loans that they approved at 80%."

By 'Banks', do you mean the Reserve Bank? It is they who introduced the rule and it's a condition of a banking license.

Well what Property Investor in their right mind would want to invest in a falling market with poor rental yields? Even if they lowered the LVR restrictions you still wouldn't see much change until the market has bottomed out. That could take up to a year or two to fully take effect.

Yup. A renter can only pay a certain maximum amount for rent per week, and the higher house prices go the worse the yields are.

Wrong you can crank up the rent to the point the tenant has to decide between a house and a tent or their car. Its no different to paying a mortgage you could also argue there is a maximum amount you can pay so you pay it or sell up. Having a roof over your head is pretty much at the top of the list so as rent increases it just means you have less to spend on other things. There is still a big gap in whats being paid in rent and what could be extracted if push comes to shove.

Difference is the tenant is paying the Darklords mortgage, not their own.

If it is a falling market why are apartments being sold for $8.7m or more??

Overseas buyers, riding the hype train, stupidity, greed, "property is the only investment in New Zealand," poor financial literacy and money laundering.

The market may be quiet right now but prices won't fall through the floor (despite plenty here yearning for that to happen).

Over the next 2-3 years, prices will likely rise by a few per cent.

Auckland and Wellington remain excellent cities for long-term property investment. Demographic trends, combined with NZ's increasing attractiveness, globally, as a place to live fully support that. NZ is a destination of choice. (Just think how many people in Manchester would love to live in NZ, following the recent atrocities there.)

Location, as always, is key. In Auckland and Wellington, properties without traffic/transport problems will fare particularly well.

But we absolutely need to address the plight of first home buyers and older people who want to own their own homes. Otherwise, NZ's social fabric will be torn - and very difficult to stitch it back together. Personally, I think the answer lies in regional development - and creating more jobs in the regions. New-wave industries can prosper in the regions - while providing jobs.

Does your crystal ball give a 100% confidence rating with each forecast prediction?

Really where do you think these "New-wave industries" are going to come from if property prices keep the cost of living in Auckland so ridiculously high? I've just seen another Multi National IT company close one of it's AKL sites due to not being able to attract qualified staff to work in their CBD offices.

BAHAHAHAHHAHAAAAAAAAAAHHHHHHHHHHH *chokes* BHAHAAAAAAAAAAAAAAA

Tothepoint, the average house value in Manchester is £178,420, at current exchange rate (today 1.81) is just shy of $323000, where are they going to buy somewhere in Wellington or Auckland with that? (assuming they have no mortgage and we shouldn't assume that because debt levels on those house values are also pretty high in Manchester.)

Not to mention that National have just made major changes to immigration policy and lots of Brits are no longer able to migrate to NZ as easily as before.

Honestly, you run on like an advertising campaign repeating to the letter almost the same comment over and over. What is up with that?

Yes, yes, no one disagrees that a long term landlord anticipates ups and downs in the housing market. But why do you keep repeating it? Everyone knows that the housing crisis has not been caused by the professional long term landlord, but the foreign capital flights and greedy speculators.

To be fair to tothepoint he didn't say that Mancunians would buy in Auckland, just that they would love to buy in Auckland. Also there are most likely higher than average priced suburbs in and around Manchester where properties could be sold to purchase a place in Auckland.

Hi Gingerninja,

Respectfully, there are plenty of regional cities/towns across NZ where one can buy an adequate 3brm home for $323,000.

You miss the point of my post.

But there aren't that many jobs in those locations....

And that's exactly the reason why I'm advocating regional development!

I don't wish that NZ become a two-tier society with the wealthy living in Auckland and Wellington - and an underclass of citizens living in provincial towns/cities. I think that would be hugely damaging to NZ.

How much less can you afford to accept if you can buy a house that cheaply. Say $700,000 cheaper at 5% = $35,000 per year and the reality is that some of these cities have significantly lower unemployment than Auckland. Living and transport costs are significantly lower, and free public education far better.

I haven't missed your point. You are suggesting that the various global crisis' will lead people to want to move to NZ, particularly NZ's premier cities. And you are right, they may well *want* to, they may even google about a bit to see what that would practically involve but then the reality will hit them. They just can't and they won't, not in any statistically significant way.

1. The average urban Brit would find it very hard to live in bumblef#$k New Zealand. Some would want to "escape to the country" sure, and yes, maybe some of those could take their $323000 (which in reality is a lot less, because that figure envisages no UK mortgage and that is just not the reality of anyone under 50 in the UK) but then, what would they do for work? And how would they meet the increased skill point system that INZ has recently introduced with the higher wage requirement?

2. I moved to NZ from the UK 9 months ago and am part of various forums and groups of Brits in NZ/ wannabe Brits to NZ and NZ expats returning from the UK. These online places are all full of people complaining that they are no longer eligible for visas and even if they were, they can't afford the NZ house prices. Almost all of the wannabe Brit migrants want to move to an NZ city, preferably Auckland or Wellington, very very few express a desire to live in the regions.

3. Percentage of Brits moving to NZ has been decreasing and all those headlines about post-Brexit and post-Trump migrant stampede's didn't actually translate into actual numbers of new migrants. I checked the actual numbers (rather than the stats, which looked huge in the headlines). For example, the increased numbers of Americans sending in an expression of interest request was less than 200. However, because only a small number of Americans migrant to NZ, it made for a headline statistics and people on this very site crowing about there would be floods of yanks fleeing to NZ. But this never happened;

http://www.stuff.co.nz/world/americas/us-election-2016/88785550/america…

4. Most of the Brits I know, are very very VERY experienced in house price cycles and unlike NZ-ers, the average Brit does not ever say that house prices never go down, there is a house price crash every 10 years or so, maybe less than that in the UK. We all know someone who has either had negative equity or currently still has some (after the GFC) or been burned and almost all the Brits I speak to on these forums, who have moved to NZ in the last 12 months, have left all their capital in the UK and are waiting for what they believe is an inevitable house price correction before they buy, they have no intention of buying at what they consider incredibly inflated prices.

I have a rental property in the UK, turning over a nice 8% after letting and management fees because I bought it in the crash. My current mortgage is 5 year fixed at only 3%. I can't get anything that good in NZ, so won't buy here. I am also on various landlord forums and whenever a newbie wouldbe investor pops up, asking for advise on investing in property, all the experienced landlords in the UK tell them to run a mile. Partly that is because of recent changes in legislation that have made property investment less of a cash cow than it once was and more in line with the return on other investments. Interestingly, these changes have come about because of public outcry against property investment and how speculators and BTL landlords are stealing houses from first home buyers. Eventually, the government responded. Maybe that will never happen here though ay?

Hi Gingerninja,

Thanks for your comments.

I'm happy to let readers draw their own conclusions.

I do agree with you though, that Auckland and Wellington represent very good long term investments, for those who can afford them, in general. NZ has a tax/legal system that makes housing a very advantageous long term investment. But I don't think the yields are there for Wellington or Auckland at the moment and I would guess, that at some point, the political climate will change (as it has in the UK) and that tax/legal advantage will be increasingly eroded.

I would love to buy a house in Wellington, i've got a young family, and would like to buy the house that they can grow up in and I can grow old in. However, I have never bought in a bubble and I never will. I've seen the devastation that wreaks.

One data point does not constitute a market

That was hardly an "Apartment" it had nearly twice the square meter age of my house at nearly 400 Sqm !

CJ you are talking about Auckland.

There are still good returns on property around the country.

The will get better as well as investors and first home buyers aren't able to buy, the people with plenty of equity will once again do very well.

If you are in such a good position equity wise why are your comments so angry and negative. Oh that's right you live in a town where property values are falling as are the rents being paid. You want it easy for investors to borrow money in order for your poorly performing market to lift in sentiment. And things are going to get worse for you as winter bites and the election gets closer. If National loses the election there will be a huge shakeout especially in Auckland as markets love certainty and that will include equities.

Property is a rubbish investment, at least right now

On the contrary, Fritz. Property remains an excellent long-term investment.

Notably, there's an enormous underlying demand for real estate in NZ.

Well you are lucky if you get yield above 4%, and capital gains from here are likely to be subdued.

It may have been good in the past but not anymore

Where are you getting a better yield?

KFL, GEN, OIC and many other blue chip stocks

The reality is that the consumer has found a resistance point...Bank repricing of interest rates and an expectation from consumers for more, now links up with ....slowing conditions in the two key employment sectors of housing and retail...Wage growth remains absent, and underemployment high....And all of this is well before anyone really panics, which is the Reserve Bank's worst scenario...Households have been able to maintain living standards in the face of collapsing wages growth by dipping into savings....But burning through savings can't last forever....It's folly to imagine (asset prices) will only ever go up. It's double-folly to imagine than when it swings into reverse the effects it won't be just as powerful on the way down.

http://www.afr.com/news/economy/the-australian-economy-turns-down-and-t…

And it's not just NZ that's starting to notice a softening property market, Vancouver, Toronto, Oz and the UK are staring to see their sales and prices fall (For various reasons a part form the big reason).

FT article: House prices — sellers forced to offer discounts

https://www.ft.com/content/20bb4b1a-398d-11e7-ac89-b01cc67cfeec

Vancouver Is Seeing Less Sales In May…and More Inventory

https://betterdwelling.com/city/vancouver/vancouver-is-seeing-less-sale…

In AU, owner-occupied residences are exempt from CGT

AU govt has just changed the rules - that exemption no longer applies to non-citizens

does that capture kiwis now too ?

"The Australian Budget earlier this month removed an exemption from capital gains tax on a main residence for foreign and temporary tax residents. It raised concerns from Kiwi expats that they would have to pay tax of up to 50 per cent of any house sale profits. Brownlee said today that the policy had not yet been written into legislation and it was unclear what its exact impact would be."

To put it another way

If you are a non-citizen and you own and occupy your residence it will be subject to CGT

Gordon, not angry just stating why investor borrowing is down.

Haven't got a problem with lvr at 60 % for new borrowing on additional property being bought, but investors shouldn't have to have all previous property that the Bank lent at 80% altered down to 60%.

Doesn't affect us but we are just more picky now on additional property having to throw equity of 40% in.

Rents haven't really dropped a hell of a lot Gordon just that there aren't as many people around compared to the thousands of extra houses being built.

Chch is definitely growing though and is going to be the City of choice, affordable and quality lifestyle!

Reminds me of a decade ago when I moved to NZ. Had a short term rental in Rolleston for the first month... Rolleston... "the city of the future" was its motto if I remember correctly. Well, it certainly wasn't the city of the present at that time and was unlikely to be a city in its own right at any point in the near future (my opinion, take it for what it is).

TM2, good luck with that assessment. I'm seeing a whole bunch of confirmation bias in your comments. My experiences suggests that your rather fixed views tend to make a small fortune out of a large fortune. One should be nimble and adjust to changing parameters. Wishing it were so, and complaining about how it isn't so doesnt change reality.

And the lending figures are mirrored by the sales volumes. Sales down 38 percent in Auckland y/y, nationally 33 percent. The last time Auckland saw a decline of this magnitude was in 2008. New Zealand is facing a balance sheet recession, and the conflict, even on this website between real estate bulls and bears suggests that a full blown crisis is straight ahead, and unlike 2008 there will be no Federal Reserve , get out of jail card.Prices will fall upwards of 60 percent, unless toothepointy keeps buying.

"This is a crisis. A large crisis. In fact, if you got a moment, it's a twelve-storey crisis with a magnificent entrance hall, carpeting throughout, 24-hour portage, and an enormous sign on the roof, saying 'This Is a Large Crisis.' A large crisis requires a large plan. Get me two pencils and a pair of underpants."

Cowpat

"Prices will fall upwards of 60 percent, unless toothepointy keeps buying"

You win the internets today. Very funny mate.

Perhaps a Fibonacci retracement is what was meant? 61.8%. ( others being 23.6%, 38.2%, 50%, and a confiscated value of 100%.). That would take property price back to just 2002 levels - arguably the last time they were 'affordable' on a price/income basis.

You'all forgetting that the world has changed. Globalisation and the massive growth of the middle-class in China and India means that prime property locations have grown to encompass entire cities. This has never happened in human history before (except maybe during Roman times).

Yeah, wouldn't be surprised if at some point this starts to drive a new wave of nationalism in NZ. Will young Kiwis be happy to be a servant class to foreign investors?

Sad thing is, they will not know any different, so may fail to question that, just as they will see renting as the norm and not consider home ownership, even think it's fine to have their life dictated to them by a landlord.

I wonder how many of them notice that when an expert is interviewed on the tv or radio it is almost a surprise now to hear a kiwi accent.

It's already well and truly happening.

Hi Cowpat.

You write: "The last time Auckland saw a decline of this magnitude was in 2008."

Have you considered how much Auckland house prices have risen since 2008? That's a mere nine years ago......

By the way, my interests in markets (including property markets) are largely academic/analytical.

What I really want to see is social equality, with all NZers having adequate housing that suits their needs. With sustained capital growth in housing (especially in the main centres) that's becoming an increasing challenge.

1/ Yes I have considered how much Auckland house prices have risen since 2008, that is how I have calculated the future fall. 2/ i am unsure what ago......... refers to , 'mere' is a subjective term. 3/ Your posts usually are lacking in any analysis. 4/ Your responses to those that are using facts to suggest there may be price falls are always countered by your facts , that people are yearning to purchase in Auckland and Wellington, 5/ If New Zealand house prices are irrelevant to you , then you have limited grasp of economics , whether you live in a cave or own multiple properties. 6/ The fact that you repeatedly state you have no allegiance to the real estate industry , but qualify with ' sales', gives me concern 7/.We are not seeing continuing capital growth, we have witnessed two decades of debt fueled religious addiction .8/ Falling sales are always an indicator of future price falls. 9/ If prices are to continue upwards , why is no one buying.

Cowpat, you hit the nail on the head with your last point

"If prices are to continue upwards, why is no one buying?"

That's just basic economics / logic right there. Why on earth would anyone suggest that prices will continue to go up even a couple of percent is beyond me. Sounds like rambling to be honest.

I think Cowpat missed the nail and hit her thumb because people are still buying houses in Auckland. Just because it's not red hot doesn't mean people aren't buying.

This very article said "The volume of transactions is lower, the number of unsold listings is higher".

You know like when you're at a bar and the bartender screams out "last call" so they can serve the final round of drinks? At that point in time, most people have left the establishment. Sure, there might still be a small number people there to buy a last round of drinks, but for all intents and purposes (and common sense) no one is buying drinks anymore. The party is over, Zach.

The party is definitely not over RichMuhlach. Do you want me to scream out how many properties were sold in Remuera and the wider DGZ and how much they went for in the last 2 weeks?

Not really, because that would mean you'd be back in your old gloating ways which means all the sympathetic comments you've posted the last few days were meaningless and all for show, which would make you either a liar, an attention seeker, or both.

Also, anyone with common sense knows that Remuera properties are not exactly representative of the common NZ Housing Market. Why you feel the need to continually (without being prompted) sprout sales information only confirms that you are a Real Estate Agent.

RichMuhlach I like to think of Double-GZ and me as on the ground reporters of the housing market in the NE and SW sectors of Auckland's DGZ respectively. It would be good to have commenters who specialize in other areas like the North Shore, Western suburbs and South Auckland. So many commenters are claiming that the bar has closed but that is not what we are currently observing. My interest on this forum was initially piqued by commenters who claimed that the party was over well over a year ago and I found this odd as I was still seeing properties selling quickly and for high prices and was able to accurately predict the percentage of price increase when others were predicting a decline.

Zach, I reside fifty percent of the time less than 100 metres from New Zealand's most expensive apartment. . Zach , your a well informed commentator , but to argue that properties are selling quickly and that the market is unchanged , does not stack up with the hard data. I appreciate the fact that yourself and DGZ rack up the kms on the pedometers looking for 'sold ' signs, those signs are staying up a lot longer.

Cowpat, some signs are staying up for longer and others are not. However even the signs that are staying up longer are eventually selling. I'm not sure how significant it is that a property takes ten weeks to sell rather than four weeks in the overall scheme of things.

Zach , my argument is not one of are houses selling, as there will always be someone that is buying/selling irrespective of the market conditions,( and lets be honest, there is always an idiot or someone for whom price is irrelevant ), the problem, as sales volumes decline from historical averages, you end up with the analogy of cream buns and atherosclerosis, at present , I am just waiting for the plaque to disembark.We have eaten too many cream buns.

Well, I think you are going to be waiting for a very long time. Get a good book and put your feet up.

I have been a regular reader on interest.co.nz over the last year. I haven't noticed anyone claiming that the party was over till very recently (ie 2017) during 2016, there were just lots of people saying that they thought a bust was imminent and giving theories for that. It's only been the last 5 months that there have been observations about quiet auction rooms, and then that being matched by hard data.

My own anecdotal data is only about West Auckland, where my parents in law were scoping the market December 2016 and Jan 2017, in order to decide whether to sell or rent out their home. In the end they decided to rent out because all the open homes and auction rooms were dead.

During late 2015 early 2016 there was a lot of talk about the Auckland property market dropping 10% and at one stage we were all eagerly awaiting the data that would prove who was wrong and who was right.

I reply to ZS, then DGZ replies to me. Now I reply to DGZ, then ZS replies to me. Now one specializes in NE, the other in SW? Couldn't make it any more obvious that you are one and the same person and *gasp* a Real Estate Agent? I must have missed that comment where "you guys" decided which "person" specialized in which area.

I have been reading the comments section for the past year as well, and have only noticed people claiming the party is over earlier this year after China clamped on capital flight and when interest rates started climbing up. I don't know who the commenters you are referring to, but doesn't it suck when someone is obviously wrong but keeps on harping the same lie over and over again without any logic or data to back their claims up? I think they young kids call that "trolling" these days...

Oh come on, they have been claiming the party is over every year for the last ten years or more.

DGZ is in Remuera while I'm on the superior Epsom side of the motorway.

Which one are you in this list:

https://www.barfoot.co.nz/find-us/find-a-salesperson?branch=38

I am not on that list coz I am not a RE Agent. I have a Mon-Fri job in the CBD and quite technically focussed. However I know more than 50% of the RE Agents on that list, hmmmm I must be one of the Kings of Remuera Real Estate you would have thought LOL!

"I have a Mon-Fri job in the CBD and quite technically focussed"

--- B & T head office :

Head Office

34 Shortland Street, Auckland City

Auckland 1010

You should read off the same hymn sheet DGZ though. B&T are on record highlighting massive drop in sales. His call outs in last B&T report:

• “The number of properties sold was the lowest in the month of April for nine years” -

• “The market is changed from that experienced over the past few years”

• “Buyers are being more selective, are taking their time over committing and are not prepared to pay above market price. Vendors have not lowered their price expectations significantly but accept that to achieve above market their property has to be special.”

Re: imminent recession possible. It's a triple whammy. Not only has Chinese capital flight abated, but domestic lending is down, and the neoliberal government is wedded to fiscal austerity. if Steve Keen is right then aggregate demand should be nosediving.

Oh boy, what has happened to the commentary section at Interest.co.nz? Folks, look at the pathetic narrow-minded, self-interested comments above. Why can't we have robust, open-minded discussions where we are willing to learn from each other for the benefit of all of us ?

lol, ditto ... there are a lot of angry folks out there! so objectivity has left the site...

Lots of angry people here because many have missed the bus. I have a few mates that are still waiting at the bus stop for a house that they should have bought years ago when they had a chance to get on the property ladder. Yes its a sad situation but that's life.

Lots of people on the bus with no headlights. Nights coming and the bridge around the corner is out....

Yvil, Eco Bird - what would happen if the sentiment of the comments on this site were reflective of the sentiment of society or part/s of it? I'm not necessary saying this is true, but perhaps you've missed a shift? If there were an element of truth to this, one would then need to reconsider where the narrow mindedness falls, but it would take an open mind to realise ones own narrow mindedness - bit of a catch 22 scenario.

Sentiments can be manipulated, charged and driven in all sorts of directions, Logic and facts can't ...

I personally don't have an issue with which way sentiments go as long as they remain objective and within the boundaries of human common sense ... Narrow mindedness is to follow a crowd and repeating nonsense without checking facts or reasoning with logic -

How did some of the sentiments against Property investors and Boomers start all of a sudden and is continuously being fed and charged? Is it because it is election year and some party cheerleaders are pushing to build up such sentiments making them the enemy of the state? and the cause of FHB misery? the blood succers of poor tax payers AS ? or they all of sudden became parasites because they worked hard and now have a passive income? was AS invented in the last 9 years or people just woke up to the fact that it exists? Is negative gearing a New Loophole?

this is just one example of pushing sentiments and charging up the ill informed ... I hope you agree that we are all trying not to go down the slippery slope or demonising any part of our society and over-charging our Sentiments .

It's sounds like you think sentiment is controlled as opposed to simply being part of human nature?

What do you think the sentiment of black workers was towards the owners of cotton farms in Southern America? Do you think the slaves cared whether the owner had worked really hard to buy the cotton field (with the banks money)? Imagine how funny the slaves thought the owner of a cotton farm would be if he said that they were injust if they felt they were being exploited...'but I've worked so hard to exploit you..., you're so narrow minded...'!

Unless you missed it, that is how a lot of Darlords sound when they complain about other people disliking their wealth generating practises..

Name calling such as "Darklords" is, in my opinion, not part of a robust, constructive argument.

Lost objectivity? When even the think tanks are predicting house prices to be lower December 2017 than they were 2016?

http://www.infometrics.co.nz/lower-house-prices-slow-economic-growth-20…

I'm pretty happy to use objective data. And I think that the data supports a slow down over the next few years. Although the jury is out for me whether that will be considered a "crash".

Actually if you read the article carefully the astute investor can find some reassurance. High migration set to continue, building consents lowering in Auckland.

*assuming National form the next government.

Some data is out there , but whether it can be fully used to support predictions of this sort, then that is questionable and certainly not Objective! ... let alone forecasting a precise 2.7% lower price in 2017 ...really??, why not 2.85%??

They quote: “Surging house prices have driven household debt levels to record highs, and it seems that some of the cautionary lessons learnt during the Global Financial Crisis are already being forgotten,”

“People that have heavily leveraged themselves to purchase property, most particularly in Auckland, are likely to find that increasing debt-servicing costs cause a significant degree of financial stress"

Wow, So how can anyone protect people who have got themselves into hot water just to own a property instead of renting until they are more capable of weathering market changes? Anyone who took the risk should bear the consequences. Unless we have to go back to the Nanny State to save those who cannot think for themselves ??

And : “Net migration is forecast to peak at 73,436pa in September this year and then remain at above-average levels during the next five years,”

No one knows if the market demand will be subdued come October 2017 or it would pick up with a vengeance .. and how would it be subdued if the migration is to peak and stay above average for 5 years according to them? Does that make any sense?

Chinese are part of the demand, not all the foreign demand... Local investors certainly stay away from the market early winter and before Elections, and come back after the dust settles ... that is not new !!

You see , this is where General wishy washy announcements / reports do the damage and steer discussions into nonsense territory ... get people emotionally involved or add fuel to some politically charged views serving certain agendas.

you would expect that the authors of these reports and other similar ones to eat their words in few months if their predictions were off by a mile , but they usually don't , instead they will come up with another outrageous one to cover the first blunder.

Is Accusing landlords of being the blood succers of society feeding on the AS, an Objective discussion ? was AS invented by the current Gov?

Or trying to picture landlords / Boomers not working for wages of having businesses to employ people as parasites in the society or money launderers in an aim to get others to hate and demonise them ... Is that Objective too?? ... or is it narrow mindedness and jealousy ?.

In my view, There is a degree of Hate and Envy oozing from these discussions which is driving Objectivity out of this Site .. We could all do without that and have a civilised discussion regardless where the market would go or who wins the election.

I hope we, at least, could agree on that one.

Yet you remain uncivil. Just saying...

Yes, but this is my point. You cant have it both ways. You can't dismiss the data that disagrees with you and only point to the data you prefer.

So far the data suggest that the housing market in Auckland peaked in 2016 and has been cooling since then. There are numerous data points on this, time on the market, actual yoy prices, inventory, sale volumes, estate agent commission etc etc. There is not direct evidence to suggest that latent demand is going to translate into a price surge, because otherwise rental inflation would have matched house price inflation. And when you look at the history of NZ immigration to house price inflation, the two don't always correlate anyway. They *are* strongly correlated of course, but if you look at the chart below, you will see that house prices can deviate from the migrant numbers suggest. For instance, if the issue was supply and demand then house price inflation (the blue line) would have been above the net migration inflation figure in 2014,2015, 2016, but it isn't. Especially, when compared to the last migration boom 02/03, where the housing market sky rocketed way longer than the net migrant numbers would have propelled it to, if they had indeed been the main and only driver. There must have been other factors for the house price boom from 2003-2008.

https://resources.stuff.co.nz/content/dam/images/1/d/1/p/4/d/image.rela…

{kind=link}

And when Chinese Capital Flight and low interest rates have been shown to be strongly correlated to housing market booms across the globe, and indeed low interest rates correlated to ever property boom ever, anywhere in the world, across history, why would any one insist that if and when these factors change, the housing market will be unaffected?

You are right and most of these correlations are correct .... and they are part of the complex and dynamic factors driving the market ... I am not suggesting that I don't like the Data at all or disagree with it - I do not like the prediction and interpretation based on this data ... simple example, look at the historic Auckland sales prices in the last 40 years .. the curves were published here by D chatson I think.

I have lived through (and invested in property) since 1999 and lived through few elections and migration waves and experienced what happened hands on--- every cycle is different , but regardless of the reasons, we have never had such strong demand and such shortage in supply since then ... BTW rent always lag behind and the fact that rent is capped has to do with the ability to charge a certain amount pw and it is purely market driven - and we do have a lot of rental properties around in this cycle - I would disconnect rent from house prices at the moment. Historically it was based on yield but now that train has left the station.

this is not about what I like or that I support a specific agenda, I would love prices to go down as much as people are dreaming of so my kids can get on the market and get their first homes... and contrary to common belief , most landlords who bought properties 4-5 years ago have almost 70-80 % rise in value so even a 20% drop will not be a disaster - after all they are there for the long run ..

I just do not like these misleading interpretation of data and conditions in a way to suggest that the market is going to do this or that -- No one knows that for certain yet alone putting any numbers on it ...From past experience , with a view of the current situation, I think that the housing market will rebound after October this year because no matter who promises what, the shortage will push the market up again for another possibly 12-18 months and be only slowed down by added supply, increase in interest rates , kerbing migration or introducing DTI ... Hope I am wrong !

Fair enough. Can't massively disagree Eco Bird. My own forecast would be a slight drop in price value this year (less than 2%) followed by a decade of some years of stagnation and some years of single digit growth.

That is purely guesswork, because the data is conflicting IMO. Some of the data suggests further boom, some suggests bust, some suggests stagnation and some data points remain still unclear (like Chinese Capital Flight.. how big effect was it really having, will it return?) and most importantly, what is next for the world economy? Things don't look great.

perfectly correct and that is why it makes any prediction worth only the opinion of its holder ... less than 2% YOY possible , cannot see a decade of flat market though - this investment class is always buoyant both on the upside and downside - good chat though - and thanks for that

How can a market be buoyant on both the upside and the downside? It's like saying the Titanic is unsinkable...

Well said Gingerninja & EcoBird, I agree with you both

..you make the mistake of many..that high demand must mean continued prices. Afraid not, inability to pay simply means we will have a reset of price.

Bad Sediment has set in now. Fear and competition has settled and no urgency left in peoples minds to think a 900k house in Glen eden is a great investment. With Chinese capital being nearly impossible to leave china pushing up prices the markets have to come back down to a realistic dti. It's logical.

Given the huge drop off in investor lending we should soon see a closing of the funding gap, and hence credit rationing, we've seen in recent times. I doubt deposits will continue to decline forever. If investors are now shunning both property and deposits, where are they putting their capital? Is there another Hanover event waiting in the wings?

"where are they putting their capital?" What capital? In aggregate the 'capital' was borrowed in the first place, hence the funding gap that needed to be sourced offshore. The credit squeeze that the banks have on at the moment has nothing to do with 'less borrowing' for property ( hence 'there must be more money in the system that HAS to go somewhere'), it is simply a matter of risk containment - by the banks and/or, belatedly, the Government.

There is no Magic Pot of Money looking for a new home now that property investors have been reigned in. All there is is a lesser requirement to borrow to fund that activity. But as prices fall, there WILL be less capital to redeploy....(ie: Capital : wealth in the form of money or other assets owned by a person or organization or available for a purpose such as starting a company or investing.)

What capital? You assume there is some real money in the New Zealand economy. Previous housing purchases were financed with debt and house equity which is also just debt. It's not like most investors were walking in with cash. If the market cools perhaps debt flatlines but there will be no river of cash with nowhere to go because there is no cash only debt.

David Chaston, I know you read CoreLogic's reports. In their latest report out last week, on page 26 it shows investors at 39% with a commentary staying the investors are back and not down at all yoy. I realise CoreLogic's is quartery but I'm still surprised at the stark contrast. I'm certainly not arguing the data you provided above but I would love your feedback. Thanks

That's the SHARE of Sales, not value. Look at value changes in the previous pages (eg pag 20,21). Note that Corelogic classifies based on number of properties registered to same owner, so some of this will be bridging and move from the 'MPO' line to the "Mover' line as they reclassify in the following months.

In terms of share, RBNZ figures show similar per C30 - around 35% of new commitments were Investor. The issue is, the whole market is 30% less YoY.

The market is going to be flat for along time due to the LVR alteration and election year, and China's restrictions.

Buy good property with upside providing it is positively geared.

Yes it is still possible but not Auckland.

The market is going to be flat for along time due to the LVR alteration and election year, and China's restrictions.

Buy good property with upside providing it is positively geared.

Yes it is still possible but not Auckland.

It's going to be worse than flat. 10% drop this year

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.