Here's my summary of the key events over the weekend that affect New Zealand, with news ASIC is about to tighten the screws on banks cross-selling policies.

First up however, counting in the first round voting for the French presidency is underway and far-right candidate Marine le Pen looks like she will come in second behind centrist Emmanuel Macron. The have 23.7% and 21.7% of the vote respectively and face each other in a runoff on May 7. Another centrist candidate got 19.3% and the extreme left candidate got almost 19% and their supporters will now need to decide who to line up with in the second round. If the far left supporters don't vote in the same numbers, it looks like Macron will be the next president in France.

And speaking of political popularity, the latest WSJ/NBC political poll shows a clear majority of Americans think the new US president is doing a poor job. In fact, those polled want a more active government.

And staying in the US, their spring house selling season is off to a strong start. Existing-home sales rose by +4.4% to their highest pace in over 10 years. Supply shortages resulted in the typical home coming off the market significantly faster than in February and a year ago. Only the West saw a decline in sales activity in March. In fact, US mortgage rates dropped below 4% for the first time since November, providing more fuel for their housing markets.

Across the Pacific, China is claiming that the value of mortgages issued by its banks is actually declining, the result of a regulatory crackdown on over-exhuberant buying.

Moving south, the real estate froth may be easing in Australia. Auction clearance rates in Sydney eased back to 75.6% after several weekends of more than 80%, and it was a similar story in Melbourne.

The head of ASIC is raising the distinct possibility that banks may have to offer and sell products from its rivals. Under their drive to ensure customers interests are placed first, he says he will use his powers to police competition and "product intervention" could be used to ensure banks only sell products that are in the best interests of their customers – which might not necessarily be their own. And he wants new power to limit the ability of banks to "cross sell" customers additional products from by another part of the bank, a common tactic that boosts bank profits. (If this found its way here, maybe a Westpac 'adviser' would be obligated to offer an ANZ Kiwisaver option to its client? for example.) Customer-first policies are about to get new teeth rather than be bland corporate-speak, especially in Australia.

In the trade arena, the IMF and World Bank have dropped a pledge to fight trade protectionism from the closing note of their spring meetings. The IMF statement said members would "work together" to reduce global trade and current account imbalances "through appropriate policies". Meanwhile, Japan has picked up the ball and is advancing the idea that the TPP could be revived without the US. It has also rejected the idea that the US would get better trade terms from it outside the TPP than within it.

In New York, the UST 10yr yield is back up today and now at 2.25%.

Oil prices are dropping and now just over US$49.50 for the US benchmark, while the Brent benchmark is now just over US$51.50 a barrel.

The gold price is higher however, up +US$7 and now at US$1,285/oz.

The New Zealand dollar is marginally higher today at 70.3 USc. On the cross rates the Kiwi dollar is at 93.2 AU¢ but against the euro at 65.6 euro cents. The NZ TWI-5 index is just on 75.2.

If you want to catch up with all the changes on Friday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

16 Comments

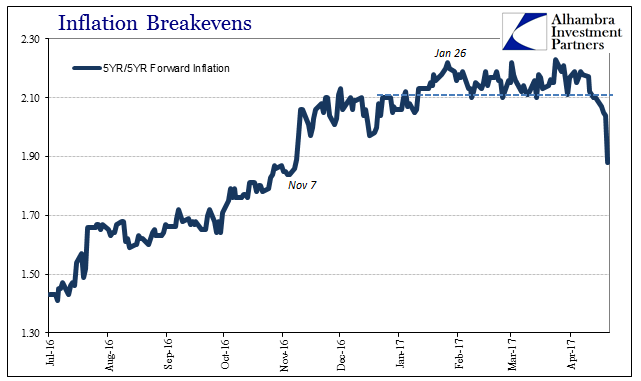

Analysis carried out at the Fed and elsewhere suggests that the decline in market-based measures of inflation compensation has largely been driven by movements in inflation risk premiums ,and liquidity concerns rather than by shifts in inflation expectations. [emphasis added] Read more

{kind=link}

Maybe, there are greater concerns than trade protectionism to consider? Sources willing to suppress a liquidity preference to finance cross border trade comes to mind. Do previously, acutely negative Yen and Euro cross currency basis swaps suggest otherwise?

The head of ASIC is an extremist. He's wanting more competition by banks selling the products of other banks. Essentially the collection of a commission and transfer of risk to another bank. That's exactly what led to the US sub-prime crisis and the toxic products traded in London. He then goes on to talk about "light touch" regulation. This means no regulation.

http://londonprogressivejournal.com/article/285/gordon-brown-and-light-…

Given that "light touch" was used in London, New York and Iceland I don't think this is a model that Australia should be following. It looks like the head of ASIC doesn't read much which would explain his incompetence.

He doesn't see the obvious answers to reduce their excessive privilege - break the big buggers up and require 20% to 30% real equity. It seems to work for the rest of us.

Everyone listed to Greenspan up until he admitted his career at the Fed was a mistake and that banks should have 20-30%. Unless the story is excessive leverage, and transferring the risk of financial products to third parties then no one wants to know about it.

The financial sector wants to become the economy at the expense of everyone. It's not a sustainable model.

Also from Mervyn King, former Bank of England governor:

“During the 20th century, governments allowed the creation of money to become the byproduct of the process of credit creation. Most money today is created by private sector institutions – banks. This is the most serious fault-line in the management of money in our societies today,”

More from the "Maestro"

In terms of monetary policy, Greenspan long ago recognized that there wasn’t any anywhere in the world. As early as 1996 in his infamous “irrational exuberance” speech, there was the “maestro” admitting that the very concept of money had long ago gotten away from central banking.

"Unfortunately, money supply trends veered off path several years ago as a useful summary of the overall economy. Thus, to keep the Congress informed on what we are doing, we have been required to explain the full complexity of the substance of our deliberations, and how we see economic relationships and evolving trends."

"There are some indications that the money demand relationships to interest rates and income may be coming back on track. It is too soon to tell, and in any event we cannot in the future expect to rely a great deal on money supply in making monetary policy. Still, if money growth is better behaved, it would be helpful in the conduct of policy and in our communications with the Congress and the public."

Did money ever become “better behaved?” Of course not, as it was just as unreasonable to suggest then as it would be to do so now twenty years later. We need look no further than Greenspan’s own words in June 2000 to settle that issue:

"The problem is that we cannot extract from our statistical database what is true money conceptually, either in the transactions mode or the store-of-value mode. One of the reasons, obviously, is that the proliferation of products has been so extraordinary that the true underlying mix of money in our money and near money data is continuously changing. As a consequence, while of necessity it must be the case at the end of the day that inflation has to be a monetary phenomenon, a decision to base policy on measures of money presupposes that we can locate money. And that has become an increasingly dubious proposition."

How that doesn’t disqualify him and all his compatriots from further discussion about money and especially economy can only be a matter of ideology shared not just among economists but with the media itself. His Fed abandoned its primary mission because math; regressions alone told him and the rest of them that interest rate targeting would be sufficient monetary control even though there was every indication that just wasn’t the case. As his ability to define and measure money had only become worse by the middle of 2000, perhaps the gigantic stock bubble that had just burst was enough of a common sense clue that what was wrong in money shouldn’t have been so easily dismissed.

Even in what he said at that FOMC meeting, which is a matter of public record, you would think that any central bank caught in a position of not being able to define money would immediately change that. Read more

Perhaps the real rate of inflation is actually 10.5% per annum. Gold in Euros was EUR 400 in 2005 and EUR 1000 in 2015. My calculation goes something like this; ((1000-400)/10*400)*0.7*100 = 10.5%, the 0.7 factor is to strip out compounding.

http://charts.kitco.com/KitcoCharts/index.jsp

11% is also about the expected return on commercial property in NZ.

So about the rate of new euro creation.

The rate of money creation rate is the inflation rate for investors. The CPI is just consumer inflation. When the rate of money creation is that high it's a work around so that consumers are being shafted if they want to do anything other than consume. Perfect for transferring wealth upwards, destroying the middle class and positioning housing to be out of reach of each new working generation.

On a lighter note, Fekete says the Bank of England Gold Standard was designed by Sir Isaac Newton, I didn't know that.

For a number of years I have been working on a plan to reestablish gold coin and gold bill circulation that, in promoting peace and prosperity would equally benefit all nations. I came to the conclusion that the British sovereign was the most eligible coin for the purpose. It is the oldest coin that has been struck continuously at the Royal Mint without changing its in weight or fineness through many a year of peace, wars and revolutions. The sovereign financed world trade successfully between 1815 and 1914 and is fully capable to repeat this feat during the next one hundred years. It has the highest name-recognition of all coins ever struck anywhere. It is known and hoarded in all countries of the world. The sovereign is hall-marked with the name of Isaac Newton, ‘humanis generis decus’, Master of the Royal Mint and the father of the gold standard in modern times. On its reverse the sovereign depicts St. George in the act of slaying the dragon. Surely the symbolism will not be lost on people long suffering from the ravages of the global experiment with irredeemable paper currency, nor on producers of gold long unfairly prevented from bringing the benefits of their product to the world.

http://www.professorfekete.com/

He also invented a lot of the anti-counterfeiting technologies. Isaac Newton was a clever hard working chap.

I am in awe of his achievements due to his contributions to Physics and Mathematics, but it seems his wisdom has permeated even more widely.

Given the openly hostility coming from the media I am surprised that Trump's poll numbers are as high as they are.

The US media is in an echo chamber listening to its own made up anti-Trump narrative , and the US public are simply not not buying it anymore .

Its a sad situation where journalism has in many cases become a dishonest profession, and has been bastardized by lies deceit and false reporting to the point we need to question everything we read.

I am left astonished at some of the things Trump is alleged to have said ( by certain media outlets ) only to go onto the internet and look at the actual clip, only to see he said no such thing .............its distorted to the point one cannot imagine how the media gets away with such lies without consequence

Its refreshing to read that boatman.

http://www.oftwominds.com/blogapr17/long-game4-17.html

The Neocon camp has also ordered its media arm--the corporate-owned mainstream media-- to go into full attack mode. Bernie Sanders got a small taste of the MSM's one-sided, negative coverage, but that was merely a training exercise for the main war against any and all potential threats to the Neocon camp's total dominance.

What's up with the date; or has DC suddenly got clairvoyance?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.