Here's my Top 10 links from around the Internet at 10:00 am today in association with NZ Mint.

Bernard Hickey is still on vacation, but he will be back on Thursday.

I welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

I am still keen to get your suggestions for suitable cartoons. If you notice a really good one, please email me.

See all previous Top 10s here.

1. New 'security' arms race

The granting of approval by the RBNZ for local banks to issue 'covered bonds' is part of a corrosive trend. Investors are giving rising importance to 'secirity' when they make their investments, and a senior official at the Bank of England has warned about a 'safety' arms race. Unsecurred depositors are being pushed further back in the claims ranking by the emergence of more senior and more specifically secured borrowing instruments being launched worldwide by banks.

The traditional 'negative pledge' arrangements we have all relied on are being eaten away. And you would want higher returns for your more risky position, wouldn't you? The full copy of the BofE remarks are here », and this is a key part of what he said: (its a .pdf. see page 9)

The larger the existing fraction of secured financing, and the greater the uncertainty about this fraction, the greater will be their incentive to seek security. Not to do so runs the risk of other creditors leapfrogging ahead of them in the seniority queue. Creditors’ incentives are very similar to those during a bank run, except with investors now seeking security rather than immediacy.

As with a bank run, this dynamic risks becoming self-fulfilling. The greater the level of, and risk around, encumbrance levels, the higher the return unsecured creditors will demand given the risks of subordination. And the higher this cost, the greater banks’ incentives to finance instead on secured terms. Both banks and their individual investors have incentives to encumber the balance sheet by progressively - and self-fulfillingly - larger amounts. There is an arms race spiral.

2. 'It wasn't me! Honest. It was them'

Joseph Stiglitz is an academic economist and a Nobel prize winner. He is forthright and a go-to authority when you need criticism of other economists.

He is no fan of politicians either, especially European ones. Here he is in a recent interview in The European:

Academic economists played a big role in causing the crisis. Their models were overly simplified, distorted, and left out the most important aspects. Those faulty models then encouraged policy-makers to believe that the markets would solve all the problems. Before the crisis, if I had been a narrow-minded economist, I would have been very pleased to see that academics had a big impact on policy. But unfortunately that was bad for the world.

After the crisis, you would have hoped that the academic profession had changed and that policy-making had changed with it and would become more skeptical and cautious. You would have expected that after all the wrong predictions of the past, politics would have demanded from academics a rethinking of their theories. I am broadly disappointed on all accounts.

"Trade deficits cause fiscal deficits"

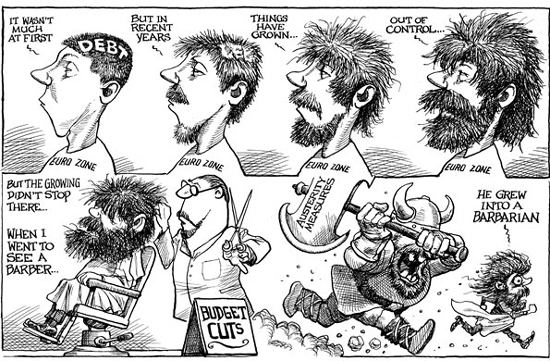

3. 'We need more deficit spending'

Fiscal austerity is 'not working' in the Eurozone. This is a problem because fiscal looseness (irresponsibility) cause the problem in the first place. The issue is that no-one wants to acknowledge that economic pain is a price that has to be paid for that irresponsibility. Some people think that because a solution causes pain during the rebalancing, it is not working. Some columnists support the idea that 'rebalancing pain = failure". Martin Wolf is one and he has the charts to prove it.

I have this sense that we have seen it all before. The NZ finance company collapse was fuelled by 'investors' who wanted high returns, no risk, and no work. A whole bunch of companies sprung up to indulge them. And when it went horribly wrong, those 'investors' pointed their fingers forecfully. Mainly they wanted someone else to mitgate their pain.

In Europe, we have something similar, but on a far grander scale. The whole idea that a sustainable recovery can come about painlessly from here through the magic of moneyprinting mystifies me. Here is Paul Krugman in the NY Times (he is also a Nobel Prize winner):

For the past two years most policy makers in Europe and many politicians and pundits in America have been in thrall to a destructive economic doctrine. According to this doctrine, governments should respond to a severely depressed economy not the way the textbooks say they should — by spending more to offset falling private demand — but with fiscal austerity, slashing spending in an effort to balance their budgets.

Critics warned from the beginning that austerity in the face of depression would only make that depression worse. But the “austerians” insisted that the reverse would happen. Why? Confidence! “Confidence-inspiring policies will foster and not hamper economic recovery,” declared Jean-Claude Trichet, the former president of the European Central Bank — a claim echoed by Republicans in Congress here. Or as I put it way back when, the idea was that the confidence fairy would come in and reward policy makers for their fiscal virtue.

4. History lesson

Louis Hyman at Bloomberg reminds us that mortgage-backed securities have failed before. We took a long time to forget the consequences, but we did. And then we made the same mistakes again.

Time magazine reassured readers in 1926 that "real estate bonds are by no means jeopardous investments. In fact, they should be the best of all securities, for they are backed by tangible buildings and real estate."

Such reasoning reassured investors then, as now, about the inevitability of rising house prices.

Banks loved the new invention because it allowed them to skirt regulations. Although the Federal Reserve regulated the proportion of savings that could be lent as mortgages (half of savings deposits) there were no restrictions on mortgages funded by bonds. These bonds, however, had a maximum length of five years, forcing the mortgage debt to be refunded, at minimum, every five years. But since the balloon mortgage, so popular in the 1920s, was refinanced every three to five years, there shouldn't have been a problem as long as more investors could be found.

5. Can gold really be used as currency?

Felix Salmon, a Reuters blogger, tried to buy stuff using a gram of gold as the medium of exchange. He reports "it worked, kinda". The problem was he had to find some store person who only knew vaguely about the issue and someone who could be convinced on the spot that they were getting a 'good deal' - ie better than paper money. And he had to pay 50% more for his actual gold than the paper money equivalent. Not very convincing.

I think the only thing he really proved is that gold is more like play money.

Most interestingly, however, at least to me, was how much it actually cost us to obtain that gram of gold. For the purposes of the video, I was using the value of one gram of gold based on its market price per ounce. But if you go out and attempt to buy a gold bar, you’ll never be able to find one for a mere $53. In fact, my producer wound up paying double that, in Manhattan. Even if you do a lot of searching online, you’ll be hard pressed to find one for less than $80. We didn’t try to sell the gold — we wound up getting a delicious lunch instead — but my guess is that in most cities the effective bid/offer is absolutely enormous. And much bigger than for any major global currency.

6. Urban planning for dummies

Yes, there is a new book out with that title, in the Dummies series. But do we really want a bumch of dummies planning our cities?

Yes! Absolutely. And who do you think is doing it already anyways? That's the point. If the people who are already involved in planning did things just a little bit better and had a little bit more of an opportunity to make those dialogs work and more people came to the table, I think that provides the opportunity to do things with cities, especially the really hard things, like saving energy and putting things closer together and doing transit oriented development. Big issues change a lot of peoples' lives, and that makes them hard to do. A lot of professional planners, I think, are very gunshy because if you propose big things you have to deal with a lot of people. There are many opportunities to get a good combination of big picture and little picture issues out there. Having more dummies planning cities is, in fact, what we want because that’s who lives there and that’s who needs to be on board if we're going to make the really big changes that we need to make.

7. Pandering to a [very] privledged class

Helping people with student loans has bipartisan support in the US - Barack Obama and Mitt Romney both support it. It's pretty popular in New Zealand too - in fact we make such loans interest-free. You can't get any more supportive than that, except by writing off those loan, and there are folks in New Zealand who want that too.

It's classic middle-class welfare - giving benefits to voters and underpinnig unions, rather than to those who really need it. Invented by the left, retained by the right who are too scared to reform.

Here's a journalist who reckons its just plain wrong:

As a class, we've already benefited from subsidies to higher education, we've acquired human capital and a credential that sets us apart from most people on the planet, and we're certainly not the Americans in most dire need of help, though we are more politically influential than the less fortunate. "If we think it more important to spend this dough on education," says Will Wilkinson, "then we should hand out the $6 billion in the form of scholarships to deserving prospective collegians of modest means, to help them earn their degrees without having to take out any loans at all."

And, here's another perspective. The Americans are talking about an US$6 bln subsidy. In New Zealand, our subsidy is NZ$1.6 bln for student loans in addition to NZ$2.0 bln that the taxpayers pay directly for the courses. On an equivalent per-capita basis as the US, we are spending about twelve times as much. Make sense to you? You really think the educational and social outcomes are better here than the US, let alone twelve times better?

8. What's about to happen with fixed mortgage rates?

Changes in wholesale money costs have an approximate relationship to the pricing of mortgage rates. Recently, we have seen quite a sharp fall in NZ swap rates - they are down some 40 bps points in the past month or so. Maybe the reductions will keep going if the Aussies reduce their official rates as expected tomorrow. Anyway, you would expect that such a fall in wholesale costs would open up the prospect of pricing reductions for fixed mortgage rates.

But as you can see, that fall followed a 60-70 bps rise since the start of the year, one that did not result in rising mortgage rates. Do you think a fall in carded fixed mortgage rates is coming? Are the banks hungry enough for market share, or desperate enough to protect the size of their mortgage book? If one small one (Kiwibank?) moves will a big one follow?

9. China is being buried alive in copper

Some people think the Chinese are hoarding copper. Their stocks of the metal seem far in excess of what they may need. The reasons may be strategic, they may be psychological, or there could be a weird regulatory incentive. Here is the FT to help you choose:

According to Wikipedia, compulsive hoarding is a disorder characterized by the excessive acquisition and inability or unwillingness to discard large quantities of objects that would seemingly qualify as useless or without value.

We’d like to make the case that China is suffering from this disorder and that we’re at the stage where a psychopharmacological intervention needs to be organised by China’s friends and family. If not China’s hoarding tendencies could destroy the world as we know it.

10. The last laugh

Homer does an ad for Mastercard.

18 Comments

Low interest rates are coming at a cost

QE quadruples FTSE 350 pensions deficit in one year Pension deficits at the country's biggest companies have quadrupled in 12 months in the wake of the Government's quantitative easing policy.

http://www.telegraph.co.uk/finance/personalfinance/pensions/9232364/QE-…

BazzaMcKenzie

For the money printing shysters, every day they keep themselves in office through this theft is a success. That the lives of others is thereby destroyed is of no consequence to them. They are all sociopaths.

China is not hoarding Copper per se, as in hoarding in order to ensure supply etc.

In China commodities esp Iron Ore, Copper, and other metals, "stockpiling" is used as a medium of finance. Since Banks lend at a higher amount and at a lower rate for such commodities, traders use this stockpiling as a means to finance their other business (eg property speculation ). This is a very common practice in China. (until the commodities price crash leaving the Banks a big hole in the balance sheet and their borrowers bankrupt)

The growing Bank's margin also shows why Banks are still making huge profits even though the economy is treading water. Unfortunately most banks are still hiding and projecting losses and so this increase margins will not be going away soon. (also the reason Oz banks are trying to disconnect their lending rates from their OCR)

As for Gold, sooner or later the fiat money system will implode, esp if Euroland breaks up (sooner rather than later if Hollandie wins) and ECB pumps liquidity again to stem panic.

Time to get the safe deposit box ready again.....

#3 "The NZ finance company collapse was fuelled by 'investors' who wanted high returns, no risk, and no work". Sounds a bit like property investors and the outcome will eventually be the same. Of course the finance companies were just an alternative route to investing in real estate.

Absolutely. The established fiat-lenders were just capable of holding on longer. The question is how much longer?

5. Can gold really be used as currency?

My understanding is that Gold is more useful as a settlement mechanism between nations.

For instance there has been talk of India and China paying for their Iranian oil with Gold.

Central Banks accumulate Gold not so much because their citizens like Gold, but because they see Gold as useful in the future when international fiat currencys(eg the US dollar) will be called into question.

Deficit Spending In Action

Mr Krugman thinks you can spend your way to prosperity and is vocal against those who suggest any kind of austerity, but what about the British example (note that British GDP is about $1500 Billion a year so these are big figures):

- Borrowed $500 Billion pounds

- Depreciated the pound by 20%

- Pegged interest rates at .5% for more than three years

- Bank of England put $325 Bilion pounds of new money into the system

http://www.guardian.co.uk/politics/2012/apr/25/double-dip-recession-george-osborne?CMP=twt_fd

And so the net result of following Mr Krugman's advice has been (drum roll plse)?

Double dip recession.

Hugh Hendry is back with a bang after a two year hiatus with what so many have been clamoring for, for so long - another must read letter from one of the true (if completely unsung) visionary investors of our time: "I have not written to you at any great length since the winter of 2010. This is largely because not much has happened to change our views. We still see the global economy as grotesquely distorted by the presence of fixed exchange rates, the unraveling of which is creating financial anarchy, just as it did in the 1920s and 1930s. Back then the relevant fixes were around the gold standard. Today it is the dual fixed pricing regimes of the euro countries and of the dollar/renminbi peg."

http://www.zerohedge.com/news/hugh-hendry-back-full-eclectica-letter

Andrewj - Thanks for the link to Hugh Hendrey's latest client newsletter, he is always an interesting read.

Re Item 7

Pandering to a [very] privledged class

We have been conned into making our children borrow money to get an eductaion. Calling it middle class welfare is just plain wrong. Children are not middle class, they are poor. They might have middle class parents they might not. But they themselves are not middle class.

The loan approach is an accounting trick to make the books look good- look how much money the government are owed- that sort of stuff.

Progressive taxation used to be the mechanism by which society got back what it had put into education.

Instead now we have been conned into debt as a solution. It is not.

Harvard do not charge fees for its students- they simply have to be good enough to get in.

Our loans mean that we pay to educated out children today out of current income. There is no other way. The loan is an accounting trick and a load of nonsense. But if you repeat something stupid often enough, people will believe it.

More on Item 7

It's classic middle-class welfare - giving benefits to voters and underpinnig unions, rather than to those who really need it. Invented by the left, retained by the right who are too scared to reform.

So if you actually believe any of this nonsense why not do the right thing and bring in Student loans at 5 years of age. After all it is the early years that matter most. Why should those 5 year olds get a free ride. Its crazy. In a couple of years they will all be in London earning millions trading currency, why should your money go towards teaching them to read write and count. It is just crazy. Make them stand on their own feet and pay their own way.

Of course people give benifits to themesleves because they can see the benifit of doing so. We live in a democracy where every person over the age of 18 and not in prison has a vote. What is wong with voting to make sure that children get eductated.

At some deeper level, what is the point of anything- surely the only real point is to bring children into the world and look after them, educated them, feed and cloth and house them.

As Sir James Goldsmith esentially said, the economy has to work for us, not us for it.

Your focus should shift to student allowances - not limited to the loan scheme. These allowances cost over half a billion dollars a year, are non repayable and supposedly for low income earners. However, we all know they are going to those who syphon off their income into trusts and companies. At least student loans are in theory repayable, unlike the allowance.

.

In the US student loans have gone in tandem with massive inflation in the cost of education. Isn't it strange how whenever there is plenty of debt floating round we get inflation.

Um, Plan B (or is the latest iteration C or D or even E?)

The simple cause was first noted by Philo of Alexandria. It has recently been re-popularised by Glenn Reynolds (InstaPundit).

It's good to see the recognition dawning that Democracy, as currently constituted, results in the Tax Consumers (and here we must count students as primarily Consumers rather than Producers of tax) , voting themselves more goodies from the Magic Money Tree.

And of course, Tax Consumers well outnumber net Tax Producers. So the goodies flow...

This was the basis for Ben Franklin's parting quip - to the effect that here's your Republic - if you can keep it.

But Education (disclosure, I was the CFO-equivalent of a large Polytechnic back in the day, so see this with an insider's POV) has long since subsidised Markers, not Traits, to use Reynolds terms. And the NPV of most education schemes (which emit such productive outputs as Circo-Arts, Aromatherapy, and Tourism/Travel) is most certainly negative. That is, the current cost of the boondoggle is more, much, much more, than the increment in a student's future income streams, across a very wide slice of 'education', at any discount rate you care to try.

This has three highly undesirable results.

- It produces a false sense of entitlement in the student population, in terms of jobs available and incomes attainable. This is not good at a personal level.

- It then produces a sense, 3-5 years down the track, of betrayal as the gold turns out to be gilt, and a check-out position looms for those eager young BA's. This is not good at a societal level.

- It has consumed, permanently, resources not therefore available for other projects, not least not available to the originators of the tax money involved. This is not good at an economic level.

What, in fact, we are looking at there is nothing more or less than a Bubble.

Class of 2012, Discuss!

Regarding hoarding copper, maybe it is simply that the Chinese have been looking at this graph

Opps! and here is the graph : http://www.smithsonianmag.com/science-nature/Looking-Back-on-the-Limits…

Good link.

If you highlight it and click the 2nd icon from the right (above when you're commenting)

http://www.smithsonianmag.com/science-nature/Looking-Back-on-the-Limits-of-Growth.html#

It comes out like that.

:)

Ok thanks.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.