Yesterday we reviewed the 2016 mortgage rate trends, and noted that the largest bank not only had the highest rate offers during the year, they ended the year with the highest [two year fixed] rates as well.

Today, I want to look at market shares more closely.

And what we find is that same bank is gaining market share.

And those gains are not insignificant.

They are gaining on their four main rivals, capturing significant new share, leaving those rivals with languishing market positions.

The richest is getting richer; the biggest is getting bigger.

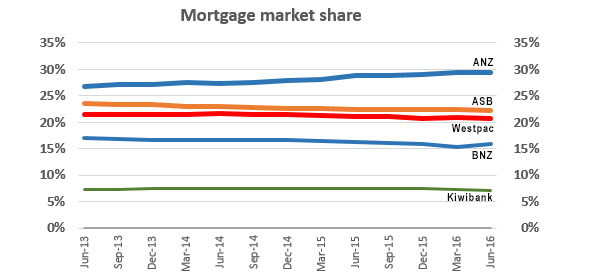

Here is the key fact; in the three years to June 2016, ANZ won 40.3% of all new mortgage business, even though it started with just a 26.7% share.

In the 12 months to June 2016, it won 35.8% of all new business.

Mortgages now represent 55.4% of all its loans, a record high for the bank. Commercial and other personal lending are now a minority part of its business.

Meanwhile, the rivals that could challenge it are going backwards.

ASB has seen its market share fall to 22.3%, down from 23.5% three years ago.

BNZ has seen its market share fall to 15.8%, down from 17.1% three years ago.

Kiwibank has also struggled to keep up its earlier market gains. Its market share is now 7.2%, a slight slippage from the 7.3% it had three years ago.

And Westpac has also gone backwards. Its market share is now 20.7%, down from 21.6% three years ago.

All four rivals are conceding ground to ANZ.

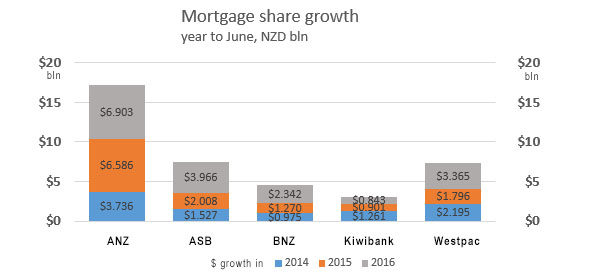

The minnows don't count; ANZ grew in 2016 by more than the total mortgage loan book of HSBC, SBS Bank and TSB Bank combined.

SOURCE: RBNZ G1

In a rising interest rate market, what can its rivals do to stop being run over?

in 2016 we saw that customers ignored ANZ's higher interest costs of up to 25 bps.

A new strategy is required; new tactics are needed.

The problem is that shareholders (especially Aussie shareholders) want their returns and dividends without having to stump up any more capital. Management of all banks are under pressure to keep the profits flowing in the short term. And their bonuses depend on this. Blind eyes are being turned to the atrophy in market share. A short term game is being played here.

Another problem is that mortgages are a commodity, and the cheapest funding goes to the largest player, reinforcing its dominance and its ability to punish rivals who threaten it.

Another brutal fact is that Kiwibank is in no position to shake things up any more - unless its new NZ Super Fund and ACC shareholders are in for a long game of low margins to chase a meaningful market share objective.

It will make for an interesting market to watch in 2017, one that may not benefit borrowers, or in fact any of ANZ rivals.

It is not hard to see [a more activist] Commerce Commission perhaps taking a new interest in our biggest oligopoly. Don't hold your breath, but at some point unless current trends change, 'new management'; at the competition regulator could take an interest.

SOURCE: RBNZ G1

11 Comments

Chasing market share is all very well until interest rates rise and mortgage collateral becomes severely compromised. In that scenario, the bigger the market share, the bigger the capital losses. It is all very symptomatic of today's short term thinking...

Could it be that the ANZ is actively looking for customers requiring mortgages and the others are sitting back ,happy with their share or is the ANZ just that much better in the self promotion game.

I have had personal loans and a mortgage with them in the past and never really got the feeling that they valued my business in fact just the opposite.

I had a friend with Westpac, he purchased another house (he is a landlord and property speculator). Westpac wanted so much security that he wasn't going to do the deal, ANZ were more than happy to lend to him with much less security, so he changed banks and is now out looking for more 'deals'.

That's a good thing, is it?

I find it easiest to get morgages off anz I went to the other three main banks and they all wanted to charge commercial rates as it was for a block of flats.anz we're had way cheaper rates than the other three

Looks like ANZ is the bank to avoid if you want to minimise the risk on your deposits.

Clearly they have been absolutely outstanding in lending more recklessly than other banks.

Peri, I completely agree. The fact that our largest bank is also the one lending most recklessly is very troubling. It's pleasing to see other banks responding to a perceived increase in credit risk, but it doesn't mean anything if one of the big four fails to toe the line.

Generally in financial markets ANZ I understand are thought to be in the best shape. The honest truth is that if one gets into trouble they all will. They have all been made to dramatically increase their capital over the last few years.

The big issue out there are the moment is some developers are in trouble due to escalating costs.

ANZ is in "better financial shape" than their main rivals, if you use overall leverage as the criteria. See this comparative. But they have actually gone backwards since late 2014. ("Gone backwards" = increased their leverage.) It is not a welcome trend. That is, they have grown their lending faster than the capital in the business on a relative basis. And part of that is because the Aussie regulator is requiring ANZ to move money from NZ to AU.

What is the turn over rate for mortgages between one bank and another. Once a bank has your mortgage there is generally little incentive to change, not just the cost but the inconvenience of change, the uncertainty of future interest rates and relationship with the bank. The aggressive approach to growing their mortgage portfolio will pay dividends in the medium term.

The time most people in the street will change banks/mortgages is when they sell and buy a new house/property.

Will there be a timing issue in these two data points David?

The advertised rate comparison was 12m ended Dec whereas this mortgage growth is 12m ended June... notwithstanding that advertised rates are usually discounted, the two time series may be misaligned.

"Richest getting richer" probably requires more disclosure statement analysis, i would have thought...

Still its clear they are getting bigger in terms of net growth and may be worrying for smaller players.

But the big headline is $20b in mortgage debt growth! Yikes, thats a lot of coin. Its probably worse for 12m ended december.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.