By David Cunningham*

New Zealand’s latest inflation stats mark a big turning point in our battle against the monster.

For the first time in more than two and a half years – or 10 consecutive quarters – December’s numbers saw quarterly Cost Price Index (CPI) inflation sitting below 1%.

It’s the clearest sign we’ve had yet that the pandemic-fuelled inflation surge, felt the world over, is finally coming to an end. In fact, inflation is now falling dramatically in most Western economies.

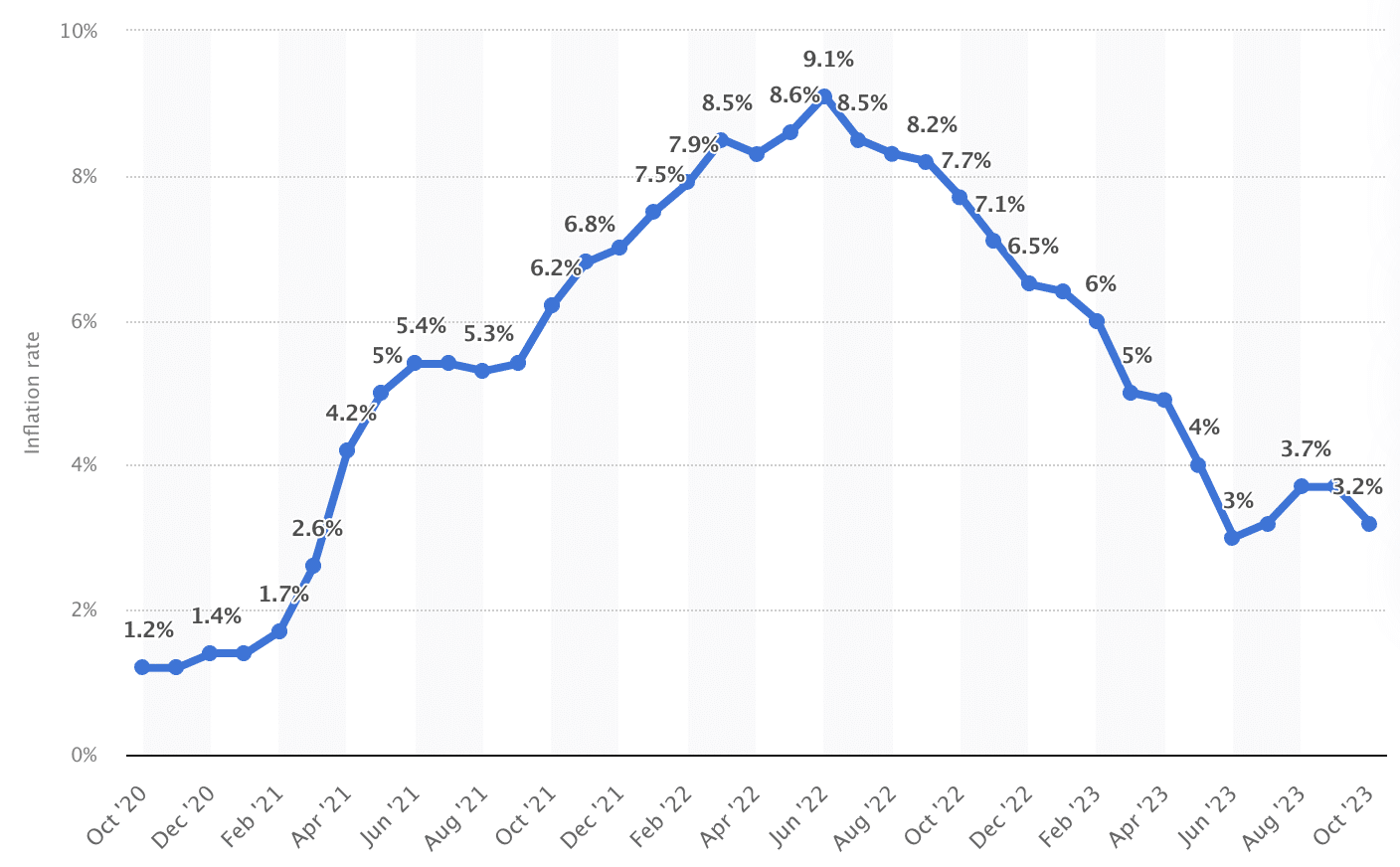

The chart below tracks New Zealand’s quarterly and annual inflation rate over the last few years. It’s fair to say that things were going pretty well up until late 2020, when the aftermath of Covid really started to cause havoc – with quarterly inflation averaging around 0.5%, or 2% total per annum.

And actually, if we were to extend the chart back even further – right back to 2000 – it’s the same story, meaning quarterly inflation averaged 0.5% for roughly 20 years before this latest spike.

With a remit to keep annual inflation somewhere between 1% to 3%, that’s not a bad outcome for the Reserve Bank of New Zealand. Bang on the mid-point of 2%!

So where is inflation headed now?

One of the best ways to get a gauge on where annual CPI figures are going is to take a look back at where quarterly inflation stats have been.

We saw some big quarterly inflation numbers in 2023 – 1.3% in March, 1.1% in June, and a massive 1.8% in September (when the Government removed the petrol discount, a.k.a. fuel excise tax reduction).

As we move forward, those numbers will – one by one – start to drop out of the total annual inflation calculation as new quarterly data is released.

Assuming actual quarterly inflation remains low over the coming quarters, annual inflation is likely to fall pretty rapidly as those high historical numbers are bumped from the equation.

To demonstrate, the new (illustrative only) data on the right-hand side of the chart below shows how annual inflation would track if quarterly CPI inflation were to return to that 0.5% level that’s been the average for most of the century.

As you can see, those numbers would have annual CPI inflation back at 2% by September this year. It’s a hypothetical scenario at this stage, but it feels like it could be a reasonably realistic one.

What does this mean for interest rates?

A rapid decline in inflation would likely see short-term interest rates fall significantly over the next year.

It’s exactly what wholesale markets are pricing to happen – despite cautious rhetoric from the Reserve Bank as part of its last Official Cash Rate (OCR) announcement of 2023, which suggested that it was likely to be 2025 before OCR cuts start to come through.

For longer-term interest rates, there’s likely to be a continued downward drift as we creep closer to anticipated OCR cuts.

Right now, some economists are forecasting the OCR as low as 3% in a couple of years, implying a lot more downside in longer-term interest rates.

Impact on home loan interest rates

For starters, bank interest margins on fixed-rate home loans – a.k.a. what they charge over and above where wholesale interest rates are at – are currently extremely wide.

The bank margin on one-year fixed home loan rates, for example, would normally sit somewhere between 1.0% and 1.5%, but at the moment it’s up at 2.0%.

That’s just one side of the story, though. We’ve also got to consider what’s happening with term deposits.

The rates currently being offered on six-month and one-year term deposits are hugely competitive – to the point where they’re actually making the banks a negative margin (i.e. a loss) of about 0.75%.

Until those term deposit interest rates fall, there’s limited relief in sight for home loan borrowers.

But when it does happen, sooner or later, that will be the catalyst that sets home loan interest rates tumbling down again.

I think it’s pretty realistic to expect the one-year fixed home loan rate to be sub-6% by the end of 2024, and sub-5% by the end of 2025.

The interest rates rollercoaster is in for some serious action!

*David Cunningham is CEO of Squirrel, a mortgage broker that also offers peer-to-peer lending and savings and investment products and services. This article first ran here and is used with permission.

60 Comments

‘Tumbling down’ is a bit of an exaggeration.

Nonetheless, I agree with his central position

Compare this well reasoned analysis, based on empirical evidence, to the drivel we get fed from NZ's bank economists. Chalk and cheese!

I too agree with the position.

But others may not. For them to be taken seriously they'd need to show that something quite different will happen this time. I can't see anything different. If people do - please share.

There is a big difference in the US - massive increase in interest rates but no recession, the opposite in fact. Markets are pricing in a rate cut based on past history, but it’s not panning out like normal.

The US is humming along because nobody ever mentions the huge amount of stimulus their government is throwing into the system. This won't last. (Even if Biden gets back in.)

As you say "Markets are pricing in a rate cut based on past history". Indeed they are. Past history shows that when the governments take back the punchbowl (pull back on the stimulus) their economy will contract quite quickly and central bankers will respond by dropping rates quite quickly.

It all looks like it is different at this juncture. It always does. But its not. We're just at the inflection point where things appear to be humming along and optimism we've dodged a bullet reigns supreme.

Scratch the surface and you can see signs of contraction coming more swiftly (more announcements of layoffs led by the ICT sector (as per normal), rumors of debt stress in commercial property, massive real estate write-downs looming, hovering indicators showing neither down nor up (trendless), global engines of growth (e.g. China) having major issues, etc.)

There are always signs of contractions somewhere. Economists are always incorrectly calling recessions. IMO there is nowhere near enough evidence to say the US is heading into recession and needs a rate cut.

You may be right, they may be too late yet again, but that is the lesser risk compared to lowering rates too early.

.

He has had this position ever since rates started going up. Finally has an objective basis though now, rather than simply trying to drum up business.

re ... "He has had this position ever since rates started going up. Finally has an objective basis though now ..."

Not so. Bouts of inflation caused by supply shocks (including energy shocks) run to established patterns and timelines.

Most economists would have mapped out what would happen after the RBNZ dropped rates to extremely low levels while throwing heaps of cheap money into the system. And all would have been in broad agreement.

The public arguments you saw then, and see now, between respected economists are about degree and timing - and not the overall likelihood of what would happen, and what will happen.

My view, and clearly Mr Cunningham's, is that we have an uncompetitive banking oligopoly maximizing their profits because they can do so with impunity - while using 'inflation' and a 'difficult economic environment' as a cover.

ComCom has much work to do.

This is hardly drumming up business. I’d be waiting based on this if I was thinking of getting a mortgage

I agree it’s probably the most likely scenario give or take 1%. However I certainly wouldn’t rule out a much slower rate of OCR decreases or even none at all. The US is looking a bit bubbly, it’s hard to see any significant rate cut there when their economy is going strong, that leaves the RBNZ in an even more difficult position.

I think the currency concerns are a bit exaggerated

Hard to know. Our currency improved a lot against the US after the GFC as our interest rates were a lot higher and we were the rockstar economy. Could be the exact opposite soon, why would anyone want NZD?

Just reading the title I would agree (first time ever with the biased Squirell lol) that 5.99% end 2024 and 4.99% end 2025 are very possible.

Do you see the RBNZ making big cuts, 0.5% or more in one go? I think it will be cautious 0.25% cuts unless the fan is really hit. So they would need to start soon to have sub 6% rates this year.

And even if central bank does deliver 4 x 0.25% cuts this year and next, are the big banks going to rush to quickly pass it all on??

His central position seems to be that if future inflation rates are low (like 0.5% per qtr, hypothetically) then interest rates will likely fall…. Wow, what a revelation!

But what if quarterly inflation doesn’t magically go from over 1% per qtr recorded over the last several quarters to an immediate 0.5% flatline? What if the Fed doesn’t cut in March because of unexpectedly high jobs growth? What if oil doesn’t stay at its current low price? I don’t have all the answers but I suspect his position is optimistic, befitting of someone selling mortgages

It could be lower than 0.5 of course

Lol... 'But when it does happen, sooner or later'...

We broke to refix in 2021 for 3 years at 2.6% after purchasing our first house in 2020. Wish we had gone for 5 years! Despite the downward trajectory predicted, even 5% after 2.6% is a significant jump. We will manage as I suspect will most people, aside from any major life events (touch wood).

I had to break a 3.05% fix for 5 years in late 2021 as we traded up. Unfortunately the bank was adamant we had to discharge the old mortgage and take out new lending. Was ~$130k and our new loan size is basically quadruple, works out to be about $100 extra per month the bastards....

Ended up with a 4.95% fix for 5 years, which might turn out quite nicely as we'll be up for renewal December 2026 and *hopefully* we can refix at a similar rate.

There are a lot of people who got stuffed by the banks saying 'no' when they tried to break and re-fix at the low rates.

The court cases and class actions will appear in time as they work through the various processes required (e.g. the Banking Ombusman service who make so many mistakes and are the subject of complaints themselves) before it arrives before a Judge.

ComCom has a lot of work to do here.

Back in 2017 when inflation was around 1.8% and the OCR was 1.75% we still had one year mortgage rates of around 5% and floating of around 6%.

Unless the world shuts down again I don't think you should expect sub 5% rates any time soon.

LOL. You may want to check your facts there. (And I'd also mention that rates were in a downtrend and banks we being criticized from the RBNZ on down for not passing OCR cuts on.)

These will help:

Fixed mortgage rates: https://www.interest.co.nz/charts/interest-rates/fixed-mortgage-rates

OCR: https://www.interest.co.nz/charts/interest-rates/ocr

Facts.

Feb 2017

https://imgur.com/a/9l0QSKF

Feb 2018

https://imgur.com/a/4M8XGyU

We also had a relatively robust economy. I think our economy will be in a bad shape by mid year.

of course that’s only relevant in terms of the OCR if it nukes demand and inflation. Which I think the current setting will probably do

Tl;dr fix for 6 months, folks.

Which is what the article suggests.

Let's keep in mind this author's business and livelyhood depend on people taking out mortgages.

Retail interest rates will come down, but much slower than predicted as all banks will be trying to rebuild their profitability after a few very difficult years. They're all in the process of rebuilding their squeezed margins from below 2 to historical average of around 2.5%. I'm told they predict at least 1,5 years of very tough market conditions still.

Many of the banks are terminating contractors as their contracts expire, its mainly perm hires now.

I think the world will take a long time to adjust to higher rates. Chris Joye was bang on the money.

Many asset classes have to rebalance valuations based on higher risk free yields

Yes exactly.

Probably add 0.5% to the author’s predictions

Methinks the RBNZ will make the bank's lives quite difficult if the banks hold their margins high. (2.5% is absurdly high when computers are doing all the heavy lifting.)

I expect that by that time the RBNZ will be facing serious criticism for making the economy tank far further than most believe was necessary.

The RBNZ will be trying to make amends for another stuff-up and will be trying to get the economy moving again. Banks gouging (yet again) will not be acceptable to anyone. A threat by the RBNZ to adjust the levers if banks don't play ball will probably be enough. And if that doesn't work they can threaten to bring in some new levers that are currently under discussion. And ComCom will be looking very closely at their behavior and may - I live in hope - actually come out with a reports that effects real change in the banking sector.

"as all banks will be trying to rebuild their profitability after a few very difficult years."

It is hard to take such comments seriously after the banks have made record profits for the last few years!

re ... "Let's keep in mind this author's business and livelyhood [sic] depend on people taking out mortgages."

Yet another person that doesn't quite understand what mortgage brokers do.

Banks - not mortgage brokers - make the vast majority of profits from mortgages.

Mortgage brokers exist primarily to find the best deals for customers. And they do this, for the most part, extremely well. Why? Because too many people simply take the rates on offer from their banks and get conned into believing they've got a great deal because their bank offered them a piddlingly small discount.

Banks pay mortgage brokers commissions because mortgage brokers cost less to bring in new business than what it costs the banks to get new business. Not many people know that. But that how it works.

The only valid point you've made is that both banks and mortgage brokers make easy money with more mortgages. Somewhat counter intuitively, mortgage brokers can do quite well in economic challenging times as people seek their services to get the best deals because they're under financial stress.

disclosure: I have never been a mortgage broker but have used them, and I have worked in banking and insurance in many parts of the world.

That's a huge straw man there.. there was no implication whatsoever that brokers make more money than banks from mortgages.

It is an entirely factual statement to say that they rely on people taking out mortgages for their commissions.

The low sales volumes over the last couple of years has had a clear impact on their revenue. Brokers have been touting for business hard on all the social media platforms.

Squirrel in particular have been trying to talk up lower rates on the horizon for months now, in an attempt to persuade those on the fence into the market.

re ... "It is an entirely factual statement to say that they rely on people taking out mortgages for their commissions."

And they do quite well out of re-financing existing mortgages onto better terms! Especially when existing mortgage holders are facing cashflow stress.

The good mortgage brokers are in no way dependent on new mortgages, or bigger mortgages, as the huge pool of mortgages re-fixing every year is simply enormous, and poorly serviced as most people simply accept the bank's offered terms rather than seeing what the competition has on offer.

re ... "Squirrel in particular have been trying to talk up lower rates on the horizon for months now, in an attempt to persuade those on the fence into the market."

You may believe that statement but people with a greater understanding would conclude that Squirrel has been challenging the bank economist's nonsense, repeated ad nauseum, that rates will be 'higher for longer'. The bank economists want people to re-fix long to maximize bank profits.

They have NOT been trying "persuade those on the fence into the market." Their message is directed at the huge pool of people coming up to re-fixes.

What they have been saying is 'don't believe the banks'! Believe instead in non-bank economists and history. And "Don't re-fix long".

Why are term deposit rates so high? Surely the banks have more term deposits than usual right now, why pay so much?

Because the OCR is high. The OCR pushes both deposit rates and lending rates up. To capture deposits banks need to add a premium to the OCR as bank deposits are riskier than parking money at the RBNZ at the OCR rate.

The common theme here is that banks don’t need deposits, they can just make money up.

Savings accounts are lower than the OCR yet people invest in them.

Surely the banks have a lot more in TDs now than 3 years ago, so why do they need more TDs? And if they don’t, why pay such high rates?

Banks have 'minimum capital requirements' that limit how much money they can 'create'. Without deposits they'd not to able to create as much.

re ... "Savings accounts are lower than the OCR yet people invest in them." Yup. Have I mentioned that some people either ain't that bright and/or are extremely lazy? To be fair, that comment isn't completely correct. At any given time there is a certain amount of money in the system that is earmarked to spent soon. 'Savings accounts' are a place to get a small return before the money is spent. (But most is the former.)

But surely they are well over their minimum right now? For example I would never have considered a term deposit 3 years ago as the returns were so bad, but now I would, so surely they are flush with deposits. Maybe they need them more to counter the increase in defaults and risk.

"Maybe they need them more to counter the increase in defaults and risk."

I expect you are 100% correct.

Mortgage broker says loan costs to go down. Well he would say that wouldn't he.

Yes but I think he’s broadly right. ‘Tumbling down’ is a ridiculous comment though, and demonstrates his inherent bias

LOL. To many of the higher-for-longer crowd here - 'tumbling down' would be exactly the right description.

On a more serious note - in recent times, actions by central banks have overshot, sometime wildly overshot, what they believe has been 'required' to bring inflation down.

In the analysis above, the future assumption is that both rates and inflation return to long run quarterly averages. The long run averages are obviously higher than periods directly after central banks have overshot and have been forced to drop rates below the long run averages.

So 'tumbling down' may be on the cards. (I say 'may be' in my professional analyst voice. I think 'will be' is more likely to be correct.)

Tradeable inflation is what has been coming down, not non-tradeable. And the days of it doing the heavy lifting are over if you want to look at where US inflation has been for the last 5 months (ie. going nowhere, certainly not down). https://www.techopedia.com/wp-content/uploads/2023/11/Screenshot-2023-1…

{kind=link}

Non-tradeable inflation is still close to 6%. But hey, lets cut interest rates so Councils and Insurers can jack rates and premiums up even more. And poor supermarkets must be feeling the pinch by now, right? They'll need to raises prices again to compensate for lower demand.

Cast your mind back to the last bout of inflation in NZ. And the time before that. And the time before that.

Can you ever remember such a big deal being made about non-tradeable inflation?

Was it ever mentioned as a primary reason for not starting to normalizing the OCR in the face of clear evidence that inflation is coming down? Nope. It was not. Only as a passing reference. (And on one occasion dismissed outright along the lines of "it's normal for the effects of lower tradeable inflation to take time to flow through to non-tradeable inflation".)

So what's changed?

If the RBNZ is using a new target measure they haven't provided any analysis I've seen as to why this measure is suddenly so important. Perhaps we're right and the RBNZ is just pulling any measure it can to justify their jawboning?

In the absence of the former - it is difficult not to conclude it is anything but the latter.

I think it’s the non tradeable that can spiral out of control. I doubt they would want to make rate cuts until they are certain that won’t happen. I reckon we got pretty close to spiralling uncontrollable wage inflation last year, closer than many realise.

re ... "I think it’s the non tradeable that can spiral out of control."

Why do you think that? It hasn't since the RBNZ was formed some 30 years ago. (The same goes for other countries with central banks whose have inflation fighting as a core remit.)

In essence, you're saying you believe "this time it's different". Could you identify why you think it's different this time?

Just because it hasn’t happened doesn’t mean it can’t. I haven’t had a fatal car crash in the last 30 years but that doesn’t make me immune. Uncontrollable inflation is a serious problem, much more so than a recession.

The trend of rates is still much higher than the mad covid years. Extend and pretend is dead.

Felt the world over by printing and spaying cash everywhere in a massive global overreaction. Inflation is still alive and cpi is a bit of a joke. Key issue in NZ that underpins all else is the cost of shelter. Rents and mortgage payments to support ponzi price.

Hold the ocr at its historically normal levels, and let reality find its normal.

I bet the new government has taken this advice very seriously. Not.

https://www.nzherald.co.nz/nz/politics/treasurys-warning-to-new-governm…

A CGT for what I hope will be a partial return of interest deductibility? Seems fair.

NZ Inc. desperately needs 'investors' to taught what real investment is. A CGT would help 'investors' understand this critical concept so much better.

I'd love this man to be right.

I'd make a bet with you that he'll be right but I don't want to take your money. :-)

RBNZ, slow to react both ways, causing more pain than required. If only they didn't fall for the "transitory inflation" groupthink and acted quicker. Now they are claiming caution which will probably cause a depression. Idiots.

Im thinking more likely to slightly rise in short term with possible light dips but another series of rises in longer term to around 7%....(yes I am aware this contradicts the current Fed forecast)..... my 10 cents

Okay. But why? What would be coming that forces the rises?

Just looking at historical and deleting the GFC from the equation ... Im thinking future patterns are more likely to normalise ... I think many are basing their future on what plays out based on an extraordinary event (GFC) ...Maybe im wrong...but returning to a very low rate 'utopia' just doesnt sit right . There are some other factors ... (unusual for rates to plunge or dip without a bump somewhere ) Also thinking many will have tapped themselves via FOMO etc and that will show thru as it is now (easy to blame rates but it was a spree and it certainly exhausted available affordability) . House prices still out in space in some very minor locales ... I think many have forgotten...'the norm' and prefer too see the 'rockstar' return ...but its some distance away from where I sit. Other factors (stability etc etc) but I will leave it there.

.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.