By Roger J Kerr

Did the RBNZ work out for themselves that they needed to hurriedly update their economic forecasts between scheduled announcements, or were they gently nudged by some forces across the road in Wellington?

As they are completely independent of the politicians, it is unlikely to be the latter and that is despite the Prime Minister’s hint that it should not take five months to change a LVR percentage amount!

Let us hope that the economic update from the RBNZ on Thursday is about the economy, inflation forecasts and thus the appropriateness of monetary policy settings and not concentrated on whose fault it is that house prices keep going up and that the banks need protecting from their own lending policies.

On the assumption that the RBNZ again reduce their 12 month inflation forecast (due to the higher currency value), the interest rate yield curve should steepen as short-term rates move lower and the long end is pushed upwards through stronger US economic data and a lift in the US 10-year Treasury Bond yield to 1.55%.

The higher NZ dollar value and resultant lower inflation is not the only factor behind a likely decision by the RBNZ to cut the OCR to 2.00% on 11 August.

Over recent months the RBNZ has become preoccupied with the risk that lower interest rates at this time would only fuel the already red hot residential property market even more and cause financial stability problems when the inevitable correction occurs.

What is becoming increasingly apparent is that the banks would not necessarily pass on a 0.25% cut to the OCR into their home lending interest rates.

The banks are not funding too much off their books off the wholesale OCR/BKBM market.

Retail deposit interest rates have not moved lower over recent months as the banks hold rates to hold retail investors from transferring their money to higher yielding dividend stocks and illiquid property syndicates.

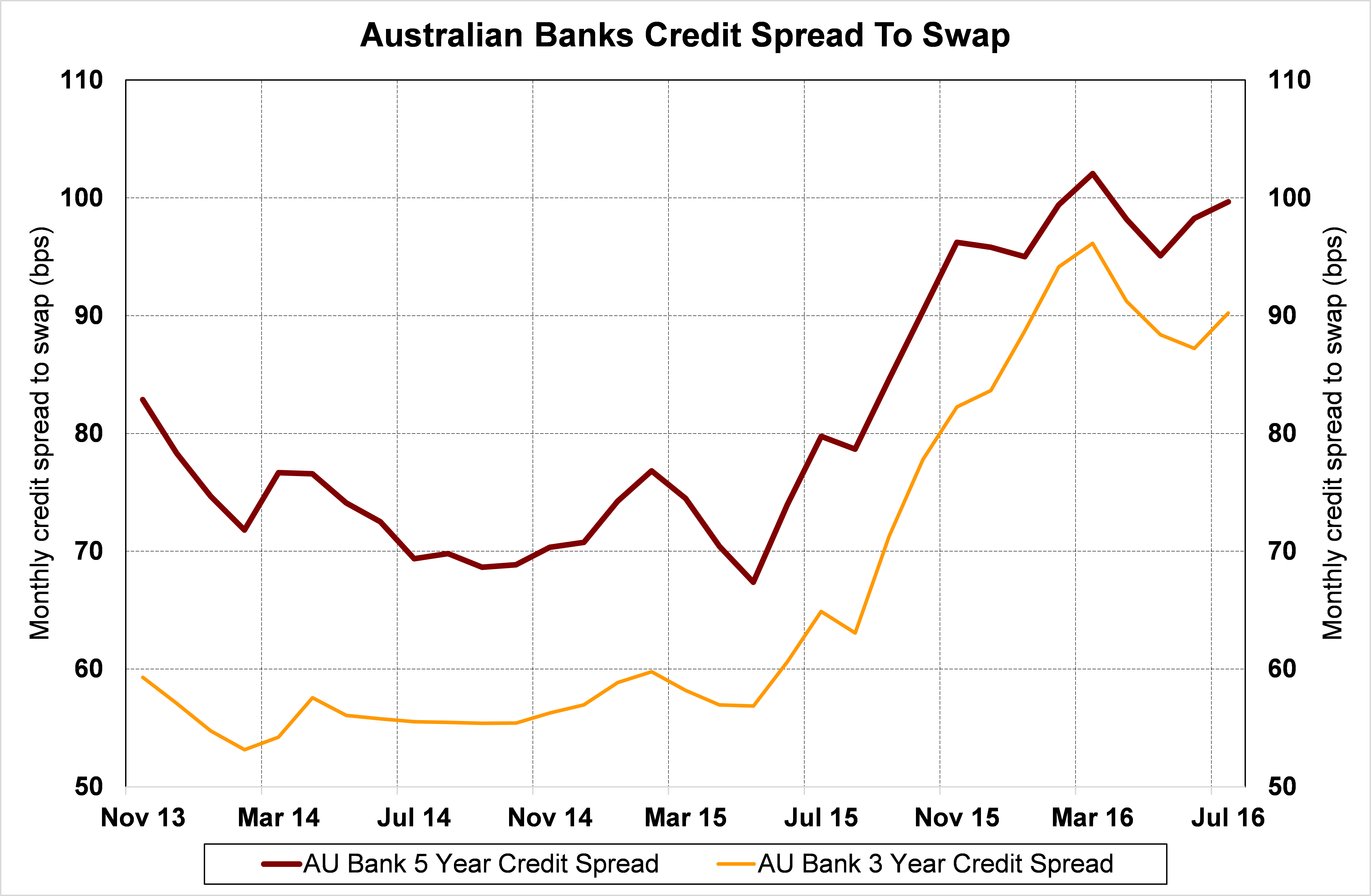

The credit spread the banks pay on offshore wholesale debt markets have moved higher again in recent weeks due to Brexit uncertainties and the Australasian banks on credit watch negative from Standard & Poors (refer chart below).

The only impact an OCR cut would have is a lower NZ dollar value, and that is what the RBNZ need to shift the annual inflation rate back within the mandated 1% to 3% target band.

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.