By Kymberly Martin

NZ short-end swaps closed up 2 bps while NZ long-end rates closed down 2 bps.

In the early hours of this morning US 10-year yields have pushed back up from 1.51% to 1.57%.

The RBNZ delivered a 25 bps cut yesterday as widely anticipated. This takes the OCR to 2.0%. However, as feared its accompanying statements and published 90-day bank bill track did not appear sufficiently dovish to a market that was already pricing 65 bps of OCR cuts. NZ short-end yields were immediately spurred higher.

After opening at 1.96%, NZ 2-year swap abruptly found itself trading toward 2.05%. However, receivers were soon drawn back into the market, yields declined, and 2-year swap closed at 1.98%. The market now prices a 1.60% trough in the OCR within the year ahead. It also prices around a 30% chance of a rate cut at the RBNZ’s September meeting. We continue to look for the OCR to be cut to a trough of 1.50%, most likely by year-end.

At the longer-end of the NZ curve yields also experienced a brief spike higher. However, by the end of the day they had succumbed to the enduring forces of lower yields globally. NZ 10-year swap closed at an historic low of 2.39%.

Overnight, in reasonably quiet, Northern-hemisphere summer trading, equities posted positive returns. Commodities were led higher in the early hours of this morning by a 4.5% rebound in the WTI oil price. This helped boost core yields. US 10-year yields traded up from 1.51% to 1.57% currently. German equivalents also traded higher (within negative territory) while UK 10-year Gilts consolidated at historic lows.

Today the BNZ PMI will be released. Anything close to its June reading of 57.7 would indicate recent strong momentum continuing into the second half of 2016. However, this is unlikely to influence market pricing of OCR cuts, which is being impacted by low inflation gauges rather than a lack of appreciation of solid domestic growth dynamics.

Daily swap rates

Select chart tabs

Kymberly Martin is on the BNZ Research team. All its research is available here.

1 Comments

The market now prices a 1.60% trough in the OCR within the year ahead. It also prices around a 30% chance of a rate cut at the RBNZ’s September meeting. We continue to look for the OCR to be cut to a trough of 1.50%, most likely by year-end.

Hmmmmm...

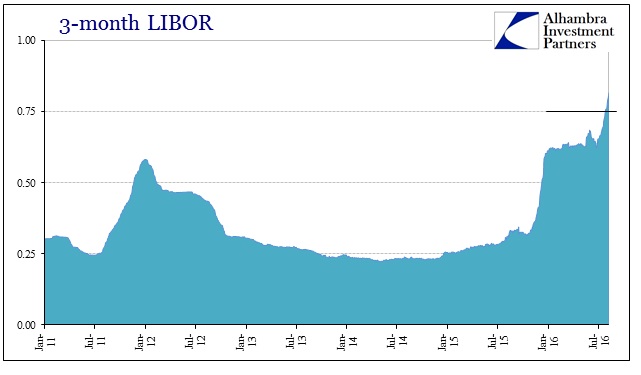

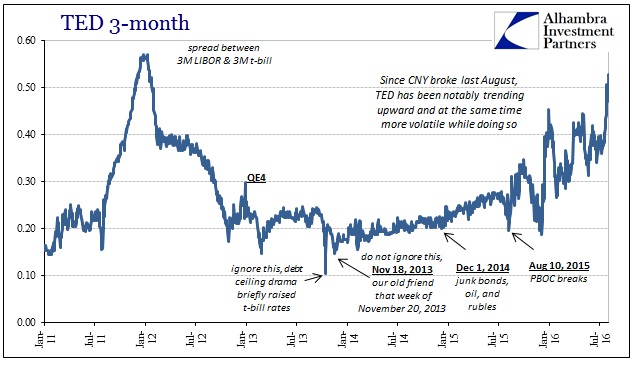

LIBOR has been rising far out of proportion to either rate hikes or 2a7 money market fund reform (which has become the latest mainstream bogeyman to, like 2007, attach a benign but plausible-sounding explanation to what is becoming a very real problem again). That has left the TED spread, the difference between 3-month LIBOR and the 3-month T-bill, surging in what used to be a universally accepted indication of interbank funding risk; i.e., liquidity. Only for the most part it has been ignored because economists, primarily, have determined it either exclusively a product of regulatory reform (2a7) or, like 2007, another market "disequilibrium" that can't possibly mean what it so clearly does.

{kind=link}

{kind=link}

But it is eurodollar futures that truly draw and direct our attention again in just that manner, especially in the absolutely astounding move since last summer. The Fed says they are going to raise rates and even managed to do it once, at least in federal funds. Eurodollar futures instead only rise in price (meaning the indicated money yield falls). They suggest even more illiquidity and funding problems that only bring this all full circle; to emphasize just how little monetary policy has grown despite mistake after fatal mistake, opportunity after opportunity, to do so these past nine years. What the eurodollar futures curve has done since last August, a period of time during which a string of negative events that were also judged "impossible" actually happened, is nothing short of extraordinary. And the Fed disregards them all over again. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.