New Zealand’s largest general insurer has revealed research indicating there’s somewhat of a rift between the misfortunes we’re most worried about occurring, and those we end up making insurance claims on.

Insurance Australia Group (IAG) – the owner of State, AMI, Lumley and NZI, and underwriter of ASB, Westpac, BNZ and the Cooperative Bank’s general insurance – says those it surveyed in conjunction with Nielsen, considered a house fire to be the second most concerning incident to occur.

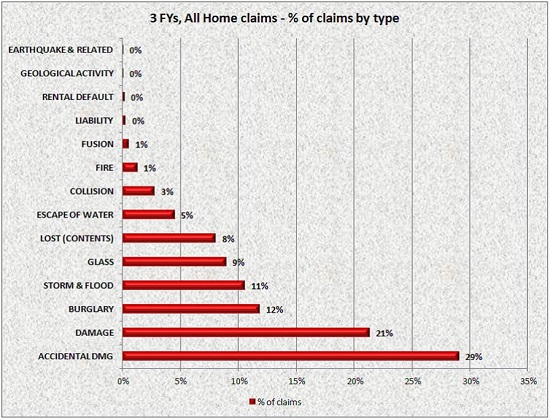

However house fires only accounted for just over 1% of all the home insurance claims IAG received between 2013 and 2015.

IAG spokesperson Craig Dowling notes that while few people will experience a house fire, claims of this type are by far the highest value, with the average costing $31,000.

Half of all the home insurance claims IAG received were for ‘damage’ or ‘accidental damage’ caused to a property. This includes damage to personal items such as dentures, spectacles and hearing aids plus malicious damage caused by other people through vandalism or graffiti.

This was only number eight on the list of 10 incidents New Zealanders were most worried about.

Home burglary was number three, with this accounting for 12% of home insurance claims made, and earthquakes number four, accounting for less than 1% of claims made during the post-Canterbury quake period.

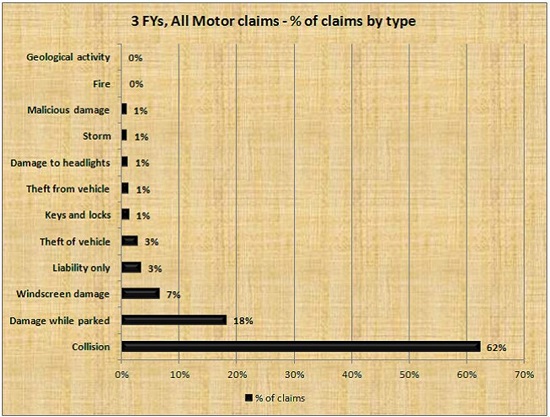

The number one incident survey respondents were most worried about, was having a car crash.

IAG confirms 62% of car insurance claims made between 2013 and 2015 relate to collisions, while 18% relate to damage to a car while parked, 7% to windscreen damage and only 3% to theft.

Survey respondents ranked vehicle theft at sixth on their list of concerns.

They considered storms and floods to be the seventh most worrisome incident to occur, with this accounting for 11% of home insurance claims received in the three years to 2015.

Despite lost contents (such as mobile phones, photographs, tablets, glasses/ hearing aids) only making up 8% of all IAG’s home claims, this was ranked fifth on survey respondents’ list of concerns.

Here is a list of the top 10 incidents New Zealanders are most worried about occurring:

1. Having a car crash

2. A house fire

3. Home burglary

4. Earthquake

5. Losing personal items

6. Vehicle stolen

7. Storm or flood

8. Damage to property

9. Tsunami

10. Volcanic eruption

Here are graphs provided by IAG, detailing the sorts of claims it received between 2013 and 2015.

2 Comments

Interesting but insufficient information. While the things we actually worry about, but are in the low range of actual claims might be relatively expensive (house fire for example), the risk of one occurring is actually quite small ("just over 1%"). How is this reflected in premiums?

Considering that Insurance is the process of offsetting risk onto another, and an insurer accepting the risk, is the premium actually reflecting what the risk is? If the house is newer, built of flame resistant materials, has smoke alarms, fire extinguishing systems etc are these reflected in the premiums, or are we all subsidising the others which aren't, and contributing to excess profits?

You'd be surprised at how far premiums really go.

Lets say you have 100,000 customers, each paying $1000 per year (rounded figures)

That gives you $100,000,000 'in the kitty' (ignoring taxes, EQC levies and the like)

If just 1% of that 100,000 (1000) customers have a serious fire requiring significant repairs or rebuilding (lets use the average of $31,000) then already you "used up" $31,000,000 - or 31% of your premium for the year.

On top of these major losses (just from fire), insurers pay day to day claims, overhead costs (including salaries). And are expected to return a profit to shareholders (they are a business at the end of the day - just like any other business).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.