Here's my summary of the key events overnight that affect New Zealand, with news of a mix of confidence signals around the world. New Zealand looks great by most comparisons.

Firstly, American home resales volume rose in October to it's highest level in almost ten years. Their median price for all housing types in October was NZ$329,400, up +6% from a year ago and is the 56th consecutive month of year-over-year gains. The median price for a single-family home rose +5.9% to NZ$331,500. Sales on the US West Coast showed the highest gains of any region.

In a taste of fragmentation to come, the EU has today signaled it will require international banks to hold sufficient capital in the currency zone to meet local capital requirements. This is part of a retaliation for a similar rule adopted by the US authorities and shifts banking regulation into a more regional, protectionist state. Both sets of requirements will likely hurt UK-based institutions the most.

Portugal has repaid the IMF €2 bln early for amounts due in 2019. This is part of the €78 bln bailout that the country got in 2011.

And in an indication of just how far the EU has to go to restore consumer confidence, there is a survey out today trumpeting that fact that European consumer confidence is now at a 2016 high. The latest index reading is a negative -6.1, but almost two points improved from October. The EU has never had positive consumer confidence since this survey was started in 2005.

In Sweden, an assessment there shows that when interest rates are low or even negative, people save more at a bank. The motivation changes from trying to earn a return, to having the security of ready funds. It is a consequence of low confidence.

In South Africa, data out overnight indicates that unemployment there has reached a 13 year high - of an eye-watering 27%.

In Australia at a conference in Canberra yesterday, a senior S&P manager essentially warned that Australia's AAA credit rating is at risk of a downgrade if there are more delays in getting their Federal budget balanced. Given the political impasse, it seems unlikely we are about to hear of any improvements any time soon, and certainly not in their upcoming half year fiscal update. A cut in the Aussie rating will probably have some sort of backwash effect on us, although New Zealand sovereign CDS spreads are uniquely low at present, and 10% lower than for Australia.

In New York, the UST 10yr yield is lower again today, now at 2.31%.

The US benchmark oil price is marginally higher and now just under US$48.50 a barrel, while the Brent benchmark is now just under US$49.50 a barrel.

The gold price is down to US$1,208/oz and at a nine month low

The New Zealand dollar will start today just a little lower at 70.5 US¢. On the cross rates it is a bit lower too at 95.4 AU¢, and against the euro at 66.4 euro cents. The NZ TWI-5 index is now at 76.2.

If you want to catch up with all the local changes yesterday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

19 Comments

In a taste of fragmentation to come, the EU has today signaled it will require international banks to hold sufficient capital in the currency zone to meet local capital requirements.

Hmmmm....

It seems like balance sheet constraints are in conflict with monetary policy objectives…

Balance sheet constraints are driving prices in a way where financial conditions abroad are tighter than financial conditions in the U.S. Where borrowing a Eurodollar is more expensive than borrowing an onshore dollar. The feedback of this on the U.S. dollar and financial stability risks are making interest rate hikes less possible and also less effective. Read more

So the takeaway from the last line is that the US (and rest of developed world) has painted itself into a corner, in which monetary tightening becomes a risky option, but further easing is also effectively a dead end.

As a thought experiment, what might happen if interest rates were suddenly hiked by say 1%, either just in the US or across the whole low-interest world simultaneously? Apart from the immediate stress on mortgage-holders, inter-bank borrowing, and a further crash in bond values, what other flow-on effects would there be?

don't forget your pension

http://www.wsj.com/articles/era-of-low-interest-rates-hammers-millions-…

With pensions around the world increasingly reallocated funds to equity markets in a desparate effort to close funding gaps amid recklessly low central banking rates, and traditional banks tapped out by regulatory restrictions on their balance sheets, struggling Euro Zone countries are increasingly being forced to turn to hedge funds to fill their debt issuances. As Reuters points out, struggling nations like Spain, Italy, Belgium and France have seen a 3x increase in debt issuance allocations to hedge funds. Read more

Don't hold your breath.

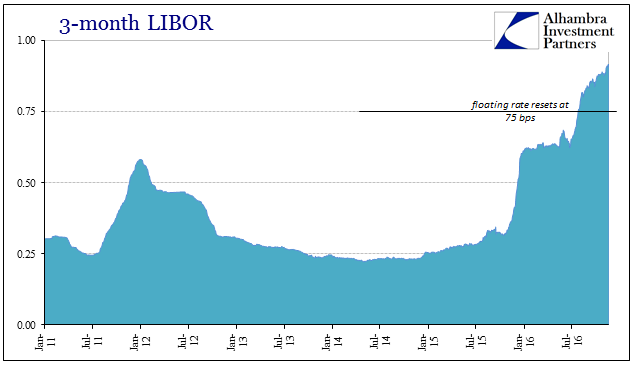

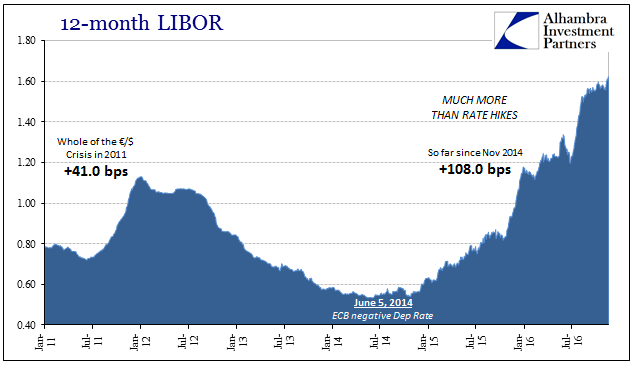

3 month LIBOR trades at 0.91983% while 12 month LIBOR is quoted at 1.62289%

{kind=link}

{kind=link}

Complex stuff. Good news out of the US reminded me of Yellen's Optimal Control strategy:

https://www.federalreserve.gov/newsevents/speech/yellen20120411a.htm

The idea is that you are better to hold interest rates low for longer until unemployment is sorted, then ramp them up very rapidly to stop things getting out of hand. The slide show link at the bottom of the article shows interest rates rising from their present level by 4% over the next 3 years (slide 8).

Perhaps the flaw is evident in the grandiose title "Optimal Control", the idea that experts know best how to manage the economy from the top down. The Imperial/Soviet/Harvard Grand Delusion so favoured by all civil serpents and government employees everywhere (including the Military Bureaucracy); since a Mandarin State, preferably under an autocratic ruler, gives them enormous license to boss everyone below them about.

Beware people who like telling others what to do.

Sudden hikes would be pretty crippling in the US. With the Fed rate being where it is there are a lot of people with mortgages, car loans etc around the 1.99% to 2.6% range. Most are paying down a lot of debt, the remainder at the bottom are struggling with payments. Most of the young works have extra suffering with 3.6 to 6.3% Federal and private student loans. The suffering being minimum repayments on low wages, whereas the ones on higher incomes are on IBR and set to repay over 10 years or up to 20 years at around 10% of their gross income.

I have no doubt that sudden hikes in the US will create a lot more suffering. Imagine owing $250,000 on a house worth $200,000 (underwater) but able to make payments. Then imagine interest rates going from 1.99% to 3.99%. A lot of people would struggle to pay or refinance and those extra interest payments would suck the life out of the US economy. People in the US prefer maintaining good standing on their credit cards and student loans. The credit cards are more useful than a house and the student loans cannot be written off in bankruptcy so they have to maintain the minimum payments on those. People will walk away from their houses if the interest rates go up fast.

I ran some quick figures and the difference between 1.99% and 4.99% on $250k repaying over 20 years is about the same difference as a typical car payment in the US. Given that most are about one car loan payment from insolvency that would be about the point where there would be major problems. Bring on optimal control for the next disaster.

Perhaps a bit of hardship will encourage financial responsibility.

Another conclusion is that the money system needs to hyperinflate to keep working, but at the moment is being constrained. Continued constraint will mean failure, turning the taps back on means hyperinflation (of assets again probably). Just another version of price or quantity, as I said 3 years ago if interest rates go up the system will fail :-)

".....interest rates are low or even negative, people save more at a bank."

So there is the proof that lowering the OCR increases peoples saving tendency and therefore tends to lower inflation further. Ie. As I have been saying for some time now, the inflation rate/OCR model used by most Reserve Banks does not work at low inflation rates and is actually counter-productive. (That is, until late in the cycle when the asset bubbles that lowering the OCR cause become so established and large that the wealth effect kicks in. Of-course those asset bubbles then go on to become the next crash that starts the whole cycle again )

I still think that we need to look at ways of allowing deflation as this should be the natural consequence of a healthy economy that is increasing productivity. Obviously we would need to seriously change the economic governance and banking models that we use.

"I still think that we need to look at ways of allowing deflation.."

In theory i think you are right; in practice it doesnt seem possible. Its like trying to unwind economies to scale - imagine if every farm / business for example was somehow forced to become smaller ... which in turn has to lower output, productivity and wages, which in turn lowers demand and affordability of debt ...

And it is the rollover of new Debt that keeps commodity prices up and Oil up to the system

It certainly does have problems with our set up as things are. The fact that banks are able to virtually print money as inflation works through means that with deflation they are in the reverse situation. Clearly that won't work and needs to be changed, and it can be changed because they did not always have the ability to do this. The changes that are required need intellectual horse power and clear thinking. The present system is fundamentally flawed because what seems to happen is that natural increases in productivity must be offset by other things rising in price, whether justified or not to keep inflation positive. So we are getting value and economic distortions. I suspect that the increasing wealth disparity is one consequence with the fruits of increasing productivity being transferred to the value of assets in the hands of the wealthy.

I think the thing you are ignoring is the usefulness of debt - it allows to bring forward consumption so that investment in capital goods works. To reverse this process to my mind is just not feasible. To wipe debt would be to wipe pension funds for a start. (in reality this would reveal the true position - the wealth just isnt there).

The increases in productivity also have to EXCEED diminishing returns in order to realise anything. ie you may invest in a bigger gold digger, but as the gold gets more difficult to locate (given we always get the easy stuff first) you have to do more than just lift productivity in order to keep the system working. The alternative is to paper the gap with more debt - which is what the world has been doing for 30 years. But its coming to the end of its ability to cover the problem.

Does debt bring forward consumption? Isnt the otherside of the ledger showing defered consumption? Saving for my pension brings forward consumption?

Do you think new debt is 100% backed by new savings? Or runaway capital values...

How can this be?

"Prices are dropping in certain areas. It's the investment properties that are just dropping right out, as much as 20 or 30 per cent," he said, citing Auckland central areas

http://m.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11753…

I can not belive the herald can get away with publishing that without a disclaimer that its a paid advertisement. They have been promoting that guys property investment seminar all week.

I guess now that he has just lost 30-40% on his potfolio he needs to make money somehow

Talked to a cousin in Australia yesterday, who told me that today Chinese have to be residents to purchase in Australia under the new regulations, they have literally left the market.

Check this out, NZ has won a silver medal in the race for the biggest increase in millionaires.

Didn't we do well!! Over 20% increase... wonderful news ;(

And that in a large part because of our beloved National government.

(Thank you JK we understand your motto, any medal is good news to you)

Global Wealth Update: 0.7% Of Adults Control $116.6 Trillion In Wealth

http://www.zerohedge.com/news/2016-11-22/global-wealth-update-07-adults…

And here a close-up, only Japan has a larger increase percentage wise.

http://www.zerohedge.com/sites/default/files/images/user5/imageroot/201…

{kind=link}

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.