Here's a special holiday update of some key events and data you may want to know about today.

First up, the number of Americans filing for jobless benefits unexpectedly fell last week. At the same time, a closely watched survey of consumer sentiment moved higher mainly through continued optimism over household finances. All this suggests the sharp slowdown in job growth in March may well have been an aberration.

The US Administration has reversed itself and now decided not to declare China a currency manipulator. Instead it will 'ask'(remind) the IMF of its role in this area. It has reversed position on export guarantees as well, deciding to keep the American EXIM Bank. (And the President has signaled he will likely keep Janet Yellen as the Fed chair, also reversing an earlier stance.)

The OECD has released a review today that suggests that employment is growing in the 35-group nations, pushed up in equal measure by falling unemployment rates and rising participation rates. It turns out employment rates now are higher that before the GFC.

In Australia, their small business ombudsman has been investigating the behaviour of large corporates around how they pay their small suppliers. They found an abusive, unfair system where the large are taking advantage of the small. In fact, Australian corporates apparently pay their small suppliers 26.4 days after the due date, on average. That was the worst of the nineteen countries surveyed (New Zealand was not included.) Their ombudsman says the situation is so serious, it calls for legislation to force change.

And staying in Australia, their central bank issued its latest update of its financial stability assessment yesterday. The general conclusion is that the financial system is in good condition. Indeed the Reserve Bank says that banks have actually become more resilient and able to deal with challenges. Their main concern is the lift in mortgage debt and slower growth of household incomes. If unemployment were to rise and/or interest rates were to lift markedly, that would create challenges for some families who basically have not built up any buffers for a bumpy ride. But it is just a risk at present – interest rates look to remain stable and the job market is still healthy.

And more from Australia. Rising electricity prices and recent blackouts in South Australia are driving people across the country to install solar power capability, with panel installations in March at a five-year high.

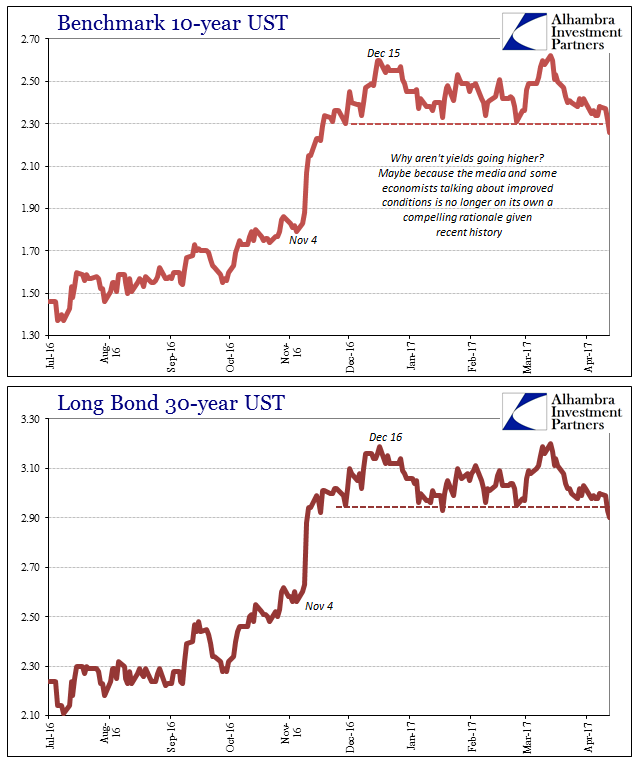

In New York, the UST 10yr yield is sharply lower today, now at 2.23%. An escalation of the conflict in Afghanistan seems to be behind the risk-off rise.

The US benchmark oil price is lower today and now just under US$53 a barrel, while the Brent benchmark is just over US$56.

The gold price has jumped another +US$11 today, now at US$1,286/oz.

The New Zealand dollar is a little lower against the greenback this morning and now at 69.9 USc. On the cross rates it has held its own at 92.4 AU¢, and 65.9 euro cents. The TWI-5 is now at 75.1.

The easiest place to stay up with event risk over the holiday period is by following our Economic Calendar here »

Daily exchange rates

Select chart tabs

2 Comments

First up, the number of Americans filing for jobless benefits unexpectedly fell last week. At the same time, a closely watched survey of consumer sentiment moved higher mainly through continued optimism over household finances. All this suggests the sharp slowdown in job growth in March may well have been an aberration.

The UST10s &30s say otherwise.

{kind=link}

Someday there may indeed be a pick-up in global growth, though we will probably need all our fingers (and some toes) to count how many “unexpected” occurrences disrupted that “pick-up” over the years to come. And when it does come, there will be no need at all for vagueness about its features, as it will be obvious and unmistakable. Until then, these poor attempts at rational expectations manipulation should have been curtailed by now by even a modestly curious media that is sick of writing the same lines over and over. In other words, when global growth actually does happen it won’t be much talked about, and certainly not to the unceasing degree of the past seven years. Read more

Their (RBA) main concern is the lift in mortgage debt and slower growth of household incomes. If unemployment were to rise and/or interest rates were to lift markedly, that would create challenges for some families who basically have not built up any buffers for a bumpy ride. But it is just a risk at present – interest rates look to remain stable and the job market is still healthy. (my emphasis)

Exactly - one that prevents economic lift off and causes banks to seek liquidity rather than finance growth opportunities.

Witness JP Morgan.

Just this week, however, Mr. Dimon declares he is no longer so bullish. The events of these past few years have apparently been enough to, like policymakers, disabuse all notions of recovery. In his 45-page annual letter to JPM shareholders, the bank’s CEO now says, “there is something wrong with the US economy.” Outside of Economics, banking, and politics, his summation was met with a resounding “you just figured that out?”

What’s perhaps most important about his sudden reckoning is that he looks everywhere else for its cause. This is much the same problem as with Federal Reserve and indeed all global central bank authorities who do the very same, a tradition that started in Congress on March 28, 2007. The last place any of them will look for answers is within.

For JP Morgan, there are any number of balance sheet figures that show the bank’s part in all of this, from 2007 to the “rising dollar.” For one, there are its liquidity preferences as defined in the most traditional way – “cash due” and “deposits with others”, a category that includes JPM’s reserve account at the Fed. In 2007, only 3% of the bank’s assets were in cash, down just slightly from an average of 4.1% over the prior six years. It jumped to 7.6% in 2008, which only makes sense, but then fell back to 2.3% in 2010 despite QE1 – or actually because of it.

In other words, it seems very likely JPM was confident enough in the effects of QE toward establishing recovery and a return to pre-crisis conditions so as to hold so little cash so close to panic. That was maintained only to 2011 and resumption of the same monetary problems that have never been resolved. The proportion of cash hit 6.4% in 2011, then 7.4% in 2012, nearly the same relative balance as during the worst of the crisis. Rather than remove this idle liquidity in response to the third and fourth QE’s, JPM’s balance sheet at the end of 2014 would be 19.9% cash (only some due to regulatory changes). The proportion has declined somewhat due to efforts in early 2015 to restrict institutions holding their cash balances at the bank. As of the end of last year, JPM still shows 15.6% of its assets as cash. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.