A chill wind has blown through the auction rooms, with the number of residential properties going under the hammer at the latest auctions (3-9 June) dropping to 157. That's down from 185 the previous week and 192 the week before that.

It suggests that auction room activity is now bouncing along on its winter lows.

However while fewer properties were offered at the latest auctions, there was almost no change in the number that sold, with 63 selling under the hammer at the latest auctions, almost unchanged from 64 the previous week.

That pushed the latest sales rate up to 40% from 35% the previous week.

Those figures may be a sign that those people who are selling by auction at the moment are more likely to be serious vendors with realistic price expectations, rather than time wasters setting overly optimistic reserves.

The details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices and rating valuations of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

128 Comments

The percentage of sales at or above RV would certainly support your assertion that vendors are being more realistic, Greg. Over 80% being sold below RV.

Because HP are dropping to the floor, then under it until they're in the dust. Its going to be a tough few winters, Thats my personal opinion

Yes, we are 1/3 at best into this certain housing bear market

They take around 6 years to play out, with Japan being the longer recent case of 20+ dealing with the bears sharp claws.

So 4x more long winters to slay and neuter this worldwide ponzi and get to a healthy, sustaining and regulated DTI of 3 to 4x incomes

"Science" or "I reckon" or "how I think it should be"?

Just Informing you of the world average, so you can best prepare to winter out, the many long winters ahead.

Look at it with open eyes, we've crashed 25% already in just 18months, without any significant pain roiling our economy yet.......what drops will occur when much more widespread stresses are apparent in the coming years???

Making a "world average" isn't great science, because your assumption is all the countries shared the same circumstances.

Japan never bounced back, because their housing crash coincided with the end of growth in their economy and population. There's around 8 million empty houses in Japan, and a shortage still in NZ. Likewise in Europe, Ireland recovered from their GFC housing crash, less so the likes of Greece.

"and a shortage still in NZ" - Yes, a shortage of affordable houses - a glut of expensive houses. This is not even taking into consideration the multitude of ghost houses! At last count 200k) as at 2018 census.

For your benefit Zac https://www.stuff.co.nz/business/industries/125463204/ghost-houses-a-sp…

Homes in general from the looks of it. Will future houses be more or less affordable? Unless you make some fairly severe changes to how we generate new housing, they're probably going to be at the 'expensive' end.

Even our old crappy houses have a demand that close to a couple hundred grand get spent on them to meet the government's regulatory requirements for them.

Did you even read the article you posted?

"With a lack of supply blamed for the country’s housing crisis, the nearly 200,000 unoccupied dwellings identified in the 2018 Census would surely be a handy addition to Aotearoa’s housing stock"

I used this article purely as a historic reference to validate the said 200K. The article was published in June 21 using Census 2018 figures. Do you think its more now? 300K?

If you read the full article, you'll see it notes the proportion of empty houses hasn't changed significantly for decades. So probably not.

At any given time there's a certain volume of empty houses to be expected. People hear "oh there's 200,000 houses noted as vacant, so there's actually more than enough", when the bulk of them are either only temporarily empty, or located away from the areas where people want to live.

You're flowing with lots of baseless assumptions on an article that's very outdated. Again, I only used it as a reference for the said 200K. This is not something I would expect from an individual who's lived through a few rodeos. Once the results of Census 2023 are out you will know how useful such assumptions are in current times. The changing of Australian immigration settings could have a significant effect on future Census too.

If you went through life betting on established trends reversing without any other significant changes, your success ratio would be fairly low. That's not to say life doesn't present such instances, but that they're rare enough so as not to be a method of thinking to apply day to day.

Australia becomes slightly more appealing by changing their immigration laws, but I don't think citizenship eligibility is holding that many people back. Most likely, it'll probably reduce the number of kiwis returning back to NZ that are already there.

OH - Okay then....LOL!

Well, why would census 2023 show you results from a future change to immigration settings? That'd be something you wouldn't pick up on for another several census'.

I repeat - "The changing of Australian immigration settings could have a significant effect on future Census too"

https://www.stuff.co.nz/business/132109458/brain-drain-to-australia-inc…

Better renumeration/lifestyle prospects alongside Australian Government support (safety net) is perceived. Its just getting started as our wealthier elderly can now shift and unite with family and receive equal support. Why downplay such a significant change? edit

That's something that could happen. As in, it's in the realm of possibility.

To increase the likelihood of your punt, you'd want to establish a large existing pent up demand for people who want to migrate to Australia, but haven't already because of a lack of existing citizenship eligibility. I think most people that really want to go, would go regardless.

That's not even mentioning the other side of the coin to create a higher percentage of vacant houses; we'd also need less incoming migrants to replace the ones leaving.

https://businessdesk.co.nz/article/opinion/most-migrants-here-for-a-goo…

Yes, I realize this is just an opinion however, the breakdown of skills category of immigrant arrivals doesn't seem to support broad based high end incomes and skills. At least not at this stage.

Time will tell.

So you're wanting to weigh future emigration predictions of your own to Australia, against 9 months or so of existing post covid immigration to NZ?

The random assembly of factors to your perspective and amount of changes you make to your posts would suggest taking a bit more time to consider ideas before forming them.

Again, time will tell.

Citizenship is a massive change for people who have children. Now people with kids can move to Australia knowing that their children can get citizenship and qualify for (a) the NDIS and (b) student loans. Whilst people might have happy to gamble with their own personal financial wellbeing by going to Australia without a safety net, they are usually not prepared to gamble their kids. Now they don't have to.

What percentage of existing migrants to Aussie have kids?

There is NO shortage of HOUSES in NZ.!

There is an Over supply of " Jacinderized underclasslings" that want the government to give them houses.

There are many young people who want a 3bed 2 bath new home now and with out paying market rates ( which are high but offsett by low interest rates that aren't 26%, like in my day)

There are the just plain Useless mob that will never get anywhere because of their piss poor attitude

Plenty of houses ! Don't buy the left spin!

Simple averages and Max borrowings are needing your close and urgent attention!!!

When the average couple can now just borrow a Max of $500,000 ...... how quick will the market drop the required 300 to 600k to match this epic, once in a lifetime crash in borrowing capacities??

This unwind will take years.....and our OCR MUST STILL GO HIGHER.

When the average couple can now just borrow a Max of $500,000 ...... how quick will the market drop the required 300 to 600k to match this epic, once in a lifetime crash in borrowing capacities??

I guess once that "average buyer" represents the total sum (or upper end) of house hunters. In the meantime, people who can afford more, will likely pay more.

Or buy in the cheaper areas! And rent!

Not 4 x more long winters NZGeck, you're being generous and understating the facts.

At least another 11 hard winters to come as 13 is unlucky for some. Properties have to drop to a quarter of what they were in 2021. There will be no need for slumlords or greedy bwankers when the former tenants are housed and not owing millions.

If that scares some specuvestors, tough! Its better to know early so you can get out while you still can!!

In the scenario youre predicting, people would be worrying about caloric intake rather than home ownership.

Flying high has reached peak doom goblin. A parody account I suspect, possibly HW.

Interesting character, I think he/she used to be super bullish about property? (I recall them having a go at my bearish views)

so yeah maybe a troll account. Or may they have genuinely changed their viewpoint 180 degrees

No whats this HW rumour started by poppy. Any cognitive dissonance displayed by me is probably brought on after a year of couch surfing.

BEEN SINCE SAVED BY LOTTO PB. Now 10 mill in cash and shares.

Flying high is HW2. See comment further down.

Drops of 100 to 150K per year, for the next 4 years, seems about right to correct our market somewhat. Then the DTI stake impales the spruikers heart. The market then has 2% average annual rises, matching average wage increases.

I dont rule out a decade of deflating home values.......so this case has drops of 50k per year in that scenario.

The investor confidence in NZ property is now shattered beyond repair.

Everyone stairs in bewilderment that TA/AC are no longer effective at being the leading "Talking Golden Geese" of ponzi pumpers.

Confidence that prices will rise (revert to normal) is completely broken and has sunk without trace......for many, many years.

The investor confidence is property is now shattered beyond repair.

Why would 6-12 months of falling values, after decades of values doing the opposite, be enough to shatter things beyond repair? Most investors will be better off today than they were 5 or 10 years ago. A smaller subset will be getting their fingers burned for decisions made in the last 36 months.

You'd need a total economic collapse to have the affect you're claiming.

They take around 6 years to play out,

Yes, perhaps particularly true given NZ's 3-year local government revaluation cycle. We've kind of lost sight of real market valuations (by an individual valuer on an individual property). Though REA's will tell you RV has nothing to do with market price, they are definitely still a bit of an anchor in the minds of the general public. Not saying that is a good thing - it's just the way it is.

Who to trust?... when fecking REAs can tell Homes.co to change a valuation, and thus unduly influence tthe market, based on their unqualified opinion and publish it on thier website, then aĺl market credibility is lost....

https://homes.co.nz/address/waipu/waipu/338-south-road/Z5rbN

#- read the comments below the historical price graph!!!

NZ property market is screwed over by the REINZ , Agents, the media, Homes/ one roof, and other money grabbing assholes. Not buyer and sellers.

if David Parker concentrated his pathetic little mind on RE reforms, transparency and honesty, he would do more for the economy than the currently fucking unmandated rubbish he is sneaking into law!

FYI

https://www.oneroof.co.nz/estimate/338-south-road-waipu-whangrei-northl…

Oneroof.co.nz: 815,000

Homes.co.nz : 1,490,000

The numbers don't stack up. If I add the properties sold over CV excluding Auckland Central Suburbs it's 11 nationwide (8 in Auckland). So did only 1 property sell above CV in Auckland Central (making it 5.5%) or are the totals wrong for both the country and Auckland Region?

Edit: ok, had a look at the actual results, it's max 1 over RV (2 have unspecified RV and none of the rest was above, so yeah) making it 5.5%

Nice.. over the next few months it'll move closer to zero.. wish it could go negative:)

Well spotted Danicriss. There was an error in the figures for Auckland's central suburbs, which has now been corrected. Cheers.

Agents are finally coming to grips that lies can only take them so far.. they seem to be more frank about prices being soft in the near future..

Hello, remember last week? " we've seen a huge TURNAROUND " "sales are back"...

Nope! The Hurt locker is all go. Hang on to your hat's, this is going to get ugly

As a country, NZ is in the unfortunate position of borrowing heavily to repair or maintain vital infrastructure, giving the illusion of economic normality. We are finding out what happens when prosperity is placed overly on Real Estate (this is the part that was avoidable). We continue to live way beyond our means and foreign investors are now expecting a higher return.

Ten Year Government Bonds

Portugal 3.06%

Spain 3.35

Greece 3.62%

Australia 3.95%

United Kingdom 4.23%

New Zealand 4.49%

https://www.bloomberg.com/markets/rates-bonds

In the near future this great country of ours will be swallowing austerity pills.

As a country we now find ourselves in the unfortunate position of borrowing heavily to either repair or maintain vital infrastructure giving the appearance of economic normality.

Not only that, but given our pay as you go tax structure, and changing demos, we're also faced with a future of increased taxes, less services, or both. Apparently, tax revenue in the US would need to be 40% higher immediately for Americans to retain the same level of government services by 2050. And realistically many people actually want more services.

Fun times, but again Poppy, this is a global issue.

"Fun times, but again Poppy, this is a global issue" Yes - however, the solution (austerity) is a local one.

You're dealing with the same economic and demographic fundamentals, so the solution would be universal. I don't think anyones resolved it, and it'll likely involved a combination of austerity and increased revenue.

Fair comment :)

Housing bubbles can take years to deflate, if a touch of history can teach us anything.

The desperate propaganda attempts to prop up the ponzi aren’t a new thing either as many have pointed out.

Reading the local Selwyn rag just the other day, there was the following headline;

”Property slump, have we survived it?”

Inside they inelegantly attempted to insinuate that Selwyn has probably weathered the national housing slump with minimal drops in prices. To quote from the article,

“ I expect the Selwyn market to still be one of the best performing markets in the country going forward.”

And…

“But now in the last couple of weeks we are seeing more people buying and selling in the district.”

I suppose what does one expect to hear in an article where the only two people interviewed were Bayleys real estate agents.

I’ll finish the article with a third more balanced viewpoint for you,

”random interest.co.nz comment contributor however disagrees with the positive sentiment and says everything is turning to shite fast. Economy is going to implode, we are all going to starve and Adrian Orr is responsible for everything from the Ukraine war to aids. Anyone who disagrees with a single word of this is a spruiker trying to prop up the ponzi”

There you go 👍

Lol.. Jamin. Good comment.

Hah, brilliant.

In that case Jamie I’d love to hear why house prices will not continue to drop? The article certainly did not give any solid reason so I’ll have to rely on random interest commentators.

And I did not say everything is going to shite as a result of further price falls… I never even insinuated that. On the contrary, I think it would be wonderful for society if housing was affordable!

Hi Sam

thanks for your reply.

The above news paper contribution wasn’t supposed to read as if it was from you. But rather an average of the absolute dribble I see posted on these forums daily. But also obviously a joke.

Jamin 🙂

Good time to buy...when we look back on 2023 we'll say that was the bottom of the market...

Shhh, don't tell everyone. Keep it quiet and you'll have the auction rooms all to yourself!

Leverage alert 🚨

Harvey W, unlike TTP, at least you've got the courage to admit your optimistic forecasts are based purely on guesswork :) By my own admission, my earlier predictions of significant house price falls were poorly timed. Hands up who predicted the arrival of COVID and the resulting monetary stimulus?

Whats a half dozen years between friends who started with the same deposit, enough for a median house. One friend ignored your advice and bought a home whilst another took note and followed it. HP rose say 60 percent since 2016 to now. The one who did not buy cannot afford to now as the bank won't lend enough. S/He also could have lost their money in the 2020 share collapse. Destined now to rent until death

Congrats poppycock

Houseworks/HW2, you're a comedian. You just gave yourself away with that comment - lol!

by Houseworks | 23rd Jun 19, 4:28pm "in answer to retired poppy. He has long been discredited and the term poppycock fits him perfectly"

BUSTED!

Pardon me poppy, only said in jest my friend. Though you could explain your rationale not go full commando

You've been running this rumour ever since I returned. No worries

BUSTED!

I haven't seen any particularly spectacular losses at the auctions. Except the odd case where people appear to have paid just way too much back in 2020-21.

I'm still quite surprised by the number of houses that get good bids yet are passed in. One got over 100k above CV and QV estimate and appeared to be a quarter million more than they paid (can be inaccurate as previous sales records not always up to date) yet still passed in. I guess there could be many reasons for this, like one partner not really wanting to sell.

I will watch with interest as to what happens.

"Except the odd case where people appear to have paid just way too much back in 2020-21"

LOL! - I think you can pretty much guarantee everyone did!

In 2020-21 there were three categories:

Too much

Way too much

Just way too much! (Come on, Te Atatu didn't go up 100% in 3 years!)

Panic buying set in when word leaked out NZ was running out of houses! Nobody seems to want to accept responsibility for the leak.

The developer who won mine at 4k a sq m had not even been to the site, thats how crazy it got

Guy who bought the commercial building next to me came and introduced himself. Asked me how to get to the service land behind his building. I told him there was no service lane. His property ended at the block exterior wall of his building. That's why theres no doors. He looked bewildered. His wife gave him a horrible stare. Poor bugger bought the building sight unseen.

What?! You have to be kidding. Ouch... just slapped my forehead so hard it left a bruise.

If buying sight unseen, at least do due diligence and get a report.

Don't be that guy

And a 4th - Kainga Ora prices

It's trickier to collate stats and trends in NZ. For a start, the volume of sales is low so the mean tends to bounce around a bit. Every house is different, and the value of 2 side by side properties can be completely different, based on condition/kerb appeal etc. The trend is definitely downward, but I don't read too much into MOM stats.... it's best to review quarterly.

I have seen a whole bunch sell 20% plus below what they paid 2021. At a guess many might be buying and selling in the same market but I can see a few heading offshore.

Be very careful basing a view upon what is selling!

Most of what is selling has had considerable sums spent on it so it does actually sell, or at least attracts a few bids before passing in. I.e. lots of staging, fresh paint, new decks, polished floors or new carepts, serious gardening, new kitchens / bathrooms, etc. This costs. Add in real estate agent fees and the actual gains? Probably sweet f.a.

Now compare that to what is left behind unsold. E.g. do a price search in the same area in a similar price range ... Sad picture? Sure is. Throw in a few more mortgagee sales and job losses that then become bank 'encouraged' (enforced?) sales and average prices will continue down.

No vendors do not have realistic expectations. They are being greedy, plain and simple.

I do not see an easy end to this madness. Too much money is spent on the cheap quality houses and it's not good for society or the future of the country.

A greed...it's greed.

Ticket clippers enjoy the next few years with decimation of income. But it's all good, clippers will have save and paid down debt during the stratospheric boom times v.s. going long on rental interest only leverage to avoid tax.

Too much money is spent on the cheap quality houses and it's not good for society or the future of the country.

So then people should be spending even more money on higher quality houses? It sorta sounds like things are tough enough as they are.

Most are except sellers who PAID TO FOMO MUCH DURING THE COVID PERIOD when 200k returning kiwis made the demand quotient go crazy.

What goes up comes down!

To every action there us an equal and opposite reaction!

As much as Orr and Robertson take their dumb tools and try and controll the crash. There are bigger forces at play.

The price of any transaction is determined not by the willingness of the buyer to buy, but their capacity to pay. And given that most of the property sector transactions here and everywhere involved new Debt, restricting the capacity to pay is what will determine future prices. And that is happening before our eyes.

It won't matter now if we keep going down the Inflationary road or do an about-face and Deflate the economy, because both roads lead to less new Debt being created. One by Price (higher % to tame Inflation) and the other with Quality (more Debt reclaimed/repaid as the economy contracts)

While you might think of inflation as a slow boil of the economy, a deflationary meltdown is more like a guillotine chop. As the Fed has embarked on the most intense rate-hike campaign in history, we’re seeing cracks in the economy – strengthening fears of such a deflationary bust.

eg: This Buyer wanted to buy but...

$42m Gold Coast mega-mansion returns to market after sale falls over. When Chinese billionaire property developer Riyu Li reportedly sold his Gold Coast hinterland estate, Bellagio La Villa, for $42 million in February, it was touted as the highest price paid at auction in the Sunshine State.

Agreed. It's not that buyers don't want property, they absolutely do. Current rates and general inflation means buyers cannot service the debt at the asking price.

"Current rates and general inflation means buyers cannot service the debt at the asking price."

At current mortgage interest rates and household income levels, for many aspiring owner occupier buyers, house prices are UNAFFORDABLE.

Different words. Same point.

There are also those who simply don’t want to throw money into a bonfire until some semblance of fundamental value returns…

"Fundamental value"

Many people have different definitions of that term.

For example:

1) most recent comparable transaction price

2) construction cost

3) replacement cost

4) yields

5) price momentum

When there was upward price momentum up to Nov 2021, many residential property buyers believed that there was fundamental value and that house prices were justified, and ignored the warnings of high house price risks by the RBNZ. Many people have increased confidence only when there is upward price momentum.

Some of the commonly repeated arguments used to persuade buyers to buy were:

1) house prices don't fall by much - after all during the GFC, house prices only fell by 10%

2) historical house price growth for the past 50 years has averaged 7% p.a. and this can be expected to continue (aka house price doubles in 10 years)

3) ask anyone who has bought property in the last 10 years, how many have regretted buying?

I like that "The price of any transaction is determined not by the willingness of the buyer to buy, but their capacity to pay"

So what happens when the stock clears and buyers have limited options?

And millions of cashed up immigrants flood the market with gazillions of rupees and yuan $$. There will be green shoots everywhere and we'll be rich!! Rich I tell ya.

OMG....wait-what, is NZ about to run out of houses - again?

Hahahahaha

The calapse hasn't even started

People who bought full sections in West and South Auckland at the peak will have to take quite a hit if they need to sell now. I see some when searching for mortgagee sales.

I'm wondering what the bank's calculations for mortgages on properties like this was. How much would they lend on such a property and how much equity would be safe? I imagine owners of these properties will have other holdings, like a family home, that the bank will sell if the mortgage is not covered by the sale.

Some of these buyers will be developers / builders who treat the sites as 'trading stock'. Their losses will be less significant.

The last column in the table is really good information - however it would be best qualified by the year in which the rating valuation was last set.

i.e., a 2-year old valuation versus a current year one will make quite a bit of difference to the conclusions one can draw from that stat.

There is a kind of mischievous ignorance that many people like RE and both sellers and buyers use when it suits them about RV (CV).

That is the RV is more or less correct at the time they are done, but that date is different from when the data is released so is out of date on release, but any RV can be used to set a present guestimate on a today price if you know the ratio the market has moved up or down since that RV was taken.

So for example, if the RV was taken to years ago and the market value of property in that area and for a property of that similarity has increased by 20% then I can use that RV to estimate what the present value might be, prior to confirming by more immediate actual sale and/or other valuations surrounding that property.

That is all it can be used for.

You use to be able to get a table that showed this changing ratio from the confirmed sales over time and by area.

There was a time when housing was way more affordable (before 1995) and hardly can sales were by auction.

This is when supply more equaled demand.

This all changed when more restrictive policies were introduced.

This is because we all know that it is the underbidder that really sets the price at auction, which means you need at least two people to bid, which also means you need to have always one more buyer than there is a seller to keep this 'supply less than demand' scenario. IE the market is more restricted in favour of the seller.

Auctions can only exist (with few exceptions) when supply is always less than demand and are the best way to get as much money from prospective buyers as they can gouge.

Are you sure policies got restrictive around ‘95?

I think it was more to do with rising immigration

Inputs like immigration have very little effect if supply is allowed to increase at the rate of demand.

Other jurisdictions have had the same or greater rates of immigration than NZ but have not had the increase in house prices because their land use policies were less restrictive to development.

Do you read Macrobusiness? Leith ‘The Unconventional Economist’ has gone right off supply side viewpoints and is big on migration impacts (demand side). I agree with him although I think he downplays the supply side a bit too much.

no matter how much you enable supply NZ is too small to build enough houses when you have demand shocks (high immigration, cheap debt etc)

Yes, I subscribe to macro business, and Leith did not change his mind. I replied to this point you made in a comment in another article and read the link you supplied.

It had nothing to do with immigration, or restrictive land use policies.

It was the mid 80s when Roger Douglas decided to emulate Regan in the States and Thatcher in the UK, and deregulate financial markets here. Foreign capital flowed in and credit became readily available.

Then in 1987 Black Monday happened, and scared people off the stock market. Money piled back into the relatively boring and slow - but safe - property market instead, pushing up prices with the new flood of money.

The property boom we've seen since then up until about 18 months ago has almost entirely been due to increased availability of credit, and the crash we're about to have is almost entirely due to a reduction of the same. Things like immigration and land use planning are minor influences in comparison.

If that were 100% the case, why have other markets with lower rates not had the same level of house price increases?

It's likely those other externalities driving things further. Demographics, land use, that sort of thing.

"why have other markets with lower rates not had the same level of house price increases?"

Can you tell us which "other markets" are you referring to specifically?

Jurisdictions like Texas, whereas like Of Regans California were affected as is described, but as Pa1nter points out this financial deregulation caused different effects to housing depending on the different underlying land use policies used.

"Jurisdictions like Texas"

Don't know what data set you're looking at.

House price index for Texas has risen to 2.21x the level of 2009 peak in 14 years - from 227.38 in 2009 peak to 503.83 in Q32022.

https://fred.stlouisfed.org/series/TXSTHPI

If you were going to use this data set for Texas hen you would have to compare it with California https://fred.stlouisfed.org/series/CASTHPI since that was my comparison. But in reality, it is the wrong data set to use as you would have to also fact in inflation and income increases to give value to how affordable on a median income multiple the housing was. But at a glance this data set is already showing housing is more affordable in Texas.

The median income multiple automatically red flags how dysfunctional a housing market is or not.

Agree C. The Biggest driver by far is that money got forever cheaper for 40 years ....until 2021. Then everything changed.

Borrowed amounts were allowed (by the flush banks) to get bigger and bigger and bigger at 7%pa, far more than could ever be supported by average wages at 2%pa, if mortgage rates ever normalised, disaster will strike. A ticky tacky straw debt castle was built well into the clouds.......in hurricane alley.

Here we are today, where if you could easily short the NZ housing market - it's the best bet for the next few years, hands down!

I agree with your comments about credit but I strongly disagree immigration didn’t have an impact. Check out the graph at the link below, immigration picked up heavily in the 1990s. There’s pretty strong correlation, if not causation, between net migration and house prices.

https://www.infometrics.co.nz/article/2017-08-top-ten-things-know-migra…

Demographics also played a part ie. lots of boomers entering house buying age in the 90s.

Every generation become "boomers", house prices always rise and fall... it's just how you time your sales and purchases!;that makes a difference to how rich uou are.

Agreed but 100bucks is not worth a lot

The likes of credit, immigration, the need for Govt. subsidies, etc. are accelerants that can only have the effect they do if the fuel has been ignited, otherwise, they have little to no effect.

Fuel = Land/Houses

Ignition = Degree of supply restrictions

Accelerants = degree of credit availability, immigration etc.

But if the ignition is driven by large supply restrictions, then the accelerants have a huge multiplier effect, which is hard to control.

It's a first principles issue, ie have land use policies that allow housing to be supplied at the rate of demand.

Here's a couple of scenarios to think about.

What would happen to house prices,

1) if inflation got back to 15% (similar to 1980's level in NZ) and mortgage interest rates rose to 18-20% levels?

2) if banks were only allowed to lend a maximum debt to income of 1.0x to purchase a house?

For starters you'd have FHBs not competing with equity leveraging investors for the same house. RBNZ C31 paints a picture, average monthly number of borrowers vs amount borrowed FHB/Investor. Up until 2017 similar amounts being borrowed, but nearly 3x as many investors as FHB.

- 2014: FHB 1600 @ $300k, Investor 4600 @ $296k

- 2015: FHB 1855 @ $323k, Investor 5452 @ $335k

- 2016: FHB 1959 @ $373k, Investor 5236 @ $342k

- 2017: FHB 1807 @ $388k, Investor 3419 @ $331k

- 2018: FHB 2207 @ $393k, Investor 3384 @ $341k

For the same 3BDRM house on large piece of subdivideable piece of land:

Equity leveraging investors on interest only terms, can pay more than owner occupier buyers.

Property developers in Auckland, building townhouses and apartments can pay more than equity leveraging investors on interest only terms and owner occupier buyers.

Exactly. On a free cashflow basis, the investor at $500k interest only is paying $1k per month, while a FHB on P&I is paying nearly $2k per month on the mortgage. The investor, because they're pretending they're running a business, then also (up until recently) deducts the mortgage interest as an expense. The FHB, who also derive an income from paying for somewhere to live/rest between work hours, did not have that luxury.

In my opinion this is the single most important change to implement - i.e investors must have the same mortgage terms as FHB (P&I payments to actually pay off the loan in 25 years).

Couple that with a ban on home equity use for investment properties and then we would be very close to a housing market that is geared towards homes vs investment.

If the residents of NZ want to encourage more residential ownership by residential owner occupiers then it comes down to government priorities and government policies.

Singapore focuses on encouraging resident owner occupiers and less on owners of multiple residential dwellings, non resident owners with their tax policies.

1) Property taxes (which we call rates)

i) note that they differentiate between owner occupied and non owner occupied,

ii) and they are on progressive rates - the higher the imputed rent, the higher the rate to determine property taxes (which we call them rates in NZ)

https://www.gov.sg/.../property-tax-on-residential-property

https://www.iras.gov.sg/.../property.../property-tax-rates

Imagine bringing in a progressive rate system in NZ to calculate rates.

2) Stamp duty is differentiated between

1) citizens vs residents vs non resident buyers

2) first, or any property beyond their first property

https://www.propertyguru.com.sg/.../calculators/stamp-duty

https://twitter.com/GRomePow/status/1643083095376285698?s=20

The Singapore progressive multi property tax is an excellent idea.

"On a free cashflow basis, the investor at $500k interest only is paying $1k per month, while a FHB on P&I is paying nearly $2k per month on the mortgage. The investor, because they're pretending they're running a business, then also (up until recently) deducts the mortgage interest as an expense. The FHB, who also derive an income from paying for somewhere to live/rest between work hours, did not have that luxury. "

Here is an interesting comparison of the different cashflow scenarios for a residential property investor who rents out their property in the long term residential market.

https://youtu.be/WQmOd6JL-6E?t=788

Currently, the cashflow of such a property investor would be a negative cashflow ranging from negative $209 per week (a property investor with a mortgage of 75% LVR, on interest only terms) to negative $515 per week (property investor on a 100% LVR, P&I mortgage)

Compare that with an owner occupier buyer at the same 6% mortgage interest rate, buying the same new build house at the same price used in the video on the following financing terms:

1) 10% deposit (90% LVR), 30 year mortgage, P&I - negative $728 per week (this is $210 per week more than the worst case property investor (or 40% more) of $515 per week)

2) 20% deposit (80% LVR), 30 year mortgage, P&I - negative $647 per week (this is $132 per week more than the worst case property investor (or 26% more) of $515 per week)

3) $150,000 deposit (same as deposit used in above video), 30 year mortgage, P&I - negative $599 per week (this is $84 per week more than the worst case property investor (or 16% more) of $515 per week). On a like for like basis, the property investor who puts down $150,000 deposit pays $209 per week, compared to the owner occupier who pays $599 per week for the same property - so the owner occupier pays $390 more per week (or 186% more) than the property investor.

For the owner occupier buyer, they are paying more than a property investor in EVERY scenario. Both are purchasing the same property, at the same price, at the same mortgage interest rate, for the same mortgage term.

Due to these cashflow economics, no wonder the house ownership rate in NZ has fallen to their lowest levels in almost 70 years.

https://tradingeconomics.com/new-zealand/home-ownership-rate

https://www.stats.govt.nz/news/homeownership-rate-lowest-in-almost-70-y…

Why would you leave out the other two choices that are automatically included in such a matrix? Namely low prices and low rates or high prices and high rates, although the latter is starting to happen for purchasers who bought at the peak and are seeing their interest rates go up on renewal.

But to answer your point 1) It is far better to own a house at 3x median multiple in the 1980'a at the higher interest rate and inflation because you could fix in the debt at a far lower total amount and then have inflation of both house prices and your income 'inflate' your debt away. That's why so many people people who bought then and prior to are debt free and have high equity, even if that equity is unearnt and is mainly due to non-value added monopolistic rentier gains.

The point about Texas is that it has far lower prices due to its land use policies than the likes of California even when they share similar interest rates, immigration etc. And yes even they saw a greater than usual increase over Covid due to supply disruption, but because their land supply chain has never been disrupted then they had the least absolute $ increase. There are many things that are hard to control in the supply chain but the easiest one to control is the one you control most directly ie the land under your feet, yet that is the one most jurisdictions choose by bad policy to restrict unnecessarily.

Out of the four options, a matrix of house prices and interest rates gives you, Texas has the best with low house prices and low-interest rates, compared to any contemporary.

The oldies often bemoan 22% interest rates, I suspect an exaggeration on not only the interest rate but how long it actually lasted, but anyway I'd rather pay 22% on a smaller loan than 2.2% on a larger loan, even if wage inflation were only 3 - 5%. Because that 3 - 5% makes a bigger dent against the principal on a smaller loan. Oh imagine how good it would be if we had the wage inflation of the "22%" interest rates days, back when Muldoon had to legislate a freeze in wages because people were getting such big increases. They don't know how lucky they were back then.

"Why would you leave out the other two choices that are automatically included in such a matrix? Namely low prices and low rates or high prices and high rates, ..."

Let me clarify further.

Here's a couple of scenarios to think about.

What would happen to house prices in NZ from current house price levels,

1) if inflation got back to 15% (similar to 1980's level in NZ) and mortgage interest rates rose to 18-20% levels?

In this scenario, I am assuming all other current existing conditions that currently exist in the residential property market in NZ are unchanged - such zoning laws, construction costs, foreign ownership laws, tax laws, and current house price levels. (i.e from current housing market conditions in NZ, we are only changing the one variable above)

2) if banks were only allowed to lend a maximum debt to income of 1.0x to purchase a house?

In this scenario, I am assuming all other current existing conditions that currently exist in the residential property market in NZ are unchanged - such zoning laws, construction costs, foreign ownership laws, tax laws, and current house price levels. (i.e from current housing market conditions in NZ, we are only changing the one variable above)

"There was a time when housing was way more affordable (before 1995)"

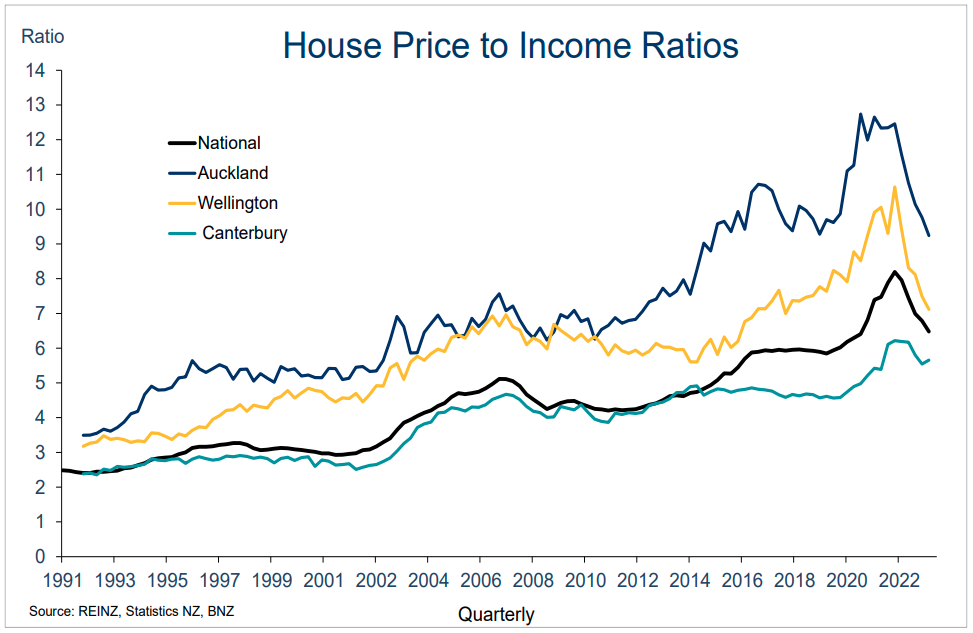

House prices in New Zealand pre 1995 were on a nationwide house price to income ratio of less than 3.0x.

Refer

https://www.interest.co.nz/sites/default/files/2023-06/bnz-jon3.png

{kind=link}

Yes, I have been pointing that out and the reasons why on this site for on a decade now.

1995 you say? ... Actually a few years later.

This was when the National Government of the time decided they didn't want to do social housing and that private landlords could do it instead.

They very quietly changed the tax laws to enable it. Nobody noticed - except some tax accountants - as this 'brought us into line with other OECD countries'. Except it didn't.

All the OECD countries had Capital Gains Taxes at that time!

It's been good to read Interest.co.nz's articles on real estate. They appear to be better balanced unlike the NZHerald and Stuff's opinion articles on real estate.

One question that always comes to mind reading these articles is using statistics to support one thought line or another. Generally, %'s are used to support the argument (which in theory should be good), however, the way they are used feels more like a running commentary on divining tea leaves.

I was happy to see in this article the actual number of sales being compared instead of just the percentages which would have been misleading. Too often too much store is put into % movements.

And often the measure, either average or median house price is used to describe the entire market. This is not useful.

It would be much better if the information could be broken down into housing segments or categories. (e.g. Premium, Full Houses, Terraces, Apartments, lifestyle, new builds etc). Then the averages and percentages might be more helpful.

For example, it's obvious that there is a demographic sector with a lot of money who are chasing after premium housing of which there is limited availability. Intuitively that sector will be holding up well. Including that segment in the overall averages skews the figures and percentage gains (or not) markedly (due to high $$ sales and low numbers sold.

Other demographic information would also shed more light on what is happening though that is harder to gather. Otherwise, again it becomes a matter of divining tea leaves to speculate what might be happening (which is what unfortunately the market influencers are doing way too much and too often). But it should be possible to gather this information at the point of sale.

Interest.co.nz is doing a good job in reporting. Is it also able to influence how statistics are collected?

Keep up the good work

Anyone purchasing a house today will probably see the value of house drop 15% over next year, we have already seen a 25% drop in many areas over last 18 months. Many people have pointed this out on this website but a few just keep talking up market.

Yes agree.

I'm telling friends who are looking to buy now (typical FHBs) to only make offers in the range of the 2014 to 2018 valuations - as this is what the market will most likely be in a year or two.

Any rebound from this early stage crashing market, may possibly start in 2026/28 and will only be at the meagre 2% or so, with DTIs regulated and seeing it that all spruikers are having to eat dead rats for dinner going forward. Or perhaps the leeching spruikers can get real, productive jobs?

So don't be the "next sucker" - "bag holder" allowing an overpriced liquidation in the currently collapsing market, by a greedy- out of touch vendor.

The market confidence to buy has completly evaporated, no matter the concerted efforts to refire the Housing PONZI of the scullerious vested interests of the nefarious AC/TA, OneGoof, Holmes.c and REA toads.

If they wont negotiate to these date range valuations - walk away. Those vendors will be begging you back in 6 months to talk turkey, at that stage take another 10% to 15% off your first offer and give them 3 days to accept or walk.

All in my well researched and IMHO.

Indeed. Let the dead weight of to much unproductive debt crush the speculative. Leverage absolutly functions in reverse.

Aka compounding capital destruction.

"Leverage absolutly functions in reverse"

Many property investors who were willing to take on high levels of debt, were told:

1) debt is eroded by inflation

2) house prices rise with inflation

It's that pinching point where inflation arrives, interest rates rise, and you have to manage the cashflow in the short term until your cashflows "inflate" to cover the increased carrying costs. I don't think new investors quite grasp the math of it all.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.