By Alex Tarrant

New Zealand is included in a group of developed economies that have become housing market "high flyers" as they import significant doses of monetary easing by major central banks, Goldman Sachs says.

Housing markets that had experienced rises in prices since the start of 2009, including small, open commodity producers like New Zealand, have been placed in the select group, some of which faced concerning scenarios in the face of further monetary easing.

That meant tricky challenges for policy makers reluctant to boost interest rates to contain house prices, as that could also boost their currencies to the detriment of the rest of their economies.

In Goldman's latest Global Economics Weekly report, researchers Kamakshya Trivedi and George Cole say that policy pickle explains the recent fad for using macro-prudential measures such as controlling loan-to-valuation ratios (LVRs).

In New Zealand, the Reserve Bank is reluctant to use its new macro-prudential tool kit in conjunction with monetary policy (the Official Cash Rate) in its quest to keep general annual inflation around 2%.

Rather, use of macro tools like LVR controls, counter-cyclical capital buffers and core funding ratios, is being lined up by the Bank in the financial stability sphere; ie. if the Bank reckons a pending house price bubble poses a risk to the soundness of the financial sector, it may use those tools to try and defuse the bubble rather than just lifting the OCR. But in its quest for general price stability, the OCR is still the Reserve Bank's primary tool.

High fliers

Globally, residential home prices had stabilised since the housing bust of 2007-09. But that statement hid significant variation underneath the global aggregate: house prices had become more local and far less correlated in the aftermath of the crisis, Trivedi and Cole said in their report

Globally, residential home prices had stabilised since the housing bust of 2007-09. But that statement hid significant variation underneath the global aggregate: house prices had become more local and far less correlated in the aftermath of the crisis, Trivedi and Cole said in their report

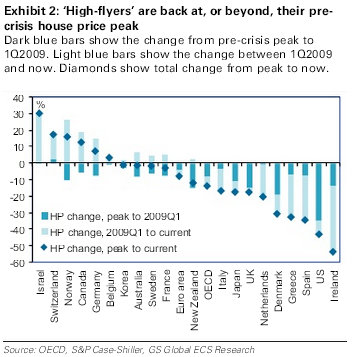

"An aspect of that fall in correlation is a sharp bifurcation between two groups: countries where prices have increased strongly and are up cumulatively since 1Q2009, and countries where the housing downturn looks to be continuing," Trivedi and Cole said.

"These two groups defy an easy geographic or economic classification. The group of ‘housing high-flyers’ is made up of a handful of small open economies such as Switzerland, Israel, Sweden and Finland; the ‘core’ Euro area economies of Germany, Belgium and France; and a number of commodity exporters, including Norway, Canada and Australia," they said.

"Typically, these countries experienced relatively modest declines in real house prices in the crisis (from their respective peak levels to the lows of the global financial crisis in 1Q2009), and have seen strong real house price gains in the subsequent recovery.

"The ‘housing low-lyers’ – countries where house prices have stabilised or are still declining –includes, perhaps unsurprisingly, those places that saw the largest housing busts, such as the US, Ireland and Spain. But it also includes parts of the Euro area periphery, such as Greece and Italy, in addition to the UK, Japan and Denmark.," Trivedi and Cole said.

New Zealand was included just within the high-flying category, having experienced a slight rise in house prices between the first quarter of 2009 and now. However, unlike surging Israel, Switzerland, Norway, Canada, and Germany, New Zealand's real house prices were still about 10% below their pre-crisis peak, which was highlighted in yesterday's QV release.

Easy conditions, commodity demand

While part of the explanation for the strong house price performance in the ‘high-flyers’ lay in the strong cyclical performance of these economies, the housing markets in these countries also appeared to have benefited from excessively easy financial conditions, Trivedi and Cole said.

"The basic story here is straightforward. The housing markets in many of the ‘high-flyers’(Canada or Norway, for example) were hit only moderately hard during the global financial crisis, and the economies in these countries bounced back strongly – partly on the back of commodity demand from the faster-growing emerging market economies," they said.

"Nevertheless, financial conditions in these countries over the past several years have been relatively easy, partially due to the easing ‘imported’ from the major G4 central bank policies. With significant output gaps and policy rates close to the zero bound, central bankers in the G4 have been pushing down interest rates at longer maturities, and this has kept longer-dated rates lower than may be warranted in certain countries."

Does housing just do better than the rest when there's easing?

Trivedi and Cole noted it was always tricky to pin down precisely whether a requisite amount of easing was ‘excessive’ or ‘inadvertent’.

"For a start, different countries operate with different policy frameworks. Moreover, issues of endogeneity loom large, meaning that the ‘housing high-flyers’ may have enjoyed strong recoveries partly on account of the monetary stimulus, making it hard to separate the two," they said.

"So the stronger house price performances here may simply reflect that domestic/non-traded areas do better if easing is successfully provided in the face of external pressure."

Should we be concerned?

In assessing whether the sharp increases in house prices in the ‘housing high-flyers’ since 2009 were concerning or not, it was also important to take account of measures of valuation and affordability on a longer-term perspective. In this respect, there are important differences among the ‘housing high-flyers’.

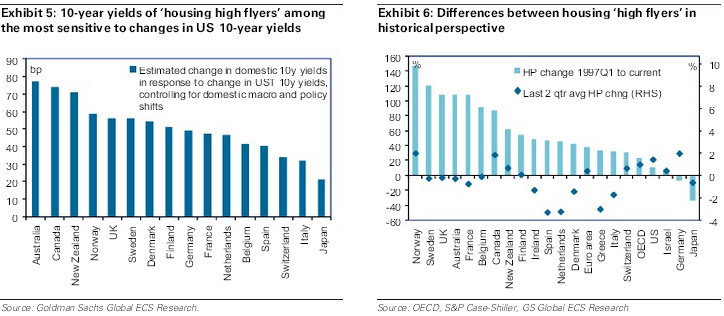

"Exhibit 6 shows the cumulative change in house prices for each country since 1997 (the year from which we have data on a full sample of countries from the OECD). It highlights important differences between high-flyers such as Norway and Germany, both of which have recorded rapid house price gains in recent quarters," Trivedi and Cole said.

"In Norway, house prices are up by about 140% since 1997 in real terms, whereas in Germany they are more or less unchanged over this long period," they said.

This suggested that it may be premature to worry about any kind of overheating in the German housing market, whereas such concerns may be more justified in Norway or Canada. On this measure, New Zealand's housing market sat just below Canada.

"And even while acknowledging that it is difficult to make cross-country valuation comparisons since different valuation levels may be ‘fair’ depending on country-specific local factors, conventional metrics such as house-price-to-rent or house-price-to-income measures tell a similar story," Trivedi and Cole said.

"Exhibit 7 shows the house-price-to-rent ratios for some of the ‘housing high flyers’. They show the degree to which valuation metrics have ‘cheapened’ in the cases of Germany and even Switzerland before recent increases.

"Even in Sweden, where valuations have increased over the recent decade, they are only now back at similar levels to the early-1980s and early-1990s, just ahead of their own housing bust," they said.

"By contrast, valuations appear more challenging in Norway, Canada and Australia, although they have‘cheapened’ somewhat in Australia in recent quarters. While not shown, house-price-to-income measures exhibit an identical pattern of valuation across the ‘housing high-flyers’.

Look at consent levels too

In addition to valuations, it was also worth considering whether house price increases were accompanied by significant surges in home-building activity.

"Because housing is extremely durable, housing busts tend to be more severe and more painful when there is over building of homes prior to the bust – as was the case for example in the recent housing busts in the US and Spain," Trivedi and Cole said.

"While cross-country comparisons of construction activity are difficult, Exhibit 8 shows an index of building permits – its current level relative to a long-term average and its historical peak relative to a long-term average. On this metric, ‘high-flyers’ like Canada, Norway and Switzerland look relatively more exposed –current permit levels here are at or above the historical average in these countries and not far off recent peaks. By contrast, Germany, Sweden and Australia have permit levels below long-term averages," they said.

New Zealand building consents are also below long-term averages. See current and past levels here.

Easing to continue

In recent months central banks in the G4 (US Federal Reserve, Bank of Japan, European Central Bank and Bank of England) had embarked on a fresh round of easing measures.

"In the US, QE3 or open-ended purchases are targeted initially at MBS, but are likely to be extended to Treasuries at the end of the year after the expiration of Operation Twist. The Bank of Japan added to its Asset Purchase Program last week, including JGBs, corporate bonds and other assets (ETFs and REITs). We expect the Bank of England to expand its Gilt purchase programme this week, and the ECB has committed to outright monetary purchases conditional on sovereign agreement," Trivedi and Cole said.

"Together, these measures are likely to keep the pressure on major markets’ long-dated yields. And, in turn, this is likely to keep easing pressure on yields and financing conditions in many of the ‘housing high-flyer’ economies," they said.

Short-term policy rates blunt

To the extent that this easing pressure was unwelcome – particularly from the perspective of providing fuel to fresh housing bubbles – this placed policymakers in the ‘high flyers’ in a tricky dilemma.

"Short-term policy rates area relatively blunt measure for dealing with any excesses in the housing market. In line with the regression evidence discussed earlier and given the pressure from lower long-dated global yields, policy rates may need to be raised substantially to move the needle on mortgage rates significantly, and in the process the authorities may have to accept considerable collateral damage in other parts of the economy," Trivedi and Cole said.

"Furthermore, any exchange rate appreciation that follows is likely to affect a country’s export competitiveness," they said.

These considerations explained, to a significant extent, the current fad for macro prudential measures among global central bankers and regulators.

"Since sector-specific restrictions on loan-to-value ratios or capital charges can be directly applied to housing-related excesses, they allow policy makers to sidestep any policy tightening that can affect the broader economy," Trivedi and Cole said.

"A number of such macro- and micro prudential measures are either already in operation or in discussion among the ‘housing high-flyers’ where the risks around the housing market are most acute:

- In Norway, the Financial Supervisory Authority (FSA) recommended a maximum prudential loan-to-value (LTV) ratio of 85% in December 2011, down from a 90% maximum (which was instituted in 2010), with a risk of higher capital charges for banks not meeting these guidelines.

- In Sweden too, a maximum LTV of 85% was introduced in December 2010, and there is ongoing discussion about additional macro prudential regulation to be enshrined in legislation.

- In Israel, only last week the MPC cut rates even as the Supervisor of Banks moved to tighten mortgage lending conditions by limiting the LTV ratio for housing loans to 70% from November onwards. This is a continuation of previous macro prudential measures by the Banking Supervision Department of the Bank of Israel (which included limiting the maximum floating rate component of housing loans to 33.3% in 2Q2011).

- In Canada, regulators have followed primarily two approaches: ‘jawboning’ by the Bank of Canada (including the recent modest strengthening of the tightening bias in its October policy statement), and tightening the requirements for government mortgage insurance in at least three separate steps since 2010, most recently in summer this year. From July 2012, the CMHC (Canadian Mortgage and Housing Corporation), which insures about three-quarters of Canadian mortgages, has lowered the maximum LTV ratio to 80% for mortgage refinancing (from 85% in 2011), reduced the maximum amortisation period to 25 years from 30 years, and fixed maximum levels of debt-service ratios.

Even in the ‘housing high-flyers’ such as Germany, where valuation concerns appeared less pressing as of now, plans were afoot to establish the framework for undertaking macro prudential policy in the future.

"As Dirk Schumacher described, the German government is doing the legal groundwork to set up a national Board for Financial Stability (Ausschuss für Finanzstabilität) that will monitor macro prudential risks at the national level.The board will consist of representatives from the finance ministry, the financial supervisory body, BaFin, and the Bundesbank, with possible measures including new capital charges, either generally applied across the board or for specific products such as mortgages," Trivedi and Cole said.

"And while it is certainly wise to prepare for the future, our quick look at simple metrics of valuation and recent construction activity suggest that, for now, housing market related risks may be relatively greater in countries such as Canada and Norway, where valuations and activity levels appear more stretched, than, say, in Germany," they said.

2 Comments

What is it we should be thinking about the words "High Flying Housing market" - We didn't do anything about the Finance Company trainwreck before it happened. Maybe we should do something about this one.

Sounds like the re-floating of the housing market is well underway worldwide, and showing significant improvements in some countries within the OECD. Some non-OECD countries have been booming all along, some city prices are up 10 times from the late 90's and still gaining strongly; mind you, I would not buy propety in any of them, at any price!

Who would have thought Israel had such high demand for housing when their population keeps shrinking and very few people are brave enough to immigrate there.

The world is once again, awash in cash! And so, we're off to the races... Not.

Hevi Groswaite

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.