By Gareth Vaughan

Is the Reserve Bank, as prudential regulator of New Zealand's banks, little more than an ambulance at the bottom of the cliff?

On the surface that seems absurd given the increased regulation of the banking sector over recent years through the likes of the introduction of restrictions on high loan-to-value ratio mortgage lending, a $550 million outsourcing policy, and imminent increases to regulatory capital requirements.

But the International Monetary Fund (IMF), in its Financial Sector Assessment Program (FSAP) report on New Zealand - its first since 2004 - paints the picture of a bank regulator that's hands off on a day-to-day basis. The IMF highlights an idiosyncratic light handed regulatory approach.

Notably the IMF points to the bizarre scenario whereby the Australian Prudential Regulation Authority (APRA) undertakes on-site visits of New Zealand banks but the Reserve Bank of New Zealand (RBNZ) does not. APRA does on-site visits of NZ's four Australian owned banks ANZ, ASB, BNZ and Westpac. During these RBNZ staffers tag along but merely in an observer capacity. This, the IMF suggests, ought to change.

The IMF's views will be no surprise to the RBNZ. Deputy Governor and Head of Financial Stability Grant Spencer told me in December NZ would get "the expected result of not ticking a lot of the boxes" in the IMF review. At that point the RBNZ had already received the IMF's draft FSAP reports.

'No direct access by supervisors to bank records or files'

The IMF points out the RBNZ doesn't conduct inspections, and on-site interaction with banks is merely prudential meetings providing an opportunity to discuss results of supervisory analyses and other issues.

"Thematic visits have also been conducted to review systemic issues in deeper detail. [But] the scope of the thematic visits does not include direct access by supervisors to bank records or files, with the review relying on increased information requests and questionnaires," the IMF points out.

"Overall, the lack of first-hand independent verification of prudential returns and assessment of banks’ risk management practices prevents the RBNZ from having a thorough understanding of the banks."

"The RBNZ is encouraged to be more active in the joint on-site visits [with APRA], focusing on work that serves the objectives of home and host supervisors," the IMF says.

"RBNZ could seek proactive engagement during the on-site visits conducted by APRA, in order to gain knowledge of, and confidence in, the home supervisory approach and the techniques that are central to APRA’s supervisory model."

Among recommendations in the IMF's 2004 FSAP was that the RBNZ should consider commissioning third-party reports and establish a small specialist team to make focused, on-site bank visits on particular aspects of credit and operational risk. In this year's FSAP the IMF notes of that 2004 recommendation: "The RBNZ elected not to establish a small, specialist in-house team to make focused on-site visits on particular aspects of credit and operational risk."

In 2014 I argued less dogma and more flexibility was needed in the RBNZ's risk management strategy. I noted the RBNZ's reasoning for why it doesn't conduct on-site reviews. This was that they could give rise to moral hazard, reduce the incentives on management, as well as increasing the possibility that a failure will be seen as a "supervisory failure" and therefore make a government bail-out more likely. I suggested this comment sounded like regulatory butt covering.

'The RBNZ’s enforcement is currently based primarily on breaches that have already occurred and is not preventive'

The RBNZ approach to supervision relies on three pillars being self, market, and regulatory discipline. The IMF points out the self-discipline pillar relies on directors’ attestations to the fact that the bank has adequate risk management systems in place.

"The RBNZ has issued limited guidance as to what constitutes adequate risk management. The vacuum created by the RBNZ not stating its expectations on adequate risk management is likely filled by foreign banks basing their attestations on home-country supervisors’ standards. For domestic-owned banks, it is likely that each may be following standards adopted from different sources. The RBNZ is very familiar with the Australian standards, but for the next tier of foreign-owned banks (as well as for the tier of domestic-owned banks) it would need to review standards on-site. Not issuing standards may result in an uneven playing field as some banks may be following stricter standards than others, thus diminishing the value of disclosures as directors are attesting to different standards," the IMF says.

"An effective self-discipline regime needs to be supported by a well-developed regulatory framework and swift enforcement when banks violate the rules. The RBNZ has broad enforcement powers, but the lack of regulatory benchmarks and the high legal threshold for issuing directions (orders) make swift enforcement less likely. To issue directions under section 113(1)(e) of the RBNZ Act when a bank is conducting business in a non-prudent manner the consent of the Minister of Finance is required. Demonstrating imprudent behavior based on, for example, inadequate risk management or insufficiently developed risk appetite statements, is made difficult by the lack of supervisory standards. As a result, the RBNZ’s enforcement is currently based primarily on breaches that have already occurred and is not preventive."

Although the RBNZ has extensive powers in licensing, supervision and enforcement, the IMF argues its effectiveness would be strengthened with broader powers to impose binding standards in all areas of prudential regulation given such powers are currently limited to solvency and fit-and-proper requirements.

"The framework for licensing of overseas insurers (branches) could be strengthened to ensure the RBNZ assesses the equivalence of foreign regulatory regimes. Supervisory engagement, particularly with large institutions, needs to move towards communicating supervisory expectations and requiring action," says the IMF.

The most significant risks in NZ

The areas of credit risk, problem assets, provisions and reserves are described as the most significant risks in NZ. Therefore the IMF suggests detailed guidelines should be issued addressing loan classification, extended loans, forbearance, nonperforming and cured loans, and provisioning.

"There need to be on-site reviews to ascertain credit portfolio quality and to verify the accuracy of internal bank reports shared with the RBNZ."

The IMF recommends amending the Reserve Bank Act to make compliance with RBNZ-issued supervisory policy evidence of prudent banking. Furthermore, it suggests issuing supervisory policy documents as warranted such as on credit risk, carrying out targeted on-site programmes either directly or through external experts to verify regulatory reports, risk management, and the quality of credit exposures, boosting proactive cooperation within trans-Tasman agreements to support cross-border supervision synergies, considering options to facilitate the taking of enforcement action based on supervisory judgment; and improving analysis to support Proportionate Risk Evaluation Surveillance System (PRESS) ratings by retaining work papers to document determinations on adequacy of risk mitigants.

'Testing of attestations through bank-specific reviews is required'

Another aspect of the RBNZ's "supervisory philosophy" that's probed by the IMF is that the banks’ own management and directors are in the best position to design risk management systems and establish limits based on the risk appetite and capital available to support those risks.

"The guidance issued by the RBNZ does not sufficiently communicate its expectations on the elements it considers necessary in management systems to monitor and adequately control material risks," the IMF says.

"The RBNZ does not impose direct requirements on banks to have comprehensive risk management policies and processes, except in the areas of capital adequacy and liquidity. The RBNZ relies on the required attestation provided by directors with every financial statement disclosure that: 'the bank had systems in place to monitor and control adequately the material risks of the banking group, including credit risk, interest risk, currency risk, equity risk, liquidity risk, operational risk, and other business risk, and that those systems are being properly applied.' Accuracy of the disclosure is tested off-site by the RBNZ through report analysis and by on-site interviews with bank management."

The IMF points out that the RBNZ's non-intrusive approach to supervision stands in contrast with the Core Principles for Effective Banking Supervision (BCP) established by the Basel Committee on Banking Supervision and the Insurance Core Principles (ICP) of the International Association of Insurance Supervisors, and can impair the effectiveness of market and self-discipline.

According to the IMF, the effectiveness of the RBNZ approach, and its convergence with the BCP and ICP, is hindered by:

(i) the absence of supervisory testing to determine compliance and the effectiveness of risk management, and

(ii) limited supervisory guidelines and regulations that could serve as benchmarks for the three pillars. While policy implementation will take significant time, there is a need to close the most significant gaps by:"Issuing enforceable supervisory standards on key risks. Such standards, tailored to reflect the complexity and risk profile of the institutions and the system, would provide transparency to market participants regarding the supervisor’s expectations in the areas being attested to by directors. Standards also help support supervisory judgment to implement preventive enforcement. Regulation of governance, risk management and controls and undertaking risk assessment in these areas need to be strengthened to promote the effectiveness of governance in practice.

Reviewing the enforcement regime to promote preventive action. Compliance with the guidelines issued by the RBNZ should serve as evidence of prudent banking and insurance. Also, in the case of banking, the legal need for the consent of the Minister of Finance to issue directions in cases not involving a systemic impact should be removed.

Initiating on-site programs to test the foundation of the three-pillar approach and directors’ attestations. The RBNZ has performed off-site thematic reviews to profile banks’ risk management in areas of concern, such as dairy and real estate. The off-site process PRESS (being Proportionate Risk Evaluation Surveillance System) and iPRESS (being Insurance–Proportionate Risk Evaluation Surveillance System) rates financial institutions based on their risk profile (and their systemic impact). The on-site activity, which could be undertaken by the staff of RBNZ or by external experts, should be targeted to areas of high risk, to issues identified through off-site analysis, or to determine how banks and insurers are managing new risks and products. It is also important to test the accuracy of the regulatory reports.

The IMF also notes effective supervision requires political will as a catalyst.

An important precondition for effective banking supervision is the willingness to act. As is well-established IMF policy, a positive assessment of the supervisor’s ability to act - based on its resources, authority, organization, constructive working relationships, and as evidenced by actions taken to impose corrective action - is not sufficient to ensure effective supervision. This must be complemented by the 'will' to act in order to take timely and effective preventive actions in normal times, and corrective actions in times of stress.

Developing this 'will to act' requires a clear and unambiguous supervisory mandate, operational independence coupled with supervisory accountability and transparency, skilled staff, and an arm’s-length relationship with the industry that avoids 'regulatory capture.' The Principle by Principle assessment reflects on the supervisor’s 'ability to act' and the conditions needed for their 'will to act.' However, effective supervision also requires as a catalyst a political will that cannot be measured nor evaluated externally.

The IMF also probes what's behind the RBNZ's "hands-off supervisory philosophy."

The statutory objectives of the RBNZ are broadly defined as 'promoting the maintenance of a sound and efficient financial system; or avoiding significant damage to the financial system that could result from the failure of a registered bank.' Broad definitions of concepts such as 'sound and efficient financial system,' 'significant damage,' or a focus on 'systemic implications' only, have allowed the RBNZ to develop over time a particular hands-off supervisory philosophy that departs from conventional, more resource-intensive supervisory practices.

For example, the current approach has limited appetite for independent verification of supervisory returns and first-hand knowledge of the soundness and risk management of individual banks. The supervisory objectives have to be clarified at an operational level. Towards this end, the RBNZ is currently defining its risk appetite framework, which will reinforce the RBNZ’s statutory objectives by translating them into practical outcomes, and clarify how supervision has to be conducted in practice.

The IMF also sees a need for the RBNZ to get increased resources for banking supervision.

While RBNZ staff are highly competent, insufficient resources are an impediment to enhancing the effectiveness of the three pillar approach, even if the low-intensity approach is retained. The competence and professionalism of staff is recognized by market participants, but the RBNZ operates under specific resource constraints and numbers are insufficient. Strengthening the regulatory discipline pillar will require increased resources, including technical capacity to develop prudential requirements and guidelines, deepen the analysis that supports the supervisory ratings, and to develop a supervision policy that reflects a balance between risk and efficiency costs of supervision. The FMA, in turn, needs to build more insurance expertise to promote adequate conduct supervision of the sector.

The RBNZ should reassess the adequacy of the resources assigned to its banking supervisory function. This will make it possible to address the recommendations of this assessment that are oriented toward strengthening the supervisory process, enhancing knowledge and risk assessment of supervised entities, facilitating early action and preparedness for crisis management, and allowing staff to analyze broader themes relevant for financial stability.

Just how well resourced is the RBNZ & what financial pressures is it under from the Government?

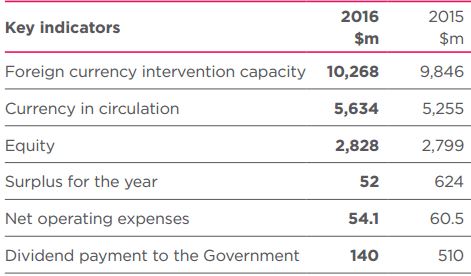

In terms of the RBNZ's resourcing, its 2016 annual report shows 240 full-time staff. Average years of service are 8.6, with 16% annual turnover. During the year the RBNZ spent $32 million on personnel, including training and redundancies. The RBNZ recorded a $52 million annual surplus and paid the Government a $140 million dividend.

The RBNZ receives no direct taxpayer funding through the Parliamentary appropriation process. Its main source of income is the return on investments held, which are funded by the issue of currency and by the RBNZ’s $2.8 billion of equity.

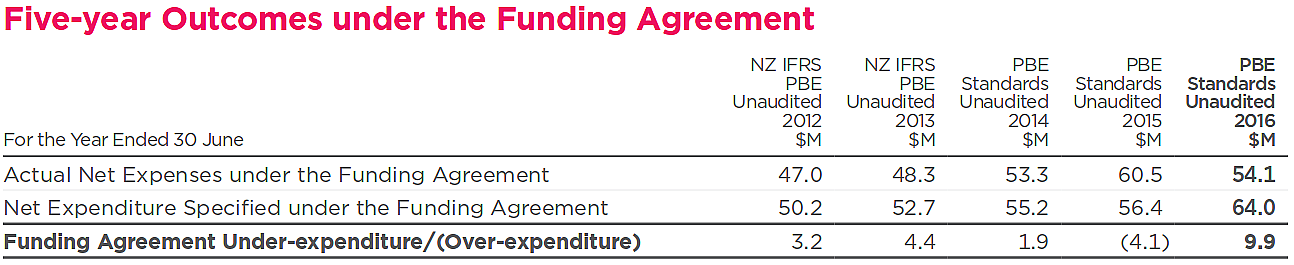

Under the Reserve Bank Act, the Minister of Finance and the RBNZ Governor have a five-year funding agreement specifying the amount of the RBNZ's income to be used to meet operating expenses in each of those years. The size of the dividend paid to the Crown is determined by the Minister of Finance each August on the recommendation of the RBNZ.

The annual report notes the "tight" current funding agreement, running until 30 June 2020, provides for annual funding increases of about 1%.

"This has involved careful expenditure management, several redundancies last year and a major review of the RBNZ’s space needs...The new five-year funding agreement required the Bank to find substantial efficiency savings. A number of staffing and business process efficiencies were implemented this year, and further savings will be made in the remaining years of the funding agreement. All business areas were reviewed thoroughly. A change management programme was adopted with a focus on working adaptively. Staff were engaged in seeking continual improvement in business processes," the RBNZ's annual report says.

The annual report also notes 2016's net operating expenses of $54.1 million were $9.9 million less than in the funding agreement. However, this "underspend" is expected to reverse in the remaining years of the funding agreement.

The charts below come from the RBNZ's annual report.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

10 Comments

"Is the Reserve Bank, as prudential regulator of New Zealand's banks, little more than an ambulance at the bottom of the cliff?"

Yes but with their hands off regulation approach they have set up NZ depositors as the true ambulance at the bottom of the cliff - with OBR - with the introduced hazard of encouraging bank runs should financial stability of a single bank becoming in question.

yes and their premise that all depositors are investors in the banks and should know and accept the risk hence the OBR.

try telling that to the average kiwi and they will look confused and ask what you are on.

We've basically setup a system that rewards greed and risk (a 'take' and 'want' and 'me' and 'now' society).

If you decide you want to be prudent and leave some cash in the bank for a rainy day, that money gets taxed, it gets a pitiful return in terms of interest paid and is at risk of an OBR event to bail out a greedy landlord/investor who's over extended him/herself in their desires to create a 'portfolio'.

How do we generate a paradigm shift away from this dumb way of seeing the world? Why have we created an 'all in' society - in a way buying and selling houses now resembles a game of poker?

What does the 'O' in OBR stand for? Open! The alternative is a "C" - Closed. Which would you prefer, because seeing any failed institution shut the doors with a "C" and let the creditors ( yes, the depositors) guess at what will happen would likely be a worse alternative?

Anyone else with significant sums deposited with the banks want to organise a run? See if together we can tumble the NZ housing market and bring it back to its intrinsic value and then start over - from a place of truth, not debt laden lies?

(Would it be illegal to collude against the banks, given they appear to be colluding against depositors?)

TM2 and all his mates who individually own millions to the banks, on interest only terms, who are eroding the quality of life in NZ to young people who want to get established, won't have a leg to stand-on if a bank run starts. It might take an immoral act to end an immoral behavior that has crept into our society..

Perhaps I should give Bill English a call and tell him we know how to fix the housing crisis once and for all?

Oh, come on, we Kiwis are quite laid back, aye.

Thank you Gareth for a most worthwhile expose. It's past time to publicly discuss and rewrite the rules of engagement between the bank regulator and the regulated.

Thanks Gareth, sharetrader. The simplistic mandate of the RBNZ can render it a slave to the inflation rate, making foresight and action on other issues important at all times and very important at some times. The Financial Times just blamed the sinking NZD on a drop in house sales. Let's hope they're wrong. A weak NZD could raise inflation, forcing RBNZ-bot to raise rates, causing another drop in house sales and prices. Not saying we are definitely in any doom loop here but RBNZ prudential supervision of housing-happy banks is probably a Good Thing. Us bank customers can only do so much.

Im reading "the end of alchemy" by Mervyn King... Great book..

He mentions that in the USA from 1865 to 1934 Bank shareholders were subject to "double liability".. ie. If their Bank failed they were liable for an amount double their amount of initial equity.

Before the 19th century , some places imposed "unlimited" liability on the shareholders of Banks.. ( I'm guessing those shareholder had quick getaway escape plans !! )

The book highlights the precarious position of risk and uncertainty that the Private Banking system operates in.. It is inherent in the nature of modern Banking , with its extreme level of leverage and size, that the system is fragile.

He also mentions that too big to fail was , pretty much, a conscious plan of Bankers to derive a "subsidy" from the public... ie.. the bailout of too big to fail ( which is a form of insurance which enables the Banks to pursue greater Risk )

It is surprising how open the discussion in England has been about banking. The issues are described in a much more grown up manner, I find it rather intriguing. Whereas in the US it is all about allocating or avoiding blame.

We of course, have become accustomed to adopting American pro-banking thought frameworks. The British seem to have adopted the Yankee drivel as a pragmatic reality, but have been more open eyed about its dangers.

There is a much larger issue here. London is the now the pre eminent centre of world banking, not New York. Is this because the legal framework and depth of understanding is more developed than elsewhere? It is plausible that this is why customers choose to transact through London, whether New York bankers, Russian Oligarchs or Saudi royals.

I came across a curious graph that compared Euro area GDP (falling) with Commonwealth GDP (rising steadily).

http://www.worldeconomics.com/papers/Commonwealth_Growth_Monitor_0e53b9…

Was Britain joining the EU in 1973 a world event, not just a local one? It was in many ways the final capitulation of the British Empire to the US, after the US destroyed the Empire trade preference system following WW2. It effectively made NZ and Aus into part of the US empire. We tend to focus on the military aspect of empires rather than the trade and banking that underpins it.

It is a curious line of thought.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.