By Roger J Kerr

Judging by recent statements and decisions it appears that the Reserve Bank of New Zealand (RBNZ) have not only abandoned monetary policy as a tool to keep inflation between the required 1% to 3% band, they have also in the process abandoned the export economy as the exchange rate is forced higher and higher.

By refusing to cut our interest rates to maintain a relativity to interest rates elsewhere (particularly Australia) the RBNZ have unwittingly and maybe naively forced the NZ dollar higher.

The rising currency value maintains tradable inflation (imported consumer goods) at low levels and possibly pushes it even lower.

The RBNZ’s mandate and remit is to maintain inflation between 1% and 3% without causing undue volatility in the economy, interest rates and the exchange rate.

Their current stance is causing annual inflation to remain below the 1% bottom limit for another 12 months on top of the 18 months they have already been in breach on their mandate with inflation below 1%.

The RBNZ’s refusal to cut the OCR over recent months has caused exchange rate volatility with the NZD/USD spiralling higher following each RBNZ statement. The Governor of the RBNZ Graeme Wheeler must be feeling the heat as two key mandate objectives are being constantly missed, mostly due to their own policy settings and messaging.

Over the last three months the RBNZ have seemingly given up on their previous monetary policy objective of requiring the exchange rate to be lower so that inflation increases to be back within the required target band.

In late 2015 the RBNZ was forecasting that house prices in Auckland would be levelling off in 2016 as their macro-prudential controls on bank mortgage lending made an impact to slow the residential property market.

They were wrong on that forecast with the housing market resurging in March/April. Since that time the objective of lifting the annual inflation rate through a lower exchange rate has been abandoned as RBNZ worries about the over-heated property market potentially causing risks to financial stability takes precedence.

When the RBNZ did not cut the OCR in late April and early June I called it a monetary policy mistake. It still looks like a monetary policy error to me as the overall Trade Weighted Index (TWI) exchange rate value soars to new highs following a speech by RBNZ Deputy Governor Grant Spencer last week wherein he signalled no urgency whatsoever to introduce further macro-prudential lending controls on the banks.

The FX markets are taking the view that the OCR will not be cut at the next RBNZ Monetary Policy Statement on 11 August as the RBNZ see no urgency to temper the housing market through further lending controls. Therefore they cannot cut interest rate at this time as that would fuel the housing market even more.

The market's reasoning that in the absence of immediate additional LVR controls a lower OCR cannot be contemplated. The TWI index today at 78.0 is now 11% above the 70/71 level the RBNZ have used for their current economic and inflation forecasts. Therefore on 11 August the RBNZ have to be substantially lowering their 2017 inflation forecasts.

Normally this would lead to OCR cuts in response, however the RBNZ are currently more concerned about the stability of our banks if the housing bubble was to burst badly.

It appears to me that the balance of risks and importance between monetary policy/inflation responsibilities and bank financial stability responsibilities has been tilted in favour of the latter with the poor exporter paying the price for that RBNZ policy bias. The banks need to look after themselves with prudent lending policies in an environment of inflated asset prices.

You just have to wonder how close the RBNZ are to things going on in the economy.

They completely ignored the Prime Minister’s threat last week to “get on with it” in respect to additional bank lending controls to take some heat out of the housing market.

To say that they are still doing their analysis and any changes could be six months away appears incomprehensibly at odds with the severity and urgency of the situation that the Government and others are highlighting.

Deputy Governor Spencer’s claim that the Government should look at its immigration policy as the cause of the housing problem also does not stand up to scrutiny as returning Kiwis are the bulk of the migration flows and Fletcher Building heads to the UK to recruit skilled immigrant workers to build the additional housing supply so desperately needed.

The NZ dollar exchange rate was pushed to fresh highs last Friday following the speech from the RBNZ Deputy Governor and an updated view from the ANZ bank that they do not expect the RBNZ to cut the OCR on 11 August.

The RBNZ claim that they have no influence on the value of the NZ dollar and they state that offshore economic and market forces determine all the movements. To disprove that assertion, we updated the TWI chart (see above in article) over the last 12 months that highlights the currency appreciation following RBNZ statements.

As exporter currency hedging runs out over coming months the RBNZ will need to lower their GDP growth forecasts as well as more industries in addition to the dairy sector pull back output, jobs and investment.

The interest rate market is now pricing just a 35% chance of a 0.25% OCR cut on 11 August.

To drive the currency back down this is the ideal situation for the RBNZ to surprise the market with a cut and threats of more cuts. The question has to be as to whether they are they sufficiently in touch to make such a decision?

Daily exchange rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

18 Comments

The productive sector, remember us? At least you are thinking of us Roger.

$55b of rural debt, most of which being serviced by below the cost of production income levels. Not much to worry about there then. Parity with $AUD which will be hurting our manufacturers and tourism now competing with a TWI at 78.

Not to worry as long as we can keep selling houses to each other (and all comers) at ever increasing, debt enabled, prices ,things should be just fine....until it isn't!

A productive sector is over-rated - just this afternoon i ate two (albeit rotten) weatherboards for lunch.

the mould gives it taste, like blue cheese

Sorry Roger. The RB can't do it alone without the government, and it's the government who are not carrying their end of the plank on this one.

More disingenuous commentary.

The Reserve Bank's mandate, as defined in the original legislation, is to achieve "price stability". Now to me the plain English definition of "stability" means something like "not moving". In fact the original definition of price stability was CPI inflation within a 0-+2% range - i.e a band that the RB is currently hitting perfectly.

The short answer is that inflation under 2% (or even under 1%) is not some hideous violation of the RB's purpose.

Price stability of housing is a d-.

I wonder how many RB officials received pay increases/performance bonuses last year?

Poor RBNZ, being set up.

Look at the global picture. Bond yields now inverted out to 5 years, lows in 10 year. NZD could go to parity against both the AUD and CAD this week if data is favourable . Every where you look something is not right, extremes in many areas, but unquestionably the banks and the overseeing Central banks are front and centre. The RBNZ could introduce mortgage to income restrictions to stop the housing market in its tracks, unfortunately it is not part of the current MOU nor ideology. Just lowering the currency does not always result in better trading conditions for our exporters particularly if every other trading bloc is trying to do the same .

Right now we stick out like a sore thumb - our currency is high because our OCR is positive and out of step with our major trading partners.

So if the OCR drops to zero, how far will the currency fall? With mortgage to income restrictions in place, this would pull a whole lot of investors out of the market.

OCR will not drop to zero , before NZ and Australia get there, questions will be asked by offshore lenders in regards to the of acquiring such funds and the purpose for which it is intended. The other side of the coin , could see a sharp decline in our currency value, inflation and a rather magnificent amount of debt attached to Auckland drywall as the RBNZ has another dilemma forced upon it.

By refusing to cut our interest rates to maintain a relativity to interest rates elsewhere (particularly Australia) the RBNZ have unwittingly and maybe naively forced the NZ dollar higher.

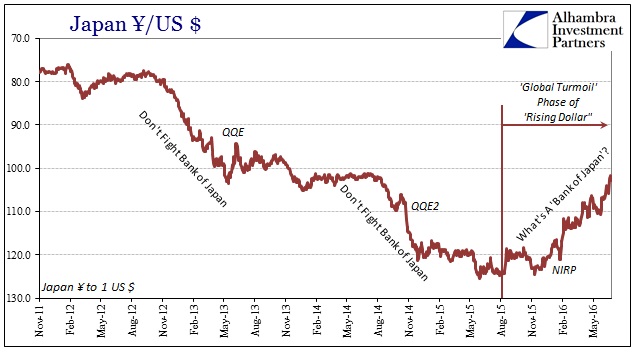

When did Japan not heed your advice? Never, and yet the yen continues to strengthen against both the USD and NZD View graphic evidence. Read more and more

{kind=link}

Mr Abe to order more stimulus tomorrow according to newswires

I agree with the theory re their ignoring their targets. I wondered at Bill English last week saying it was okay for the RBNZ to ignore the TWI, when actually the TWI is not officially a target at all. What I therefore assumed English was saying is that it is okay to miss the inflation target; he just didn't want to be so overt. Am not sure English declaring such a thing to be okay is actually good legal process; there should be a more formal declaration that the targets have moved and or the tools have changed. English though doesn't of course want to ever acknowledge the pretty clear error in not altering the targets or tools when he had the chance some years ago.

As it happens I would loosen monetary policy in other ways than lowering interest rates, as the world will eventually have to address the current paradigm where increasing debt is the only way to increase the money supply, when of course it is not. There are far more efficient ways to do so, to channel money to consumption and or infrastructure spending rather than asset price bubbles.

Key and English are no longer publicly on the same page. In fact no-one in National gives the impression of having any idea what page they are on about pretty much anything.

Well-placed sources inform me that the inner circle of the Nats is largely running on blackmail at this point. Merit has nothing to do with anything, it's all about knowing where the bodies are buried and who put them there.

don't most political parties run like that, when you see some certain people in our parliament still there after years cocking up you wonder who they have naked photos of

Roger, exporters have become just more victims of protectionism of the global ponzi housing market along with everything else. One day, things will get back to normal......after the whole thing tanks as expected.

the target used to be between 0-3 but was changed in 2002 to 1-3 maybe time it was changed back

http://www.rbnz.govt.nz/monetary-policy/policy-targets-agreements

Wow very well said Roger !

The RBNZ said the OCR may no longer influence the NZD, what a load of b.......

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.