Here's my Top 10 links from around the Internet at 2 pm today in association with NZ Mint.

As always, we welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must read is #6 on how low interest rates forever create zombies. Yum. Yum. Have a great weekend.

1. Speaking of housing bubbles - Canada's housing bubble may have started deflating.

One of the triggers looks to have been measures taken by the government to reduce high loan to value ratio (LVR) lending over the last year.

Sound familiar?

I'd be surprised if we saw any similar effects here yet.

There are plenty of hurdles to jump.

The Reserve Bank has to decide to limit high LVR lending. So far, it only has the tool and the Governor said as recently as December he wouldn't use the tool even if he had it.

Also, reading between the lines, I think the RBNZ is very reluctant to use the LVR limit.

And finally, buyers are adept at getting around rules like this.

The only real and effective way to spike a housing bubble is to put up interest rates. And, unfortunately for everyone, inflation is below the RBNZ's target band so it would struggle to justify such a hike given its current Act and policy targets agreement.

Here's CNBC with the news on Canada.

Home prices in the greater Vancouver area are down 3.9 percent from a year ago,according to the Real Estate Board of Greater Vancouver. In West Vancouver, which is sometimes said to be the wealthiest municipality in Canada, home prices have fallen 5.6 percent. Sales are down 20 percent from a year ago.

Vancouver is not alone. All over Canada there is fear that the country is in a housing bubble that is now in the process of popping. In March, Montreal saw sales decline 17 percent year over year, even while inventory continues to climb. In Ottawa, sales have fallen 16 percent.

"A housing correction—or, possibly, a crash—is no longer coming. It's here, "Macleans magazine declared this past January.

------------------------------------------------------------------------------------------------------------------------------------------

Keep it safe. Keep it in a New Zealand Mint safety deposit box. Details here »

------------------------------------------------------------------------------------------------------------------------------------------

2. How to avoid the rules - CNBC explains how Canadians are avoiding the tough rules imposed by the government on high LVR lending.

The Canadian government is attempting to engineer a soft landing. It has tightened mortgage lending rules four times in the last four years. The maximum length of mortgages is being reduced from 40 to 25 years. Home equity loans were curtailed. And the government stopped backing mortgages on the most expensive homes.

But it's not clear how effective these measures will be. The Globe and Mail recently ran a feature titled "Canadians can still buy a house without saving their pennies." It is more or less a guide to buying a house with no money down. The website eHow has a page for doing that.

Some of the loopholes people use to avoid the mortgage restrictions are quite extraordinary. For example, although the government requires buyers to purchase private mortgage insurance on mortgages with 100 percent loan-to-value ratios, eHow says this can be avoided just by getting two mortgages, each for 50 percent of the home value.

------------------------------------------------------------------------------------------------------------------------------------------

New Zealand Mint. Experts in gold & silver bullion, commemorative coins and jewellery. Details here »

------------------------------------------------------------------------------------------------------------------------------------------

3. China's relucantance to stimulate - Bloomberg reports China's new leadership are reluctant to juice its stretched economy with yet more investment.

Chinese Premier Li Keqiang signaled policy makers are reluctant to use stimulus to counter a slowdown in the world’s second-largest economy because the risks outweigh the benefits.

“To achieve this year’s targets, the room to rely on stimulus policies or government direct investment is not big -- we must rely on market mechanisms,” Li said in a May 13 speech broadcast to officials around the country, according to a transcript published last night on the central government’s website. Relying on government-led investment for growth “is not only difficult to sustain but also creates new problems and risks,” he said.

------------------------------------------------------------------------------------------------------------------------------------------

Available now. Our brand new 1 oz Taku gold bullion coin. Details here »

------------------------------------------------------------------------------------------------------------------------------------------

4. Is Spain insolvent? - Jeremy Warner in The Telegraph reckons so. This has not made him popular in Spain

A massive housing over-supply is a major part of the problem. If only we could import those houses in containers to New Zealand.

The elemental problem for Spain is that if does manage to pull off an "internal devaluation" by cutting wages back to parity, it will make its debt burden worse. It is damned if it does, and damned if it doesn't.

The country is already in deflation. Prices fell 0.6pc last month, stripping out the one-off effects of higher VAT and levies. Officials appear delighted by victory over inflation but they should be careful what they wish for. The "denominator effect" is going to bite even deeper.

The level of pain still to come depends on the housing market, the great disaster that has infected everything. Prices are down 33pc from the peak so far, or 45pc in real terms. The government's stress test for the banks is premised on a real fall of 50pc. If that proves correct, Spain is nearly there.

If the dissenters are right, Spain is nowhere near bottom. Madrid consultants RR de Acuna have a report coming out this month warning that the glut of unsold properties has risen to a fresh peak of 2.25m homes, including those in the hands of builders and banks, or in the eviction process.

"It will take 10 years to get rid of the stock. We're pretty sure that prices will bleed another 15pc," said Fernando Rodriguez de Acuna. "The market is broken, and the quoted prices in many areas are a fiction. You can't sell even if you offer a 50pc haircut. A lot of buildings will have to be knocked down and land is going to revert to farmland, or just to nothing."

6. Attack of the 0% powered zombies - WSJ reports how the Bank of Canada is now warning that low interest rates for an awful long time leave zombie banks and companies alive and feeding off the living for way too long.

Quantitative easing–or bond buying measures by central banks in major countries, including the U.S., U.K. and Japan–has led to an extended period of low rates across the yield curve. That means cheap borrowing costs, which is great for any company that’s growing and creating jobs and contributing to the economy.

But the low rates can also have scary consequences: propping up firms that would have gone bust under ordinary circumstances.

“Low for long (rates) may lead to forbearance” as cheap loans are extended to firms that are not viable, Bank of Canada analysts Eric Santor and Lena Suchanek said in a report examining the costs of unconventional monetary policies.

This also applies to lenders who are being kept afloat by low rates, since banks also need to borrow from each other.

“These zombie firms/banks would impede the needed restructuring of the economy,” according to the analysts. In other words, these firms prevent resources going where they would be much more useful, such as the creation of new and more viable firms. In that sense, the zombies are limiting competition.

7. The Bitcoin universe's new backer - Peter Thiel, the co-founder of PayPal and a very early big investor in Facebook, is well known in these parts as a shareholder in Xero and a backer of the now-defunct Pacific Fibre cable project.

Now it seems he's dipping his toes in the Bitcoin world. Liberty Blitzkreig (!) reports on how the renowned libertarian is investing in Bitpay, which aims to make Bitcoin accessible for corporates.

Here's what I consider the most amazing thing about this pretty amazing graph. It's not just that the U.S. had the shallowest recession, or the best recovery, among similar countries in Europe and Japan. It's this. We had the shallowest recession and the best recovery primarily because we (a) control our own currency and (b) used aggressive monetary policy to save the banks and lower interest rates while running high deficits.

And yet! Even as we smoked Europe and Japan in the race back to pre-recession GDP, we have actively debated undoing both of the things that clearly made our recovery superior. Weird conservatives have begged us to return to the gold standard at the very moment that an inflexible currency was dooming Europe. Normal conservatives have begged us to cut deficits even as austerity was dooming Europe.

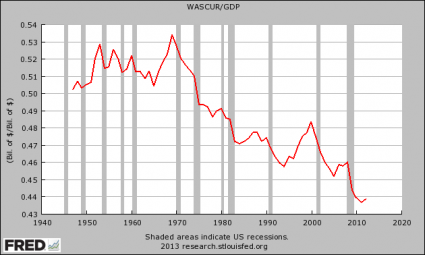

9. Some cracking charts showing the decline of the American middle class as the powerhouse behind America's consumer economy - Here's Michael Snyder with the compilation and a sample showing the wages share of US GDP since 1945.

In the old days, when the big corporations that dominate our society did well, that also meant good things for American workers since those corporations would need more of us to work for them. But in the emerging one world economic system that our economy is being merged into, those corporations have other choices now. For instance, the big corporations can now choose to limit the number of "expensive" American workers that they employ by shipping millions of jobs to the other side of the world.

And from their perspective, it makes perfect sense. They can make much bigger profits by hiring people on the other side of the planet to work for them for less than a dollar an hour. If they can get good production out of those people, then why should they hire Americans for ten to twenty times as much, plus have to give those Americans health insurance and other benefits? Another major factor in the slow, agonizing death of the American worker is technology. We live during a period when technology is advancing at a pace that is almost unimaginable at the same time that it is steadily becoming cheaper and cheaper.

That means that it is going to become easier and easier for companies to replace workers with robots and computers. As I have written about previously, it is being projected that our economy will lose millions of jobs to technology in the coming years. Yes, some of us will still be needed to help build the robots and the computers, but not all of us will. And of course the overall general weakness of the economy is not helping matters either. The American people inherited the greatest economic machine in the history of the world, and we have wrecked it.

10. Totally Clarke and Dawe with a big week in publishing.

29 Comments

No-one much seems to be paying attention but the Kiwi has fallen significantly against the US$, Stirling and the Euro in the past week - ever since the Aussies cut their interest rates in fact (and the markets woke up to the situation the Aussies face). The Kiwi has maintained strength only against the Aussie $.

I reckon as the Aussie $ continues to be re-rated downwards (off the back of a sickening home economy and the China slowdown) the Kiwi will follow it. In turn the RBNZ will no longer be able to rely on a high Kiwi $ suppressing inflation. Its hard to understand why interest rates are still set at emergency lows (at hyper stimulatory levels) with an economy that is expanding at 2.5% plus, with a housing bubble and falling unemployment thrown in - its going to get a lot harder to understand within the next few months.

RBNZ announcing their intervention started ball rolling and it hasn't recovered since

Hmm, I daresay the RBNZ would love to say their proclaimed intervention played a part, but if that were true why isnt the Kiwi also falling against the Aussie (its actually strengthened a little)? This is all about a sickening Aussie $ I am thinking.

If it continues it will provide the RBNZ with a very useful window to get interest rates back up to a neutral setting. Are they clever enough to recognise it?

Didnt BE or JK convince the financial wizkids over in the US that NZ was just like OZ and no worries then? Those same lines could be coming back to haunt us/them.

Im not so sure on inflation being no longer supressed, this is because NZers wages wont / have not changes, so if the TV goes from $2k to $2.2k and isnt sold....oh dear. Interesting to watch.

regards

OOOh I'm paying attention alright andyH, just not letting myself get " carried" away is all.

A short but ripperlishly good piece on the trap the UK finds itself in:

http://www.investmentandbusinessnews.co.uk/economic-news/uk-wages-fall-…

#9

Take care quoting Michael Snyder, he's a conspiracy theorist of the first order, a 'prepper', and some would say a fundamentalist nutter.

However, just because you're paranoid doesn't mean the bastards aren't out to get you. He often talks a lot of sense and explains stuff to we economically challenged like how the banksters create money out of nothing, who owns the Fed and so on.

It's Friday ....Yay...the old story don't shoot the messenger is not without it's contradictions.

One Monday morning the Postman is riding his bike on his usual route, delivering the post. As he approaches one of the homes he noticed that both cars were still in the driveway. Next thing, Derek, the homeowner, comes out with a load of empty beer and wine bottles for the recycling bin. "Wow Derek, looks like you had one hell of a party last night," the Postman comments. Derek, in obvious pain, replies "Actually we had it Saturday night. This is the first time I have felt like moving since 4:00am Sunday morning. We had about fifteen couples from around the neighbourhood over for some fun and games and it got a bit wild. We all got so drunk around midnight that we started playing WHO AM I." The Postman thinks a moment and says, "How do you play WHO AM I?" "Well, all the blokes go in the bedroom and we come out one at a time with a sheet covering us, with only our 'family jewels' showing through a hole in the sheet, then the women try to guess who it is." The Postman laughs and says, "Sounds like fun. I'm sorry I missed that." "Probably a good thing you did," Derek responded. "Your name came up seven times..."

#1 Which is the expected result as per Steve Keen.

regards

The only real and effective way to spike a housing bubble is to put up interest rates.

Bernard must be suffering from short term memory loss. Seems to have forgotten how ineffective this policy is. OCR recent high 2006-2008.

http://www.rbnz.govt.nz/keygraphs/Fig7.html

House price, doesn't miss a beat.

http://www.rbnz.govt.nz/keygraphs/Fig4.html

The only thing which had a significant effect was the US lead recession, and has little to do with the OCR. The other problem being the OCR is hardly at the discretion of the RBNZ, if it strays too far from the 90-day rate they will quickly have a problem with clearing the checks. Never a good look when the central bank causes financial panic, I don't think they are planning it.

The collapse wasn't the RBNZ's doing though, that was the effect of the imported GFC. The bad lending decisions these guys made were mostly prior to the bubble bursting.

NBDT institutions don't get RBNZ credit directly either, so they can't borrow at the OCR. They have to borrow of a commercial bank if they need credit.

Nic the NZer - could you explain your comment about " RBNZ, if it strays too far from the 90-day rate they will quickly have a problem with clearing the checks" to clarify for me

Yeah, the OCR market is for interbank settlement. The market dictates terms to the reserve bank, not the other way around and the RBNZ really wants the market to clear so that the banks can pay each other.

Nic,

I am not sure what you mean by the market dictating terms.

The Market can demand higher rates because of risk, but if the economy is weak the RBNZ can even so, provide sufficient money to ensure all demands for money are satisfied. Ie the people who demand higher rates are no longer required and all borrowing can be met via money flowing from the RBNZ. The people who have money they wish to lend at higher rates, then either have to lend it at current rates or hold another asset.

LOL, that is such a poor attempt at re-hashing history I cant only imagine you are mortally feared that interest rates will rise. Bit over-exposed on the debt front are we? (well we know kimy is, guess we can add another one to the list).

Kimy - you are just making yourself look foolish now. Even Nic the NZ (see post above) has appreciated that it was not the RBNZ's actions that did the Finance companies in. Has it not occured to you why various Finance company directors were prosecuted and in some cases jailed - in Kimyland do they send you to jail because your company was the victim of rising interest rates?

Kimy, the question you never seems to ask yourself, well at least not on here, is what would have happened if the RBNZ hadn't increased interest rates then, and on other similar occassions....in the 2003/2008 period they let inflation get up over 5%, even although they did increase rates (too slowly). But I guess if youre heavily focused upon housing/property inflation, bugger the rest who get damaged by 6-10% inflation, or worse as we've seen in the past before inflation targeting by cemtral banks.

Understand how it works, when inflation starts to look like a problem (hopefully beforehand) central bank raise rates, and historically they have had to do so until something breaks (the lesser of two evils argument) - so I for one would not sit there like you and MortgageBelt do trying to point out the obvious about what would happen when indeed everyone knows that is the process, indeed its almost designed to happen that way - you just make sure you know it, rather than being a denier, and protect against it. Inflation isn't an issue yet, and probably won't present itself for some time, but again, when the markets detect it, low fixed rates will be gone probably within days.

And I agree totally with you on complusory superannuation Kimy. But whilst I wouldn't rule that out in the future, indeed I expect it, it isnt going to happen any time during this particular interest rate cycle bottom. Whilst the RBNZ will use some macro prudential tools sometime next year as well, they will use interest rates as well and have repeatedly emphasised that fact. So whilst we can all debate to death what should happen, I'm just focusing on what will most likely happen, and protect accordingly. My concern is for those that might listen to the superfical observations that the likes of MortgageBelt makes, and get badly caught out in doing so.

Kimy - the RBNZ is in the process of ensuring that the banks sure up their capital even further and with good reason - all other things being equal they will raise rates next year as they will feel it is the lesser of two evils. Of course other events could conspire to change that, but they will likely be offshore ones if any, but I'm sure they will attempt to do so in a controlled manner to minimise the damage if they have that latitude. However, if someone is floating on 5%,and can't handle 6-7% over the next 3 or so years, they really weren't being realistic when they purchased as to whether they could afford the property.

Increasing interest rates will have little effect on house prices, as many other drivers boost housing. 9% of sales are due to international buyers, with very little borrowing.

Interest rates will be falling further in NZ, rates are still relatively high.

The US did not enter recession (2 consecutive quarters of contraction) until the last quarter of 2008. NZ house prices (QV data) topped out in Nov/Dec/Jan 2008 (ie 10 months EARLIER) with a QV value in the 1570s and then started to fall from then onwards under the influence of the last round of RBNZ rate rises in late 2007. By the time the US recession had begun the QV values were down to around the 1470s . QV values cratered out at around the 1420s in the first quarter of 2009 (a fall estimated at between 10-15%). In fact the US recession SAVED the NZ housing market as it caused the RBNZ to slash interest rates and prevent further falls from then on. Interest rates were slashed from August 08 onwards reaching a low at around the same time as the housing market reached its bottom.

http://www.interest.co.nz/charts/real-estate/qv-house-price-index

That is what actually happened.

People also forget that one of the reasons that the interest rate transmission mechanism was so deferred was the prevalence of borrowers using 2-3 year fixed terms - these offerered people protection from rising interest rates in the period 2004-2007. By 2007 many of these deals had lapsed laying borrowers open to the new higher rates which in turn toppled the housing market.

Probably the time-line of the St Louis FED is accurate. That starts to have rumblings in late 2007.

http://timeline.stlouisfed.org/index.cfm?p=timeline#

Of course if your definition of recession is two quarters of contraction, then you can't have an official recession for at least six months after events started. That doesn't mean that business wasn't collapsing for the preceeding 6 months or more, in fact it means precisely that it was collapsing for the preceeding 6 months, or more.

Also when I said two quarters or more. The US economy didn't start from zero growth and have a recession, it started from positive growth and later went negative for two quarters. I mean plainly you have the timing wrong, because you are waiting for the announcement to start the clock. By definition the announcement of a recession in the US is two quarters lagged, and probably the market has been different for the preceeding 6 to 9 or even 12 months.

It is not MY definition of what recession is, it is what the STANDARD definition of recession is I am afraid:

http://www.investorwords.com/4086/recession.html

As can be seen here in fact the US economy did reasonably well in the first 2 quarters of 2008, with a solid 2.5% growth recorded in Q2 of 2008:

http://recessionmapsandgraphs.com/GDP.htm

It then turned over in the last 2 quarters, with Q4 representing the 'official' start of a defined recession.

So lets be clear. In Q2 when the US economy was growing by 2.5% plus in the quarter:

http://recessionmapsandgraphs.com/GDP.htm

the NZ housing market was already on its way down:

http://www.interest.co.nz/charts/real-estate/qv-house-price-index

That's fine, but obviously doesn't mean the recession started at the end of Q4 2008. So who is rewriting history?

You need more evidence, look at the Fed time line I posted.

http://timeline.stlouisfed.org/index.cfm?p=timeline#

June 1, 2007

Standard and Poor's and Moody's Investigator Services downgrade over 100 bonds backed by second-lien subprime mortgages.

Seems the crisis started in 2007, well before Q4 2008.

June 7, 2007

Bear Stearns informs investors that it is suspending redemptions from its High-Grade Structured Credit Strategies Enganced Leverage Fund.

That would be the Bear Stearns that collapsed later on in the crisis, BTW...

Feb 13, 2008.

President Bush signs the Economic Stimulus Act of 2008 (Public Law 110-185) into law.

I wonder why he did that?

Feb 17, 2008.

Northern Rock is taken into state ownership by the Treasury of the United Kingdom.

Thats a pretty clear indication that crisis had spread to the UK by Feb 2008 if ever I saw one.

You are only out by a little over a year.

Global connectedness & forces will determine our interest rates & relative debt position. & currency level.

Also the increasing number of borrowers & 1st home buyers places a weight on the banks to keep those borrowers solvent.

There is only one direction for a world & NZ entrenched in deflation & consumers conservative behaviour and thats decreasing interest rates.....

#7

Bernard, mine your own Bitcoins

http://www.wired.com/wiredenterprise/tag/bitcoins/

So in just two weeks, those lucky enough to have snagged one of these rigs will have paid off the initial investment. Everything after that is gravy.

For most of Butterfly’s customers, though the trick is getting your hands on one of these rigs. They’ve were supposed to ship last fall, but have been plagued by production delays. Butterfly started shipping its first systems a few weeks ago, but there are thousands of customers who are still waiting for miners. Meanwhile, with more and more computers joining the network, mining difficulty is quickly getting harder. So the amount of money these machines can make per day is slowly declining.

This will get the pinky greens going!

The United Nations has published its first plan for managing the extraction of so-called "nodules" - small mineral-rich rocks - from the seabed

http://www.bbc.co.uk/news/science-environment-22546875

We have heaps of noodles...errr....make that nodules...billions of tons of them...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.