By Stephen Toplis*

We believe consistency will win out in the short term but political efficacy may yet win the day over the longer term.

In other words: no cut in March but a substantially increased chance of a reduction in rates as the year wears on.

Key to the consistency message, on February 3, in his speech to the Canterbury Employers Chamber of Commerce, Governor Wheeler said that “the Bank would avoid taking a mechanistic approach to interpreting the PTA. Some commentators see a low headline inflation number and immediately advocate interest rate cuts.” He went on to comment that this was an inappropriate response.

The question, is will the RBNZ stick to this message in its next Monetary Policy Statement? Or, has it found a reason to cut rates over and above the headline inflation figure.

There is no doubt that, was the RBNZ to mechanistically follow the headline inflation rate, that it would be cutting now. The December quarter CPI significantly surprised the Bank to the downside and it is almost certain that the March quarter CPI will be even further below that expected by the RBNZ when it put its December MPS together. At that stage the Bank was looking for a March quarter increase of 0.6%. We reckon it will be zero. The annual reading will thus be a mere 0.3% compared to the Bank’s last published estimate of 1.2%. This is a big miss and, given base effects, should keep annual CPI inflation below 1.0% right through 2016.

The second round impacts of this are important as published headline inflation also affects inflation expectations. By December 2016 annual headline inflation will have been below 1.0% for nine consecutive quarters. It’s almost certain, then, that inflation expectations will fall to similar levels. The RBNZ has said that if this happens then it will probably ease. The exact words used by the Governor are: “we would not wish to see inflation expectations become unstable and decline significantly”. One could argue that the drop in the Reserve Bank’s two year inflation expectations series to 1.63% (the lowest since June 1994) and the slump in the ANZ Bank inflation series to 1.39% (its lowest ever) is evidence that this process is already under way. Of course, given that it’s a near certainty that expectations will fall further, does this then mean that the RBNZ has already backed itself into a corner? Quite possibly.

With this in mind, if prudential and monetary policy were dictated by separate regulators, as is the case in many parts of the world, a near term cut would be a certainty. But, in New Zealand, this is not the case. The RBNZ notes that “a mechanistic approach can lead to an inappropriate fixation on headline inflation. It would cut across the flexibility deliberately built into the PTA framework, and risk creating serious distortions in the financial system, housing market, and broader economy”. This is the RBNZ weighing up prudential concerns versus monetary policy objectives and highlighting the trade-offs that may be required.

In this regard, the RBNZ will be very mindful that credit growth continues to accelerate. The most significant immediate worry will be the debt held in the rural sector (read: dairy). Of growing concern, though, will be the acceleration in mortgage lending that is again resulting in an increase in New Zealand households’ debt to income ratios. This worry is, of course, exacerbated by the ongoing strength in the New Zealand housing market. Sure, Auckland seems to be stabilising but stabilising at grossly overvalued levels. But the remainder of New Zealand is now picking up a head of steam that is probably considered unwelcome. Lowering interest rates would thus be unhelpful in maintaining financial stability.

Whatever the case, we think the RBNZ will want to see more data on this front before swinging into action. The same can be said about inflation. While it is certain headline inflation will remain muted in Q1 what will be of more interest to the Bank is what is happening to “core” inflation. Latest figures show core is about where the RBNZ wants it. Moreover, it is on a rising trend. Surely, the last thing it would want is to cut in March only to find out that core headline inflation rose again.

There are a multitude of other arguments to consider including:

- The strength or otherwise of the New Zealand economy;

- The level of the TWI; and

- The impact of developments offshore.

These factors again pose more questions than answers.

It looks to us that the economy is doing particularly well and set to stay that way driven by immigration, strong employment growth, stimulatory interest rate settings, rising real wages, soaring services exports and ongoing construction activity. Why on earth would you want to lower interest rates in that environment?

Yet the dairy sector looks exceptionally miserable and, potentially, for much longer yet. Surely, the spillover effects of this must impede the economy significantly in due course?

For the time being, though, Q3 GDP surprised the RBNZ to the top side and Q4 GDP may well do the same. Moreover, the unemployment rate at 5.3% was well below the RBNZ’s expectations suggesting a much tighter labour market than anticipated and less spare capacity. It’s a moot point that this apparent labour market tightness will be sustained but it’s probably a tad early to rule it out either.

The level of the TWI is definitely problematic for the Bank. At 72.57 it’s 6.9% above the level that the RBNZ has built into its forecasts for the June quarter. All other things being equal, this must take at least 0.7% off the Reserve Bank’s 18 month CPI inflation forecasts as at the December MPS. Moreover, the market is already pricing in an easing so if the RBNZ doesn’t meet market expectations the currency would likely push higher still. This may well be the straw that breaks the camel’s back for the Bank. That said the TWI is not much different to what it was when the Governor made his February “no-change” speech.

Offshore developments remain critical. While the degree of uncertainty remains huge, financial market conditions and volatility appear no worse than they did when the RBNZ produced its December Monetary Policy Statement. The risks are still there but there is no need to respond to them at this stage.

One of the biggest concerns is the will they won’t they question mark over the US Fed. A tightening labour market in the US coupled with rising core inflation says the Fed should tighten. But forward indicators of activity are softening so the market says no way. If the Fed does tighten and the US economy does gain momentum then this will result in a lower NZD and stronger export opportunities, both of which would argue for no rate cut in NZ. If not, then rate cuts again become live.

The other global financial market development that is occurring is rising credit spreads and increased pressure on New Zealand bank funding costs. This could result in increased borrowing rates which many suggest would need to be offset by a lower cash rate.

That too is a possibility but, given financial stability concerns, will the RBNZ be bothered or pleased by increases in domestic borrowing rates? And even if the cash rate was cut in this environment would banks pass on the cost reduction or use it to rebuild margins?

Does all this sound very confusing? It sure is to us! Unfortunately, we are obligated to have a rate track view no matter our conviction. Bear in mind, though, that any such view also has to be set alongside market pricing when determining likely market responses. Accordingly, it is important to note that market pricing currently has about a 25% chance of a cut in March, a full cut in the OCR by June and a low of 2.10% in the strip by November.

For now then, we do not think the RBNZ will go in March. It simply has insufficient information and risks looking silly in the event that measured inflation begins to turn up.However, the Bank will not want to disavow the market of the easing priced in for fear that the NZD might bounce.

So it will attempt to hold market pricing broadly where it is by maintaining an easing bias. In fact the easing bias is likely to be even stronger than in its previous statements. It may even be tempted to build a lower interest rate track directly into its forward guidance, were this the case, it though would beg the question why it didn’t simply cut now.

We do not have a formal easing built into our forecasts either. This is not because we think market pricing is ridiculous but, simply, because we don’t want to end up flip-flopping with our calls. In particular, we are conscious that there is a swathe of data to be released over the next few weeks which could have us shifting our views this way and that. Whatever the truth of the matter, it’s also worth noting that current market pricing doesn’t offer fixed interest rate investors a significant risk/reward opportunity at this juncture even if the RBNZ does go into rate cut mode. All that said, the balance of risk is very clear and we are poised to move our own rate track lower given the right catalyst.

Be that as it may, the overarching question remains: will a rate cut (or no rate cut for that matter) have a meaningful impact on the CPI inflation outcome in the foreseeable future. Frankly, we doubt it.

Stephen Toplis is Head of Research at BNZ.

10 Comments

if the inflation number is low then rates should be cut. The banks didn't mind raising rates when inflation was higher, to say 6 7 8% and the banks did not give a jot when house prices fell...

The other global financial market development that is occurring is rising credit spreads and increased pressure on New Zealand bank funding costs. This could result in increased borrowing rates which many suggest would need to be offset by a lower cash rate.

For what purpose other than to undermine the risk protection higher rates afford unsecured creditors - namely bank depositors? Foreign wholesale interest rate costs have apparently risen by a third over the last twelve months - why shouldn't depositors returns reflect the same?

They're having a hard time in the banking sector and they're almost broke. Filling a swimming pool with $100 notes has reduced their capital reserves.

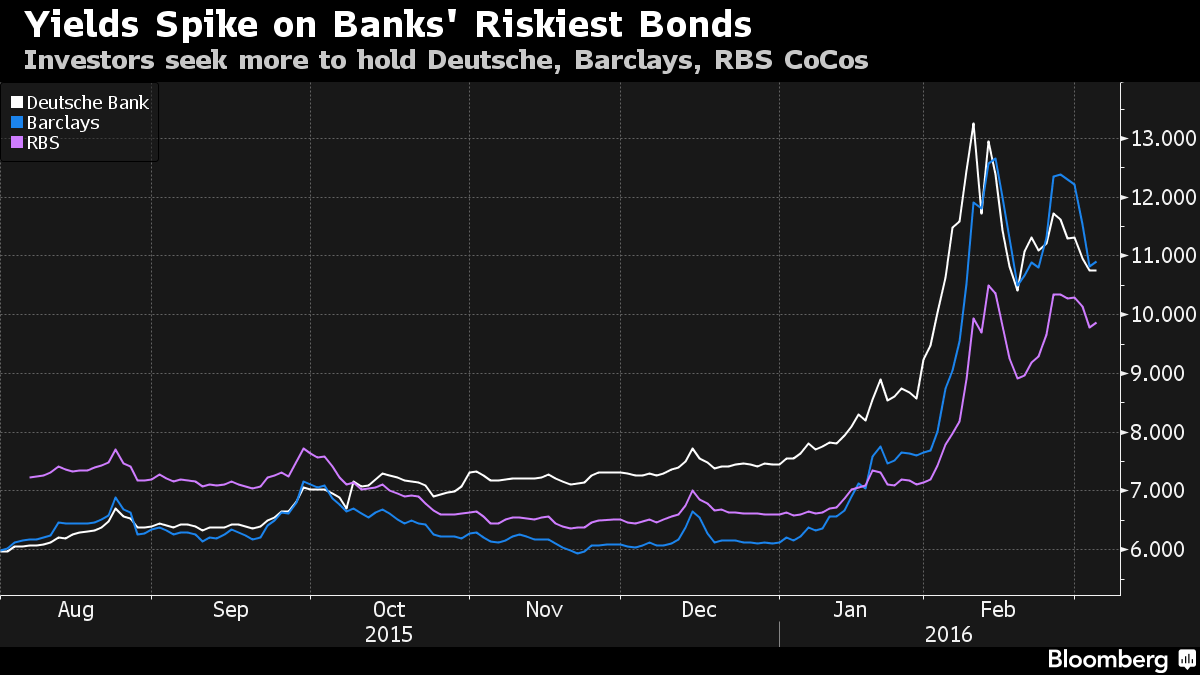

Certainly the largest banks in Europe are doing it hard in the CoCo debt market, which in function is similar to the NZ hybrid market. View graphic

{kind=link}

It seems New Zealand investors take a more cavalier attitude when it comes to pricing domestic risk in respect of their capital investment exposures.

The Office of the Comptroller of the Currency, which tracks the exposure of U.S. banks to derivatives, released this terrifying chart for Q3 2015:

The top four banks – JPMorgan Chase & Co. (NYSE: JPM), Citibank National, Goldman Sachs Group Inc. (NYSE: GS), and Bank of America Corp. (NYSE: BAC) – have a combined derivatives exposure of $174 trillion, about 35 times larger than their combined assets and hundreds of times larger than their capital bases.

http://wallstreetexaminer.com/2016/03/heres-makes-derivatives-monster-d…

http://cdn.moneymorning.com/wp-content/blogs.dir/1/files/2016/03/us-ban…

{kind=link}

"One of the dirty little secrets about credit default swaps is that they create in the buyer of protection (the insured) a strong economic incentive to see the borrower fail" Interesting article Andrew. It's a bit of a worry that our country is being lead by a derivatives trader. Our leaders can potentially make money from deliberately bowling a no ball?

There's no doubt about that. I wonder how many people realised what risks they faced when Kiwibank issued more hybrids. The high return may have overridden rational thinking.

From what I've read the CoCo market has suffered a large drop in demand recently, and it's not surprising.

SH:- Why don't depositors returns reflect the same risk?

Damn good question

The whole banking system is so opaque the man in the street wouldn't have a clue what's what - including me

But, then, to answer your question, from a person who is not-in-the-know, depositors returns are dictated by the RBNZ periodic announcements. Depositors get the OCR minus a handling fee. And they are none the wiser.

Were it not for you I'm sure a lot of people here wouldn't understand these fine details of banking

Obviously the RBNZ is not looking out for you or me - more important things to consider

Obviously the RBNZ is not looking out for you or me - more important things to consider

Such things as lunch, presumably.

oh come on as if banks care about savers, this is a monetary system reliant on perpetual credit...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.