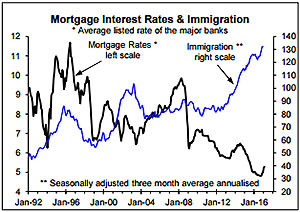

NZ is doomed to experiencing major housing cycles in part because of the link between interest rates and migration and the tendency for the Reserve Bank to conduct misguided monetary policy experiments (i.e. cut interest rates excessively when there is already an upturn in immigration/net migration boosting the economy and housing market).

This Raving focuses on the link between interest rates and immigration.

The housing market is in the latter stages of benefiting from the combination of low interest rates and high immigration/net migration, with the resulting housing boom fuelled further by increased activity by investors albeit that this has been temporarily set back by the latest lending restrictions.

It is inevitable that the latest boom like all past booms will be followed by a major downturn in the housing market, including for residential building.

This is in part because in time interest rates will need to be increased to the extent it generates a hard landing for the economy, meaning much lower employment growth and reduced demand for immigrant workers. From currently still being positive factors for the housing market, the two main cyclical drivers will end up turning against it and in turn drive reduced activity by investors.

Why does NZ experience such major housing cycles?

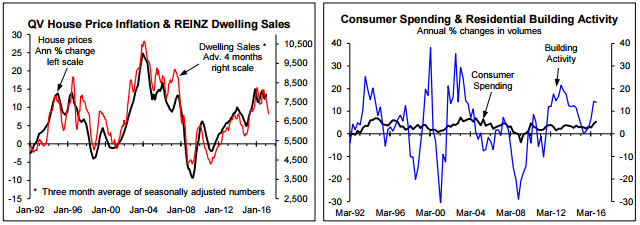

As is the case in many countries, it is normal for NZ to experience major housing cycles roughly once a decade. This is shown in the left chart for the number of existing dwelling sales and house price inflation and in the right chart for annual growth in residential building activity that is dramatically more cyclical than annual growth in consumer spending. The massive cycles create a nightmare for people managing firms impacted by the housing and residential building cycles.

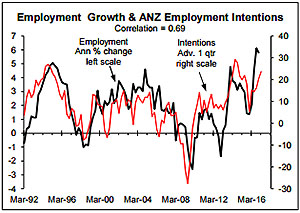

The result of cutting the OCR excessively at the time of a major upturn in immigration/net migration is overly strong GDP and employment growth which is visible in the case of employment growth in the adjacent chart in the mid-1990s, mid-2000s and again recently. The strong employment growth then plays a part in boosting immigration.

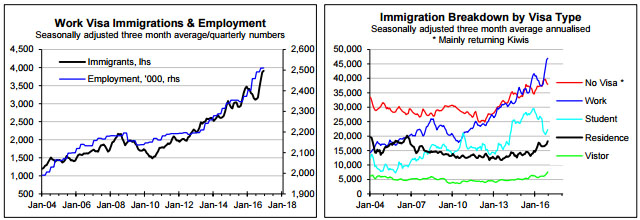

The left chart below shows a quite close link between employment numbers and the numbers of immigrants arriving with work visas. The right chart shows the growing percentage of total immigrants made up by immigrants arriving with work visas. A strong local labour market also plays a part in encouraging more Kiwis to return from OE as measured by no visa immigrants shown right chart below (red line) although what is happening in the Australian labour market is a more significant driver of the number of Kiwis returning from OE and the number of Kiwis emigrating from New Zealand.

There are a number of important dynamics that drive migration cycles as covered in our monthly housing and residential building reports including developments in the Australian labour market. But one of the reasons why housing cycles are so extreme is a link between interest rates and immigration/net migration cycles. When the Reserve Bank makes the mistake of overly stimulating the economy with OCR cuts at the time there is already an upturn in immigration/net migration it adds to the upturn in immigration.

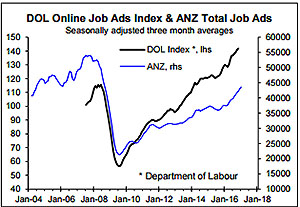

Job ads have surged significantly in the last year which means more employers will be looking to attract staff from overseas which will be the main factor behind the upturn in immigrants arriving with work visas although this may partly reflect random variation or people getting in ahead of recent tightening in immigration criteria by the government (blue line top right chart). Critically, major upturns in immigration fuel demand in the economy and labour market more than they boost the supply of labour especially when they are combined with falling interest rates. This is contrary to what seems to be a reasonably widely held view that immigration boosts labour supply more than it boosts labour demand. Immigrants need to restock a wide range of durable goods which is why they add more to demand than supply in the economy especially in their first year in the country.

NZ is currently in the latter stages of the latest major housing upturn driven by the combination of low interest rates and high immigration/net migration; with these in turn driving increased activity by investors albeit for the moment that has been at least temporarily set back by the latest lending restrictions. However, just as the combination of interest rate cuts and high immigration/net migration have driven the latest housing boom it is inevitable that the latest misguided monetary policy experiment ultimately results in the need for a hard landing that will mean much slower employment growth and reduced demand for immigrant workers by employers; and that this results in reduced activity by investors. It is inevitable that there will be another major housing downturn and via our existing housing market and residential building reports we will probably again be the only forecasters that provide a timely advance warning.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

32 Comments

If demand from immigrants has exceeded their contribution to the labour market, why have we not seen a significant increase in wages?

Had the RBNZ held off interest rate cuts surely we would have been dealing with deflation and an expensive currency.

Lowering the OCR led to more external borrowing in foreign currency (mostly US$) and the sale of those borrowings to convert them into purchases of NZ$ = a higher NZ$ than one could have expected from natural trade transactions. Arguably, if the OCR had been raised (deterring domestic borrowing) the currency could have falenl and inflation via higher import prices would have been the result. So cutting interest rates has been deflationary in all but two asset classes - stocks and property, both of which can reverse their 'wealth effect' at the drop of a hat.

Bw, why would raising the OCR lower the currency . In general terms raising the OCR or suggesting that it will be raised , usually leads to a stronger currency, lower import prices, lower inflation. There should be no shame in having a 'strong' currency ', repeatedly talking down a currency as the RBNZ , among others has repeatedly done , suggests that the currency is not the problem , but the underlying makeup of the economy. Without the appreciating currency or the interest rate differential , our banks would not have the deposits sitting in them ,that they currently do.

Luckily for Ted and the property ra-ra cheerleading brigade that the Gummster isn't head of the Reverse Bank , 'cos I'd have quickly hiked the OCR to 5 % ... and left it there ...

... until the government wakes up to the need to target immigration more accurately , to the IT and medical people we need , rather than cleaners , kitchenhands , and grape pickers ...

... and until the government wakes up to the need to fully stop foreign money from flooding into the country , pricing NZ citizens out of home ownership ...

.... and until the government get off their chuffs and start spending some seriously big sums on the infrastructure we require before house and apartment developments can be constructed ...

Until then : the OCR is 5 % !

I couldn't agree more Gummy Bear. I'm certainly no expert in this, but my understanding is that we drop the OCR to stimulate the economy, but in essence businesses (that create jobs, income, growth etc) end up paying higher lending rates to fund their activities than property owners do. So by lowering the OCR all we've done is encourage speculative and risky activity on residential housing because people can more easily get leveraged, while having marginal benefit to business and growth? Is this all smoke and mirrors or am I confusing the situation?

If we raised the OCR years ago, not lowered it, it would have forced us to clearly see whats sustainable and whats not - and removed risk, not added to it. Savers would now have more cash to spend because of increased interest rates, hopefully into business and growth - instead of being so indebted in housing because of the carrot that was being waved in that direction (through low interest rates). I get the feeling we've done this all back to front.

Definitely no expert, indeed. And, definitely confusing the situation.

It isn't that businesses can't borrow at the same rates as property owners; it's that the marginal returns on property ownership are significantly higher than that of operating business.

Not entirely sure what your second paragraph is trying to achieve.

GBHero,

Clearly,lots of others support you on this,but while I have sympathy for your views on immigration,foreign money(depending on where it is going) and infrastructure,I can seed someproblems with your proposed solution.

Had the RB raised the OCR to 5%,what do you think would have happened to the currency? There is nothing wrong with a strong currency,as Germany has shown over a long period of time,but only if the economy is structured to support it. Here,it would simply have done major damage to our exporters,the trade deficit would have ballooned and your infrastructure spending would have been further away than ever.

Germany has a weak currency , the EURO ... not a strong one ... they are the sole beneficiary of this weird new currency ... they love it ... if they'd stayed with the deutschmark , it would have been much stronger ... and given advantages to weaker world economies ... such as Greece ...

... hey , if the governments in NZ have been too slack to get on top of the ballooning property market , it behooves the Reverse Bank to wake them up with a sharp jolt !

election year so we will end up voting for someone to address housing and immigration

depending on how much you feel about it will colour most voters.

as for national these two issues could see them lose power as people want them addressed and they have lost touch

Here's what John Key promised in 2007 and yet we have continued to vote for him/National strongly for the last 10 years:

http://www.nzpif.org.nz/news/view/53038

If they were at school they'd get a D on their report and told to find something else to do.

So I have no idea why we keep voting so strongly in favor of them when they are essentially incompetent (and make promises they don't deliver on), other than the idea that it's the self-interest of current home owners who secretly like how inflated the prices of their homes have become under National. So it would appear quite probable that NZ'ers (about 40% or more) are rewarding the Governments incompetence out of their own personal gain. I'm not sure therefore who is worse, the politicians who think they can actually make a difference, or the people who vote for them?

Have you not noticed the orchestrated hatchet job our major media outlets carryout on anyone that dosen't support the status quo.

And it will only get worse, especially if there's whiff of a change in government.

Its only Feb, and the Herald are running their seventeenth article extolling the virtues of uncontrolled immigration.

Although the media is finding it tough fitting in all the pro-immigration propaganda in amongst all the anti-Trump pieces, celebrity puff pieces, & 'disgruntled consumer/fair go' sjw advocacy! Lol

The question with Key is, was he lying or just incompetent when he campaigned on the housing crisis then refused to acknowledge its existence for the next eight years?

They claimed to have a plan to address it, but since then all we've seen is them watching with glee as their personal portfolios increase at the value at the cost of locking out whole upcoming generations of Kiwis out of home ownership.

Turned out Key did want to see New Zealand become a nation of tenants in their own land, after all.

National, and the corporate powers that orchestrate them, deemed the benefits of mass immigration, export education, and protecting duopolies, to be of greater benefit (to the sales/profits of those corporates) than the benefits of governing NZ for NZers and containing house prices.

Business is fine. It's not their problem if wages can't keep up with house prices.

Eventually it is, but maybe not within the 3/6/9 years that normally affects a PM's career. Already you can get a better salary and a lower rent in Melbourne than in Auckland (e.g. in IT)...with Melbourne and Brisbane both supplying these sort of conditions, I'd doubt it'll be too long before more young Kiwis look to head offshore instead, given they've been politically abandoned by the government here in favour of the portfolios of boomers.

I'd love to not vote for National. I really would. Problem for me is that I don't see any credible alternative out there.

Perhaps if Labour had learned something from their past election defeats then we would be in a better place (e.g. have a compelling choice instead of constantly hearing how badly John Key has been performing).

Interest rates will be back below 4% after the election, and after rates have had a little play in the sun this year.

Are you saying that RBNZ will develop a ZIRP policy for the OCR or that credit rating agencies will upgrade our banks because we have an election?

Politicians will be off the hook on Auckland house prices after September, for 2.5 years.

RBNZ will be maintaining the OCR or cutting in 2018 to keep consumer spending going and to keep Jumbo mortgagees afloat in Auckland.

Banks have now significant numbers of borrowers locked into huge mortgages based on 4.x to survive.

It will be interesting - as the unstoppable forces meet the immovable objects as you point out!

Banks definately can't afford to increase interest rates too much as you say. They only make profits if they collect the interest and not have people defaulting.

There will also be a conflict where inflation is rising and RBNZ will be expected to increase interest rates. It will be interesting to watch.

Dictator - banks will raise interest rates as much as they need to as is required to fund their books. You give them far too much credit for being the ones who determine the borrowers rate when the truth is, local depositors (not happy) and offshore institutions do.

Title: "Rodney Dickens sees interest rates having to be increased to a level that will generate a hard landing for the economy"

Why ? I have read his article but I have not found any reason for his title statement above.

Please explain why interest rates will have to be increased to a level that crashes the Economy ?

The more interesting question why are you scared if interest rates increase?

A hard landing for the Economy is bad for us all Silly Robot

No it's not - it might reset asset prices allowing the 'have nots' an opportunity to actually be part of this society...

If the Economy has a hard landing due to big interest rate rises, some property owners and business owners will default. You're probably thinking "great". But that means that some people will lose their job and that many who are finding it tough will stop spending at the restaurants, on their cars, on clothes, trips, leisure, household items, they will defer a renovation etc... This means many, many businesses will struggle and some more will close down, meaning more people will lose their job, spending even less, everyone loses.

Still, the question remains unanswered: Why will interest rates have to be increased to a level that crashes the Economy ?

Actually I don't think you understand the implication of the question - if an interest rate rise causes "a hard landing" then people must be at the limit of their borrowing - this is not a good position for an individual or a country to be in.

I agree with you that people (and companies and governments) are too indebted. Still the title reads:

"Rodney Dickens sees interest rates having to be increased to a level that will generate a hard landing for the economy"

and I ask WHY do interest rates HAVE TO BE INCREASED to a level that generate a hard landing ?

To me, people's relationship to money (and money supply) is like the same as it is for a drug addict to heroine. Don't limit the supply and the druggie over doses on a good thing - often burning the house down in the process.

Limit or remove their supply, they'll go into rehab for a while and hate you for it, but will get to live another day.

'As is the case in many countries, it is normal for NZ to experience major housing cycles roughly once a decade.'

This statement says it all.

There are many jurisdictions that have high immigration and lower interest rates and DON"T have boom and bust housing cycles and do have low property prices.

Just because we continue to do the same loser housing policies that 'other countries' do then we will have graphs like Rodney has shown, and just because others do it, does not make it normal.

Thank you for pointing this our Rodney , I am a layperson , but its been evident for some time that this 10 year low OCR is likely to do more harm than good .

The OCR was 8% , a decade ago , its now 1.75%

If money was simply another "commodity" , then what commodity has ever dropped to a mere one fifth of its price 10 years ago and stayed there on increasing demand ?

Its worse in the US where money yields , or gilt rates have gone from 10 to zero or near zero

Have you forgotten NZs reserve bank cannot regulate what the rest of the world will pay for a NZ$ ?

The NZRB has no control over the foreign cash which floods into NZs property market

which was allowed to happen by Mr Key for years while in power . If anyone believes Key (a international forex trader) did not know this was happening ? I have The Brooklyn Bridge to sell you!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.