Should banks be required to pay savers the best savings account rate they offer? Australian consumer advocacy group CHOICE certainly thinks so.

CHOICE wants banks to be legally required to automatically switch savers to the best possible savings account rate they offer. It's lobbying for this in a submission to an Australian Competition and Consumer Commission (ACCC) inquiry into the market for the supply of retail deposit products.

"Competition in the retail deposit market has been curtailed by Australia’s oligopolistic banking industry. The big four banks account for almost three-quarters of all household deposits. Banks have been able to profit off consumer loyalty, introduce unfair and onerous requirements to satisfy bonus rates, and made it intentionally difficult to switch banks. The Reserve Bank of Australia has estimated that one in seven deposit accounts do not earn any interest at all," CHOICE says.

"Banks should be legally required to automatically switch people to the best possible rate they offer. This will mitigate the harmful practice of banks charging a 'loyalty tax' to long-standing customers."

It's an interesting suggestion from CHOICE. What would it mean if it was a requirement in New Zealand? Interest.co.nz's David Chaston notes most NZ banks have simplified their offering in recent times to essentially two or three savings accounts, a bonus account, a standard call account, and perhaps a children's account.

Chaston estimates if all household savings accounts had the highest savings account interest rate available applied to them, savers would've received $66 million in additional interest payments in the year to March 2023.

As you'd expect Aussie banks aren't enthused by the CHOICE proposal. A spokesperson for bank lobby group the Australian Banking Association (ABA) told The Sydney Morning Herald (SMH) given the best rates are usually on longer term products, they don't necessarily suit every customer’s needs and customers should have a choice.

“Many customers will not want to be automatically switched into different sets of terms and conditions that may not suit their personal circumstances,” the ABA spokesperson told the SMH. “Cheaper rate products often have fewer features.”

An obvious question is; if a rule like CHOICE's proposal was actually applied, couldn't banks just reduce their top interest rate offer?

'Clearly disclose the best rate available'

"Australia’s oligopolistic banking industry," as CHOICE puts it, is of course dominated by the parent banks of NZ's ANZ NZ, ASB, BNZ and Westpac NZ.

CHOICE argues savers shouldn't be required to request a new promotional offer on their deposit account every few months, saying it's concerning that up to 15% of deposit accounts in Australia aren't earning any interest.

"It should be incumbent upon the bank to switch their customers to the best possible rate available on the market. However, if the ACCC does not adopt this recommendation, then banks should be required to clearly disclose to customers the best rate available. Switching to a better rate should be simple and easy for customers, with limited friction. The ACCC should use behavioural research to consumer test the most effective ‘nudges’ to encourage switching," says CHOICE.

In February Australian Treasurer Jim Chalmers directed the ACCC to hold an inquiry into the market for the supply of retail deposit products. It's scheduled to submit a report to Chalmers by December 1.

“The vast majority of Australian consumers have at least one savings, transaction, term deposit or other retail deposit account, and collectively Australians hold over A$1.45 trillion in retail deposit accounts,” ACCC Chair Gina Cass-Gottlieb says.

“For many Australians, the interest earned on these accounts is an important source of income, and consumers are understandably keen to ensure they are receiving a good return on their savings.”

"Over the past 12 months, the Reserve Bank of Australia has increased the cash rate target from 0.35% in May 2022 to 3.60% in March 2023 in response to high and rising inflation. While banks have generally increased variable rate home loans interest rates in line with the cash rate increases, increases to the savings interest rates that banks pay their customers have often been smaller or conditional," says Cass-Gottlieb.

"The ACCC will be considering how banks have adjusted their rates for deposit accounts following these changes to the cash rate target, including the use of introductory and other conditional interest rate offers."

"We are eager to hear about competition and consumer issues affecting the supply of retail deposit products to Australian consumers and self-managed super funds. This inquiry will closely examine how banks make decisions on interest rates, and any barriers consumers face in getting a better deal," says Cass-Gottlieb.

RBNZ put spotlight on savings rates as inflation takes a toll

In its February Monetary Policy Statement (MPS) the Reserve Bank of New Zealand (RBNZ) said deposit rate increases continued to lag the increases in wholesale and mortgage rates, resulting in a further widening of bank margins between lending and deposit rates.

The RBNZ said its Monetary Policy Committee expected deposit rates to increase over the coming year, to incentivise savings, dampen inflation and support the maintenance of current mortgage rates for a longer period.

In his press conference following the MPS, RBNZ Governor Adrian Orr added to this.

"I think it's important that it's understood what we are calling out across the banks as they have been very quick to increase the mortgage lending rates, but deposit rates have lagged behind, and bank margins are holding up," Orr said.

"Higher deposit rates are a critical part to encourage savings which takes inflation pressure out of the economy."

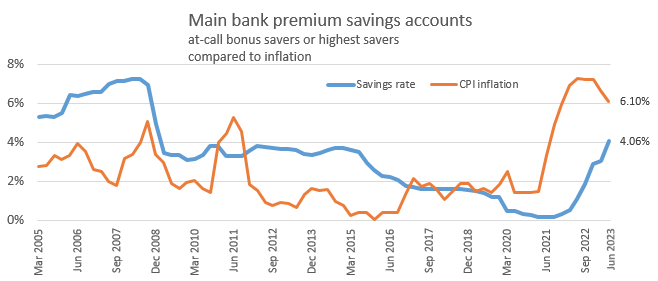

Interest.co.nz analysis at the time showed banks were offering both term deposit rates and bonus saver rates at a significant discount to inflation, which was unusual. Before 2017, the Consumer Price Index rate was typically below the average savings account rate as shown in the chart below.

*The 6.1% figure is the RBNZ estimate for CPI inflation in the June quarter. It was 6.7% in the March quarter having peaked at 7.3% in the June quarter last year.

'Increasingly profitable sources of funding'

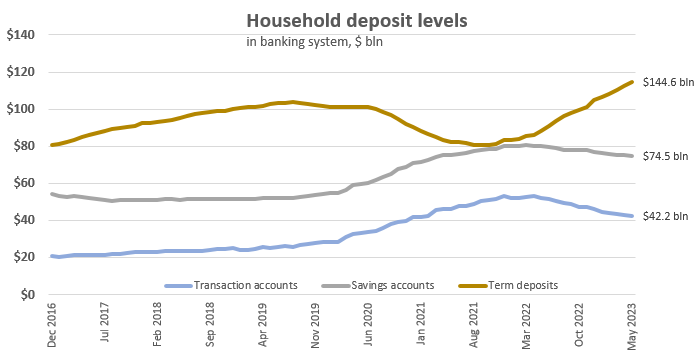

In NZ, as interest.co.nz reported in February, at-call savings accounts became popular during the height of the pandemic. From February 2020 they rose $25 billion, or 46%. At-call savings account balances peaked at $80 billion in April 2022.

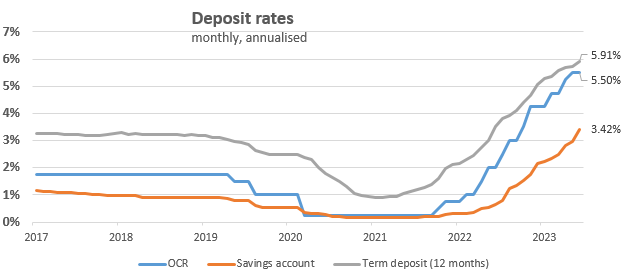

In its May Financial Stability Report the RBNZ said interest rates on short-duration deposits, such as transaction and on-call savings accounts, hadn't increased as quickly as the Official Cash Rate (OCR) and the interest income banks earn on their assets such as loans.

"Consequently, these deposits have become increasingly profitable sources of funding relative to term deposits or issuing debt in wholesale markets," the RBNZ said.

"Following heightened uncertainty and low interest rates during the pandemic, the proportion of banks’ deposit books in short-duration deposits was above its long-run average at the start of the tightening cycle. While savers are moving back to term deposits as interest rates rise, this transition is lagging the increase in interest rates."

"Banks have been comfortable holding more short-duration liabilities than historically due to their strong liquidity positions, holding down their average funding costs. The above factors mean banks have had relatively lower interest costs in the past 18 months, while lending rates and interest income have increased alongside the OCR, supporting a recovery in banks’ profits," the RBNZ said in May.

The OCR, NZ's benchmark interest rate, is now at 5.50% having been aggressively increased by the RBNZ from a record low of 0.25% since October 2021.

The ACCC issues paper is here and its press release is here.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

18 Comments

Fundamentally deposits form a part of banks required capital which backs their lending portfolios. Due to the fractional nature of their business, the banks do not lend dollar for dollar, but in multiples. (post GFC I recall the NZ level being identified as 8:1) Thus banks are making a killing, but are not accountable to depositors for the risks they use their deposits as security for. So I would suggest that there needs to be a firmer number than just "their best interest rate". You just know they'll play that for all it's worth!

Who doesn't like a good flutter? If only we could all do it with hundreds of thousands of other peoples money with no risk of blowback, where we can simply throw up a shrug and say "well hey, that's the market for yah".

Rabobank have only this week altered the terms of their Notice Saver which previously allowed interest to be paid out monthly to any other Rabo Account to compounding only. Given the tough economic conditions hardly a popular move, and in some cases I suspect would force savers to move their funds to a product with a lower interest rate.

Forcing banks to their highest savings rate would not be practical, as the higher rate accounts are bonus savers where you have to leave it or maintain a balance (WBC) monthly, or ASB 3 monthly. The main anomalies that stand out are ANZ and ASB on call savings at 2.75 and 2.90 respectively, while Kiwibank pays a far better 4.50%. ASB also has a 'Fastsaver' at 2.25%. The (bold) accounts highlighted are the main offenders in NZ, a long way below the OCR.

On a side note I see this morning the US 10 yr continues to rise.

I see no good reason to have their crazy rules for when you can or can't withdraw money, or why I have to move my money from an account that's linked to my EFTPOS card to as savings account.

I sort of lied I see a reason, and that is make as much money as possible from people not willing constantly manage the amount of money in each account.

They may say its to encourge saving, but I don't need their help.

"Higher deposit rates are a critical part to encourage savings which takes inflation pressure out of the economy."

Lower deposit interest rates and a pull back in bank lending create and conserve capital when:

19,500 mortgage holders are in arrears . Mortgage borrowing has dropped 27%. Many more people yet to roll over to new high rates. More pain coming for them. Building Industry firms filing for liquidation up 35%. 600 businesses gone into liquidation this year Link

I always spend more when interest rates are higher.

Banks should be made to lend and borrow within a margin of the OCR. i.e. +/-0.25%

Bye-bye fixed rates, no bank is going to take the risk of offering you a 2yr fix at 0.25% above the OCR, if OCR could be up 1% in a couple of months.

May as well just ban banks and we all have to use GovtBank floating rates.

I am all in favour of a RBNZ cash account.

The thing is, for the OCR to work effectively it must impact retail rates. Given that we also see year on year record profits, I would strongly argue there is room for a lower lending rates and higher savings rates, without causing all the banks to go under. I mean they can earn 700m instead of 7b. That 6.3b is a net benefit to NZ.

The thing is, for the OCR to work effectively it must impact retail rates.

It does, not directly, but it is standing behind the curtains pulling the strings.

I mean they can earn 700m instead of 7b. That 6.3b is a net benefit to NZ.

I wonder how far you go before the banks decide that the however many $billions of capital are tied up in NZ operations no longer make an adequate return and are better deployed back in Oz, or other overseas markets? I bet its well above that $700m figure.

Also, how much of that $7b flow back into kiwisaver funds and other broad index investments owned by NZers.

So, no lending for anyone without bullet proof credit ratings? No-one is going to take a chance on a business or personal loan for 0.25% risk premium.

Also would mean no fixed rates, The OCR is overnight..

Personally I quite like being able to manage risk by spreading re-fixes across several tranches.

The O in OCR is 'official': https://www.rbnz.govt.nz/monetary-policy/about-monetary-policy/the-offi…

Its still only an overnight rate...

Just make the floor OCR -0.25%, if the banks want to term out their deposit base they have to pay higher rates.

The current situation where they take advantage of the apathy of unsophisticated depositors is shocking.

I had my savings in a big bank, and for about a year the interest rate stayed at 0.05% while the rest of the country went up to ~4%. My savings account was listed as 'obsolete' but they didn't bother to tell me...

I'm a fan of what Kiwibank did recently, they now have 3 sets of savings accounts:

- General savings account (online call) - no punitive rules around withdrawals or required deposits per month.

- Notice saver (32 or 90 days)

- Term deposits (various lengths)

All are available as either regular accounts or PIEs - you probably want the PIE version.

Most of the other banks still have multiple flavours of the general savings account depending with different rules or interest rates, though as noted in the article they are mostly down to 2 or 3 types now.

I don't think it would ever make sense to move people between these different classes of account as the withdrawal rules are very different, but it's possible that some people are grandfathered on older worse accounts, and it would make sense to require banks to shift them to other accounts where they are better.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.