By Bernard Hickey

Now we've heard from new Reserve Bank Governor Graeme Wheeler for the first time and we've seen the housing market burst back into life, it's worth revisiting the eternal question of whether to stay floating or to fix your mortgage.

The short story is that economists and the financial markets are divided on whether the Reserve Bank will cut or hold the Official Cash Rate over the next year or two. Overall, inflationary pressures and the economy are subdued, but house prices are surging again and the new Reserve Bank Governor seems to be taking an orthodox approach to policy and interest rates, which means he is less likely to cut.

That means my views on Fixed vs Floating are changing. While Reserve Bank Governor Alan Bollard was in charge of setting the OCR and the housing market was lukewarm, I thought there was a greater chance of a cut in the OCR. But I've seen enough now of his successor Graeme Wheeler since he started at the end of September to believe there's a greater chance the OCR will be flat or even be hiked in the next couple of years.

The Reserve Bank has a big dilemma at the moment. The economy is subdued and inflation is below the Reserve Bank's 1-3% target range. All other things being equal, there'd be a good case for the Reserve Bank to cut the OCR, which should in turn drag floating rates lower and make floating more attractive than fixing. But house prices are taking off again and any OCR cut risks pouring yet more petrol on the fire of record low interest rates under house prices, particularly in Auckland and Christchurch.

One way for the Reserve Bank to get around this dilemma would be to use other tools to try to control the housing market, incluing limits on Loan to Value Ratios (LVRs). Other central banks and bank regulators in Israel, Canada, Hong Kong and Singapore have used such LVR limits, but Wheeler said early in November he would not use a LVR limit yet, even if he had it. See the full article and video here.

That means Wheeler is more likely to use the blunt instrument of the OCR to try to keep inflation around the 2% mark he has agreed to target in his own Policy Targets Agreement. If he worries about the housing market getting too hot then the one way (in his view) to knock it on the head is to hike the OCR. That's why I'm tending towards floating half and fixing half of my mortgage in coming months, rather than floating it all.

Everyone is different though, so it's worth running through the pros and cons of fixing vs floating and look in depth at the various factors at play. It's also worth spending some time on it. As I'll show lower down, it's a decision that could save (or cost) you thousands of dollars over the next couple of years. Here's our Fixed vs Floating calculator to help.

Also, there are many different views, and I've included those views of other economists below.

What the economy is doing and what the RBNZ is saying

Firstly, let's look at what the 'ref' at the Reserve Bank has said recently and what the latest economic and financial signals are saying.

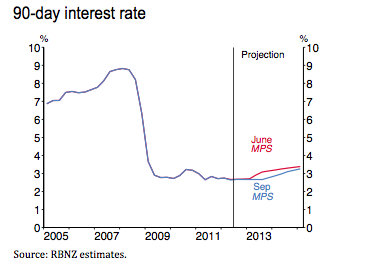

The Reserve Bank's chart below from its September 13 Monetary Policy Statement of its forecast track for the 90 day bill rate, which is typically around 30 basis points above the Official Cash Rate (OCR), tells the story.

The blue line shown is its September forecast with the OCR peaking at around 3%. The red line shown is its June forecast. These forecasts have been dropping for at least a year.

Wheeler said in the Reserve Bank's October 25 decision that New Zealand's economic outlook remained modest and the global situation was fragile. He said he was watching inflation closely and it was expected to head back to around 2% so he saw no need to change the OCR from 2.5%.

So the Reserve Bank is forecasting a rise (the blue line), but it's very slow and not much at all. If the Reserve Bank's forecast now actually turns out to be fact, then floating mortgage customers would see their advertised floating rates of around 5.7% rise very slowly to a peak of around 6.2% by the end of 2014. Although it's worth remembering that those customers with plenty of equity and good repayment records can push their banks for better deals at the moment of around 5% to 5.2%. Those in competitive situations would see their floating rates rise to around 5.7% by the end of 2014 in this scenario. Currently (Novembe 20) 18 month-2 year rates are around 5%, which would mean you'd pay more for the first 6-12 months or so and then less in the second 12 months.

Fixed rates tend to be more closely linked to wholesale 'swaps' rates than the OCR. Swaps rates have broadly fallen this year on increasing fears about a global slowdown and a slow rebuild in Christchurch.

There is a way to test the various scenarios and work out which option is cheaper (although cheapness is not the only factor worth thinking about for many people).

There is a calculator

We have a calculator here that allows you to test which rate is cheaper, depending on three different interest rate scenarios. Click here to go to the calculator.

There are three different rate scenarios. A is the high one with an OCR peak of almost 3%, B is the medium one, which is in line market expectations for a small cut and then a rebound to 2.75%, and C is the low one, which implies some cuts to 2% and then a rebound to 2.5% by early 2014.

Try it out to see which option is cheaper for you, depending on your rates view.

A simple money calculation isn't everything though. Some people put a high value on knowing exactly what their mortgage payments are going to be for the next two years because, perhaps, they have a fixed income or are very nervous about a sharp rise in rates. They may see paying slightly more for a fixed mortgage as a bit like an insurance payment.

Others may want to stay floating because they really believe interest rates will be cut again or not rise and because they don't want to be stuck fixing and have to pay an exit fee if rates do fall. The most recent memories for some people are having to break their mortgages and pay big break fees (or finding it unaffordable to do so) during 2009 and 2010. Others have longer memories of being stung with big increases in floating mortgage rates as the OCR was hiked from 5% to 8.25% between early 2004 and mid 2007. Really old people remember the 20% plus rates of the mid 1980s. I'm not that old. ;)

Everyone has different appetites for those sorts of risks about paying more or missing out on paying less, and different views about where interest rates will go. Those are the main things to consider when fixing or floating.

More than 50% of New Zealand's mortgage lending is now on floating rates, which is just below a record high and a complete turn-around from before 2008. Although there has been a slight move back to fixing in recent months. See Gareth Vaughan's article here. The decision for many now is when to fix.

The bank economists' views

Westpac's Dominick Stephens has argued that fixing made better sense than floating for most of this year. He sees the Official Cash Rate eventually being raised to 6% because of inflationary pressures, although he doesn't see the OCR starting to rise until September next year. An OCR near 6% would see floating mortgage rates around 9%.

We doubt the RBNZ is ready to signal a reduction in the OCR. The Canterbury rebuild represents a potent source of inflation pressure lurking in the near future. And reducing the OCR now might stoke the housing fire. Our view remains that rates will remain on hold until September 2013.

Fixed vs floating: Fixed-term rates out to two years are currently below floating rates, while three-year and longer fixed rates are only slightly higher. With fixed-term rates so low, fixing soon is likely to prove better value than floating over the next few years. Staying on floating would only be the better option if the RBNZ actually cut the OCR. While that’s a risk, our central view remains that the OCR will stay on hold for now, and increase steadily starting in the second half of next year.

ASB's economists expect the Reserve Bank to wait until September next year before increasing interest rates. Senior Economist Jane Turner said in a August 17 note is that "some fixed rates are now below or similar to floating rates, offering a window of opportunity (to fix)"

The economic recovery remains gradual and inflation pressures are currently subdued. Recent economic developments highlight the downside risks that remain to the outlook in the near term, and we expect the RBNZ to leave to OCR unchanged at 2.5% until March 2013. Nonetheless, we continue to expect the economy to recover which, along with the Canterbury rebuild, will underpin a swift pick up in inflation pressures. As a result, we expect the RBNZ will need to steadily increase the OCR over 2013 and 2014, returning the OCR to 4% by mid-2014.

For borrowers, this means that floating mortgage rates are likely to remain at very low levels for the rest of the year, although borrowers do need to be prepared for rising interest rates from 2013. A combination of domestic and offshore events has seen the market start to price in interest cuts. This has reduced domestic wholesale funding costs, and lowered some fixed-term mortgage rates. In some cases these are lower or at similar levels as the floating mortgage rate. Our view is these declines may not be sustained unless the RBNZ follows through, and provides a window of opportunity for those borrowers that prefer certainty to protect themselves against further interest rate increases.

ANZ National's Cameron Bagrie sees the economy in a 'grumpy growth' mode that means the Reserve Bank is likely to hold the OCR for some time. See more in ANZ's economics notes here.

The RBNZ is expected to remain on hold until early 2014 and we continue to see value in fixing for 1-2 years. This allows borrowers to save money by fixing and “locking in” rate cuts that may not eventuate.

BNZ Chief Economist Tony Alexander said on November 15 that he would stay floating or fix for one year at 5.25%.

The RBNZ is unlikely to raise the cash rate until over a year from now while the direction for swap rates looks more likely upward than downward but nothing suggests that we are yet close to a decent jump. That is because just as we are receiving better than expected data on the US housing and labour markets plus consumer confidence, and while data from China are getting better, business confidence in Australia has fallen quite a bit as businesses scale back their investment plans, and recent releases for France and Germany have been worse than expected.

Specifically, why won’t the RB ease monetary policy because of weak NZ data? First, the housing market is rising already and will become a source of inflationary pressure from next year so cutting rates now and encouraging even more aging investors to quit low yielding bank deposits for residential property investment vehicles will not only hasten and enlarge the housing boom-bust but eventually destroy the wealth of many unsophisticated and unlucky people.

Second, there is no evidence that businesses are refraining from investing and hiring because interest rates are too high. In fact decades of research shows the biggest influence on businesses is their confidence and that is fine currently.

I would either sit floating or fix for one year at 5.25%. But I would also keep an eye open for a discounted long term fixed interest rate in order to get some certainty about my cash flows during these continuing uncertain times and because at some stage interest rates will blip up. But we do not appear remotely near that point yet so borrowers look like facing good conditions well into 2013. Pity us savers though.

--------------------------------------------------------------------------------------------------------------------------

Mortgage choices involve making a significant financial decision so it often pays to get professional personalised advice. A Roost mortgage broker can be contacted by following this link »

--------------------------------------------------------------------------------------------------------------------------

No chart with that title exists.

61 Comments

I'm sorry that I don't pay enough attention to what the various "experts" say, but do any of them actually have a track record of predicting the actual movement of rates?

Bernard, although I believe rates will be low for longer, I believe your view is wrong and putting at least 50% of your mortgage at a sub 6% 5 year rate is the most prudent advice.

Look at it this way what are the downside risks to taking a 5 year rate at 5.99%?

1. If the OCR does as expected you will be about even or at worst slightly worse off if you were able to negotiate a large 50bps reduction in the floating rate with the bank (I note Bernard was only able to get a 30bps discount to the average floating rate).

2. If the economy improves in any way more quickly than expected (remember we are nearly 4 years into the downturn and to be honest I don't see another 5 years of downturn in it especially when the real effects of the maybe $30b that will flow into the hands of ChCh property owners (most won't actually go towards new construction)) then you will be glad you fixed long at a low rate.

3. If things get worse, we'll all know about it and you should be able to break preemptively at no real cost. Look at ASB for example, the 4 year rate at 6.1% is higher than the 5 year special at 5.99%, so you could potentially break in the next year and pay no penalty unless the 4 year rate drops sharply and unexpectedly.

So would you really be disappointed if a 5 year became available at 5.5% or would you be more disappointed if the 5 year rate went to 8.75% like it did only months after being 5.95% in 2009?

Hoping for lower rates may just be like going one case too far on deal or no deal (which is better viewing than the 6 o'clock news!) - just not worth the gamble.

A prudent man would say 5.99% for 5 years is good enough and fix as much as they need to at that rate to feel comfortable. 50% is my advice and aim to have the other 50% paid off within the five years anyway.

I think the point is that if your loan is going to take a long time to repay, say 15+ years, then you'll be paying a lot of interest and the 5 year fixed rate should be considered seriously. On the other hand, if it'll all be paid off in less than 10 years, the actual interest rate, be it 5.5% or 8%, won't make much difference to total repayments and it's probably safe to float or fix at a really low rate of 4.99% for 1 year.

Chris J

Many thanks. Interesting points.

But what if the OCR is cut to 0%, as it has been in most other developed economies? That would push floating rates down to 3-4%.

Also. How would you get to break your mortgage at no cost? Some banks are paying break fees at the moment, but they sure didn't during 2009/10 when people who fixed at 10% were screaming.

It all depends on your world view.

Here's one that says the developed world is in for 15-20 years of deleveraging, slow to no growth and virtually zero% interest rates. http://www.reuters.com/article/2012/07/11/us-markets-shadowbanks-idUSBR…?

cheers

Bernard

Bernard for most banks as long as the bank's offered fixed rate for the equivalent remaining period is the same or lower than what you fixed at then there is no break fee (apart from a small admin charge which they will often wave). Check the exact formula with your bank, but I know that this is the case with the standard formula that ASB use.

In 2008 when floating rates were over 10%, I fixed on the cheaper 2 year rates (about 200bps lower) and broke those as soon I realised what was happening in the US with only a very small break fee (there was a fee only because I was a bit slow to react first time round). After that I fixed for 6 month terms and broke those every 6 weeks just before each OCR announcement all with no break fees but achieving a rate at least 100bps below the floating. When rates hit sub 6% for 5 years in 2009, I put most on those rates and most of the rest on the cheap short term rates. I then broke the remaining long term rates when the Feb quake hit without penalty and floated most until now putting half on a sub 6% 5 year.

The way I see it is that I have the amount of debt that I'll be left with (after all insurance issues (settlements or liquidation of non cash settlements), spending on new projects and bits and pieces that I intend to do are sorted) is now fixed at a sub 6% level. Which means that for a total of 8 and a half years (3.5 past years, plus 5 further) I have had average debt costs under 6%PA. To have that cost guaranteed to be no higher for such a long time satisfies me - even if it turns out I could have got the money cheaper.

I can't see that it is possible that interest rates go much lower in NZ - you have seen the housing market haven't you? Cut rates to say 4% floating or offer 5% 5 year rates will see house prices soar which combined with insurance flows would push the economy into boom times. Certainly if rates did fall that much I would just load up with more debt and buy as much property as I could.

Certainty is more important to me, after all I am a property investor - I don't take risks (nor do I waste money) which is why I'm not broke.

BH, being a simple person...

In terms of fixing or floating I use a spreadsheet...

So I look at the payments over say 5 years as fixed, a nice constant line, result area under the graph is the total ammount I pay over 5 years...that 5 years is of course at 6.6%.

lets use your advertisers mortgage calculator,

400k mortgage $163,553 at 6.6% fixed for 5 years.

Now floating or 6month sums is 5.25% (using kiwibank rates).

400k mortgage $143219.

So another straight line...another area.

saving over fixed, 20k....nice car that....or be sensible and clear capital.

Lets look at those rates staying flat for 2 years then rising at 0.5% per year.

$152312

$11k cheaper...

Lets assume a rise of 0.75% per year in the OCR in years 3, 4 and 5...

$156849.6

Lets assume 1% rise in years 3, 4 and 5

$161492.28

Still saving 2k....

I know the above is somewhat rough....but are we really saying that we will see 2 years of a flat OCR and then 1% rises per annum? Some huge steps?

So Im missing something?

Otherwise 1/2 and 1/2 seems the worse of both worlds...floating or 6 months fixed seems the best still....If and I think its mor elikely the OCR drops then the savings are even bigger!

regards

"But what if the OCR is cut to 0%, as it has been in most other developed economies? That would push floating rates down to 3-4%"

Bernard - whilst 0% is not impossible, think about what might cause the RBNZ to ever contemplate cutting to that level - the answer basically is "Armageddon", and certainly not NZ falling back into recession if that happened to occur. In the Armegeddon scenario (i.e. a banking crisis) the banks would no longer be lending to new borrowers, and their cost of funding (be it much longer now than before the GFC) would ultimately push their funding costs through the roof i.e. that spread in rates now of 150bps odd, plus bank margin above OCR, could be two or three times that easily in that scenario as they try to find funding at any cost. That would be passed onto borrowers resulting in mortgage rates arguable at or above current levels despite a possible zero OCR - adding to that, the bank bill rate certainly wouldn't be sitting 25bps above the OCR, as it is currently, when banks sweep up all liquidity up that is available in that market - remember in 2007 it blew out to 100bps, so a zero OCR could have a 1% plus bank bill rate, then add on 300-400 bps liquidity spread and a bank profit margin, you really aren't understanding what a zero OCR would mean for mortgage rates.I'm surprised you're only getting 5.4% on the floating rate. A few months ago (after reading a column here) I phoned ASB to ask for the best floating rate they had, and got offered 5.25%, with a promised reduction of 0.5% off advertised floating rates for the next 2 years. No hammering required, I just asked nicely. Never mind switching banks, I'd consider switching brokers.

Good point pythagoras. I renegotiated via my broker about 6 months ago. Things have gotten more competitive since then.

Time for me to go back.

Although I've got a feeling I'm not that popular with the bank call centres these days.

I'm told one major bank call centre has a dart board with a picture of me on it...

cheers

Bernard

It sounds like you have upset cafe owners as well now. I would like an economist to study why coffee seems to have an inverse price/quality gradient, the more a cafe charges for a short black, the worse it will taste.

And does promotion of the "Latte Effect" savings method cause a decrease in sales in coffee?

Why stop at bartering with banks & cafes? Why not barter for everything? Electiricity, gas, Rates, petrol (haha - like to see this), groceries (picture a full shopping cart at the checkout with customer bartering prices down!), parking fees, etc etc ...

Also Internet, UFB is coming and thats looking a lot cheaper....

Electricity, well maybe not haggle, but how hard is moving?

BTW has anybody got an explanation of why prices are going up when there is a reduction in use? ie over-capacity?

regards

Personally I can't see much chance of a large OCR cut. Don't rule out a tinker or two however.

I'm not particularly optimistic, but there are a good 50,000 houses in ChCh that will be fixed at something like an average $100,000 (even if EQC don't realise that themselves yet).

This work alone will allow a lot of additional money to flow through the economy.

Note that I don't believe that there will be a big private spend up on new buildings in the CBD (there will be lots of small buildings but only a handful of big ones over a long number of years) and there won't be significantly higher than normal levels of new house build activity.

But even with a lot of insurance money leaking away the amount of money being spent is not the kind of stuff that makes a depression. At worst it will be a slow moving recovery and rates will remain low for longer, I can't see a scenario where the economy tanks and interest rates fall unless the Government opts for tough austerity which will get itself unelected and a change of policy anyway.

"I'm not particularly optimistic, but there are a good 50,000 houses in ChCh that will be fixed at something like an average $100,000 (even if EQC don't realise that themselves yet)."

seems pretty optimistic ;) all the pollies and you seem to assume the ground will stop shaking? It may, it may not. If it goes long enough, who's going to insure housing down there? I can't believe anyone is still offering insurance there...

It hasn't stopped shaking but that doesn't matter - the wind hasn't stopped blowing or the rain falling either. (in general that is, it's still and sunny today if you're interested).

Insurance is available in the greater part and I don't believe a shallow M6+ under the city would change that much either.

The level of work to be done is huge even if it is much lower than the Govt expect. Most of the work won't be new building however. The Govt and CERA managed to scuttle what would have been a huge CBD and new house building boom.

(I note the site of another larger office building has come on the market as vacant land - more insurance money gone).

I cant see a cut to 1.5% straight off....now 0.25% In december or Jan, yes.....if it was me that is. Meanwhile though we have a RB who now seems even more orthadox....so Jan/march maybe....I think we'll need to see 1 or 2 more months of bad data to convince them of a drop.

regards

I have had these rates from ASB.

Floating 5.25%

1 yr 5.05%

2 yr 5.35%

3 yr 5.55%

4 yr 5.9%

5 yr 5.99%

I asked about break fees as our mortgage is fixed at 6.2% until August 2013. ASB wanted $2804. Shall I, shant I do it????

The break fee is interest you were going to pay if you stayed fixed.

If you go floating on a discounted rate or short term fixed you might recover this cost in a short period.

Without knowing the amount of you loan its a bit hard to do calulation.

Another stratery might be to talk to bank and say if I fix for a longer term, say three years or more will you look to discount the break fee. They might as they know you have signalled to stay with them and might be more receptive.

As well if you don't have your full banking with them (salary direct credited / credit cards / insurances) see what they might discount if you offer them this business as well.

Best advice, talk and negotiate but don't threaten to leave as if they get wind that they think you might leave them after any discount of break fee they will won't even look at it (as they will think all they are doing it making it cheaper for you to go elsewhere) hence they will look more favourable at you refixing with them.

Keriwin - I work for Kiwibank and noted your enquiry about whether you should break or not. Feel free to give me a call on 027 289 9191 as I feel that I can save you money if you broke your home loan(s) and refinanced to Kiwibank.

Mobile Lender, Kiwibank is a funny lot. Three years ago we were looking to switch bank - Kiwibank turned us down in a 15 minutes meeting with the loan manager. Eventhough our loan-equity ratio was only 40% and repayment was below 20% of gross income. Weird criteria you guy have at the time..

Went to the big four and all approved our mortgage within an hour.. Chose BNZ and they has been pretty good to us..

Are you older Chairman Moa? I've heard (a couple of years ago) that Kiwibank are very strict on lending to older people (over 50) insisting that the debt must be repaid in full before retirement even on rental properties that generate their own income.

In the 40s I am.. Their excuse at the time was I just changed job for less than 3 months eventhough my work history spanned continously without a break for 20 years.. And my OH was in a senior managent role earning 3 times as much as me. The Aussie banks welcomed us with opne arms.. a bit sad really as we'd love to support the under-dog (Kiwi owned) and I tried and failed...

went to the ANZ 2 years ago for a mortgage .

i had 70 % equity in house and in my early fifties.

i could have had it for 25 years if wanted but chose a shorter term.

ANZ more than happy to cater for us oldies.

I had the same experience, thought we should support the local bank but had made the mistake of using KiwiBank for my pension. ANZ and Westpac welcomed us with open arms. Needless to say KiwiBank no longer gets any of our banking

Spreadsheet/calculator.

10months payment at 6.2% $=A

10months payment at 4.95%? =B

If (A-B) > $2804 then break? I'd bet they have it set so it isnt.

regards

I have spent the last two years massively reducing debt.

1. How wonderous that has been to the cashflow. A simple cost saving. Lots more disposable. True, the taxman comes calling. But I am still ahead.

2. I sleep at night. The equity and cashflow are now so strong that negative things that could pop up are not so threatening.

3. It's all on floating, because the last exercise when I looked at break fees was so ferocious. (Westpac) ( and I didn't break). Any minor advantage in a lower fixed rate does not stack up against that risk.

4. It's all on floating. Because if interest rates do go really high. I can still afford it. And fixed would only protect me for so long.

Keriwin - I work for Kiwibank and noted your enquiry about whether you should break or not. Feel free to give me a call on 027 289 9191 as I feel that I can save you money if you broke your home loan(s) and refinanced to Kiwibank.

LOL....

regards

All pretty well what I recon is going to happen over the next couple yrs....just keep a close watch of things....

" Really old people remember the 20% plus rates of the mid 1980s. I'm not that old."

That includes many who had young families in the mid 80s and still well under 60 yrs old..

BH does your predidious against baby boomers now extend well below them now?

And it also includes those who remember the long period of low interest rates before then, and the elastic effect of the high rates of the 80s thru 90s.

Steps

It seems to be the norm now to phone up the bank and get a discount on the floating rate. I currently have a 0.6% discount off the floating rate for the next two years. If the OCR does drop, I wonder whether banks will drop their floating rates by the same margin given so many of their customers are already getting good discounts off the advertised rate?

Uhm ... MortgagedUp - did you pay me your fee for assuming a similar name to mine?

On this topic of asking for rate discounts - are the bank call centres authorised to agree to discounts? Or do you need to visit your branch & see a loans officer?

Given the uncertainty that exists globally – especially in Europe – and consequently the future for interest rates, the key question should not really be “Which is best (for this read “cheaper”) option? “

Rather it should be “What degree of risk or certainty is one prepared to take or is able to take?

If anyone is interested in an early repayment penalty calculator.

I had to repay our mortgage with some early penalty cost, this calculator gave almost the same as what BNZ charged me

http://www.homeloanexperts.com.au/fixed-rate-loans/break-costs-exit-fees/#BCC

Also Hannah McQueens new book: The Perfect Balance advises how to repay your mortgage early. Downloaded the preview - but if I pay $22 for the full e-book then that's $22 I can't use to repay my mortgage early....

Had a chat to BNZ while I was in Auckland. My mortgage had another 6 months to go on a 3yr fixed term, if we decided to fix it again, they can waive the penalty cost but since we sold up and repaying back in full they told me to take a hike (in a polite way!)

.

This calculator says my break fees are $1803. ASB have quoted $2804.

ask ASB for a break down, mine had an admin fee of $600 and some interest accrued. The calculator gave me a cost of $2740 - BNZ worked it out at $2876 + fees atc...

Break fees all depend on what base rate the Banks use to calculate off. Some banks will take the wholesale rate on the day you fixed and if you had a discounted rate off 'carded' you will be effectievly hit twice - I know a few years back this was Kiwibanks practise.

In my days in ANZNat, we used the actual rate that you fixed at, therefore lower interest rate differential hence lower break costs. All this may well have changed in the last 2 years.

My experience gave me the rule of thumb, breaking to a lower fixed rate was always a break even affair. Those that made the right decision to break did so as the OCR was on it's way down and they capitalised on floating rates going even lower. If you break to a constant alternative you will remain 'break-even'

The other thing as the kiwibank mobile person said...they could save you money.

I assume if moving to kiwibank they'd pay that sum for you?

So if ASB doesnt wave a lot of that fee I'd ring that mobile, what the heck.

regards

by? thats agressive....before 2014? now I'd say yes...

regards

Bernard - what I think you're forgetting in the "RBNZ cuts the OCR to zero" scenario is that the NZD will go down the elevator shaft - why would any investor remain invested in a tiny illiquid market at no premium over the big liquid ones - and we won't be deemed a better credit risk at that time as we'll be very much a RISK currency

Bank funding spreads will blow out hugely to have to attract the required capital, as likely will NZ Govt bond levels. i.e. OCR at zero but blow out in OIS spreads maintains a bank bill rate still around 2.50%, add another 2% onto bank funding spreads and you've got higher mortgage rates, certainly not lower

Then consider the impact of the now 40 cent NZD - we'll still be importing oil and other essentials. Give it six months and 30% commodity price rises in NZDs, Chch rebuilding no matter what, and you've got the RBNZ not happy with a zero OCR...then...........

Those are the scenarios that everyone thinks they know about, when in fact no one has a clue as to how they will play out. The one I mention above has a high chance, even a probability, in a global banking crisis

OCR doesnt have to go to 0% right now though.

I see the OCR drop as a symptom and not a cause, but I do think its a valid comment....I suspect the reason we have such cheap lending is the carry trade etc....so its lucrative for foreign banks to lend to use at 3 or 4% when they can get it ofr 0.25%.....hugh profit, low risk...so while the OCR will drop I think...m not sure how much lower....1.5% maybe...

regards

This time last year I fixed a chunk of my mortgage for 12 months and kept a fair chunk on floating, being the amount I expected to be able to repay. It was a bit of a mistake because interest rates didnt rise, so I ended up paying about $500 more in interest for the amount that was fixed over the term, but that's a pretty small sum so never mind.

Now its time to review and I'm looking to increase my debt mainly because the rate is so low. I was able to negotiate a 12 month rate of 4.85%, 110 points lower than what I am on now. The bank I am talking to is working hard to poach me away from where I am now, offering a considerable amount in cash as an inducement.

Changing banks is a bit of a hassle, so it is a pity that while I can get my current bank to match the rate of the poacher, they wont give me any cash to stay, even $500 - $1,000 would keep my business. As my loan is almost due to come off the fixed term, the break fees are minimal and the poacher is willing to meet these too. The thing to watch out for is conveyancing costs. There's quite a range and the solicitors will easily eat up all the $ that the bank is offering as an inducement for the switch.

I also saw today that so many people are switching now, it's clogging the system, which may explain why the shorter fixed rates have jumped up a bit. The poacher bank tried to tell me that they wouldnt honour the promise of 4.85%, but having already said they would offer that to the end of the month, I wasnt very interested in them having second thoughts, I could stay where I am miss out on the cash but make the same savings by holding my current bank to its offer to match the poacher's original offer.

4 years ago I did my calc and figured I'd save 4k by staying floating rather than fixing....so Ive saved that and more...

No one seems to think there is much chance of the OCR going up in 2 years...and more seem to think a drop isporobable.....so the thing for me is why fix?

Conveyancing costs, I find they get met by the bank you are moving to, ask.

regards

This time last year I fixed a chunk of my mortgage for 12 months and kept a fair chunk on floating, being the amount I expected to be able to repay. It was a bit of a mistake because interest rates didnt rise, so I ended up paying about $500 more in interest for the amount that was fixed over the term, but that's a pretty small sum so never mind.

Now its time to review and I'm looking to increase my debt mainly because the rate is so low. I was able to negotiate a 12 month rate of 4.85%, 110 points lower than what I am on now. The bank I am talking to is working hard to poach me away from where I am now, offering a considerable amount in cash as an inducement.

Changing banks is a bit of a hassle, so it is a pity that while I can get my current bank to match the rate of the poacher, they wont give me any cash to stay, even $500 - $1,000 would keep my business. As my loan is almost due to come off the fixed term, the break fees are minimal and the poacher is willing to meet these too. The thing to watch out for is conveyancing costs. There's quite a range and the solicitors will easily eat up all the $ that the bank is offering as an inducement for the switch.

I also saw today that so many people are switching now, it's clogging the system, which may explain why the shorter fixed rates have jumped up a bit. The poacher bank tried to tell me that they wouldnt honour the promise of 4.85%, but having already said they would offer that to the end of the month, I wasnt very interested in them having second thoughts, I could stay where I am miss out on the cash but make the same savings by holding my current bank to its offer to match the poacher's original offer.

Now its time to review and I'm looking to increase my debt mainly because the rate is so low.

What do you plan to do with the equity released?

Why should your current bank give you cash to stay if they are matching rate you have been offered elswhere??

The cash inducment is to offset the hassles (time and cost) of changing banks.

Also as you state sometimes the cost of transferring especially if you have Trusts and LTC involved

Beware of changing banks all the time as well as they do look at track records when they look at deals outside the norm: they are more likely to back an existing client with good history and relationship with them then take a punt with someone who looks to bounce from bank to bank (and expect the same as someone who has been loyal to them for a period of time).

I banked with National for many years....when I went for a mortgage they were in-different to say the least...ASB on the other hand were extremely keen....so I moved....ditto kiwibank and they news is they seem to have stayed pretty keen to keep me.

Personally I think of a bank like a shop, Im buying a something.....they other side just want to empty your wallet for as much $s as they can.

ie Ive seen enough of the incumbent being lazy and in-different or even trying to rip you off to conclude that so called loyalty is a one way street in many cases....its even used against you.

regards

Well, I've grown tired of waiting for Floating to actually "float". Have fixed for 6 months at 4.9%.... Pretty much the same as floating anyhow - from the time of listing your house etc to an actual settlement date 6 months would just about be up.....

ZIRP in New Zealand...? No way, Josei, and I'll tell you why!

At 25 basis points per drop, we have 8 metings 'till ZIRP, unless Wheeler cuts by more, which is highly unlikely. That will put us late into the second half of next year. By then, the US housing market will have staged a strong come back, and NZ's housing market would be in a tremendous bubble that will make the last one small by comparison.

Then, the danger of collapse will be very high, since we will still have high unemployment and slow growth in the economy, and the Reserve bank will be forced to hike in a hurry, risking further economic slowdown and consequently higher unemployment.

I am willing to bet it's not going to happen! Any takers...?

HGW

however we dont have to go to 0.25% I see the OCR drop as a symptom of events rather than a cause. If we did drop below 1% it would be because we had entered a depression with significant deflation. So houses etc would already be collapsing in value and un-employemny rising significantly....

A strong comeback for US housing, well I will believe it when I see it...

I dont understand why you think the RB would raise and raise a lot....If you look at the instances where there have been hikes in say OZ and the EU well they were reversed as things went pear shaped. They only raised them and too quickly because of the inflation bogeyman fears.

Also some housing areas are up a lot....others are not....so a raise would maybe effect the boomers a bit but could kill the stagnant areas.

You are betting we wont see a 0% OCR? or we wont see <1%? or what? Im not clear. The former is simply unlikely....the latter not much....drops under 2%, yes....

regards

Steven,

I don't believe NZ will see ZIRP. I see money everywhere I look in NZ. Newer, more expensive cars, people eating out and going on holiday, people paying exhorbitant amounts for a wooden box to live in, and all of it is funded by borrowings. Ever since I moved here from California, 20 years back, I have watched NZ'rs live beyond their means by borowing. The time of reckoning will come.

Australia and New Zealand are both triple A countries, not many left today worldwide, and our standard of living is even better. So we have 50,000 people on unemployment benefits, and a hord of beneficiaries all over the country, but we are not in a depresion, or even a recesion, we are simply growing slowly and that is not a case for ZIRP.

The problem is people want government largess, they see it everywhere, and believe the rubbish propaganda that we are about to go 'kapput' unless we start growing as we were back in the go-go years Well, the bad news is that the silly season is not coming back, and it shouldn't.

Deflation is good for people on a fixed income, for people saving to buy their first house to raise their children in, for retired people, and many more types of people enjoy deflation..

The question then becomes: For whom is deflation a bad thin?. Mainly for people that have debt, because deflation makes debt more expensive, since one pays the same amount with appreciated currency, currency that is now more valuable than before the deflationary period.

Central banks the world over are fighting deflation because it will be the end of them. I am not one to fight the Feds because they will always win. They have the printing press at their disposal and the propaganda machine outputting rubbish at full blast.

Do you think they are going to fail? Do you think they will let their hegemony end? In the last hundred years the shift of power in industry between capital and labor has been won by capital. Capitalist take now the bigger share of the loot, as opposed to labor being a more important component of industry one hunded years ago.

Do you think that is about to change? I don't. They will reinflate the bubble over and over again, until the system collapses upon itself, and a new world currency is stablished still within their domain.

Have you noticed how everytime their is economic trouble, the stimulus needed is greater than before? And also how their frequency is increasing? Think 1972, 1987, 1999-2001, 2008-2010, and think of QEI, QEII and now QEternity... Eventually it will collapse.

Saddly,

HGW

I see some ppl with new cars, on the other hand ive been in checkout queues in countdown and seen OAPs with not enough money to pay for basic groceries.

Yes the former probably is debt driven, cant do the latter except via a CC....and that just delays things a bit.

I would suggest deflation is good for very few as the effects are so profound and deep. If you have a huge wad of cash well OK.

I'd suggest you have to think deeper....Ive been on such a course of thought/investigation for some years and the deflation effects are complex, difficult to fathom but profound.

If its a payout from a pension then somehow that pension has to get interest from a decimated market...even retainling its assets eg share prices in a deflationary market is hard...

Those saving for a new house will also see their wages dropping or becoem un-employed....so relatively speaking they are probably worse off.

OAPs, however consider how many get their healthcare, if its public and teh Govn cant get the tax income then they wont have healthcare and maybe not even pensions....or the state pension is or will be set to match the deflation.

Central banks are fighting this because its teh end of all of us....certainly no central banker wanst to go down in history as the Chairmn who allowed the Greatest Depression ever to happen...even while teh fruity loops in Congress and Govn seem hell bent on making it happen....mass delusion because of voodoo economics IMHO.

Printing, well I think they and we will find they cannot print enough or fast enough to stop it....and the likes of Congress will block it...until its un-stoppable...yes yes I think they will fail.

Ever greater and more frequent stimulus, yes its the effect of the expotential function and can kicking.......the amounts will get bigger and more frequent until it blows anyway.

As PDK says this debt has to be paid back, or its in other words under-written by energy....which it clearly isnt. In that case the only outcome is default. The only Q is when....I sold all my shares 30months ago....a bit early it seems but thats OK, Im $s up and out.

regards

Did a certain house sell at Auction earlier this afternoon?

It did. Tell us for how much Bernard. What was that price growth during your shortish tenure??

Chris J - that one sold at public Auction on Wednesday for $1,005,000 versus the $617,000 originally paid for it in 2005 - that's a $388,000 tax free gain and 62.88% above original purchase price - not bad eh!

Hard to beat property as an investment over that same timeframe and even better if you used mortgage leverage to get into it in the first place.

Fix or Float? Bernard could be right 5.99% for 5 years sounds historically very cheap. trouble is its costing you 1% in the meantime compared to the best short term rates available. That's a very large price to pay.

My sense it's a bit too early to be fixing out at those levels, the NZ economy is not in good shape and I believe unemployment rates will surprise to the negative over the next 1 to 2 years. My pick is rates will be lower for much longer than anyone is expecting.

House prices going up is not really a big issue unless it drives more reckless debt expansion and consumption, and I just don't believe NZers have the appetite to increase debt and we probably all have enough TVs to last us for the next few years!

Float I say, enjoy these historically low rates and repay as much debt as you can.

yep, totally agree....

Historically is the past, the future will be different.......we have used more energy for 10,000 years now that reverses....paradygm shift.

Employment and wages I think will stagger along at best....just looking at the EU and the impact of that when it lets go is plain huge....

Stay floating, clear debt and sit, hold cash and cash like things, ie liquid....if it gets worse you wont be in the blood bath, wont experience the fear and distress as you get wiped out.....if it gets better you just miss a little on the greed.

regards

Float for the next 23 months and fix at low levels just before the 2014 election. Once LAB/GRN government is in power, interest rates are only going 1 way, that is up. Their combined policies are very inflationary. Bonds, under cost construction etc.

Now is the time for me to get into debt, get a $250K loan to add to my house, have 5% interest for 2 years and fix at 6% in late 2014. The size of the loan will soon be inflated away.

Olly Newman is wrong, house prices will quadrupal within 12 months of the LAB/GRN monster being in power.

Being involved in the construction industry via chemicals I am in a good position no matter what happens in 2014. My job is quite secure and a humming building industry will help keep my job secure. Only need to convince my Aussie masters to pay me more when the inflation takes off.

I think you are completely wrong.....Set a month....I will copy this into my callender and lets see how you do.......

I think the reverse....I will be surprised if the OCR is >2%....

We'll see it will be interesting to look back....

regards

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.