By Keith Woodford*

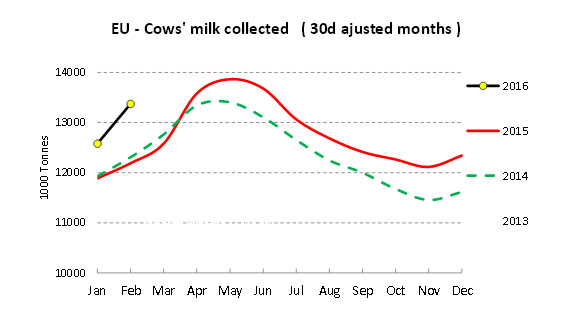

The EU has now released dairy production statistics for February 2016 and from a New Zealand perspective the news is all bad. Daily milk production has increased 6.5% from January to February. Some increase was expected – February is always higher than January on a daily basis – but the extent of the increase is a surprise.

The combined January and February production is up 7.4% from last year, and February production, once adjusted for the leap year, is up almost 10% on a daily basis from January last year.

There are some glimmers of hope in other parts of the world, and I will come to that later in this article. First, more about Europe.

Until now I had been hoping to see the EU production trajectory start to taper off relative to last year as from April, but that now looks less likely. It is now starting to look as if it could be later in the year before this tapering occurs, with the price recovery being further delayed after that.

Whereas some EU countries produce monthly data very quickly, Germany, France and some other countries take six weeks to get the numbers out. And without Germany and France in the mix, with these being the largest dairy producers in Europe, it is hard to determine the overall pattern. Hopefully by mid-June we will get a better feel as to where the current Northern European season is going.

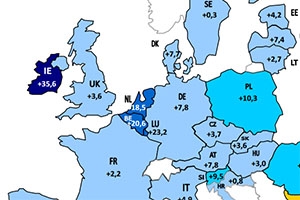

The production increases for January and February are driven by the ‘usual suspects’. Compared to the previous year, Ireland is up a massive 33%, Netherlands is up 16.5%, Germany is up 6.1% and Poland is up 8.6%. This is after adjustment for the leap year. Otherwise increases would be even greater.

Even worse from a New Zealand perspective, is that Europe is cranking up its production of whole milk powder (WMP) after holding back throughout 2015. Production in January is up 22% from the same months last year.

The reason for the increasing WMP is not because it is profitable, but rather because producing WMP is what companies do when they have no other outlet.

Production of skim milk powder (SMP) is also increasing, up 15% for January and February compared to the same months last year. SMP prices are awful, but the Europeans keep producing it because it is a by-product of butter, which remains one of the more profitable products.

Farm gate prices in Europe are drifting lower but are still about 40% above New Zealand levels. These European prices will keep coming down. However, spot prices for milk in some countries, such as the Netherlands, are only 0.17 euros per litre which is right down to NZ farmer payments.

The road ahead for Irish farmers could also be very rocky. They have a similar product mix to New Zealand, based off seasonal production, but with somewhat more value-add that New Zealand, They already receive considerably less than most EU farmers for their milk because of their powder-based seasonally-produced product mix.

It is only when looking beyond the EU that New Zealand farmers will see some glimmer of hope. Chinese global imports of WMP – not just from New Zealand – are up 22%.in the first two months of this year. SMP is also up by 25%. I am waiting eagerly to see March statistics which will give us a better indication going forward.

In a perverse way, the bad news coming out of Murray Goulburn in recent days will provide some relief for Fonterra’s Australian operations, and this will flow through to the Fonterra’s profits in New Zealand

Murray Goulburn is the farm gate price setter in Australia, just as Fonterra is in New Zealand. Murray Goulburn has had apparent success in rebranding itself as a value-add dairy company, but it seems the rhetoric eventually got in front of the reality. Both the CEO and the CFO have had to fall on their swords this week for being grossly over-optimistic in their forecasts, and now far too slow to revise them.

The latest news out of Murray Goulburn is that their market returns will now only support farmer prices of $A4.75 to $A5 per kg milksolids. Even before adding the exchange rate adjustment of about 10%, this is still a long way above what New Zealand farmers, apart from those supplying Tatua, will get this year. But Australian farmers had been told to expect at least $A5.60, or more than $NZ6 per kg milksolids, and there was no warning that the projection might be at risk.

Some months back, Fonterra’s Theo Spiering was strident in his criticism of Murray Goulburn, saying their farm gate price predictions were far too high. Well, on this one, history is showing he was indeed correct.

Murray Goulburn’s pain will now allow Fonterra to offer its own Australian farmers considerably less than otherwise. It won’t have a great effect in the current year which is drawing to a close, but on a 12 month basis it has the potential to raise net cash flows from Fonterra’s Australian operations by more than $NZ100 million. Of course this will flow to Fonterra’s profits and dividends, not to the milk price. So farm owners and unit shareholders will benefit but not sharemilkers.

Here in New Zealand, the January to March production has held right up to previous years, despite some media reports to the contrary. Yes, Fonterra is down, but the rest of the industry is overall up. For most, it has been a marvelous summer and autumn, with plenty of sun and just enough rain.

Overall New Zealand production for the total season is now down only 1.7% – a much smaller drop than many reports relying on Fonterra data have been indicating. But next season, unless we get another year of bountiful weather, and with reducing cow numbers from the current seasonal cull, overall production is likely to be down something more than 6%.

Keith Woodford is Honorary Professor of Agri-Food Systems at Lincoln University. He combines this with project and consulting work in agri-food systems. His archived writings are available at http://keithwoodford.wordpress.com

8 Comments

Interesting and concerning, thanks

The EU-28 has recently obtained an increased market share of Chinese dairy imports at the expense of New Zealand, among other areas, incentivizing European producers to continue to produce at current strong output levels.

http://www.attenbabler.com/chinese-dairy-trade-partners-apr16/

http://www.attenbabler.com/eu-28-milk-production-update-apr-16/

I still can't believe how everyone in the NZ dairy industry was so unaware of the potential of farmers in the northern hemisphere to increase their production.

Not to mention how we thought that China would just keep buying our dairy products without question, which has proven to be a foolish assumption as Andrew Js links show.

People don't see danger until it is imminent.

In desperate need of a weaker exchange rate.

http://www.independent.ie/business/farming/milk-prices-to-fall-further-…

What if the problem is not the exchange rate but the fact that land prices in NZ are so expensive despite being once cheaper than in France, Spain, etc.?

A lower exchange rate will not help. You would have to lower interest rates here which would encourage more debt and help farmers keep up production,isn't oversupply is the problem?

Yes it will. It will make the farmers product more competitive at auction and give farmers a level playing field as far as debt servicing goes. Over supply is the issue but when your competition is ramping up production (as mentioned on the site 2 days ago) cutting your production just cuts your market share.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.